Market & fundamentals overview: the overdue pullback?

After rallying nonstop for weeks and weeks, the S&P 500 finally came close to its -1% day (on Friday) for the first time in months. Is this the start of the long anticipated pullback? While it's impossible to know for with 20/20 hindsight (there is no holy grail in the markets), short term bearish evidence continues to mount. Here's my market outlook:

- Long term risk:reward (e.g. 1-5 year basis) doesn’t favor bulls. Valuations are high, but valuations can remain high for years before stocks crash.

- Fundamentals (6-12 months): still bullish because there is no significant U.S. macro deterioration.

- Technicals (1-3 months): bearish

Fundamentals (6-12 months)

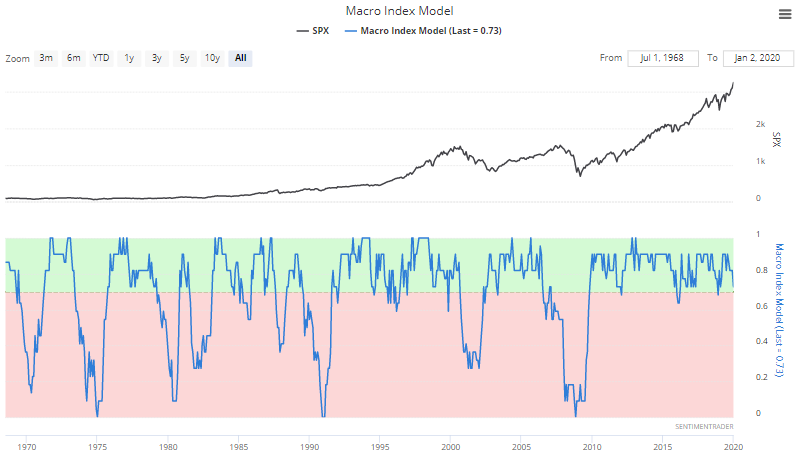

The economy and the stock market move in the same direction in the long term. Hence, leading economic indicators are also long term leading indicators for the stock market.

Overall, there is no significant U.S. economic deterioration right now. This is bullish for the stock market on a 6-12 month time frame. The main weak points in U.S. macro revolve around trade, manufacturing, and the yield curve. For more details and charts, please see the bottom of this post.

Technicals (1-3 months)

Our outlook over the next 1-3 months is bearish. Momentum is strong (more useful 6-12 months later), but sentiment is extremely high (more useful 1-3 months later). Let's start with the bullish stats, and then we'll work our way to the bearish ones.

Mixed:

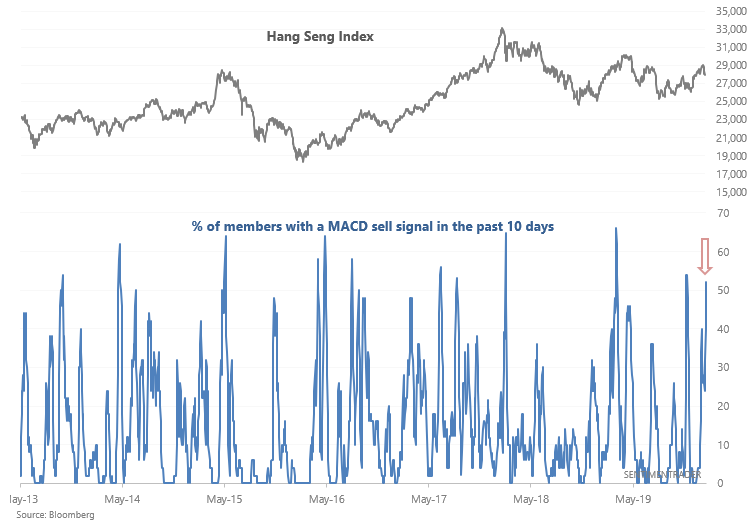

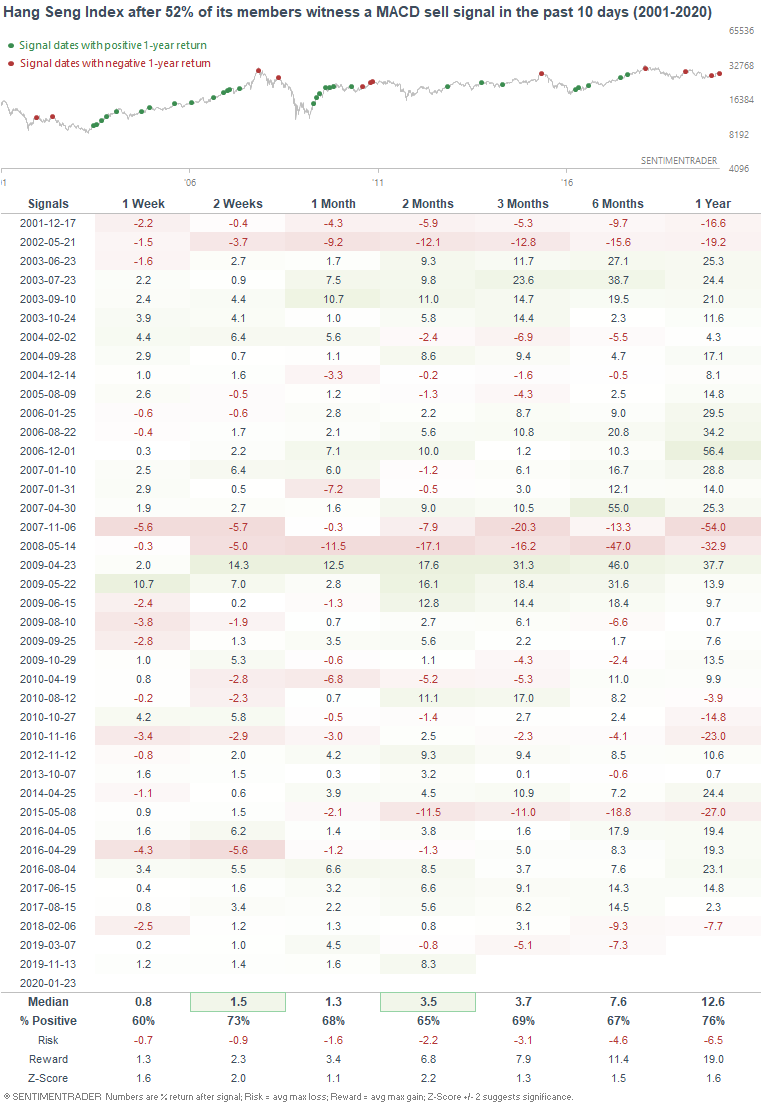

As global stocks faced pressure this week, 52% of the Hang Seng Index's members witnessed a MACD sell signal in the past 10 days:

While it's easy to automatically assume that this is a bearish sign for Hong Kong equities (and some financial marketers may try to convince you so), that hasn't always been the case. When this happened in the past, the Hang Seng Index increased more often than not over the next few weeks.

With that being said, let's dig into the market's overwhelming short term bearish bias.

Bearish:

Price pattern

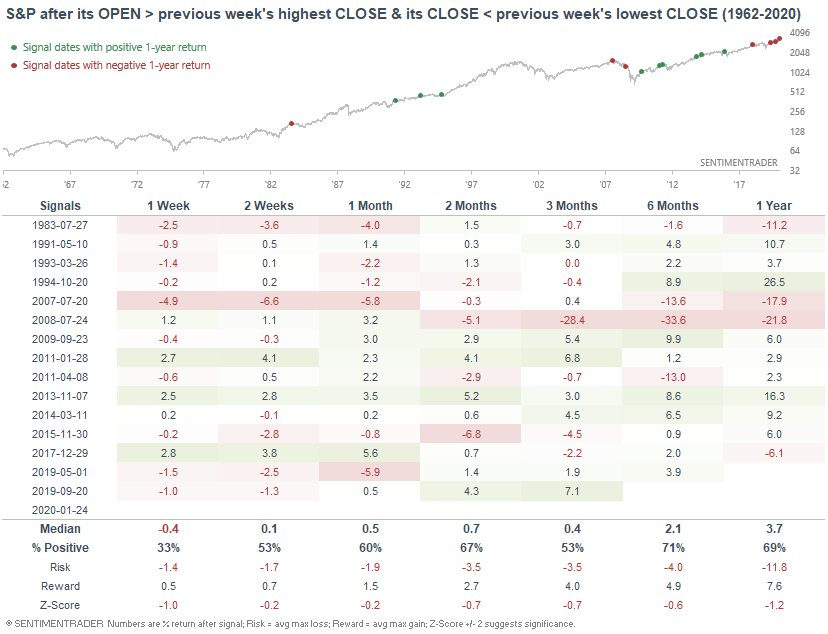

From a price pattern perspective, the S&P gapped up on Friday and fell throughout the rest of the day. As a result, the S&P's OPEN on Friday was above its highest close over the past 5 days, and its CLOSE on Friday was below its lowest close over the past 5 days:

This reversal pattern often led to short term weakness over the next week:

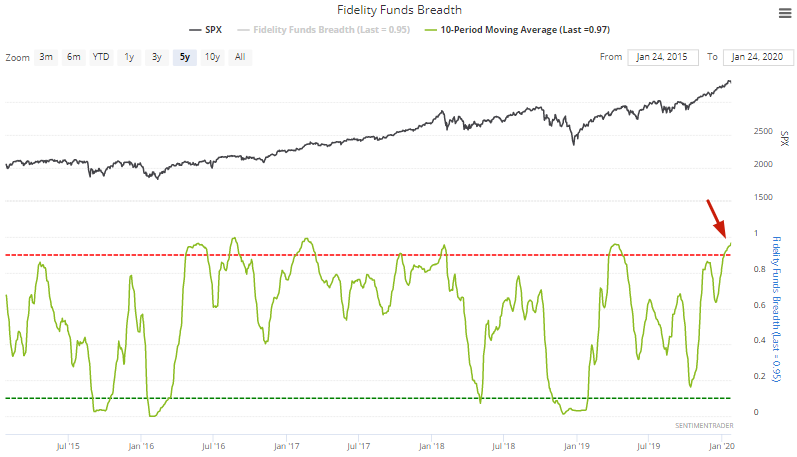

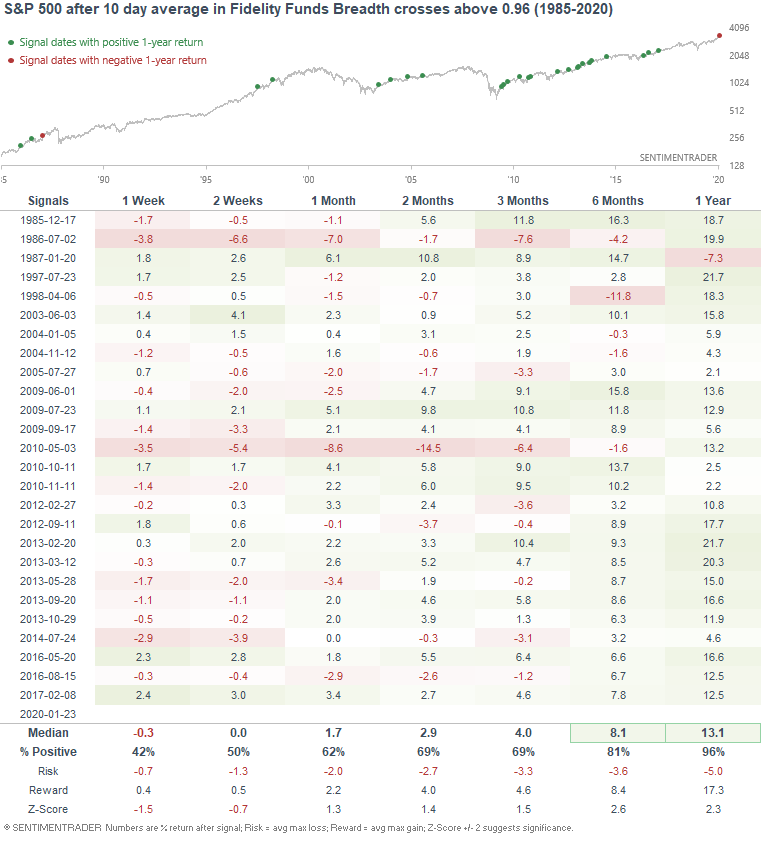

Breadth

The 10 day average of our Fidelity Funds Breadth indicator, which tracks the % of Fidelity Select mutual funds whose returns were better than short term Treasury Bills over the past 3 months, is extremely high. This is to be expected considering the rip-roaring rally over the past few months:

When the 10 day average for this breadth indicator became extremely high, the S&P's returns over the next 1-2 weeks were slightly worse than random. But from a longer term perspective, this usually led to more gains 6-12 months later. Extremely strong breadth & sentiment are hallmarks of bull markets:

Contrarian

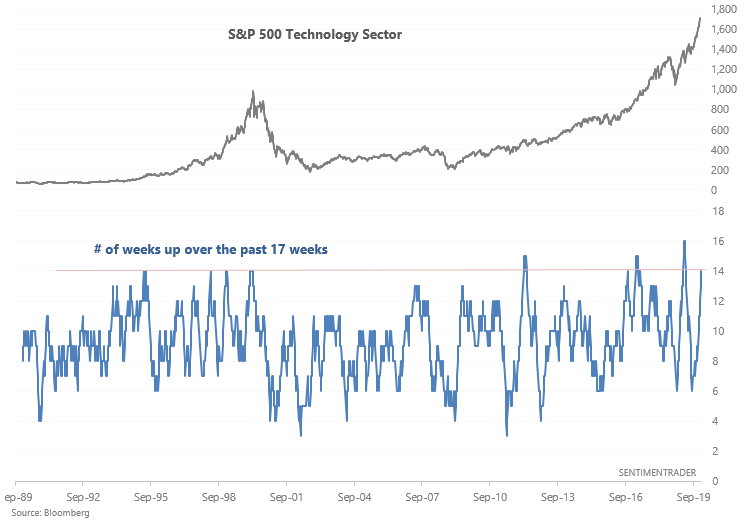

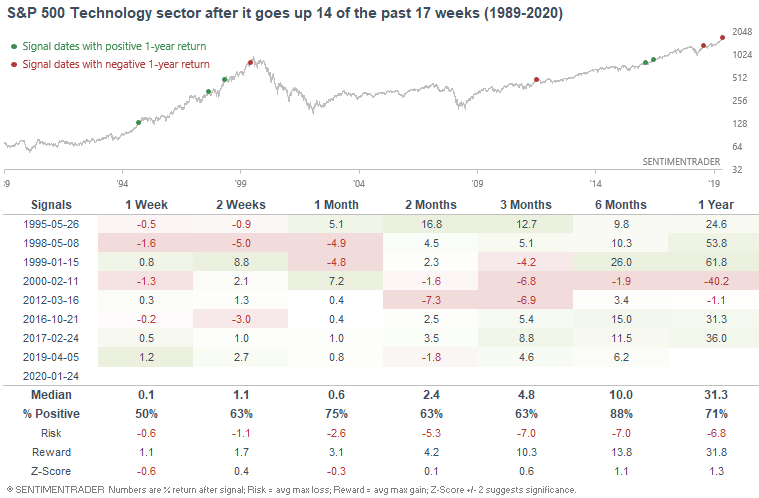

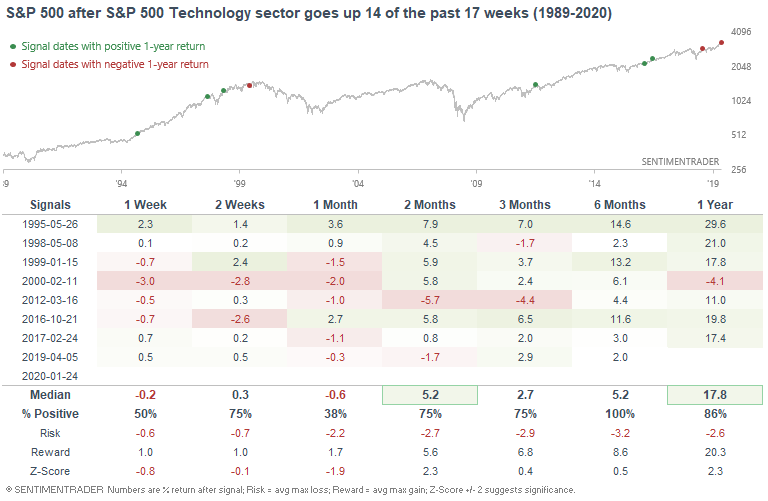

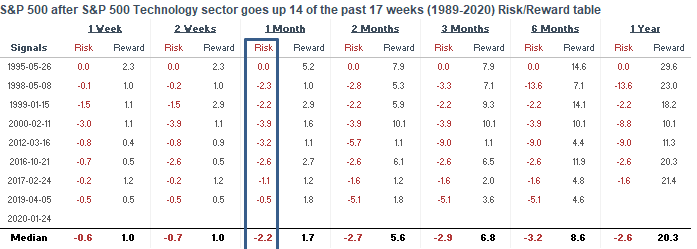

The most impressive sector over the past few months has been tech, which has rallied 14 of the past 17 weeks.

Such streaks are rare. And while it did lead to some large losses over the next 1-3 months, the S&P 500 Technology Sector didn't always fall:

On the other hand, this was more bearish for the broader S&P 500 over the next month:

Here were the S&P's drawdowns over the next month:

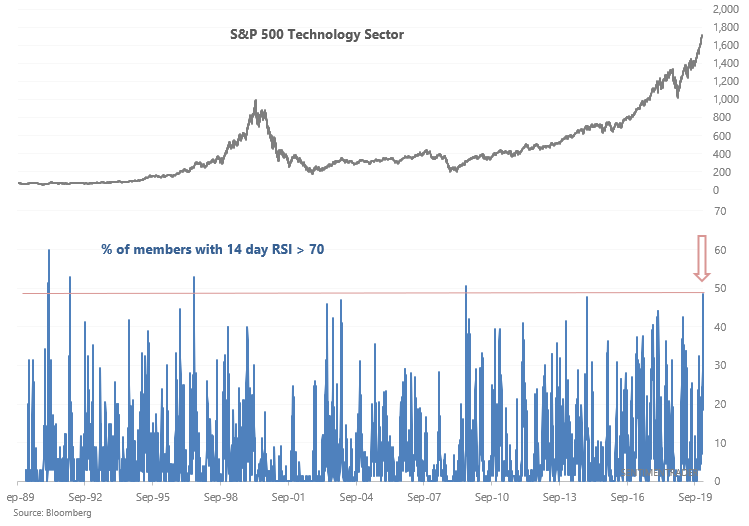

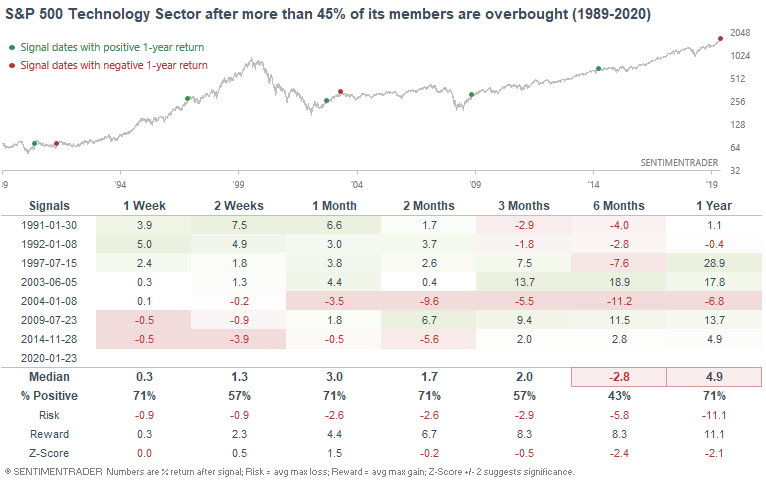

Taking a look under the hood, 48% of the S&P 500 Technology Sector's members were overbought as of Thursday (just before stocks tanked on Friday). This is an extremely large figure, and has only been matched several times since 1989.

Historical instances saw heavy downwards bias (or at least sideways choppiness) over the next 3-6 months:

Volatility

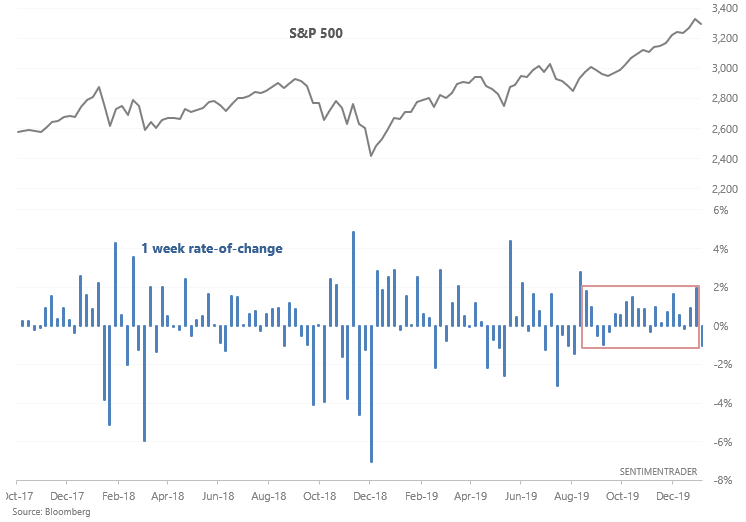

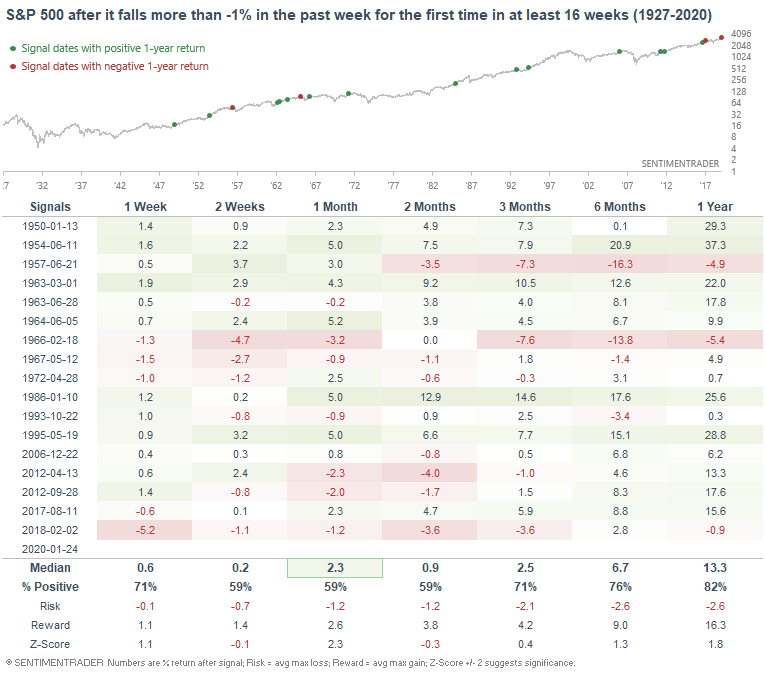

And lastly, this week saw the S&P 500's first -1% weekly decline (Friday's CLOSE vs. previous Friday's CLOSE) in 16 weeks:

When previous streaks of low volatility ended, the S&P usually saw more weakness over the next 2 months. This has been particularly true over the past 50 years, since most of the bullish cases occurred pre-1970s:

To recap

- Long term risk:reward doesn’t favor bulls.

- Fundamentals (6-12 months): still bullish because there is no significant U.S. macro deterioration.

- Technicals (1-3 months): bearish

Got any questions? Feel free to contact me at [email protected]

January 25, 2020: Fundamentals Overview Part 2

This is Part 2 of a weekly update on the U.S. stock market's long term fundamentals. Part 1 can be found here.

Fundamentals 1-3 years: market timing

I don't try to predict the future of the economy. Plenty of very smart people try, and when you add up the successes+failures, the results are usually no better than a 50/50 coin toss. That's why I focus instead on leading economic indicators. Look at what has already happened instead of predicting the future.

The economy drives corporate earnings, which drives the stock market in the long term. As a result, bull markets usually coincide with economic expansions, and big bear markets usually coincide with recessions.

Since the stock market tends to peak before recessions begin, we need to look at leading economic indicators, which also deteriorate before recessions begin. This doesn’t mean that the stock market’s exact top cannot occur before macro starts to peak. This happened in January 1973, when the stock market peaked a few months before macro started to deteriorate. However, the biggest part of bear markets always occur after macro has deteriorated significantly.

Here’s a brief summary of the leading and most important economic indicators I track, some of which I include in the Macro Index. The ones that are included in the Macro Index have an asterisk beside them**

Bullish factors right now

- Labor market**

- Housing**

- Financial conditions

- Heavy Truck Sales**

- Inflation-adjusted retail sales

Neutral/bearish factors right now

- Corporate profits

- High yield spreads

Bearish factors right now

- Yield curve**

- Manufacturing**

Bullish factors

Labor market

Labor market indicators do not show any significant deterioration right now.

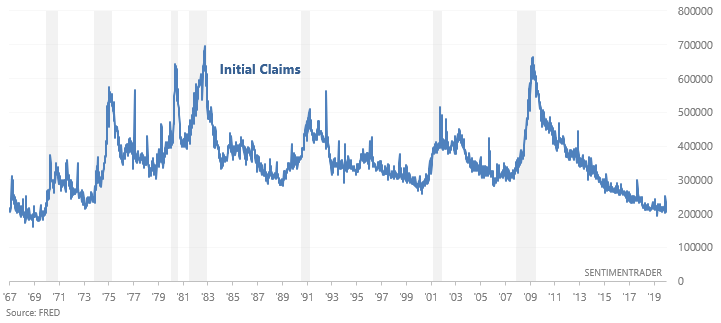

Initial Claims

Initial Jobless Claims measures the number of jobless claims filed by people who are seeking to receive jobless benefits. In other words, this measures the number of people who are recently unemployed. This economic indicator continues to trend sideways. In the past, Initial Claims trended higher before a recession began. This is still a positive point for macro, but watch out over the next few months in case Initial Claims trends upwards because Initial Claims is very low right now.

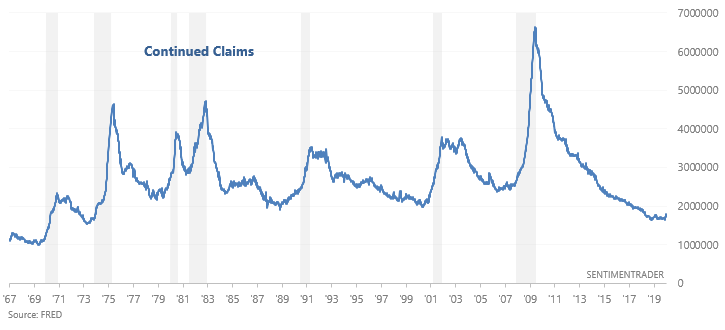

Continued Claims

Continued Jobless Claims measures the number of people who are still filing jobless claims (past the initial claim). This economic indicator continues to trend sideways. In the past, Continued Claims trended higher before a recession began. This is still a positive point for macro, but watch out over the next few months in case Continued Claims trends upwards because Continued Claims is very low right now.

Housing

Housing market indicators do not show significant deterioration right now.

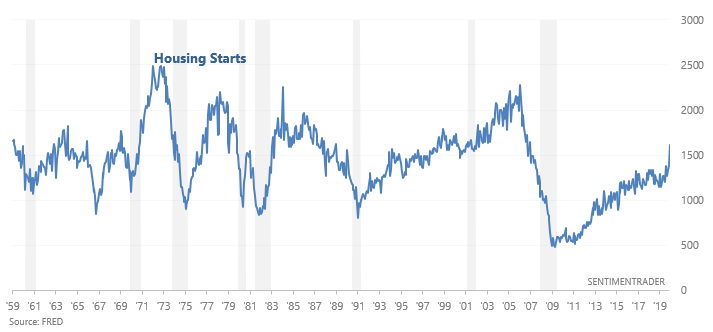

Housing Starts

Housing Starts measures the number of new homes that are starting to be built in the U.S., from the time of first excavation. This figure is trending higher right now. In the past, Housing Starts trended downwards before recessions began. This is a positive for macro.

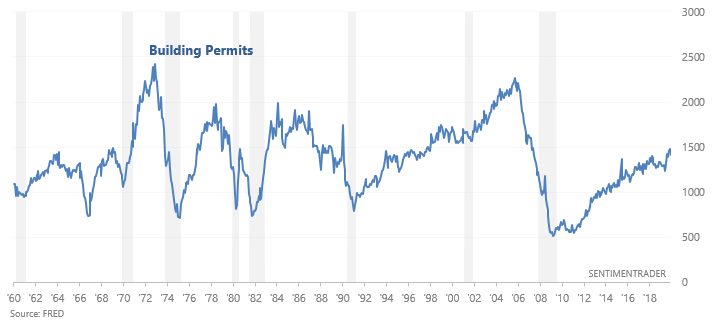

Building Permits

Building Permits are trending upwards right now. In the past, Building Permits trended downwards before recessions began. This is a positive for macro.

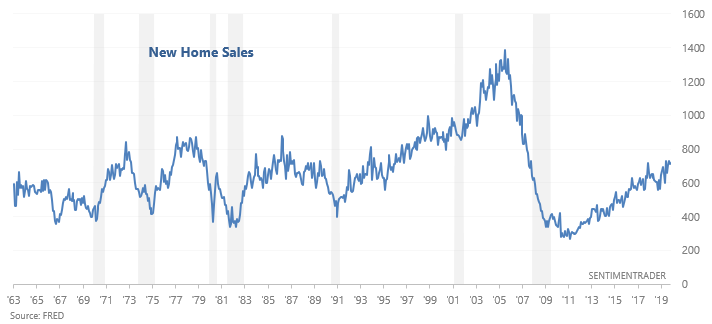

New Home Sales

New Home Sales are trending upwards right now. In the past, New Home Sales trended downwards before recessions began. This is a positive for macro.

Financial Conditions

Indicators related to financial conditions remain relatively loose. This is a positive for macro.

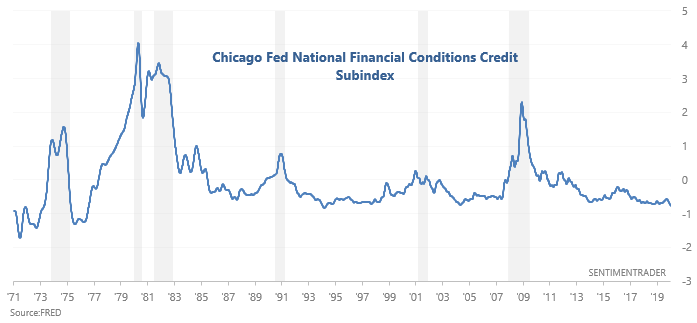

Chicago Fed Financial Conditions Credit Subindex

The Chicago Fed Financial Conditions Credit Subindex remains quite low. Looking at the bigger picture, the Credit Subindex is trending sideways right now. In a credit-driven economy, the Credit Subindex tends to trend solidly upwards (i.e. tighten) before a recession begins.

Loans

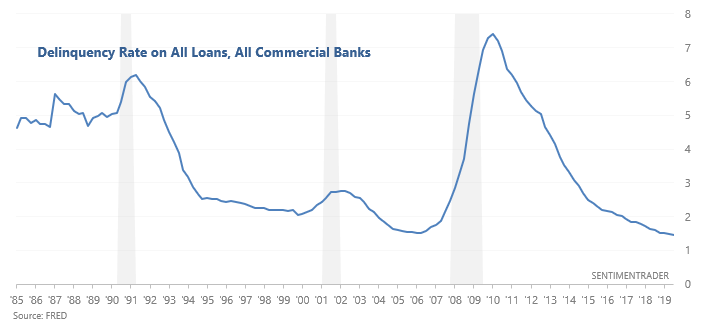

The Delinquency Rate on All Loans continues to trend downwards. In the past, the Delinquency Rate trended higher before a recession began. This is a positive for macro.

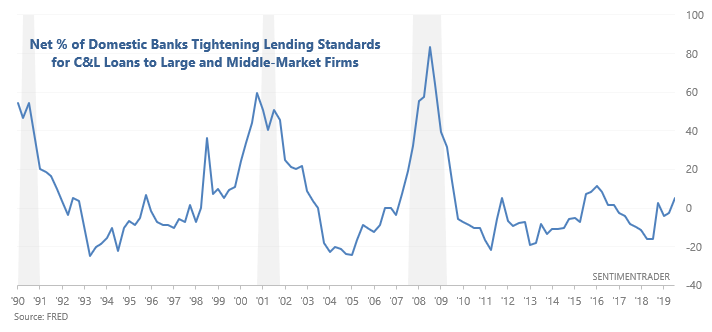

Banks’ lending standards

Banks are starting to tighten their lending standards right now. In the past, lending standards tightened for several quarters before a recession began, causing the Net Percentage of Banks Tightening Standards to trend higher. This was a positive for macro, but is now something that bulls should watch out for in case lending standards continue to tighten.

Inflation-adjusted retail sales

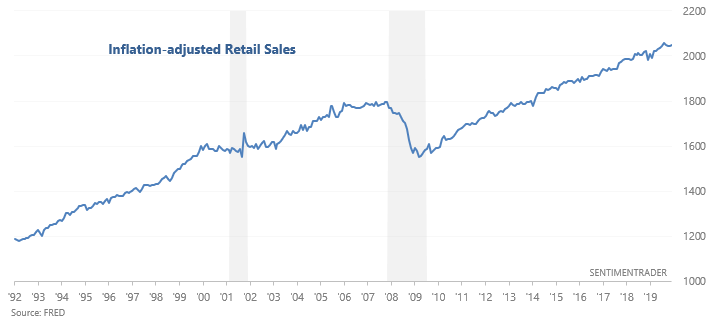

Inflation-adjusted Retail Sales continue to trend higher. In the past, inflation-adjusted Retail Sales trended sideways before recessions began. This is a positive for macro.

Neutral/bearish factors

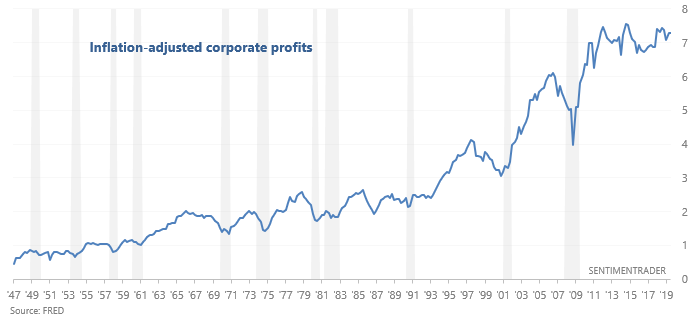

Corporate Profits

Figures related to corporate profits suggest that the economic expansion is definitely late-cycle.

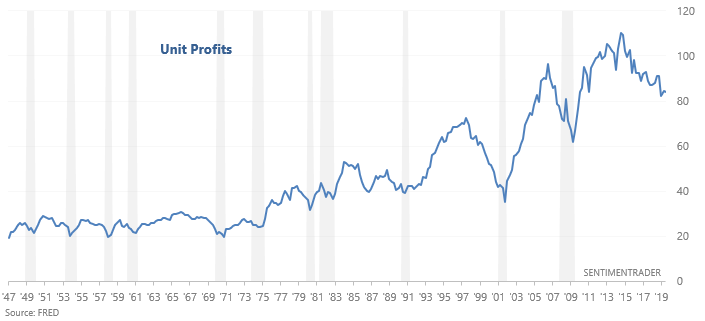

Unit Profits

Unit Profits continue to trend downwards, which is typically what happens in the second half of an economic expansion cycle. However, this indicator is not a timing tool. Unit Profits can fall for years before a recession begins.

Corporate Profits

Inflation-adjusted corporate profits are trending sideways. In the past, inflation-adjusted corporate profits trended downwards for several quarters before recessions began. If corporate profits start to trend downwards, this will be a negative for macro in 2020.

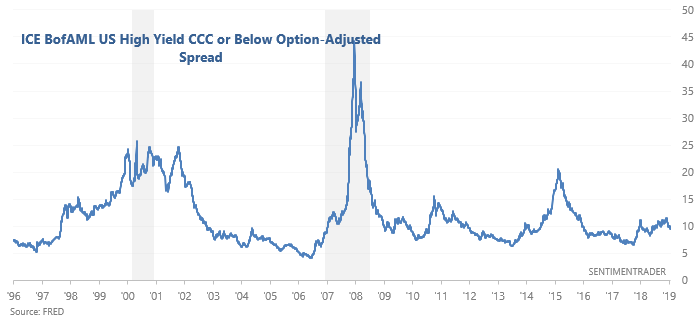

High yield spreads

From September 2018 – present, high yield spreads on the lowest rated bonds have been trending higher while the stock market has made higher highs. This is a necessary but not sufficient condition for bear markets and recessions. In the past, high yield spreads on these bonds trended higher before bear markets and recessions began. Meanwhile, high yield spreads in general are still trending lower. Overall, this is a neutral factor for stocks right now.

Bearish factors

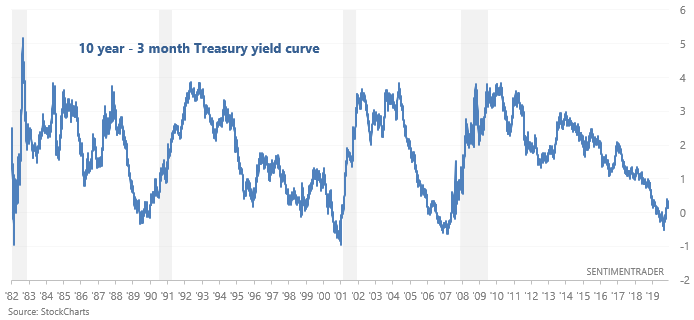

Yield Curve

Both the popular 10 year - 2 year and 10 year - 3 month sections of the yield curve were recently inverted, and are now trending higher. Here's the 10 year - 3 month yield curve, which historically has been a better market timing indicator than the 10 year - 2 year yield curve:

Overall, the yield curve is a bearish factor for macro right now because inversions & post-inversion steepenings tend to occur 1-2 years before recessions and bear markets begin. HOWEVER, the yield curve is merely one of many factors to consider, and it is not flawless.

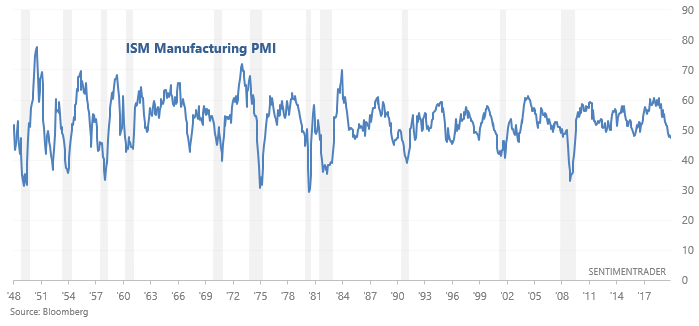

Manufacturing

The manufacturing sector remains one of the weakest parts of the U.S. economy, and this is probably related to the trade war. For example, the ISM Manufacturing PMI is currently below 50, which signals contraction. This is a bearish factor for our Macro Index.

Macro Index

The Macro Index includes:

- New Home Sales

- Housing Starts

- Building Permits

- Initial Claims

- Continued Claims

- Heavy Truck Sales

- 10 year - 3 month Treasury yield curve

- S&P 500's 10 month average

- ISM Manufacturing PMI

- Margin Debt

- Inflation