Headlines

|

|

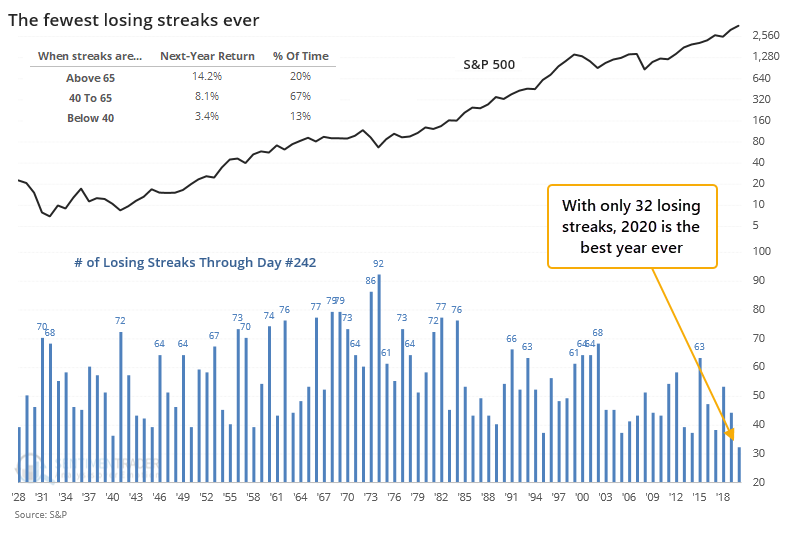

The fewest losing streaks in history:

This year has seen the fewest losing streaks in history. There have only been 32 days that were part of back-to-back losing sessions, the fewest since 1928. After other years with few losing streaks, forward returns were good but were even better after years with many losing streaks.

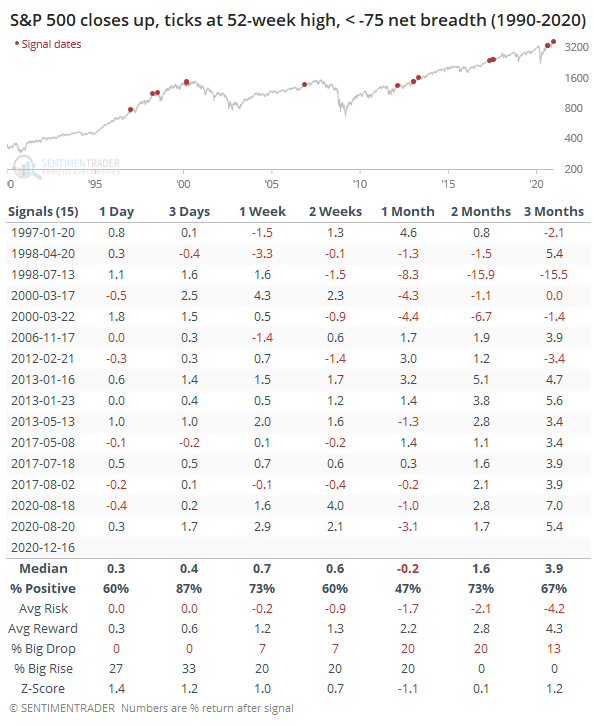

Trying for a high, with fewer issues: When the major indexes rise but with odd internal readings, it has proven to be an effective heads-up that something is amiss and we should be on guard. For most of the past few months, participation underlying the major indexes has been pristine, so no real worries there. Wednesday was slightly different. The S&P 500 rose for the day, and it ticked at a 52-week high, but by the close, there were more than 75 declining than advancing stocks in the index.Single days aren't a big worry, but if we continue to see behavior like this, it will be a warning sign.

Bottom Line:

- The market environment is pristine, but with near-historic optimism, gains tend to be muted, with a high probability of being reversed at some point over the ensuing weeks.

|

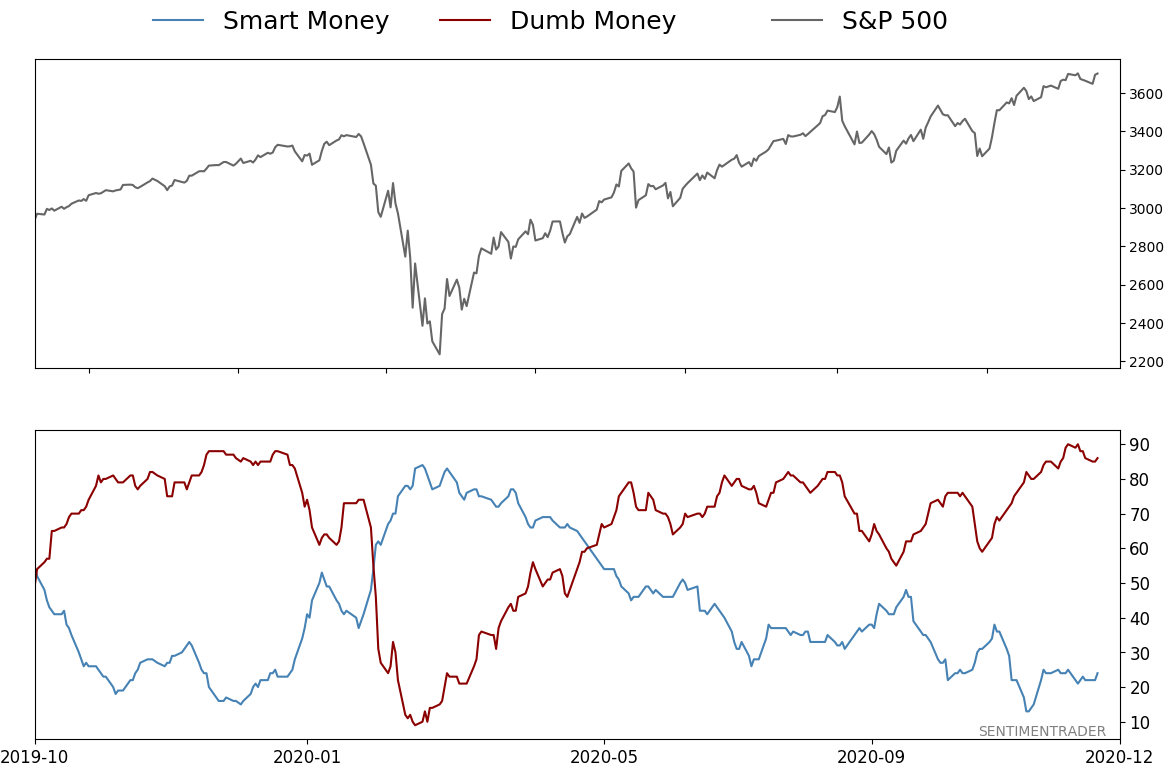

Smart / Dumb Money Confidence

|

Smart Money Confidence: 24%

Dumb Money Confidence: 86%

|

|

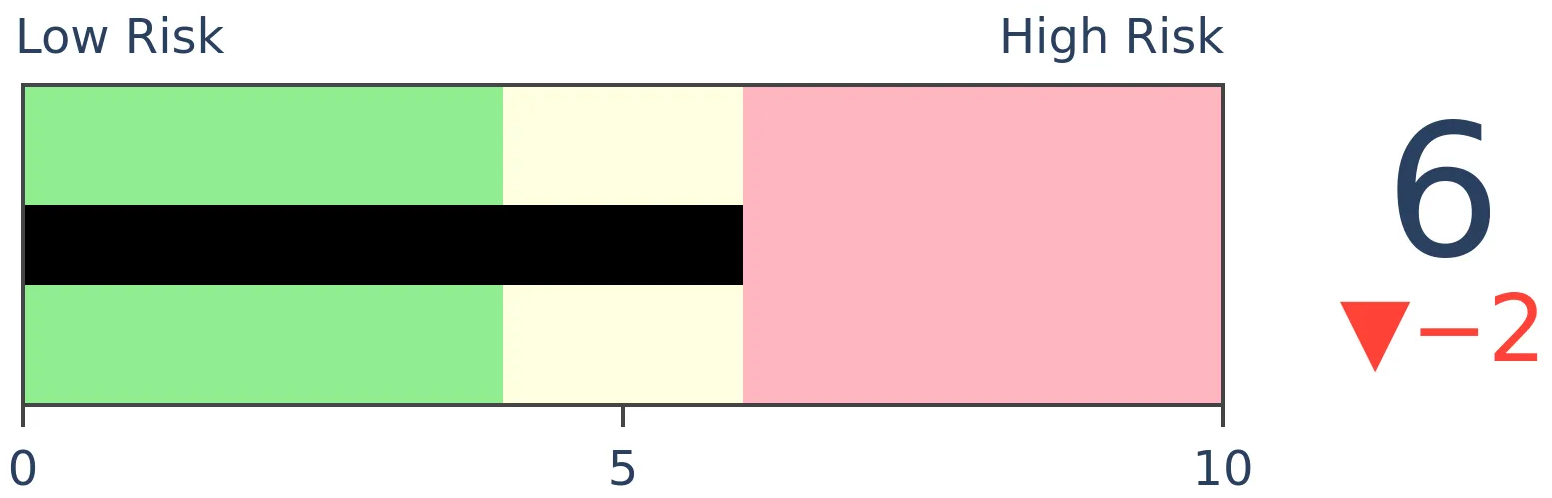

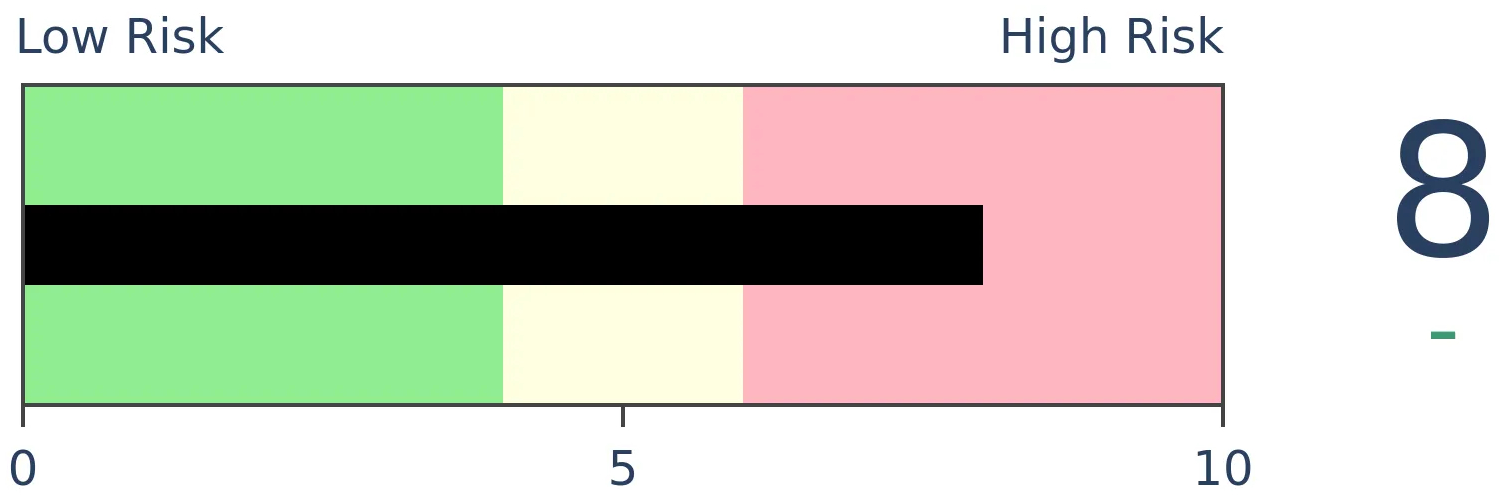

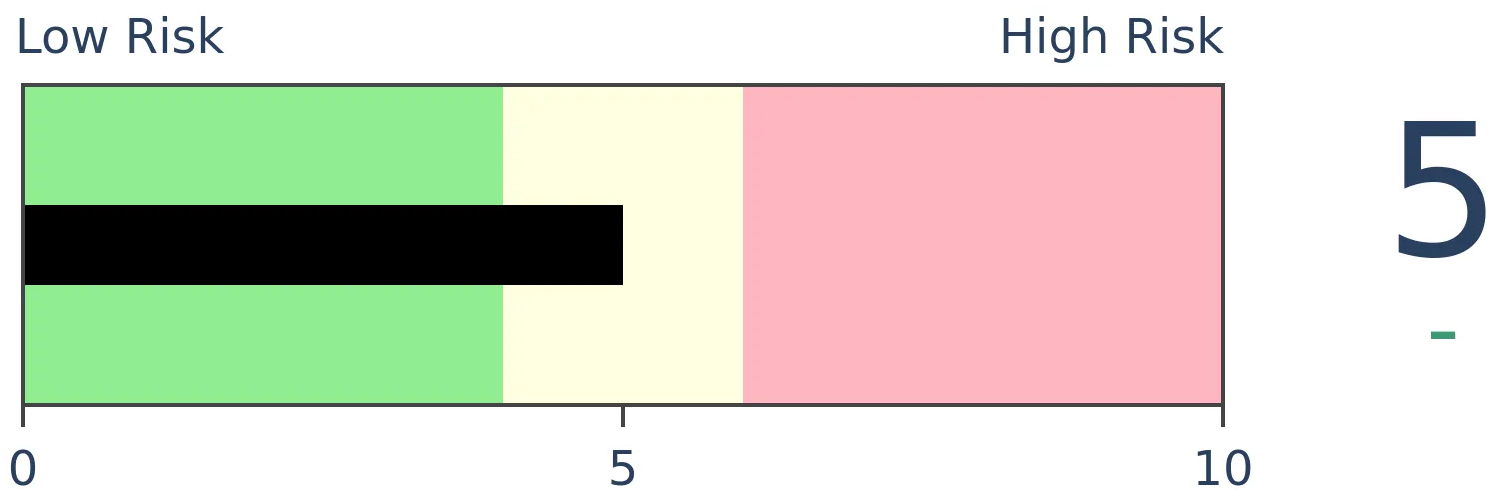

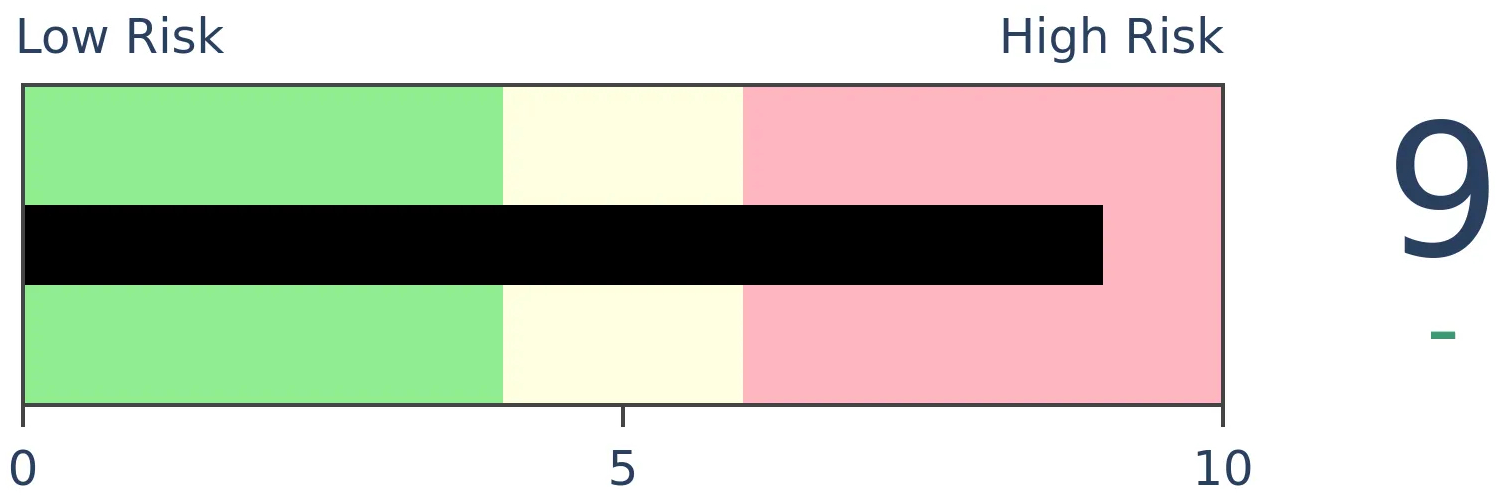

Risk Levels

Stocks Short-Term

|

Stocks Medium-Term

|

|

Bonds

|

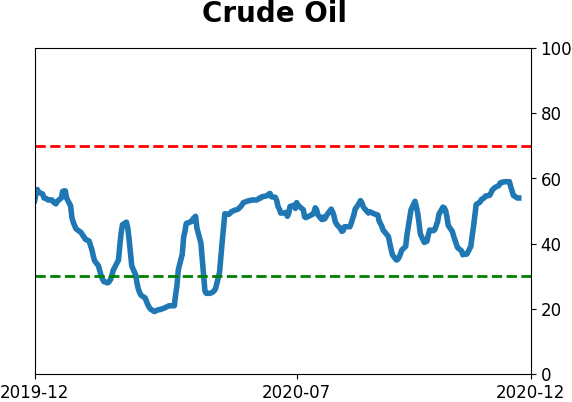

Crude Oil

|

|

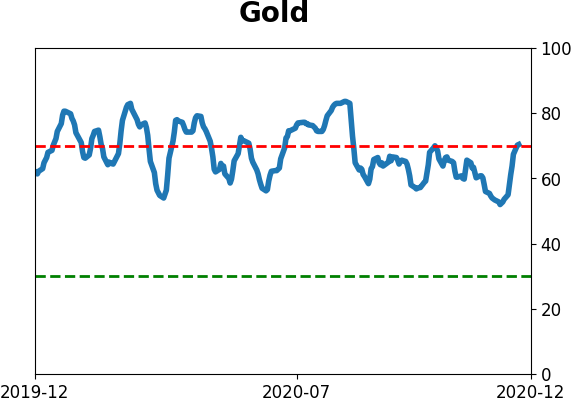

Gold

|

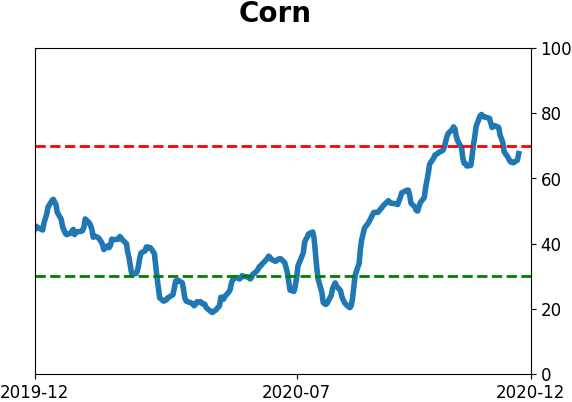

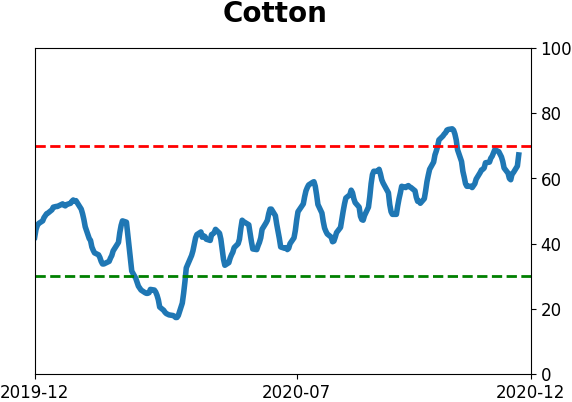

Agriculture

|

|

Research

BOTTOM LINE

This year has seen the fewest losing streaks in history. There have only been 32 days that were part of back-to-back losing sessions, the fewest since 1928. After other years with few losing streaks, forward returns were good but were even better after years with many losing streaks.

FORECAST / TIMEFRAME

None

|

Despite the pandemic, recession, and record unemployment, the year 2020 has been the most consistently positive year in history.

Strategist Callie Cox noted that this year has seen only 32 days that were mired in a losing streak, defined as back-to-back losing sessions. On a rolling one-year basis, this is the lowest in history.

The chart shows us that there is a contrary bias to this data. Returns following periods with many losing streaks were relatively high; returns following few losing streaks were relatively low.

If we look at this on a calendar-year basis, then we're currently on trading day #242 of the year. Again, no other year has had so few losing streaks this far into the calendar since 1928.

We can see from the chart that the S&P's next-year return averaged +14.2% after years with the most losing streaks, versus only +3.4% after years when there were few of them. That makes sense, as stocks meander from one extreme to the other, and it's even starker than the returns we saw in the first chart.

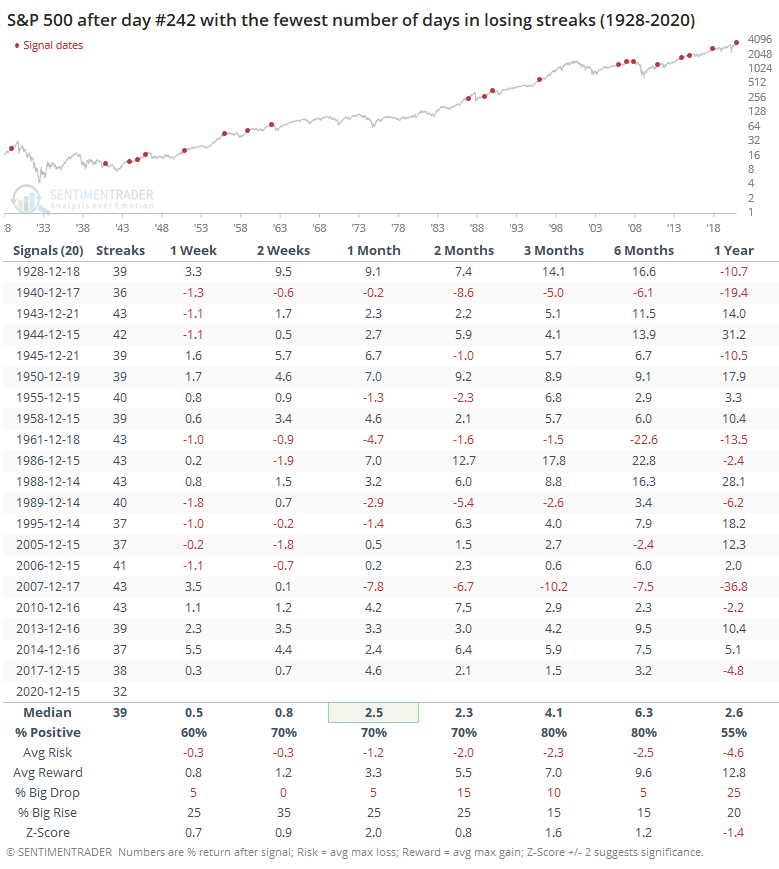

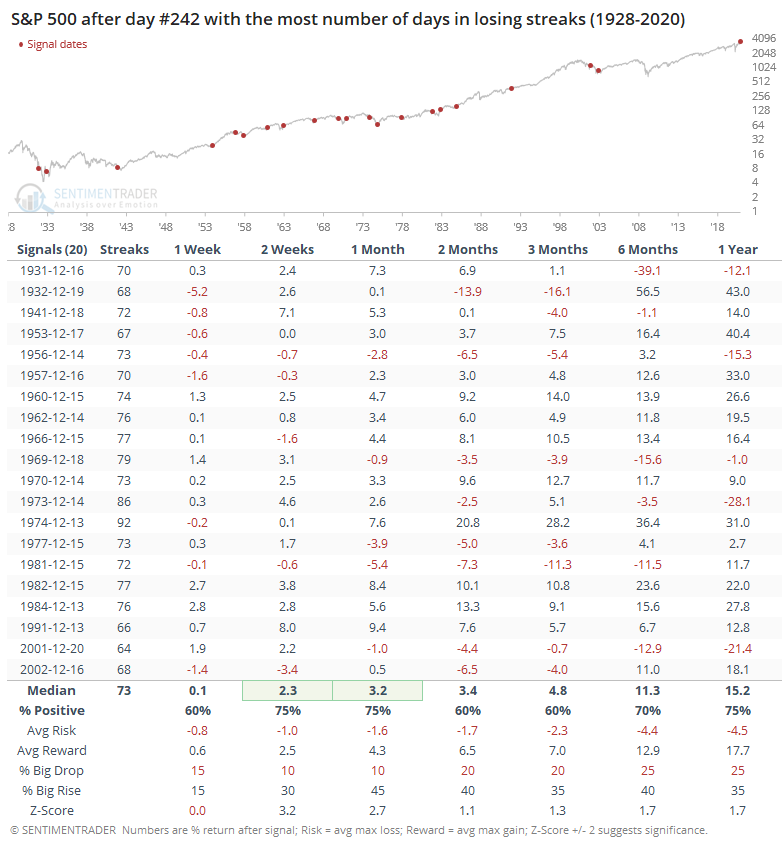

Below, we can see the index's forward returns after the 20 years with the fewest losing streaks, as of trading session #242.

When we combine positive seasonality with strong momentum, good things tend to happen, at least over a medium-term time frame. The S&P 500's forward returns were strong during the next 1-3 months, with a good risk/reward ratio. None of it was exceptional, but at least it had a positive bias.

Now let's look at returns after the years with the most losing streaks to see if there's much of a difference.

Here, returns were even stronger over the next 2-4 weeks, and much better during the next year. The percentage of time the S&P showed a gain was a little weaker over the next 2-6 months, but all the other metrics were stronger than those years with few losing streaks.

The suggestion is that during years when investors suffered, the last couple weeks of December and the first couple of January tended to do better than after those years when winning was "easy," like this year.

Overall returns after all the signals were decent, which speaks more to the idea of positive seasonality than it does persistent momentum. It's just not very common to see large, protracted declines during this time of year, even if those who traded during 2018 would scream their objection.

This year is unlike any other, with record optimism on some measures battling record momentum on others. The calendar would further argue that bulls, and momentum, have the temporary advantage.

Active Studies

| Time Frame | Bullish | Bearish | | Short-Term | 0 | 0 | | Medium-Term | 4 | 0 | | Long-Term | 47 | 2 |

|

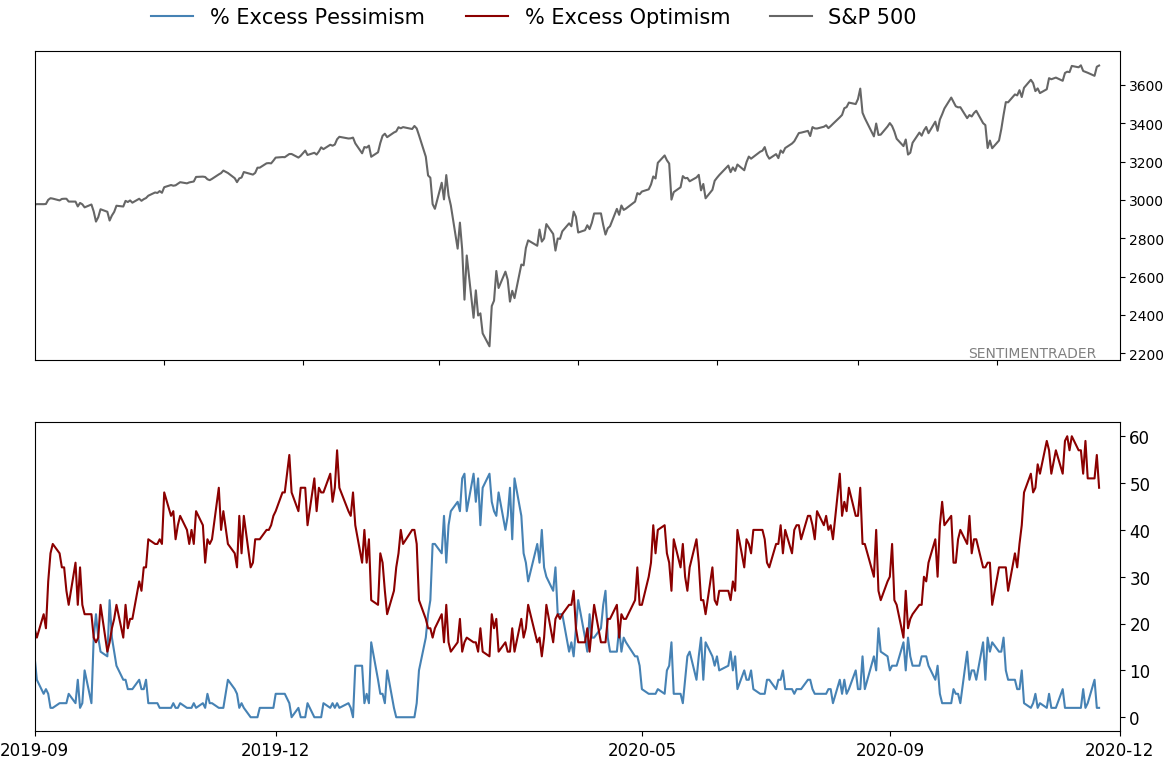

Indicators at Extremes

% Showing Pessimism: 2%

Bullish for Stocks

VIX

|

|

Portfolio

| Position | Description | Weight % | Added / Reduced | Date | | Stocks | 10.4% VWO, 9.1% XLE, 8.5% RSP, 6.6% PSCE | 34.5 | Reduced 6.7% | 2020-12-14 | | Bonds | 10% BND, 10% SCHP, 10% ANGL | 28.4 | Reduced 0.1% | 2020-10-02 | | Commodities | GCC | 2.4 | Reduced 2.1%

| 2020-09-04 | | Precious Metals | GDX | 8.9 | Added 4.8% | 2020-12-01 | | Special Situations | | 0.0 | Reduced 5% | 2020-10-02 | | Cash | | 25.8 | | |

|

Updates (Changes made today are underlined)

Quite a few of the studies that have been triggering for stocks have showed a poor risk/reward skew over a short- to medium-term time frame, even though many of them have also been quite positive over medium- to long-term time frames. We're in a very favorable seasonal window, so it would be somewhat odd to see a substantial pullback in the next few weeks. Leave it to 2020 to do just that, I suppose, but the calendar is a point in bulls' favor. Even so, record-high-and-declining sentiment, coupled with early signs of a reversal were enough that I reduced my S&P 500 position a bit. I fully expect that the energy funds will suffer some losses in the coming weeks, but as I noted when buying them, they're intended as long-term positions and almost by definition they're going to be volatile. RETURN YTD: 8.0% 2019: 12.6%, 2018: 0.6%, 2017: 3.8%, 2016: 17.1%, 2015: 9.2%, 2014: 14.5%, 2013: 2.2%, 2012: 10.8%, 2011: 16.5%, 2010: 15.3%, 2009: 23.9%, 2008: 16.2%, 2007: 7.8%

|

|

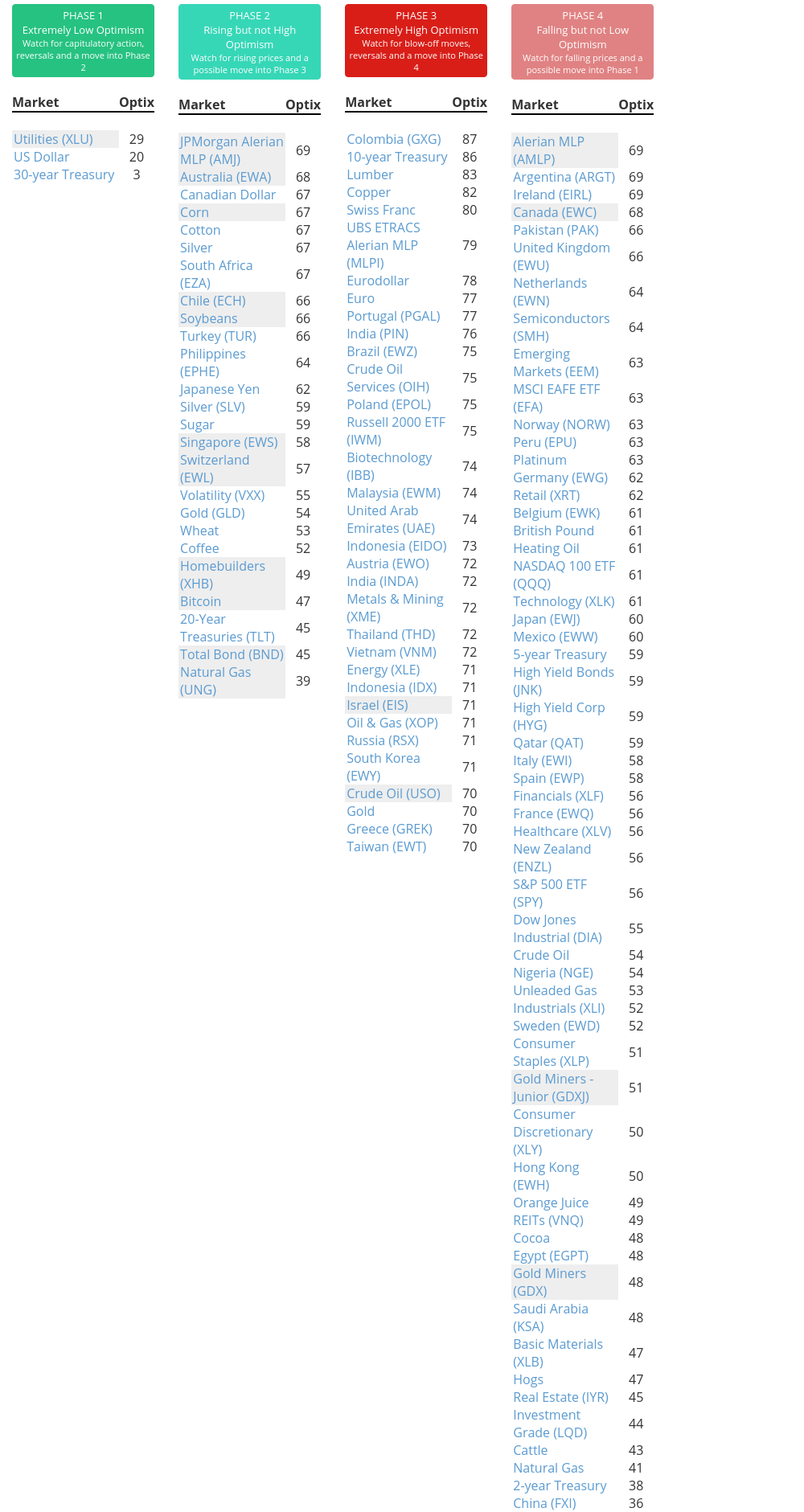

Phase Table

Ranks

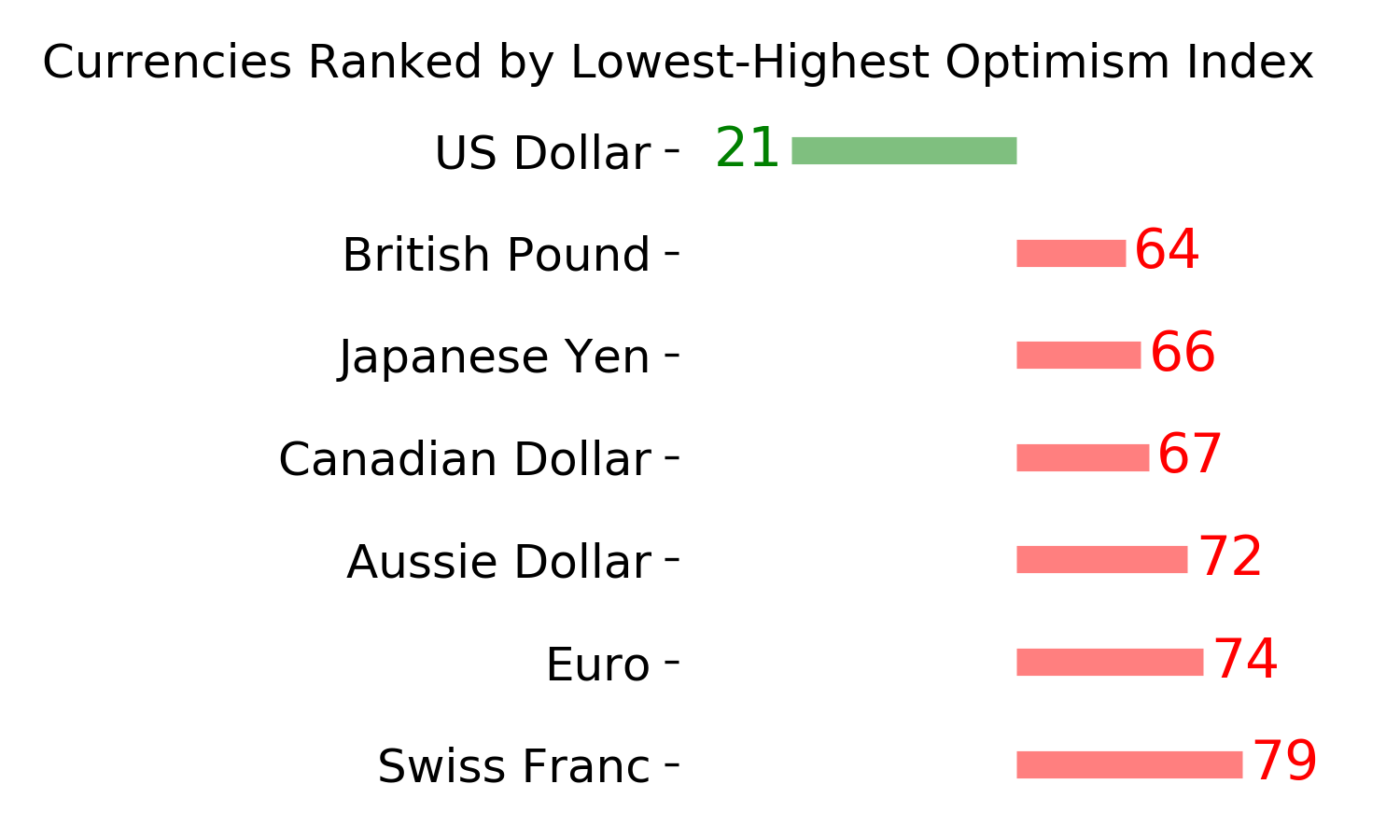

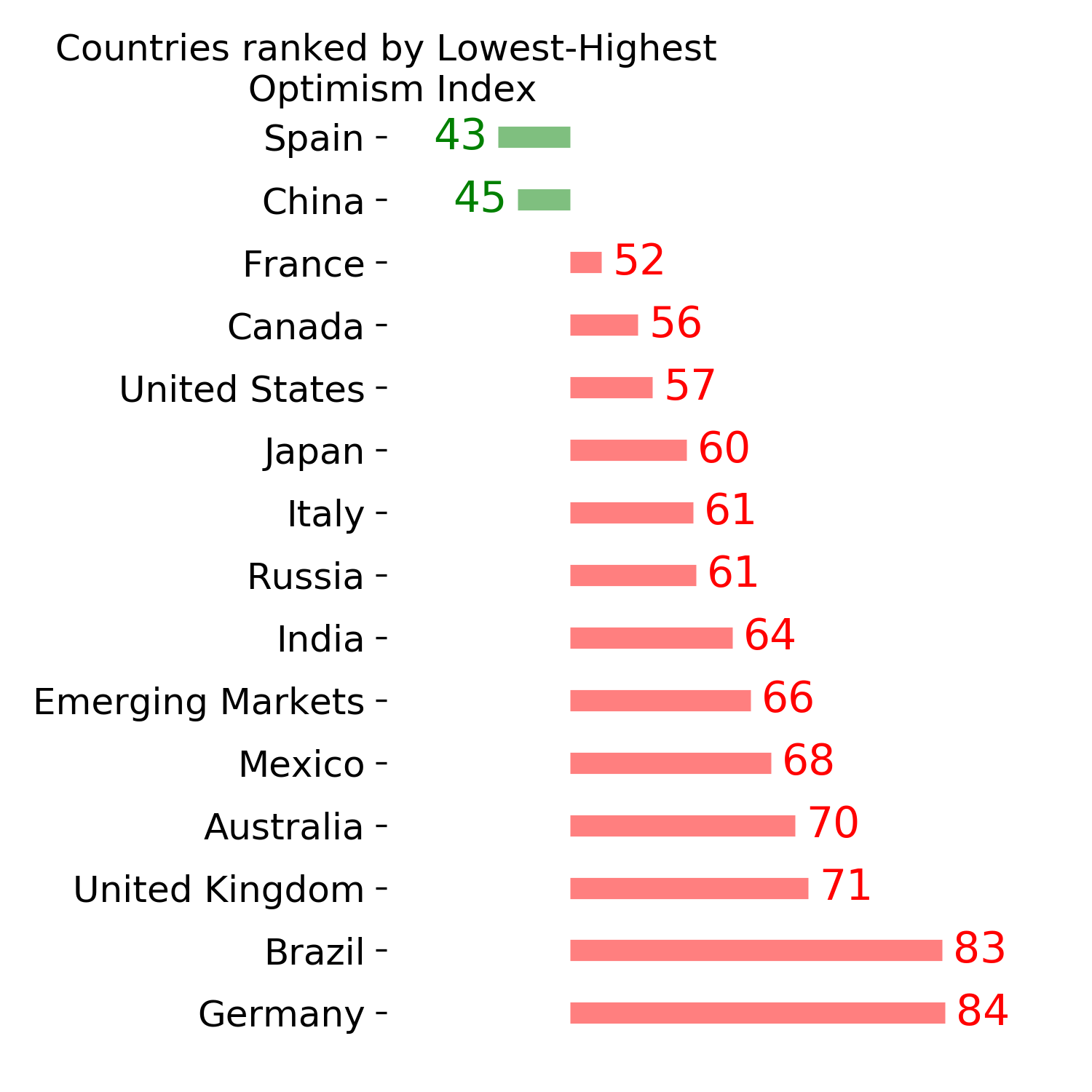

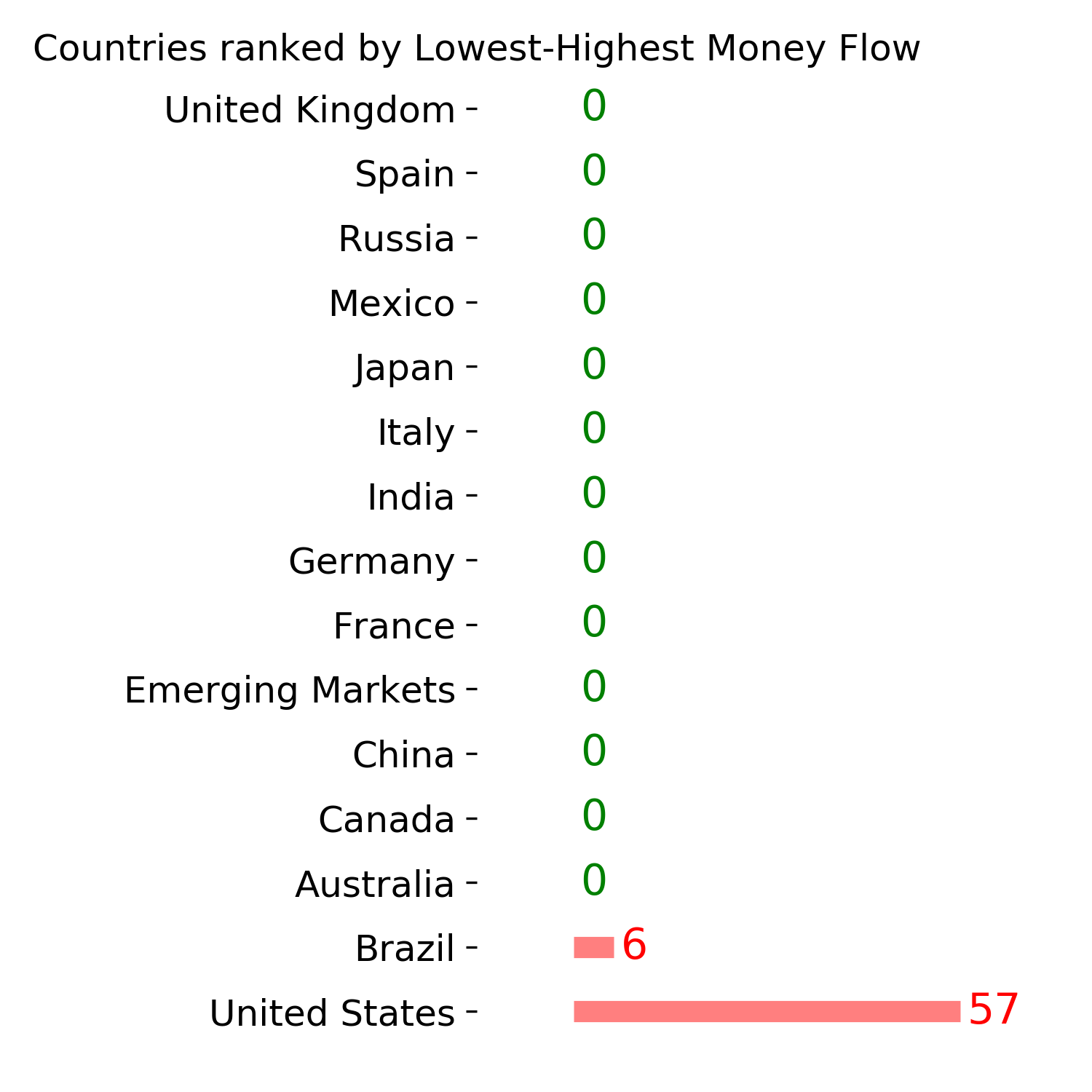

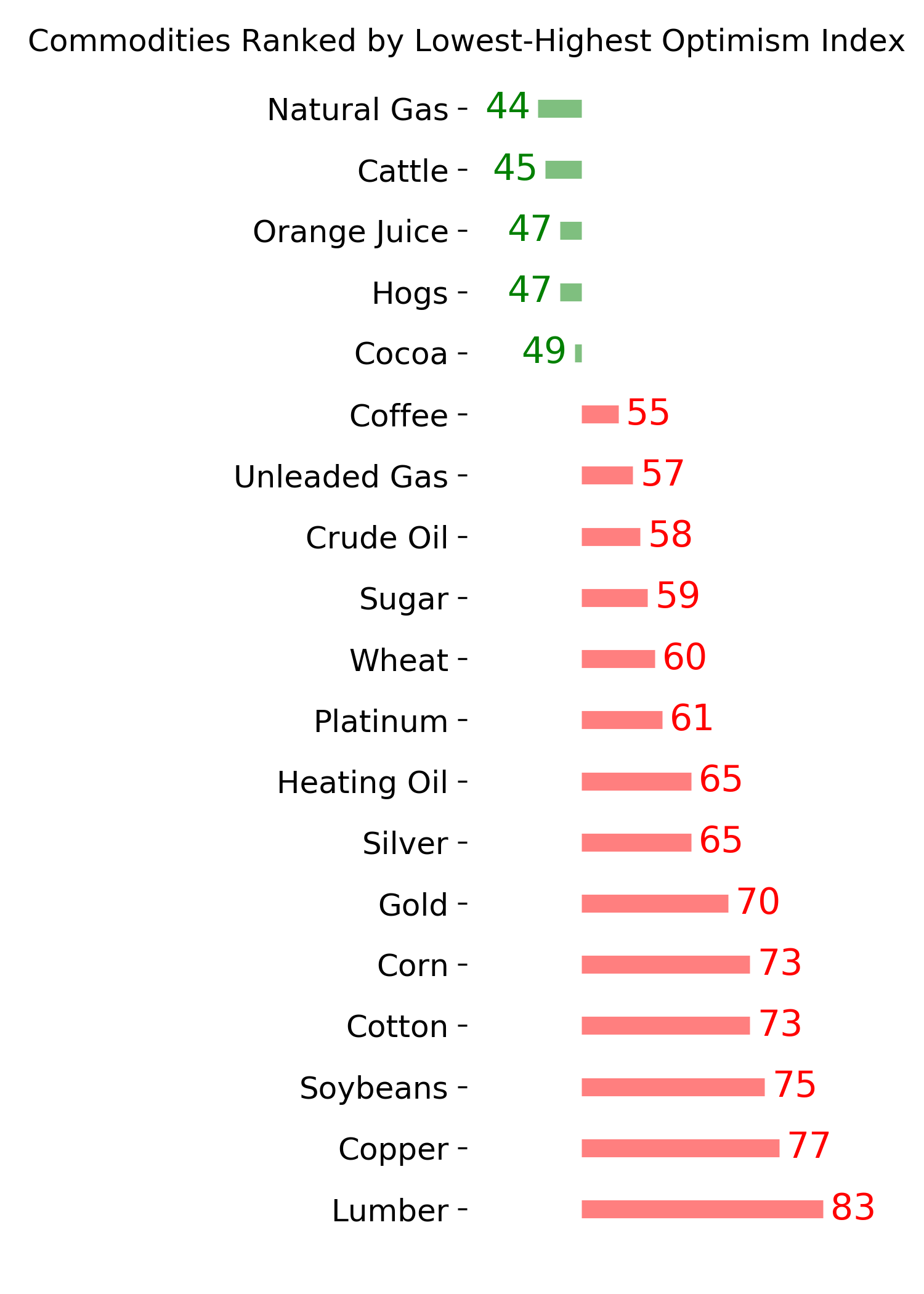

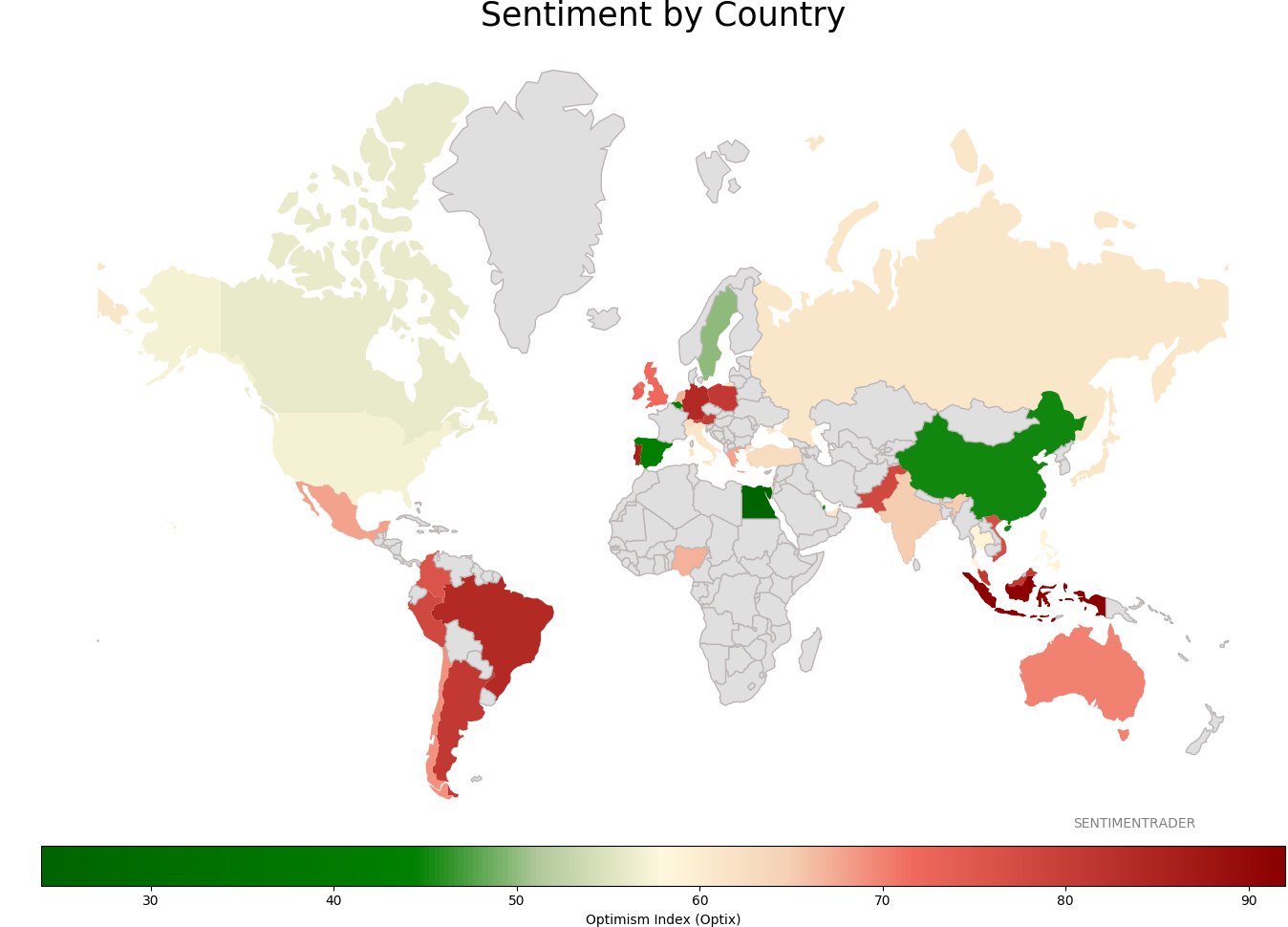

Sentiment Around The World

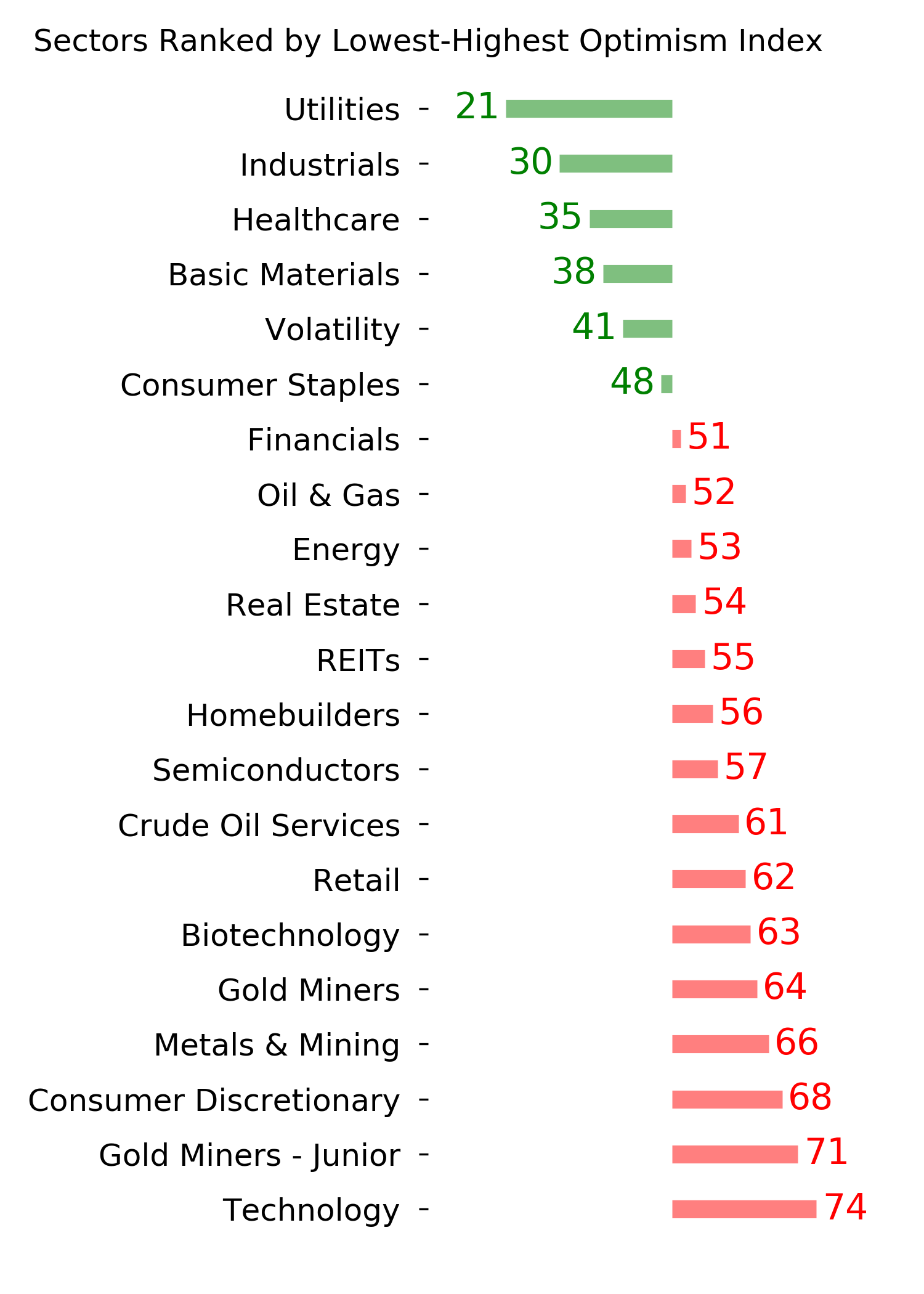

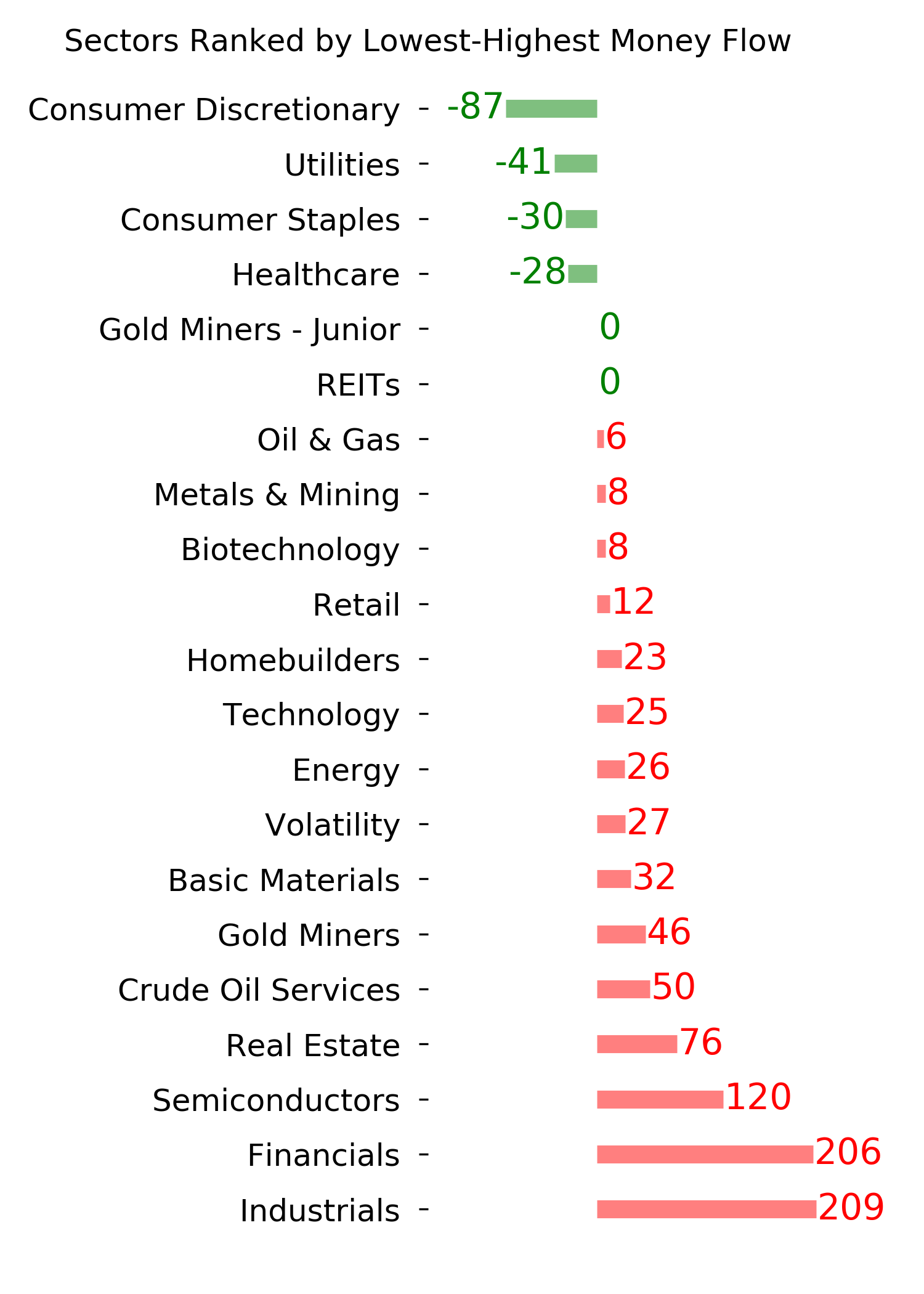

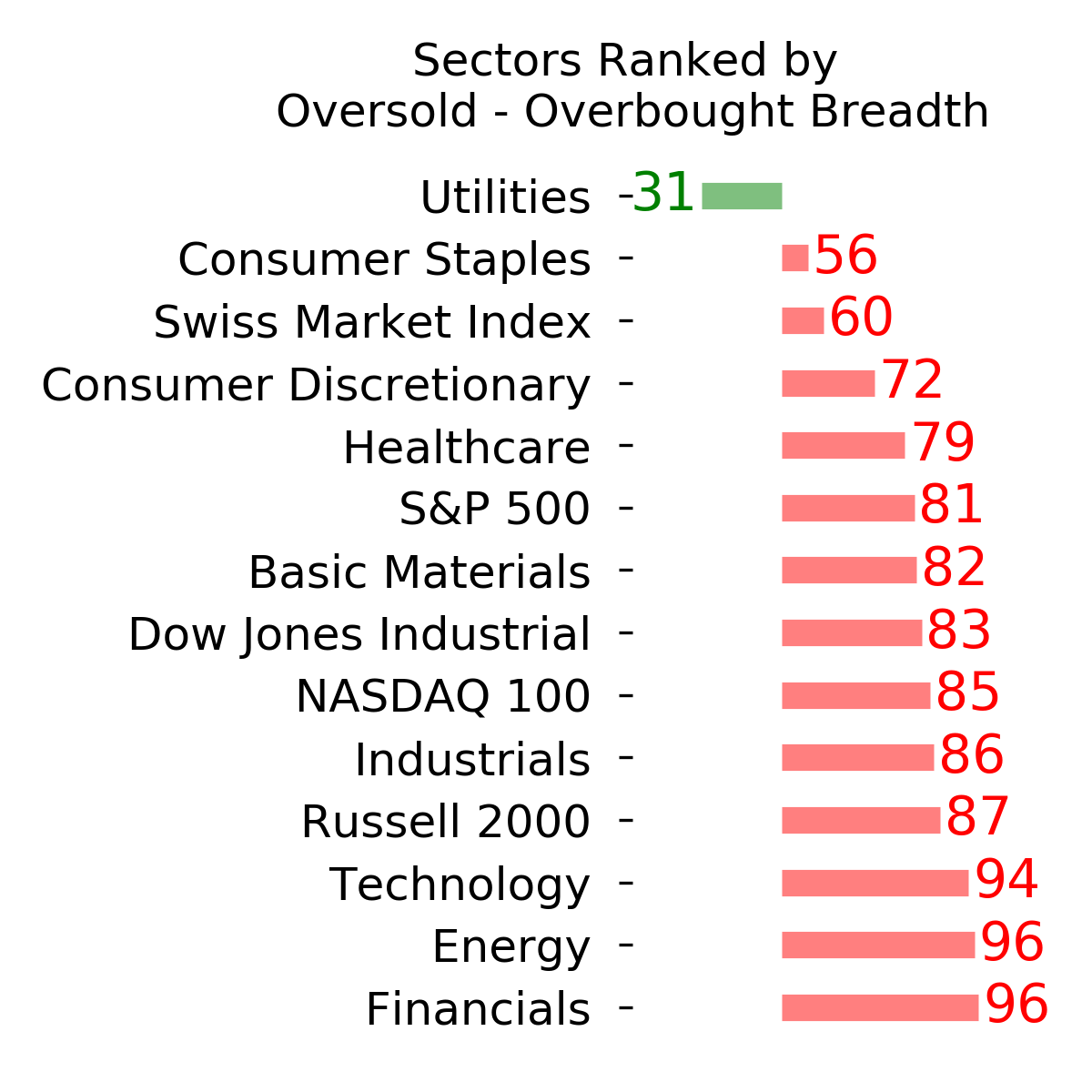

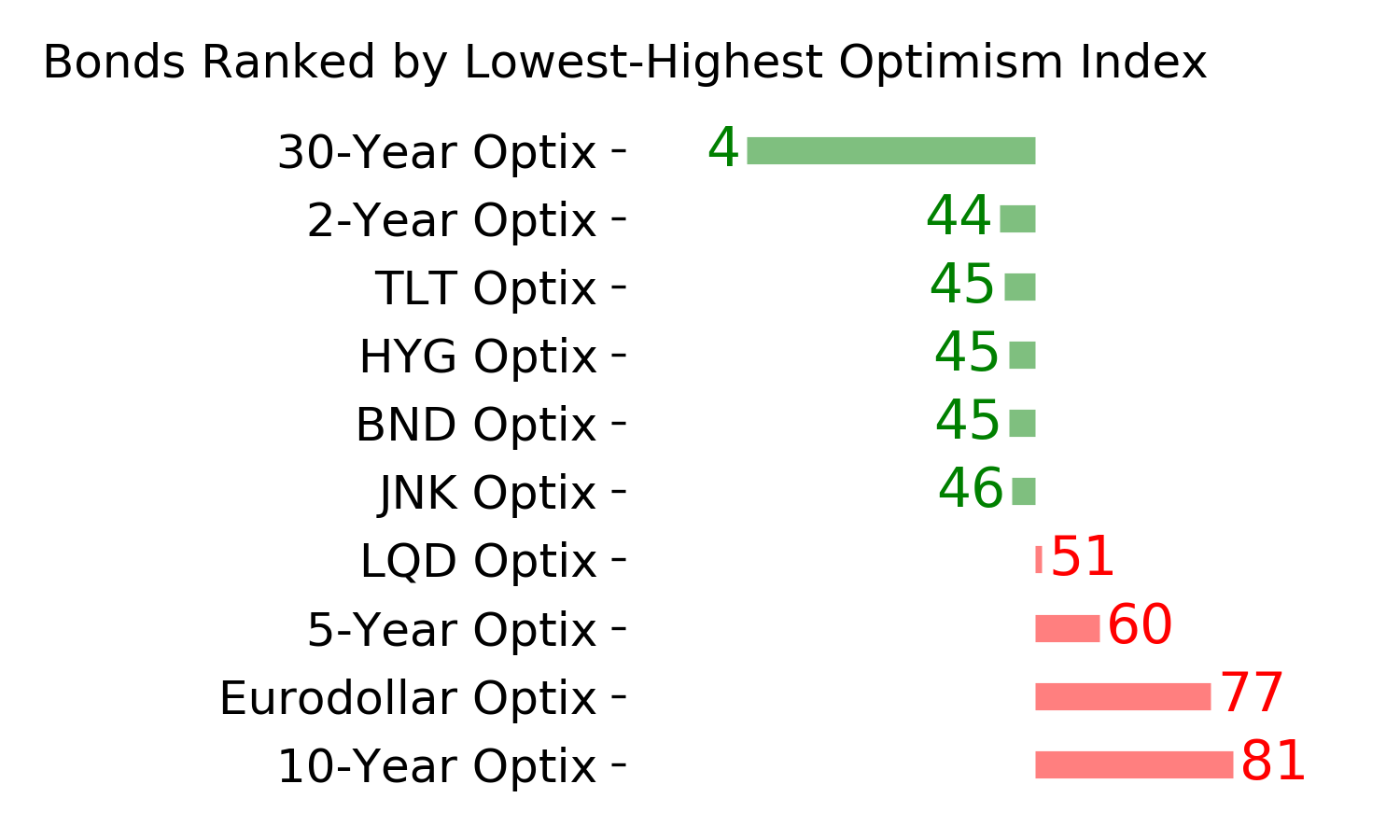

Optimism Index Thumbnails

|

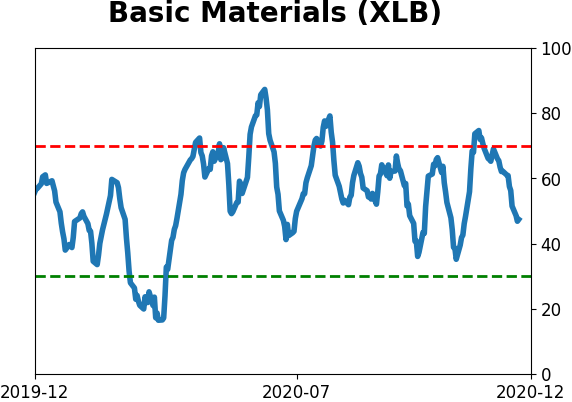

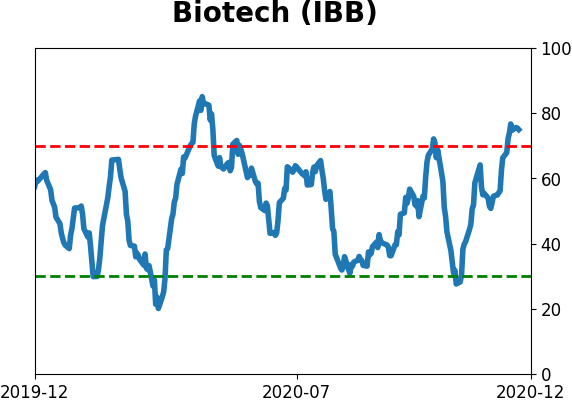

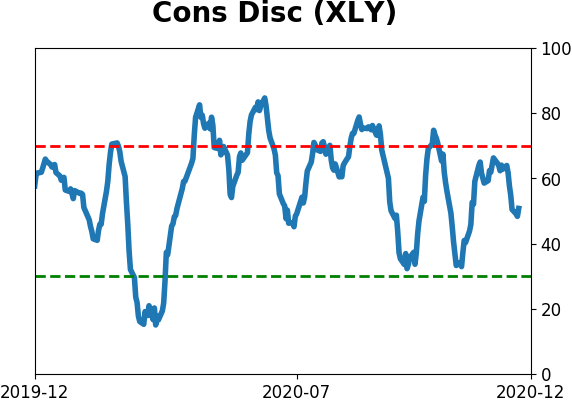

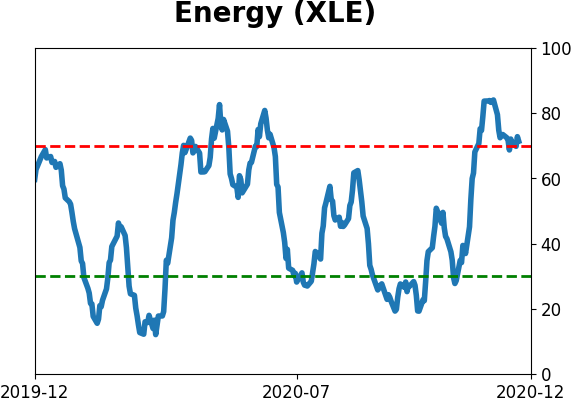

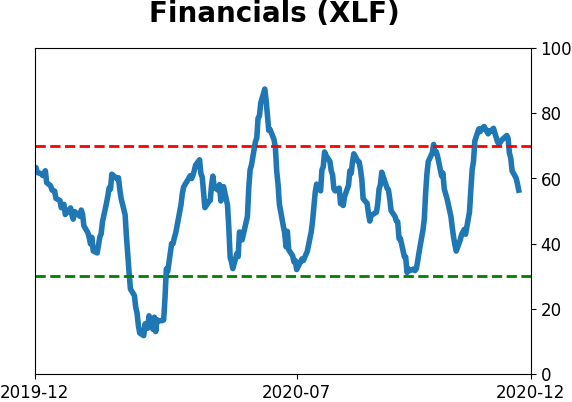

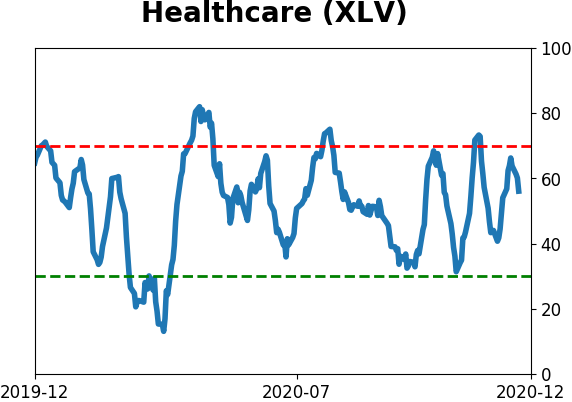

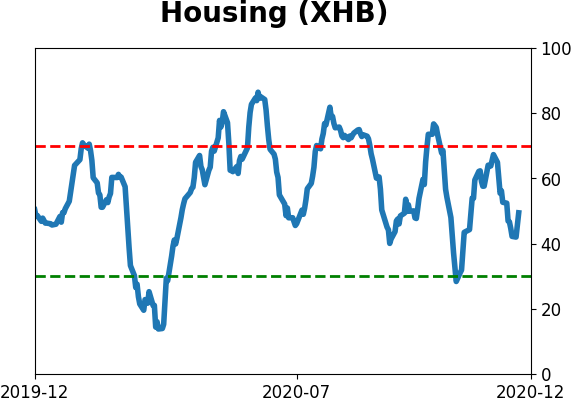

Sector ETF's - 10-Day Moving Average

|

|

|

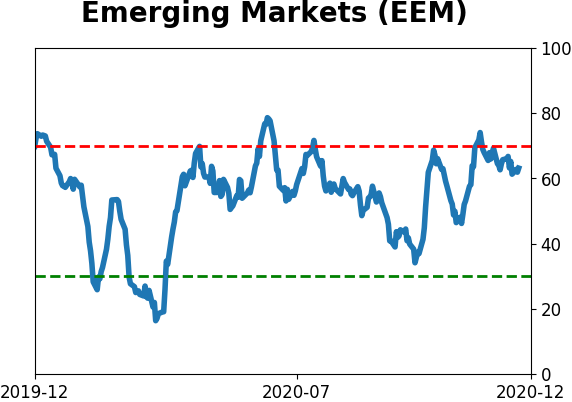

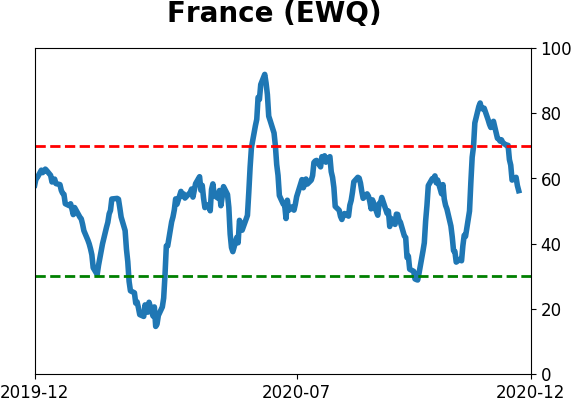

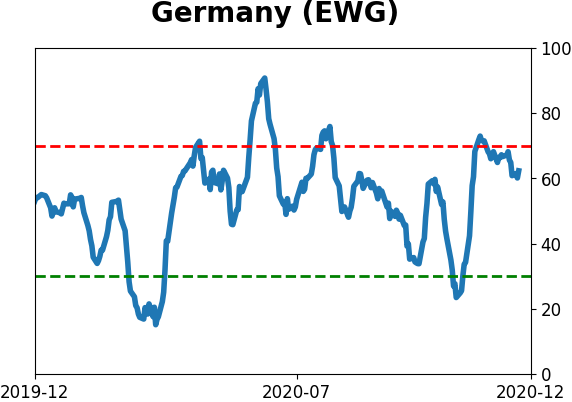

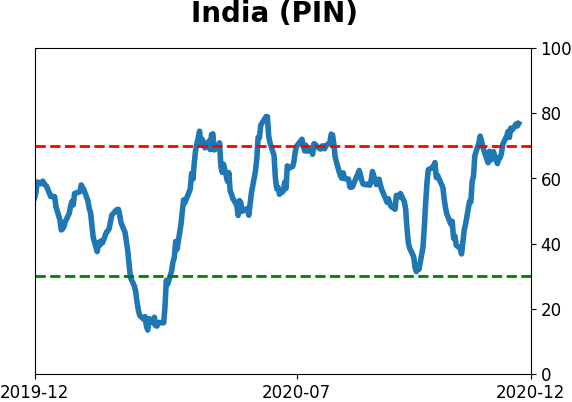

Country ETF's - 10-Day Moving Average

|

|

|

Bond ETF's - 10-Day Moving Average

|

|

|

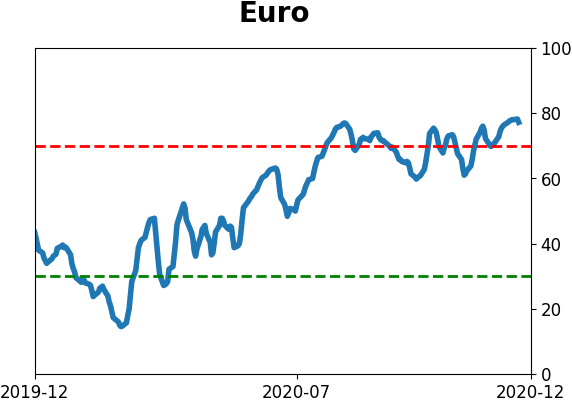

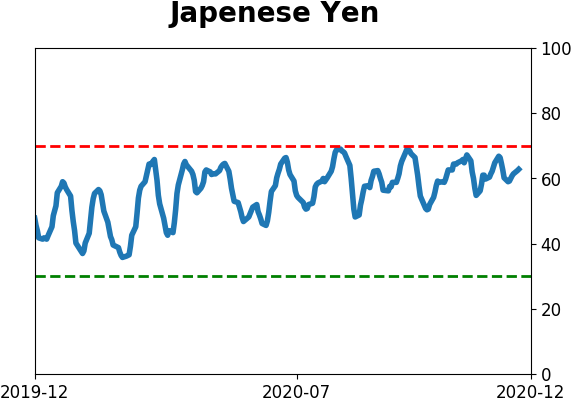

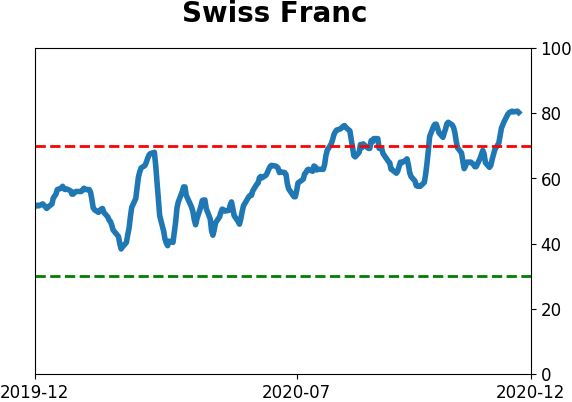

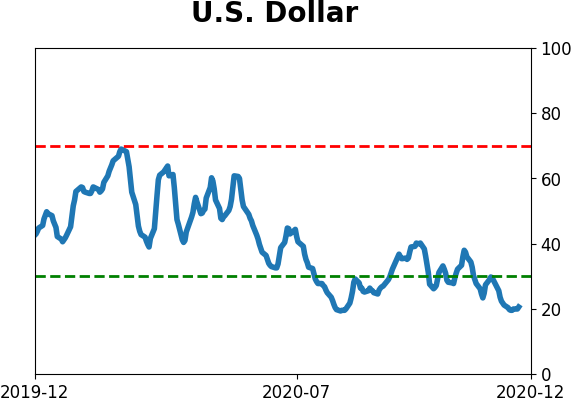

Currency ETF's - 5-Day Moving Average

|

|

|

Commodity ETF's - 5-Day Moving Average

|

|