Weekly recap - Macro deterioration, topping pattern (?), weak PMI

House view:

- Stocks:

- Short-term: Modestly bearish. A compressed VIX during this time of year consistently preceded weak returns, as did Julys with numerous new highs in the S&P 500 and Nasdaq Composite. Robust earnings have been met with a churning market, with multiple fades from emotional gaps up. SPY gapped up at the open (a sign of emotional trading) 18 times out of the past 19 days, activity seen only twice before (1997-02-11 and 2018-01-05), leading to a bit more upside then declines over the next month or so. This time frame covers 1 - 4 weeks.

- Intermediate-term: No view. Momentum is ebbing, but from extremely strong levels. Breadth has been increasingly suspect (especially on the Nasdaq) but that, too, follows a spate of excellent readings from April and May. Positive earnings haven't led to much sustained upside, and gap-up opens haven't seen much follow-through. Speculative trading activity is bumping against historical extremes and valuations by nearly any metric are at or near multi-decade ceilings. This is a tug-of-war that shows no clear edge. This time frame covers 1-5 months.

- Long-term: Bullish. The recovery from the April panic has been historic, and signs since then have supported a long-term bullish move, with primarily economically sensitive sectors leading. Long-term breadth measures have improved across sectors and world markets, which have consistently preceded positive 6-12 month returns in most equity indices. This time frame covers 6-12 months.

- Cyclical momentum tends to favor those sectors for average returns

- Defensive sectors also doing well, with momentum favoring high win rate but lower average return

- Very long-term (one year+) favors mean reversion to equal-weight, small-caps, and health care

- Bonds: Long-term cycles remain bearish. Historically, August has been one of the strongest seasonal months for TLT, but since the 2020 peak, it's been one of the weakest. That leads into September and October, which are traditionally weak. We haven't seen much among analysts' studies to suggest a change in trend.

- Commodities: Signs point to a probable secular bull market following multiple new highs. An effective commodity trend model is currently bullish. Gold (especially gold miners) and silver are extended and have a bad history of sustaining gains but gold continues to shake that off and hit new highs. Oil seasonality is especially weak for the next three months.

- Crypto: We follow several simple systems for bitcoin, which we consider the equivalent of the S&P 500 for crypto. Due to bitcoin's explosive growth over long periods, it's dangerous to equate neutral conditions with being bearish for some of these. However, if a system is "out," we consider it bearish for this summary.

- Triple 40: Bullish

- RSI Momentum: Bullish

- Trend and Relative Trend: Bullish

- PMI: Bearish

- M2 ROC: Bullish

Where we're at

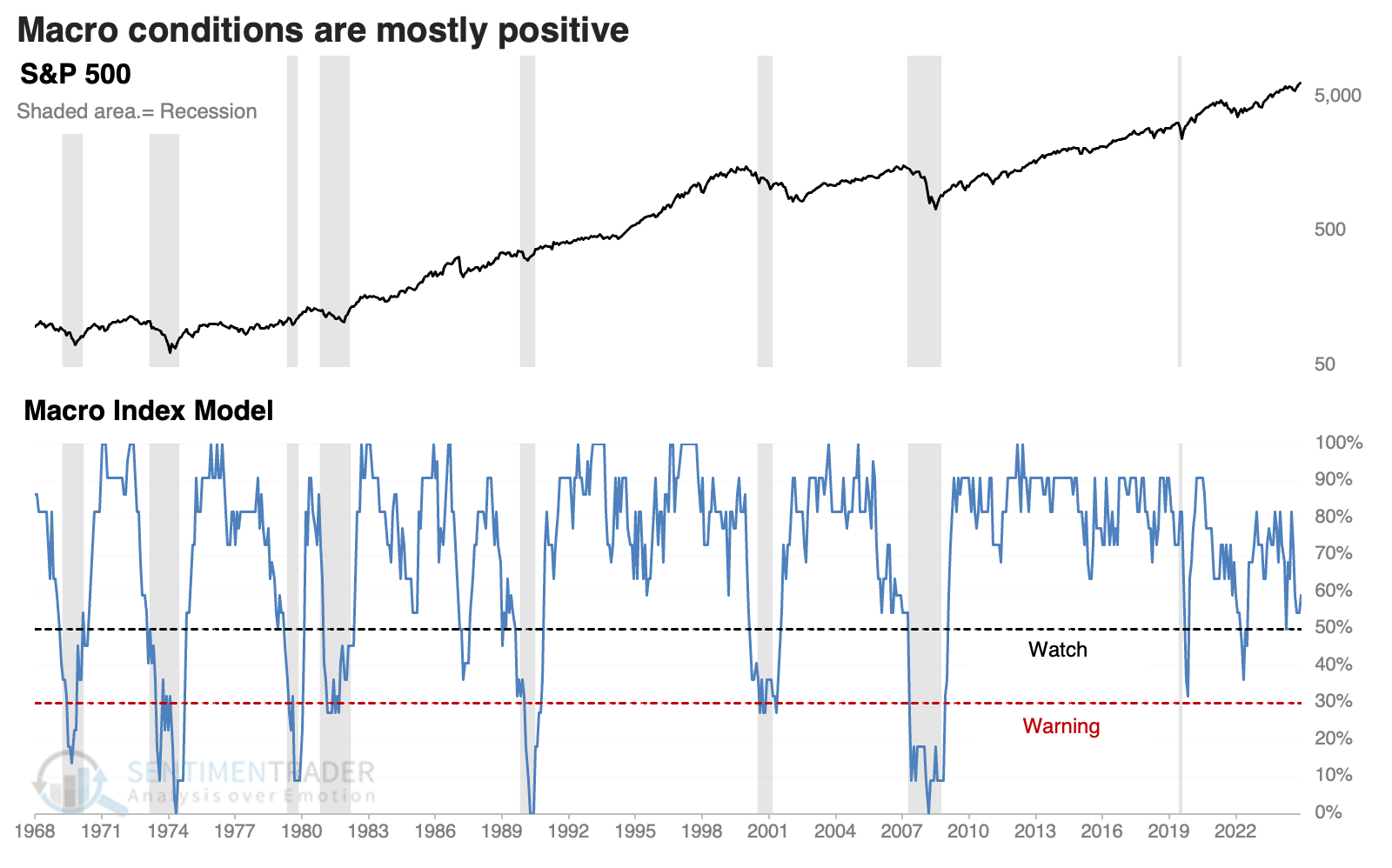

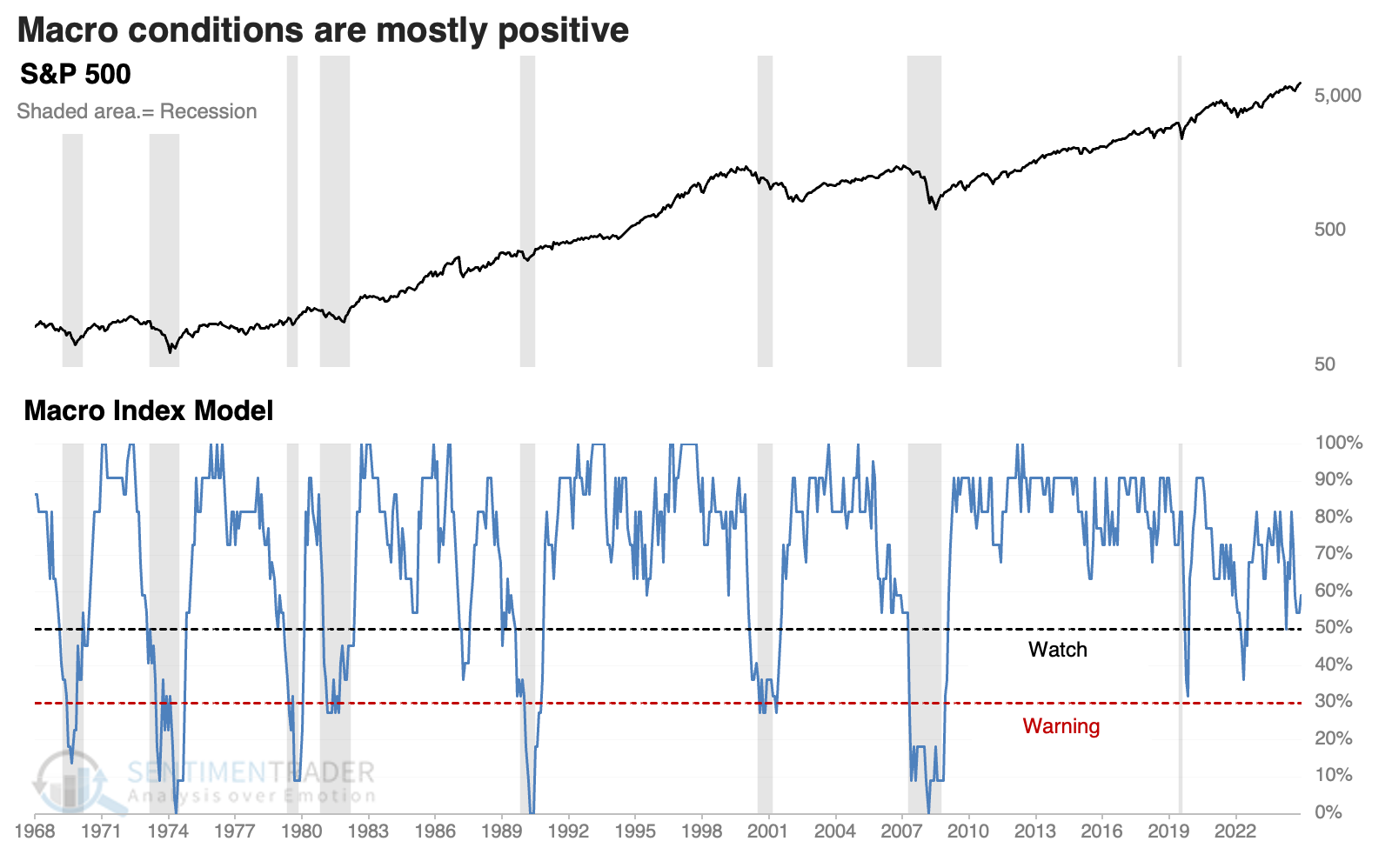

Currently, only scattered evidence suggests that the U.S. economy is in or in imminent danger of recession, lessening the threat of a deep and protracted bear market.

Our core model for determining that is the Macro Index Model. IMPORTANT NOTE: We've found an error in the chart's calculation on the website, and the team is correcting it. It is above the 50% threshold, which has been a vital level as outlined here.

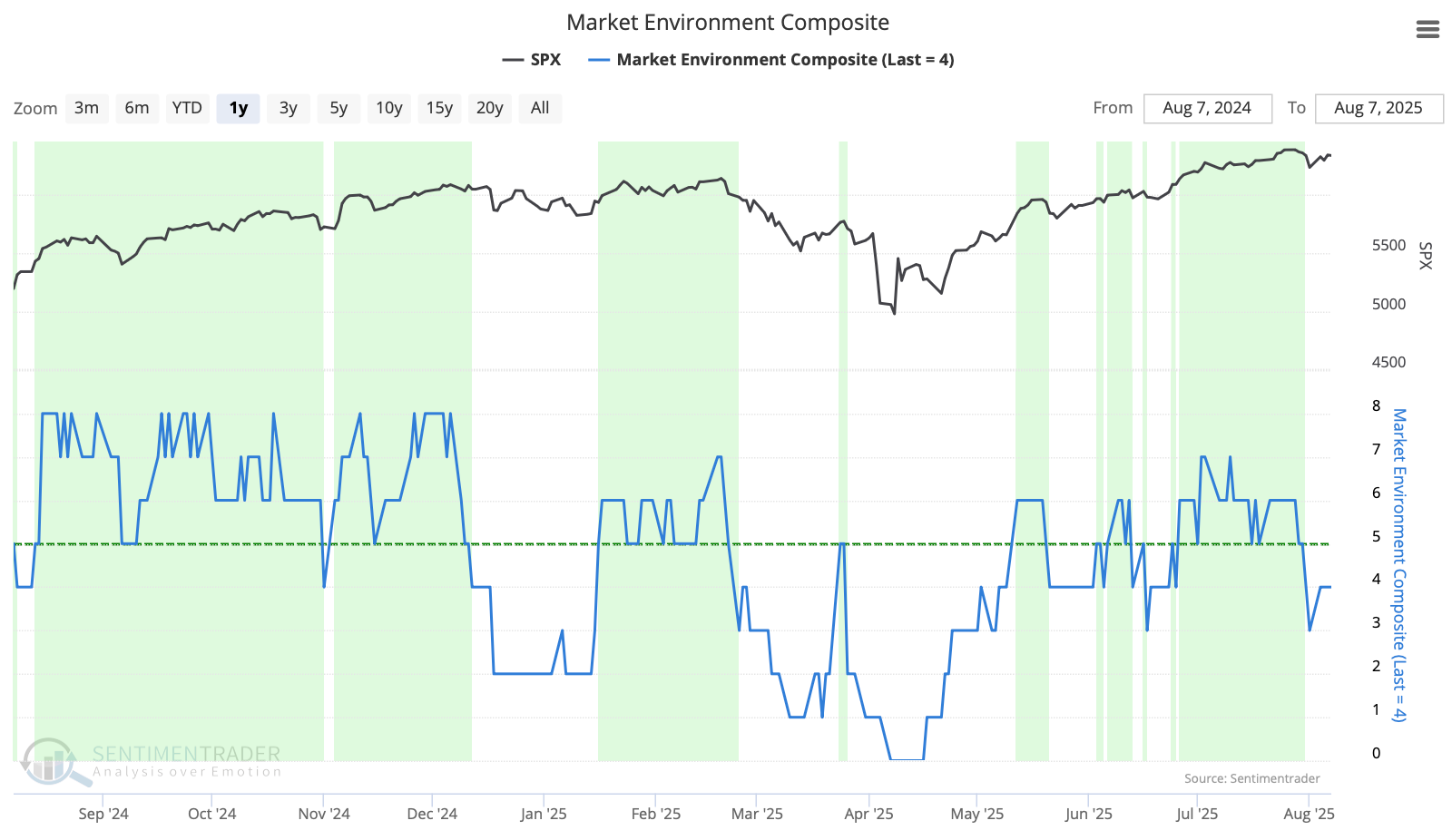

The Market Environment has been a little skittish since the April low, and has flipped back to unhealthy. The rockiest patches have occurred when the environment was unhealthy (the unshaded sections on the chart). Future returns, especially for higher-beta indices, has been markedly better, with less risk, when the environment is healthy as outlined here.

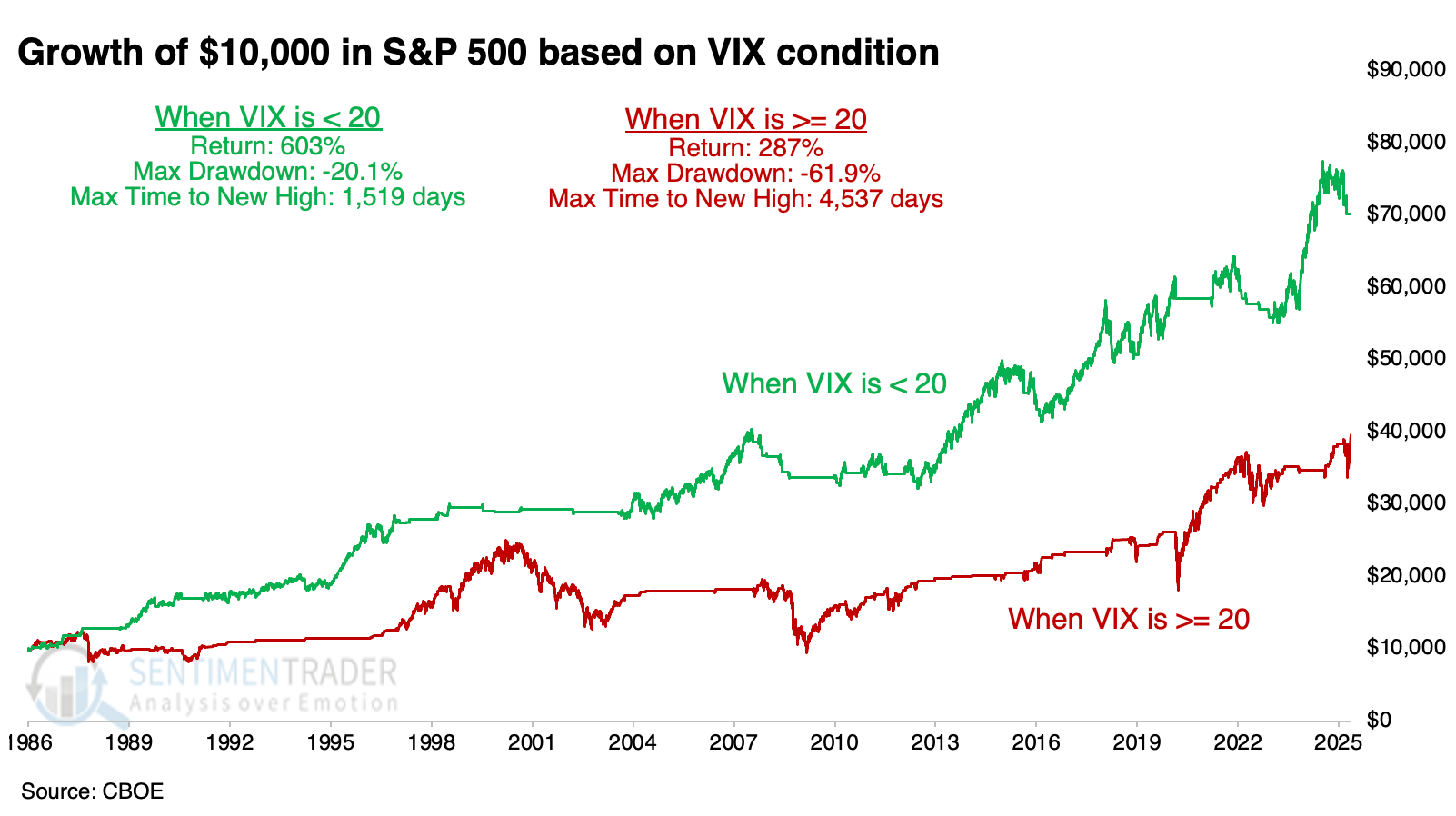

While not part of the Market Environment Composite, it is important to note that volatility is not spiking. As shown below, the S&P 500 shows markedly better characteristics when the VIX is below 20. It climbed above that last week, but only for one session and quickly dropped back below, so that's a positive.

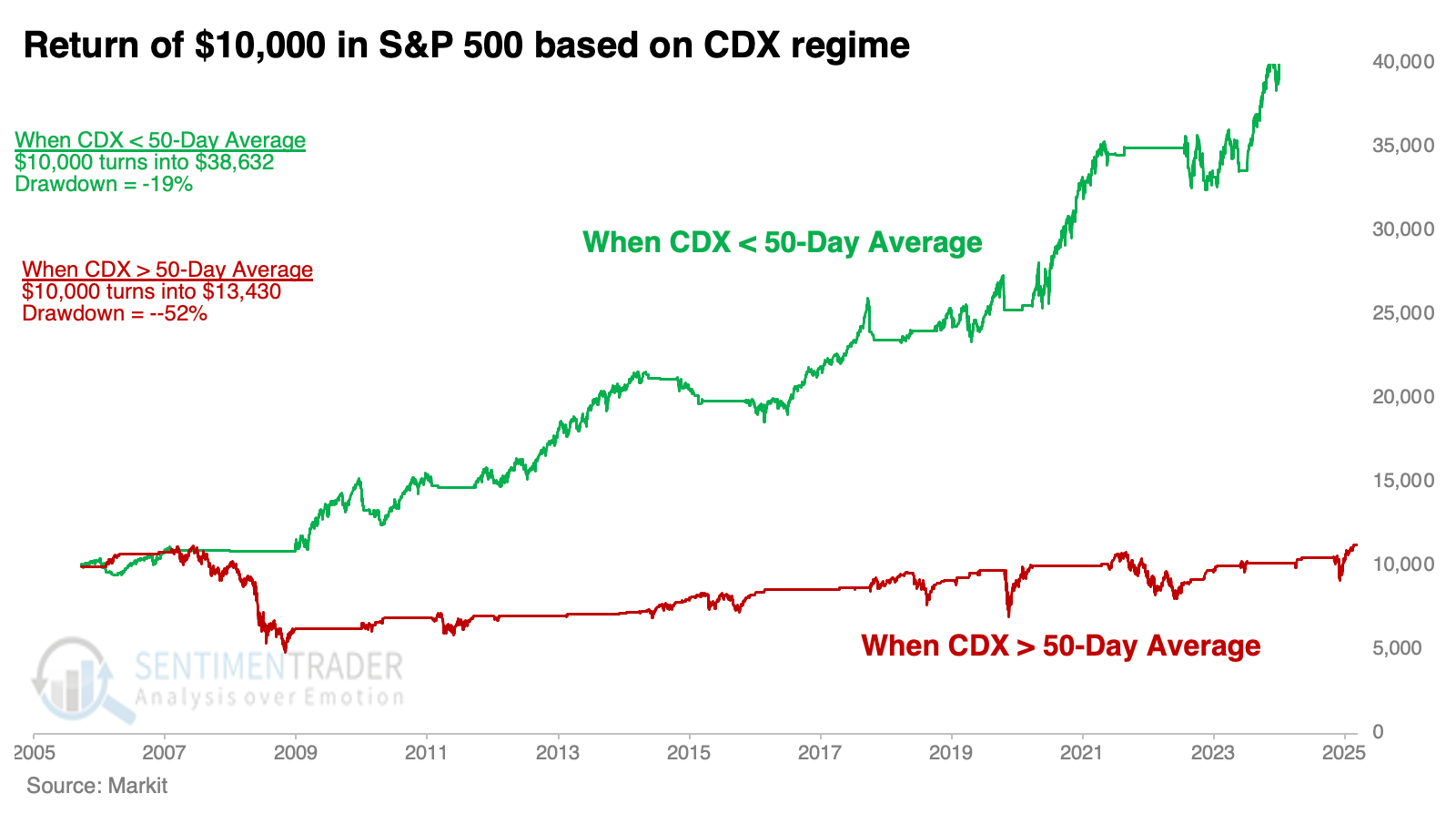

Credit default swap spreads are flirting with their 50-day moving average, which drastically impacts stock returns as outlined here. When the CDX Index is below its 50-day average, the S&P 500 has performed well. The index has now climbed above its 20-day average and is just below its 50-day average, a modest worry.

Since April, the most compelling studies have had a strongly bullish bias on longer time frames. You can follow these through the Active Studies page. From time to time, when the analysts' studies provide an overwhelming message, it will override whatever the Market Environment suggests. The bullish studies have been sporadic on short- and intermediate-term time frames, so they don't give an overly compelling reason to override an unhealthy market environment.

What we covered this week

Deteriorating macro conditions

Macro conditions in the U.S. are okay. But they're not great, and the Macro Index Model suggests they're in imminent danger of eroding to unhealthy levels.

We look for significant macro deterioration to differentiate temporary slowdowns from real problems. Our Macro Index Model combines 11 diverse economic indicators to determine the state of the U.S. economy. It is constructed as an inverse of recession probability. So, you can subtract the model from 100% to get the recession probability in the months ahead.

If the model was above 50%, there was only a modest 6% probability of a recession within the next six months, but a 73% probability if it was 50% or below.

Most investors are just as concerned with stock returns, and we can see that those also vary greatly. The worst regime - the danger zone - was between 21% and 30%. These were the months when the economy was almost certainly in recession, but hadn't been long enough for conditions to be washed out.

The best regime for average returns was just above that, from 31% to 40%. That's because stocks often surged when coming out of a recession. The next-best was when the model was above 70%, when most economic indicators suggested an economy chugging along.

Breakout meets selling pressure

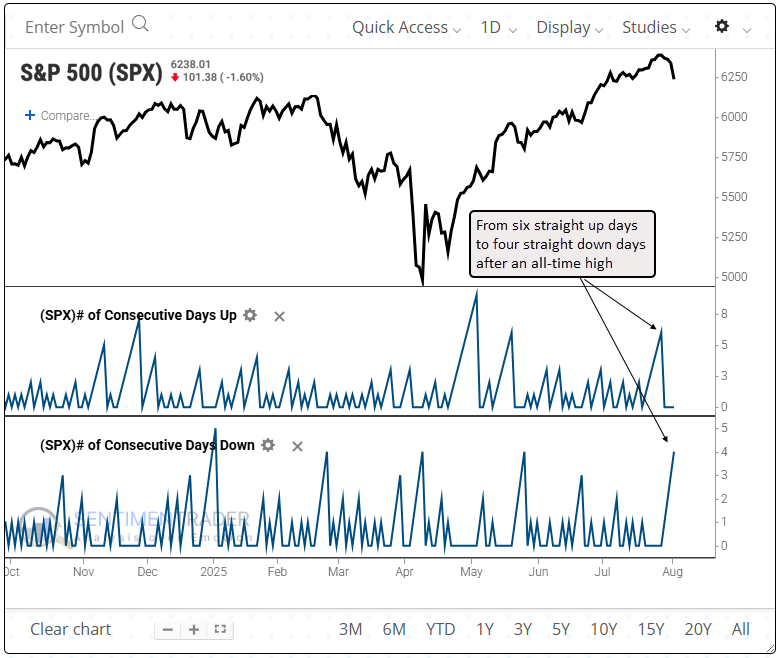

Stocks' most recent breakout was met with persistent selling pressure.

Last Friday, the world's most benchmarked index logged its fourth straight daily decline from an all-time high. The pullback follows six consecutive record closes.

Whenever the S&P 500 saw four up days in a row followed by four down days after hitting a record high, it typically bounced back, rallying 78% of the time over the following three and four months. Moreover, the 1990 precedent was the only case aligned with a significant market top.

While it's unlikely this pattern represents the start of a correction, given the coin flip win rate at the two-month mark and unfavorable seasonality, one cannot rule out some choppy price action in the next few months. Within the following four months, the S&P 500 experienced just four maximum losses exceeding 5%, and only one surpassed a 10% drop.

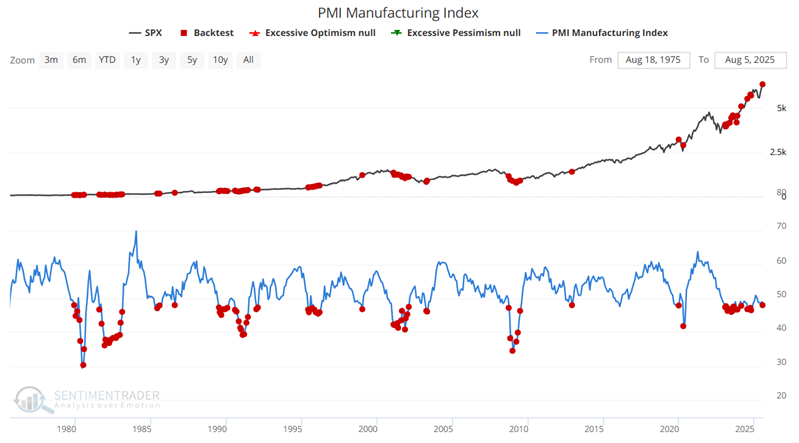

A contrary take on economic data

We've repeatedly been told that the economy is not the stock market. And yet, many investors continue to confuse the two.

Both stocks and the Purchasing Managers Index (PMI) are economic indicators. A PMI number over 50 indicates expansion, and under 50 indicates contraction. Investors instinctively prefer a strong PMI, which indicates a strong economy. The stock market, however, tends to take a slightly different view.

Most investors instinctively expect below-average stock market performance following lower PMI readings. In reality, the S&P 500 performed strongly after a PMI below 48, with a median gain of over 20% during the following year.

Even though returns following high PMI readings were positive, the S&P 500 showed a higher average return following low PMI readings than high ones and was more consistently positive.

We also looked at a system that buys the S&P 500 the first time PMI drops below 48 and holds the index for one year.

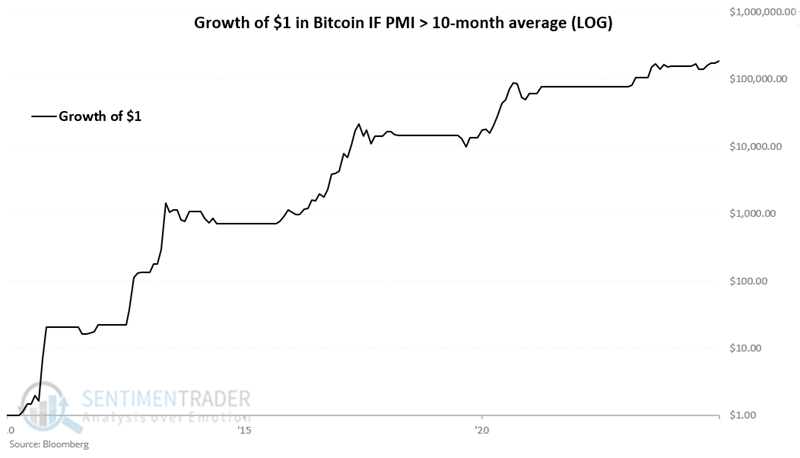

Using econ data for bitcoin

Instead of the usual technical tools, investors can use economic data to help decide how much to allocate to the relatively new crypto asset class.

The Purchasing Managers' Index (PMI) is a key economic measure of the health and direction of the United States' manufacturing sector. A reading above 50 indicates expansion or growth in the manufacturing sector. A PMI reading above the 10-month average is considered favorable for bitcoin, while a reading below is neutral. As of the August 1st report, PMI is below its 10-month moving average, so it is presently neutral for bitcoin.

Below, we see the growth of $1 invested in bitcoin when the PMI Index was above its 10-month average. The cumulative hypothetical gain is an astounding 18,732,032%.

Investing only when the PMI Index was below its 10-month average gained 913%. That's still impressive relative to other assets but includes some massive drawdowns, and the equity curve is no higher now than in mid-2011.

Real M2 is the U.S. Federal Reserve estimate of liquid assets. We are more interested in M2's rate of change than its raw value and we're even more interested in whether the rate of change is increasing or decreasing. It is currently increasing.

The PMI Index and M2 indicators presented here should be viewed as weight-of-the-evidence indicators, not automatic trading systems. They show promise as inputs typically outside of what other investors are using. Currently, PMI is neutral for bitcoin, while M2 is favorable, so crypto investors may want to watch the latest releases to see how this may change for the coming month(s).

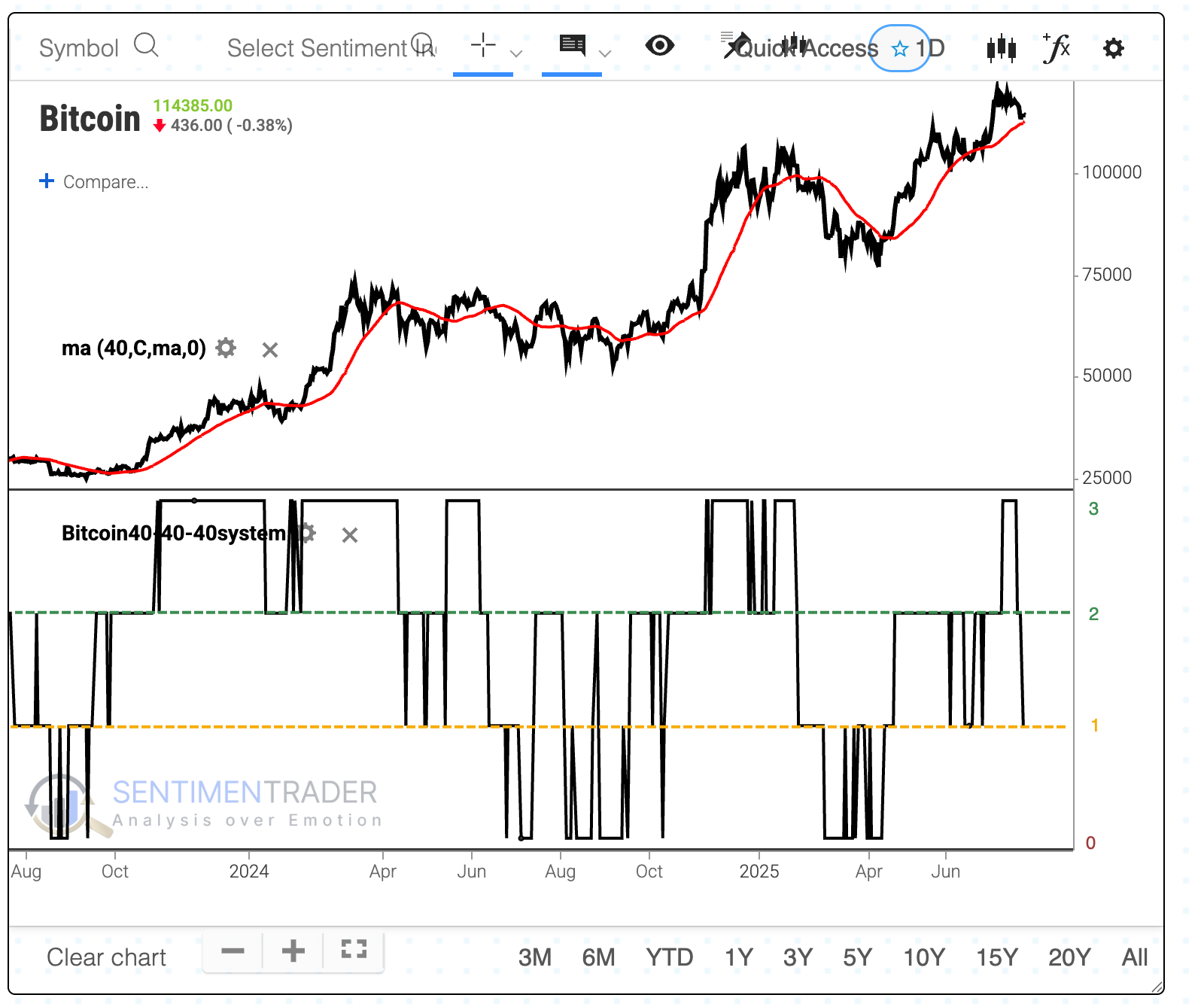

Bitcoin Triple 40 system

As cryptocurrencies become a more viable investment vehicle, demand is growing for exposure to the asset class but some protection from its notorious swings. To keep things as simple as possible, we'll focus on one measure each of price action, sentiment, and breadth within the crypto space.

We can combine the three factors into a Triple 40 system:

- Bitcoin is above its 40-day moving average

- At least 40% of traders are bullish

- At least 40% of cryptocurrencies are above their 200-day averages

This is shown in the chart below, with the system receiving 1 point for meeting each of the conditions.

Using these parameters, $10,000 would have turned into $543,000 when at least two factors were bullish. That's more than 4x a buy-and-hold return, while suffering less than half the drawdown.

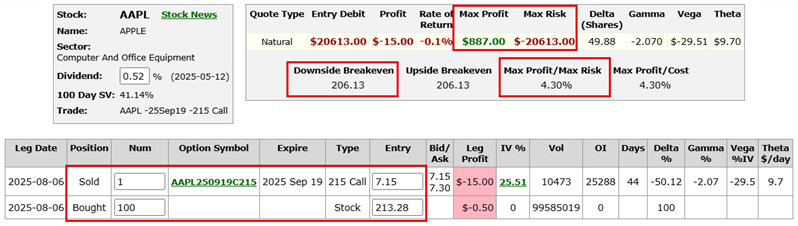

Covered calls

At a bare minimum, a covered call position involves holding 100 shares of stock and selling a call option against those shares.

If the call option sold expires in the money, meaning the stock price is above the option strike price, the call option will be exercised, and the 100 shares of stock will be called away from you at the option strike price. You get to keep the option premium received.

Some proponents of covered call writing refer to covered calls as "free money." And if a particular covered call expires worthless, then, yes, technically, it amounts to free money. But this naïve viewpoint completely ignores the risk versus reward tradeoffs involved. Let's illustrate this in a straightforward example.

On the plus side, if AAPL shares are below $215 at September option expiration, you keep the $715 premium as income. But please look at the complete reward-to-reward profile I've shared below. The colored lines on the right-hand side represent the expected dollar gain or loss for the net position as of a given date, leading up to option expiration on September 19th, 2025.

Intraday Minutes

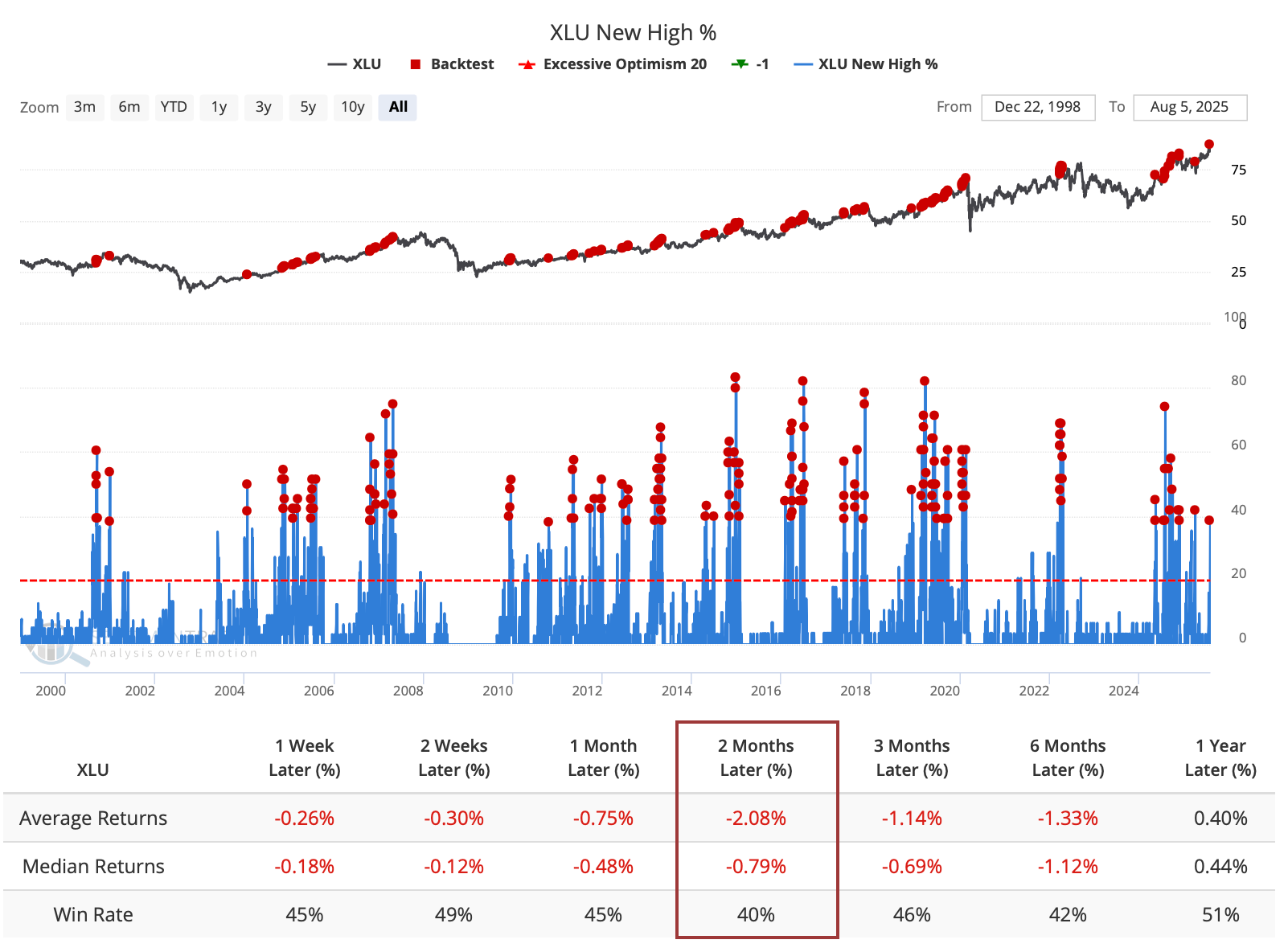

In the "unofficial" stream of intraday minutes, we looked at how utilities tend to struggle after many of them surge to new highs.

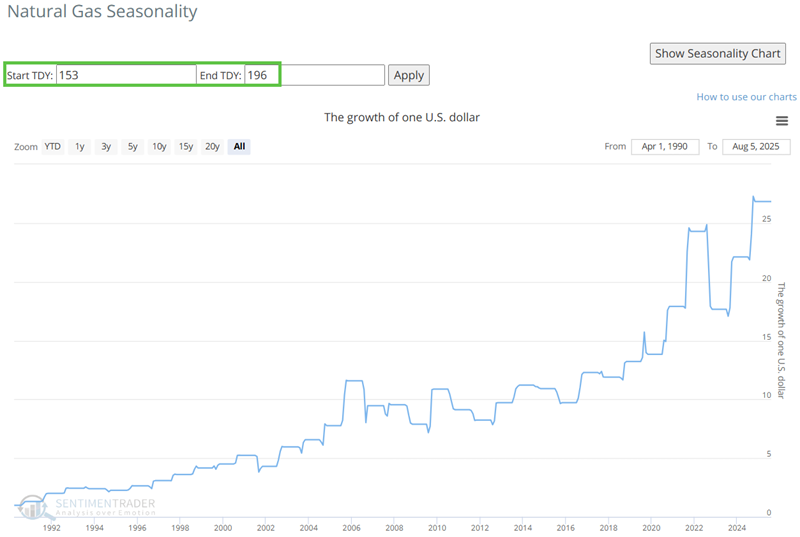

We saw that natural gas has a seasonal tendency to rise this time of year.

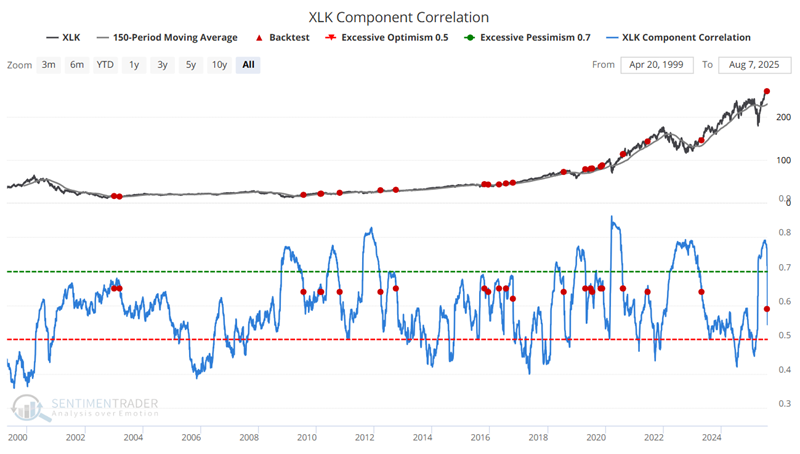

Correlation among tech stocks has cratered.

About TradingEdge Weekly...

The goal of TradingEdge Weekly is to summarize some of the research published to SentimenTrader over the past week. Sometimes there is a lot to digest, and this summary highlights the highest conviction or most compelling ideas we discussed. This is NOT the published research; rather, it pulls out some of the most relevant parts. It includes links to the published research for convenience, and if you don't subscribe to those products, it will present the options for access.