Thoughts on the covered call strategy

Key points:

- Covered calls offer a stock investor the potential to generate income

- However, they can also limit upside potential while only minimally hedging against risk

- The key is to understand the tradeoffs involved and develop a coherent strategy

The basics of covered call writing

At a bare minimum, a covered call position involves holding 100 shares of stock and selling a call option against those shares.

If the call option sold expires in the money, meaning the stock price is above the option strike price, the call option will be exercised, and the 100 shares of stock will be called away from you at the option strike price. You get to keep the option premium received.

If the option expires out-of-the-money, meaning the stock price is below the option strike price, you keep the option premium and still retain your 100 shares of stock.

Some proponents of covered call writing refer to covered calls as "free money." And if a particular covered call expires worthless, then, yes, technically, it amounts to free money. But this naïve viewpoint completely ignores the risk versus reward tradeoffs involved. Let's illustrate this in a straightforward example.

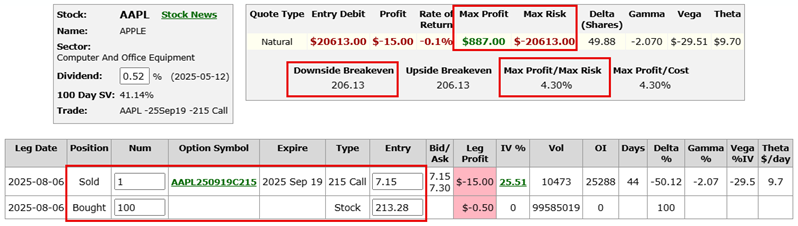

If you buy 100 shares of Apple (AAPL) at $213.28 and sell a September 2025 AAPL 215 strike price call for $7.15, you pay $21,328 to buy the shares and receive $715 for selling the call option. So, the net cost is $20,613 (all screenshots courtesy of Optionsanalysis.com).

On the plus side, if AAPL shares are below $215 at September option expiration, you keep the $715 premium as income. But please look at the complete reward-to-reward profile I've shared below. The colored lines on the right-hand side represent the expected dollar gain or loss for the net position as of a given date, leading up to option expiration on September 19th, 2025.

If you sell one covered call for every 100 shares of stock you hold, your upside profit potential is completely limited to:

- (Strike price + premium received - price paid for stock shares) x number of shares

In this example, no matter how high AAPL shares might rally, the maximum profit potential for this covered call example is $887:

- (215 + 7.15 - 213.28) x 100

On the downside, the positive is that the premium received reduces the breakeven price from $213.28 to $206.13. However, below that price, downside risk remains unlimited. To this analyst's eye, this is not an appealing reward-to-risk profile for my $20,613 investment.

How can we improve the trade-off? Two things come to mind. First, we can sell out-of-the-money options - a call option with a strike price above the price of the underlying stock - which reduces the likelihood of having our shares called away and allows time decay to work in our favor. Second, we can avoid selling options against our entire stock position. This will enable us to retain unlimited profit potential.

Developing a strategic approach

The first thing to know about covered call writing is that there is no best approach. There are many possible approaches, including:

- If you have a target price in mind at which you intend to sell your stock shares anyway, it makes perfect sense to sell a covered call with a strike price at or near that level. If your target price is reached, you can sell your shares in addition to collecting an option premium

- If you don't mind having your stock called away, selling at-the-money or in-the-money calls can make sense to receive more premium than selling an out-of-the-money call

- If you want to sell calls to generate income but prefer not to sell your shares, then selling out-of-the-money calls makes the most sense. In addition, selling fewer than the maximum potential number of calls can leave you with unlimited profit potential

This note will pursue the last approach to covered call writing.

The out-of-the-money approach

Let's set a couple of subjective guidelines. We want to sell covered calls to generate income from stock shares held. However, we hope that the call options we sell will expire worthless and that we will retain our stock shares and keep the income. Likewise, we would like to have unlimited profit potential. As a result, we will set the following rules:

- We will sell call options with a delta below 30, meaning they are well out-of-the-money

- We will sell call options with 7 to 45 days left until expiration

- We will sell fewer than the maximum number of possible call options, which requires holding at least 200 shares of stock for each call option sold

An at-the-money call option typically has a delta of about 50, suggesting a roughly 50% chance of expiring in the money. Therefore, a call with a delta of 30 or less has a higher probability of expiring worthless since it has only a 30% probability of expiring in the money.

Selling call options with 7 to 45 days gives us the potential to have time decay work strongly in our favor, as options, particularly out-of-the-money options, lose most of their time premium in the last 30 days before option expiration.

If we hold 400 shares of stock, we might sell two call options, but we could sell anywhere from one to four calls. If the stock rallies above the strike price, we could have 200 shares called away, but we would still have unlimited profit potential with the other 200 shares.

When to sell covered calls

The reality is that there is no best time or set of circumstances for deciding when to sell covered calls on shares you hold. But specific guidelines can make sense.

For example, assume that on August 6th, we hold the 20 stocks with the highest option trading volume. We will consider selling covered calls when the 3-day RSI has been above 65% at least once in the last five trading days. The theory is that the stock may be overbought and due for a short-term pullback. That short-term pullback may offer an opportunity to capture option premium.

Five stocks qualify on August 6th: AAPL, INTC, GOOGL, BABA, and META.

We will use the following filters:

- Days to option expiration: 7 to 45

- Minimum Sell Bid: $0.125

- Option Volume > 20

- Option Open Interest > 100

- Option Delta < 30

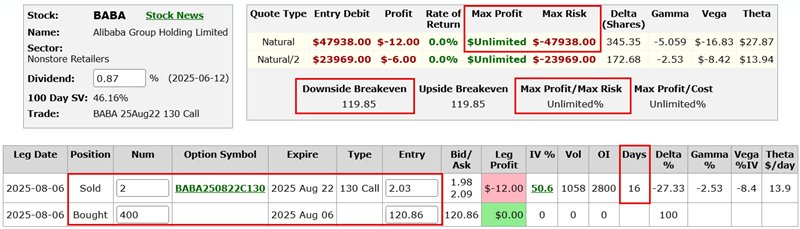

Using these settings, I found an opportunity to sell the BABA August 22 130 call for $2.03 per option. BABA shares were trading at $120.86, so this option was 9.14 points (about 8%) out of the money.

For our example, we will assume that we hold 400 shares of BABA stock and sell two call options. By selling two call options at $2.03 each, we receive $406.

Be prepared for what happens next

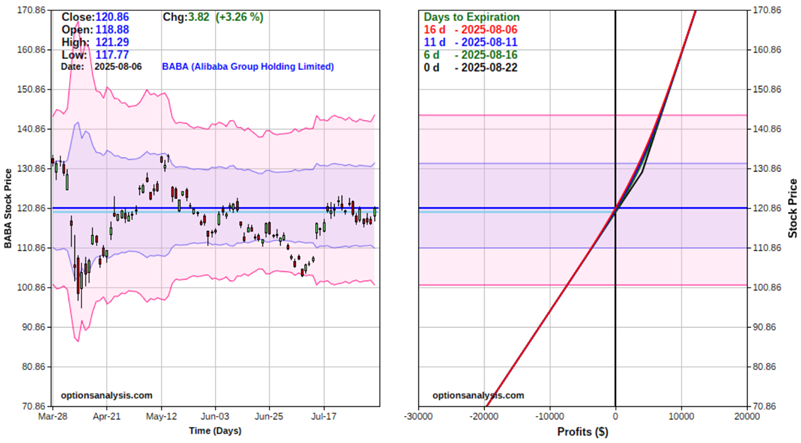

BABA was trading at $120.86 a share, so our 400 shares are presently worth $48,344. We sold two calls at $2.03, and have received $406 in income. There are sixteen calendar days left until the calls we sold expire. From here, one of three things will happen.

If BABA rallies above $130:

The calls may be exercised before option expiration. If held until option expiration, they will automatically be exercised. If the calls are exercised at $130 a share, we will be compelled to sell 200 shares at that price. This generates a profit of $1,828 on the 200 shares that get called away (130 strike price - $120.86 x 200). We also keep the $406 premium received when we sold the calls. We also continue to hold the other 200 shares of BABA stock.

If BABA remains below $130:

We retain 400 shares of BABA stock and $406 in premium. We could sell more covered calls against our BABA stock shares to generate additional income.

You are not required to hold the call position through option expiration. Some investors might close their covered call positions if the options' price declines 50% to 75% before expiration. Also, if the stock price rises towards the strike price and you decide you don't want your stock shares called away, you can buy back the calls before expiration. In the case of a stock price rise, you may end up buying back the calls at a higher or lower price than you sold them for, depending on how far and fast the stock rises, and how much time decay has affected the option price.

What the research tells us…

Covered call writing is one of the most popular and often used option trading strategies. However, most investors fail to consider the risk and reward trade-offs involved. The approach detailed here allows an investor to generate income from their stock portfolio while also not completely limiting upside potential.