Headlines

|

|

Alerts and Minutes:

Eric made some updates to the site over the weekend, so you'll see a couple of new things. The first is an alert button, which will show any new messages we've posted to the site. These could be anything from new content to site updates to data issues. They'll clear once you click the bell icon on any device.

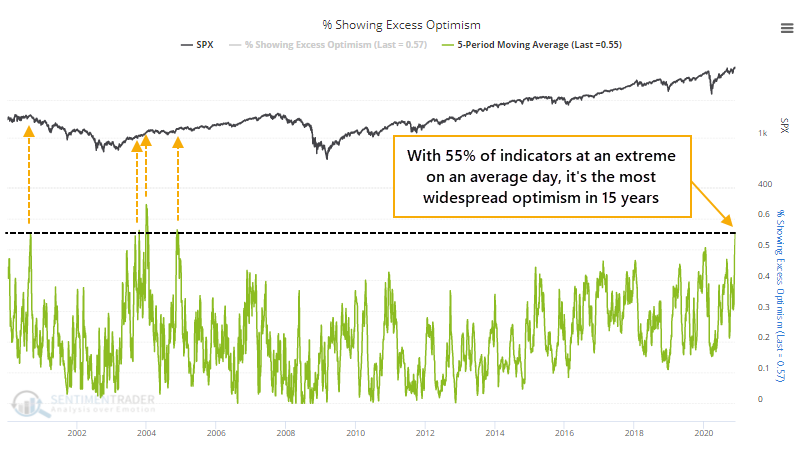

We haven't seen extremes like this in 15 years:

Options traders are supremely confident again, helping to trigger the most extremes among our indicators in 15 years. Forward returns tend to be muted after confidence like this. Momentum, breadth, and seasonality remain positive but that has helped less in the short-term.

The latest Commitments of Traders report was released, covering positions through last Tuesday: Last week, "smart money" commercial hedgers mostly continued their trend of selling copper and pretty much anything that grows. They maintained or furthered their bets against corn, soybeans, and sugar. As we've been noting for a while, this is a change in behavior in these contracts - over the past decade, when hedgers established large short positions, they would just roll right over to new lows. That has not happened in recent months, and suggests that the larger trend has changed for the better. In stocks, they've once again moved to a net long position of more than $12 billion. The Backtest Engine shows that over the past 10 years, when hedgers were net long more than $10 billion of major equity index futures, the S&P 500 was higher 3 months later after 57 out of 59 weeks, averaging 7.1%.

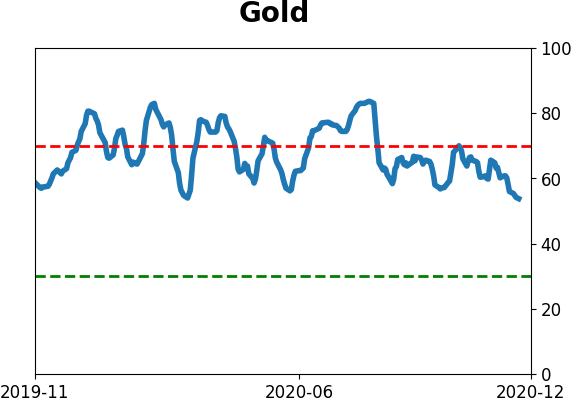

Gold's grip slips: Gold closed below its 200-day average for the first time in more than 6 months. We'll have more detail on this on Tuesday, but out of the 18 times since 1975 when gold ended a streak of more than 100 days above its average, it never lost more than 7% over the next 2 months. Mostly, it showed decent gains as the ebb in momentum led to buy-the-dippers getting interested.

Bottom Line:

- The market environment is pristine, but with near-historic optimism, gains tend to be muted, with a high probability of being reversed at some point over the ensuing weeks.

|

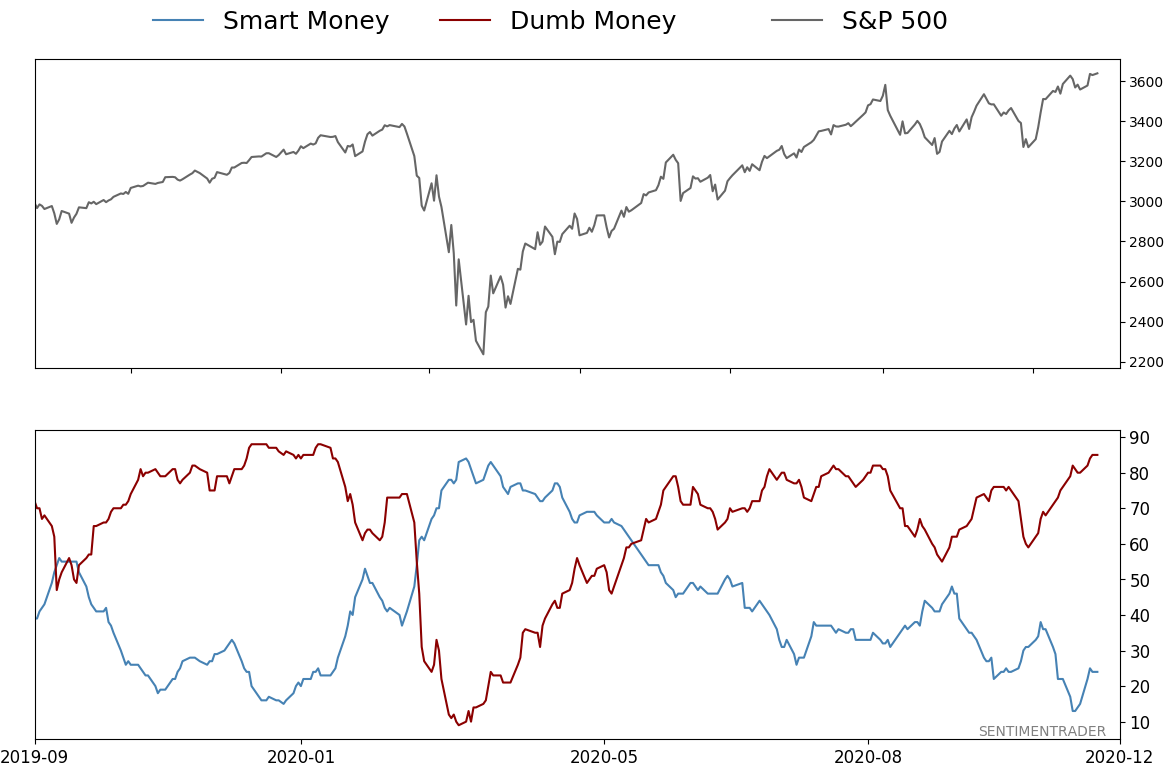

Smart / Dumb Money Confidence

|

Smart Money Confidence: 24%

Dumb Money Confidence: 85%

|

|

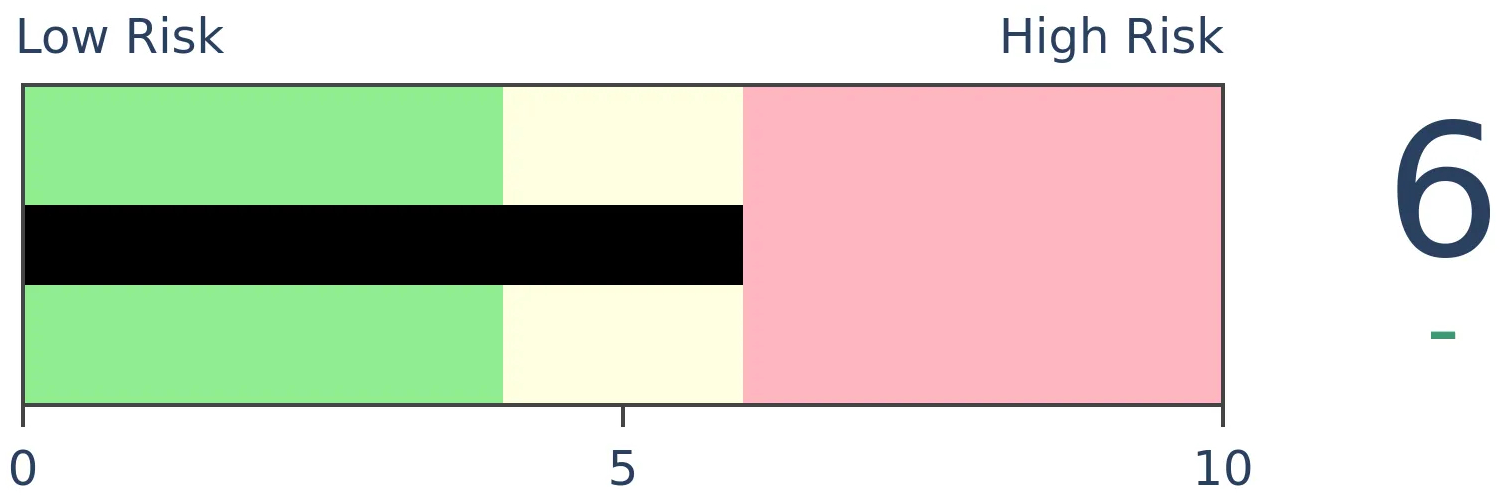

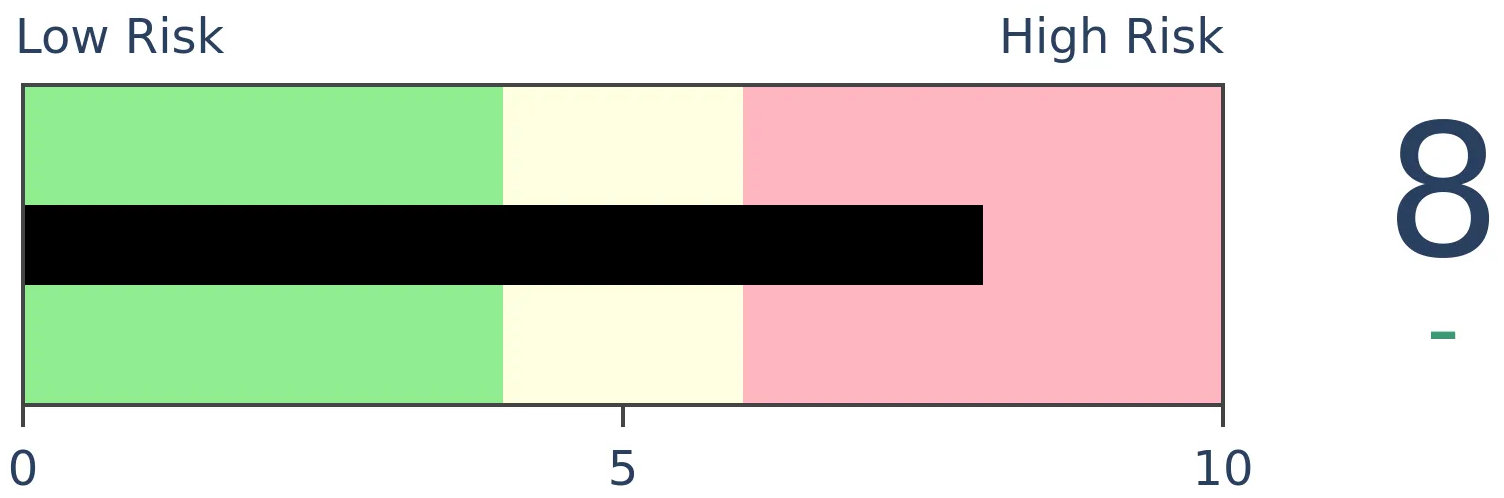

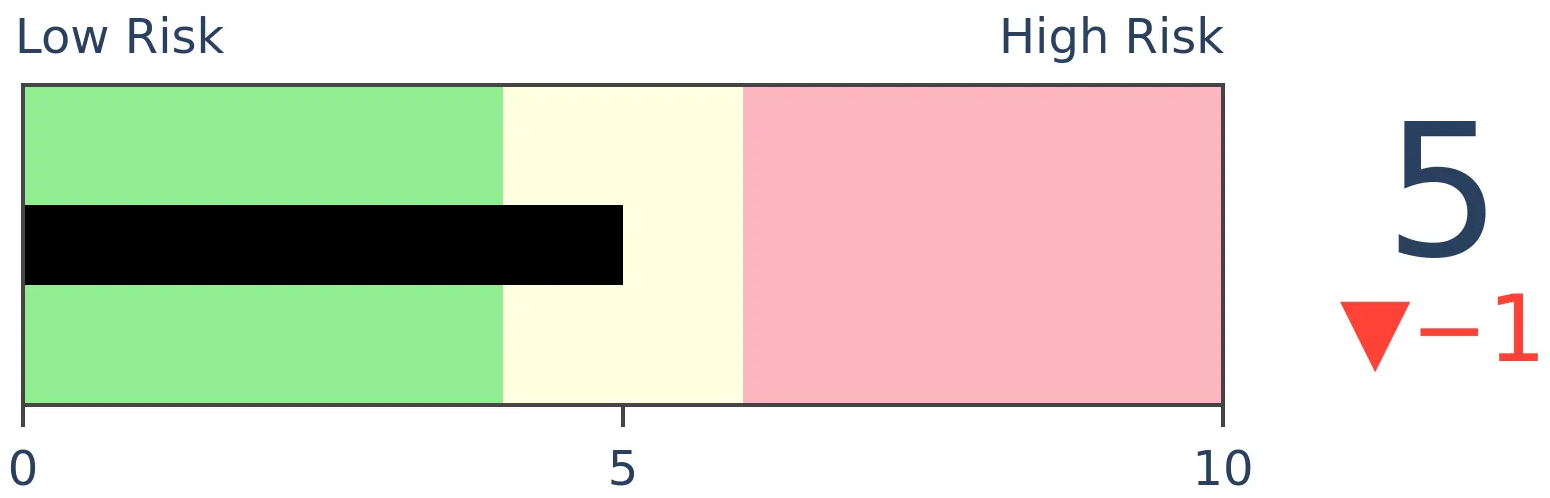

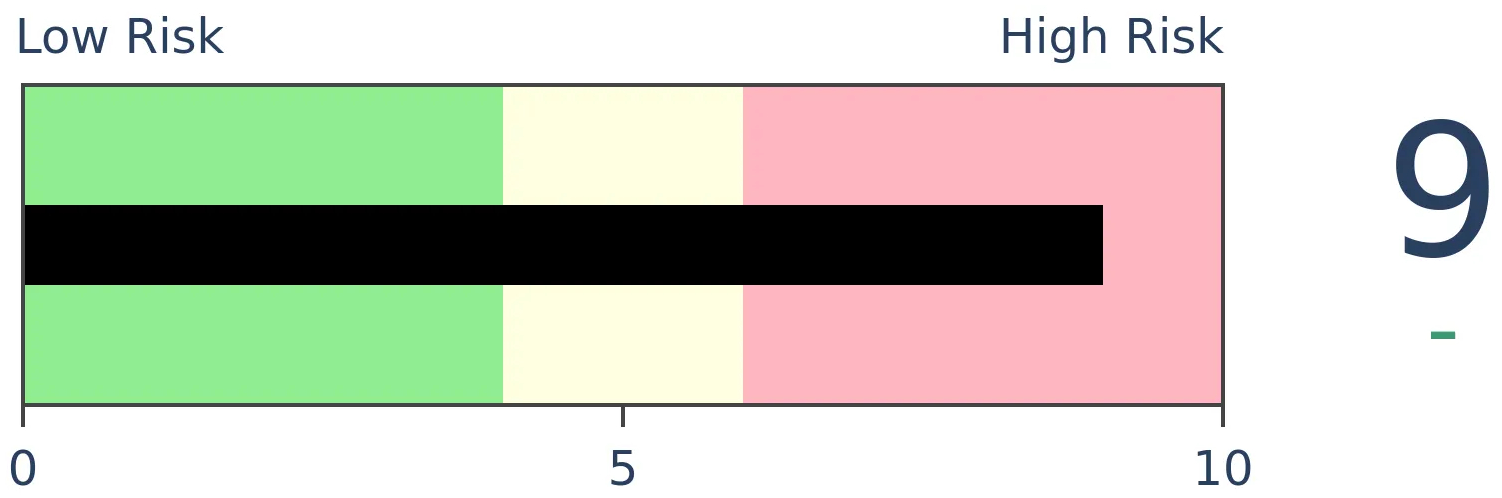

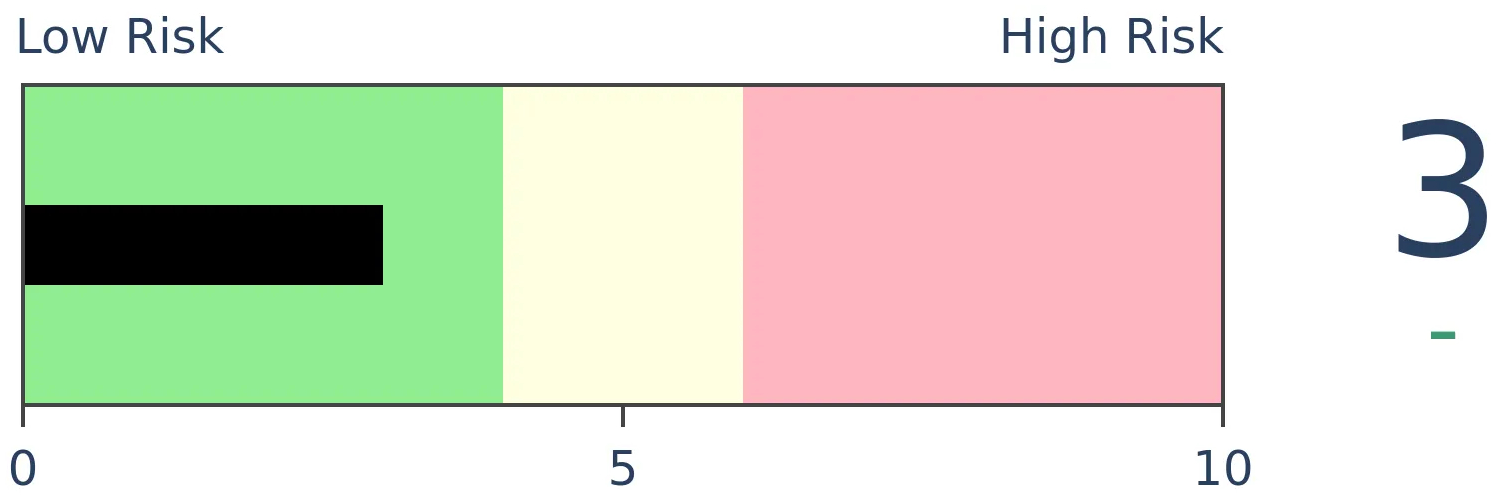

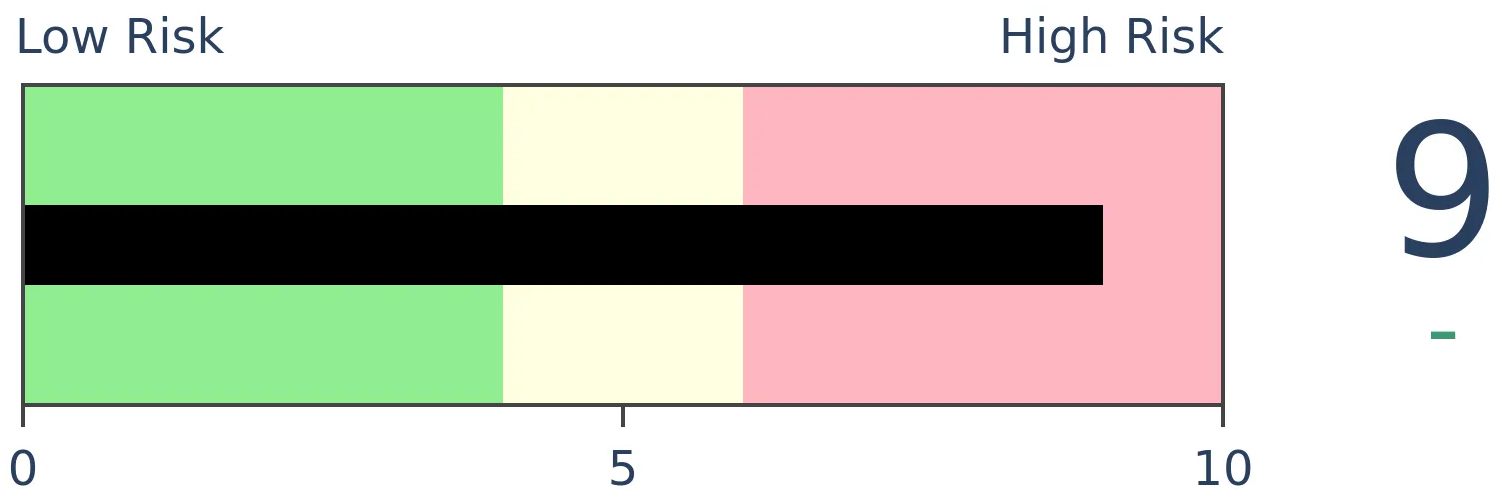

Risk Levels

Stocks Short-Term

|

Stocks Medium-Term

|

|

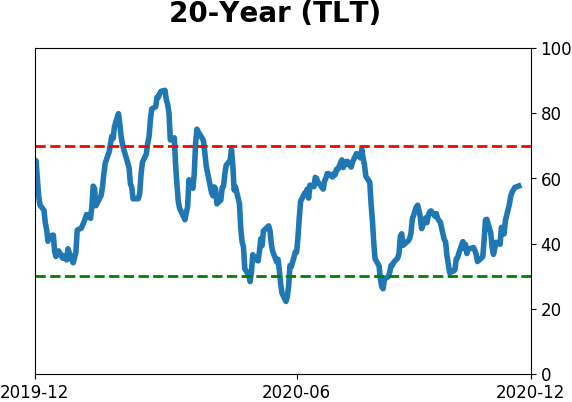

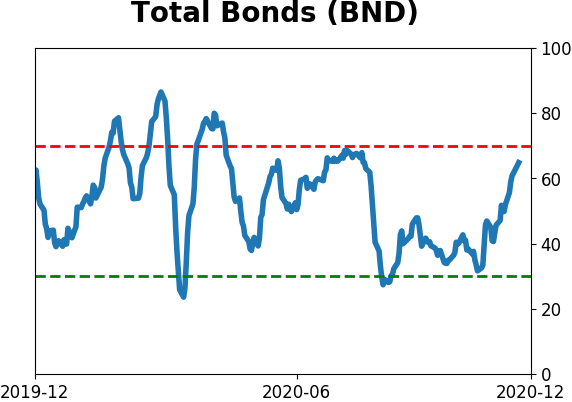

Bonds

|

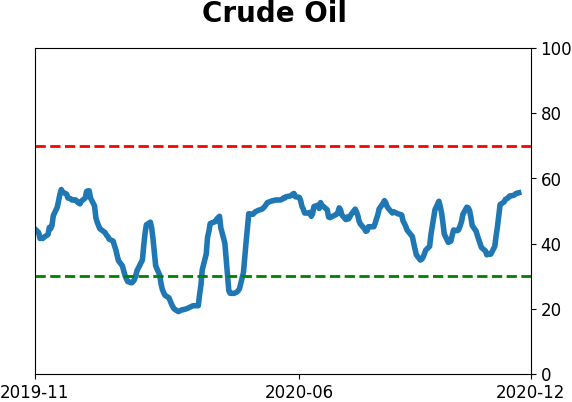

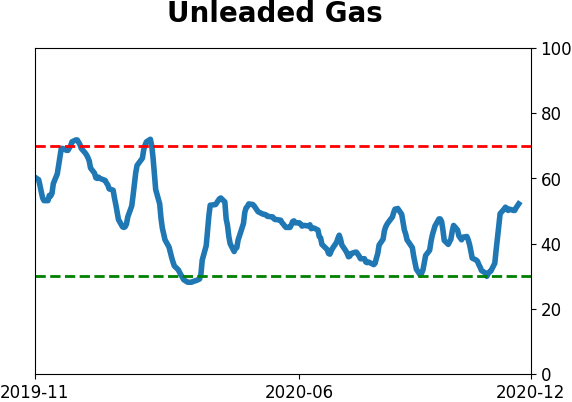

Crude Oil

|

|

Gold

|

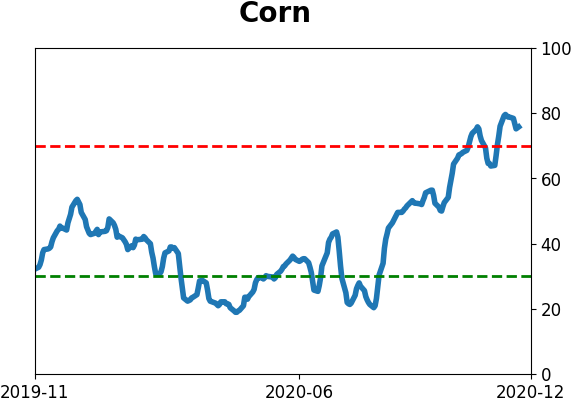

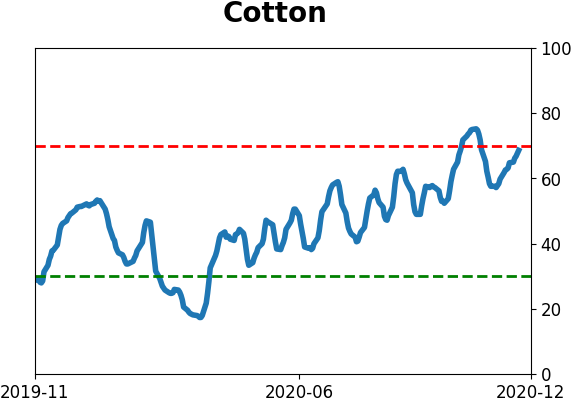

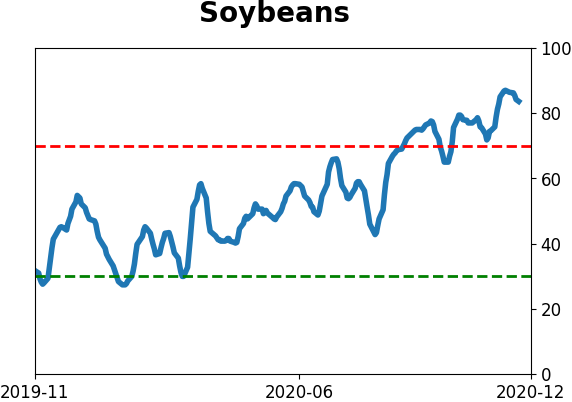

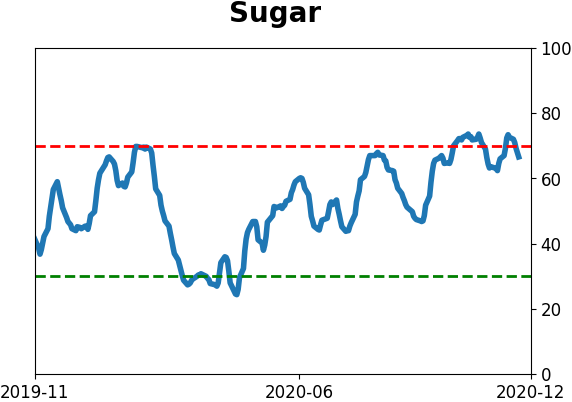

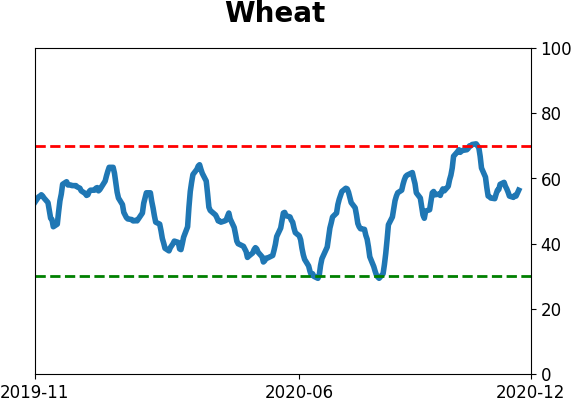

Agriculture

|

|

Research

BOTTOM LINE

Eric made some updates to the site over the weekend, so you'll see a couple of new things. The first is an alert button, which will show any new messages we've posted to the site. These could be anything from new content to site updates to data issues. They'll clear once you click the bell icon on any device.

FORECAST / TIMEFRAME

None

|

Eric made some updates to the site over the weekend, so you'll see a couple of new things. The first is an alert button, which will show any new messages we've posted to the site. These could be anything from new content to site updates to data issues. They'll clear once you click the bell icon on any device.

The other is "Premium Minutes." I've published brief intraday notes off and on since starting the service in 2001, and it was always clunky. With improvements that Eric has made, we're now able to do it in a more streamlined manner.

These are just quick, informal snippets, like a journal of anything that piques my interest. Some might turn into longer notes, while others are just things I'm watching. If you'd like to see a digest of them at the end of the day, you can receive that email. Currently, we're not emailing them as they're published, but if there is enough interest, we could enable that as well - it would be opt-in only, so not everyone is inundated with emails.

The content structure of the site is now:

Minutes - brief, informal snippets published throughout the day [premium]

Notes - longer-form research and studies [premium]

Reports - a daily summary of our indicators and models, along with 1-2 pieces of research as we've always done [basic and premium]

BOTTOM LINE

Options traders are supremely confident again, helping to trigger the most extremes among our indicators in 15 years. Forward returns tend to be muted after confidence like this. Momentum, breadth, and seasonality remain positive but that has helped less in the short-term.

FORECAST / TIMEFRAME

None

|

Overboard on options

Ever since options speculation reached a euphoric spasm in late August through early September, we've been closely watching this behavior.

It ebbed a bit in September as many of the call options lost all their value. It has been returning in recent weeks and the holiday-shortened upside bias led to more of the same.

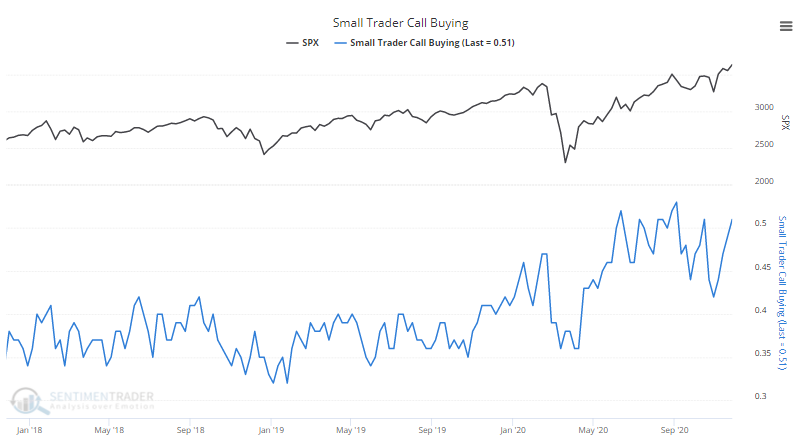

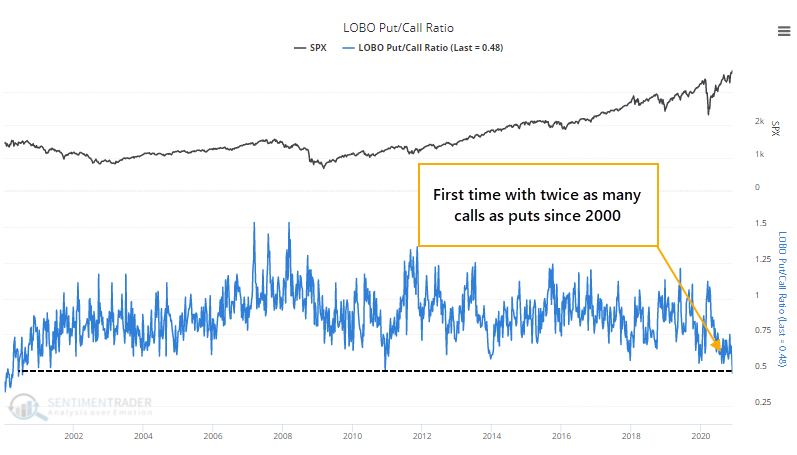

The smallest of traders spent more than 50% of their volume last week buying speculative call options. That has been exceeded by only a few weeks in recent months (and hadn't been exceeded by any week since the year 2000).

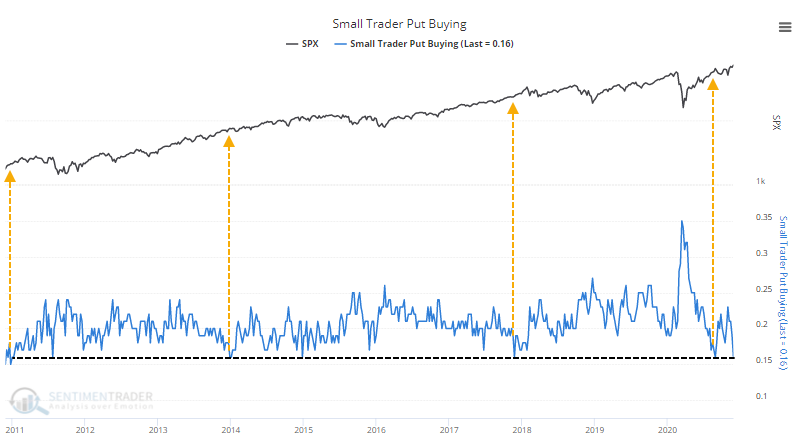

A change from recent weeks is that they also pulled back heavily on buying protective put options. Put buying made up only 16% of the volume among these traders, among the lowest in a decade.

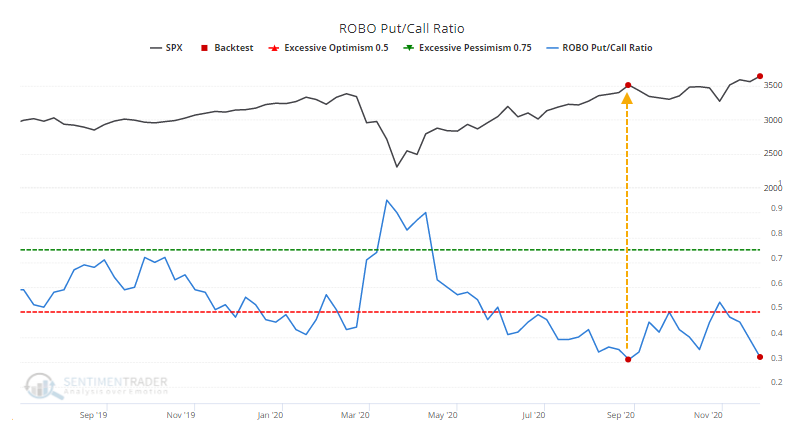

All of this activity means that the ROBO Put/Call Ratio is showing that small traders bought to open more than twice as many calls as puts, a rarely-seen level of speculative fervor.

Only late August can compare.

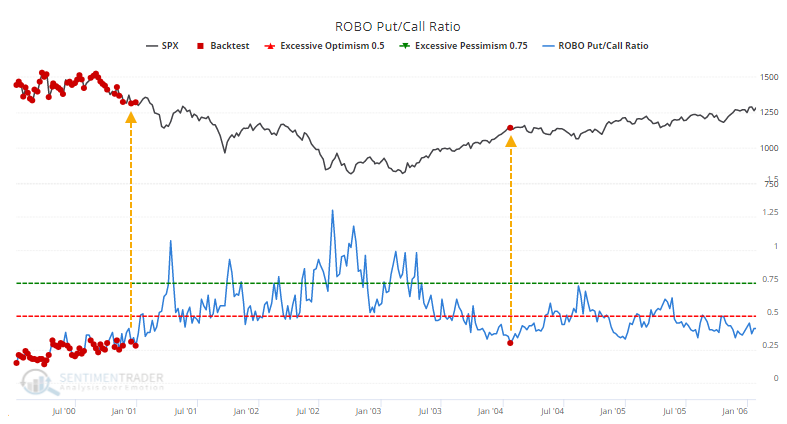

Prior to that, only many of the weeks in the year 2000, then again a single week in 2004 have matched this level of confidence.

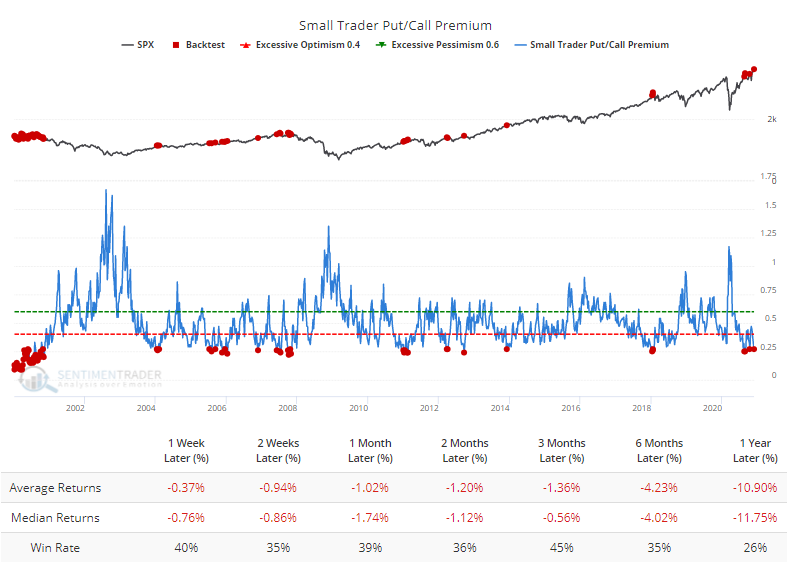

Because traders bought so many calls and were willing to pay up for them, the Small Trader Put/Call Premium ratio plunged to one of the lowest levels on record. The Backtest Engine shows poor returns after similarly low readings.

Remarkably, out of 75 weeks that showed this low of a ratio, 74 of them saw a negative return in the S&P 500 at some point in the weeks and months ahead. Only a reading in early January 2011 witnessed the S&P rise uninterrupted going forward, and even that was just barely.

It's not just the smallest of traders feeling their speculative juices, either. The largest of traders, those trading 50 contracts or more, also joined the party.

Last week, they bought twice as many call options as put options - the first time since 2000 they've done so.

The most extremes in 15 years

Options activity is but one of the many extremes that our indicators are showing. So many, in fact, that an average of more than 55% of the core indicators have been in extreme territory over the past week, the most in 15 years.

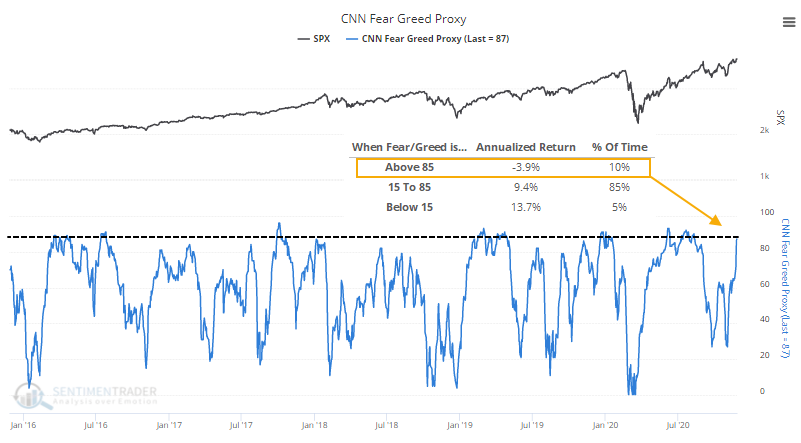

One of them is our proxy for the Fear & Greed model published by CNN. For the first time in months, it's in truly extreme territory.

When it's been above 85, the S&P 500 has returned an annualized -3.9%.

Momentum, seasonality, and perky small-caps

Always when we're dealing with extreme sentiment, we also have to consider momentum. When optimism abounds, it is often precipitated by positive momentum, and vice-versa. That's why we spend almost as much time looking at the health and quality of participation under the surface as we do measuring sentiment. Nothing can cause a sentiment extreme to fail quite like momentum.

And we've been seeing very healthy participation and momentum, as outlined multiple times in recent weeks. There has been a series of thrusts and breakouts, with some of the best underlying breadth readings we've seen in years. Decades, even. That was not the case in August.

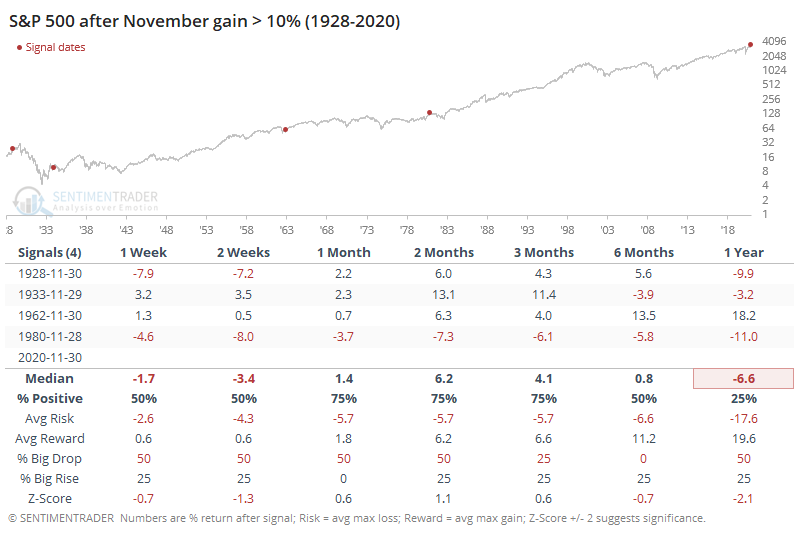

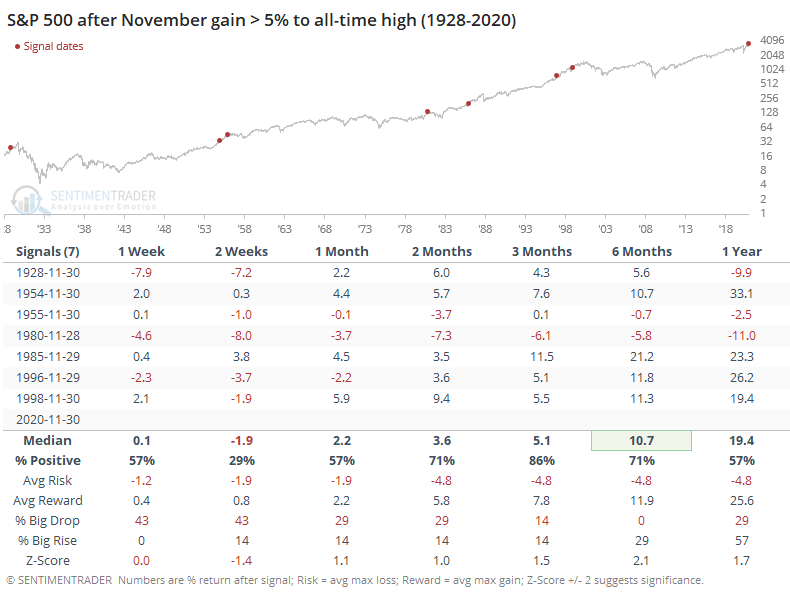

We're also in the midst of what has traditionally been a positive time of year. This will be one of the few times in history when the S&P 500 gained more than 10% during November.

Even 5% gains during this month have been rare, at least when the S&P was trading at a record high monthly close at the time. It didn't prevent losses in the weeks ahead, but they did tend to be relatively contained.

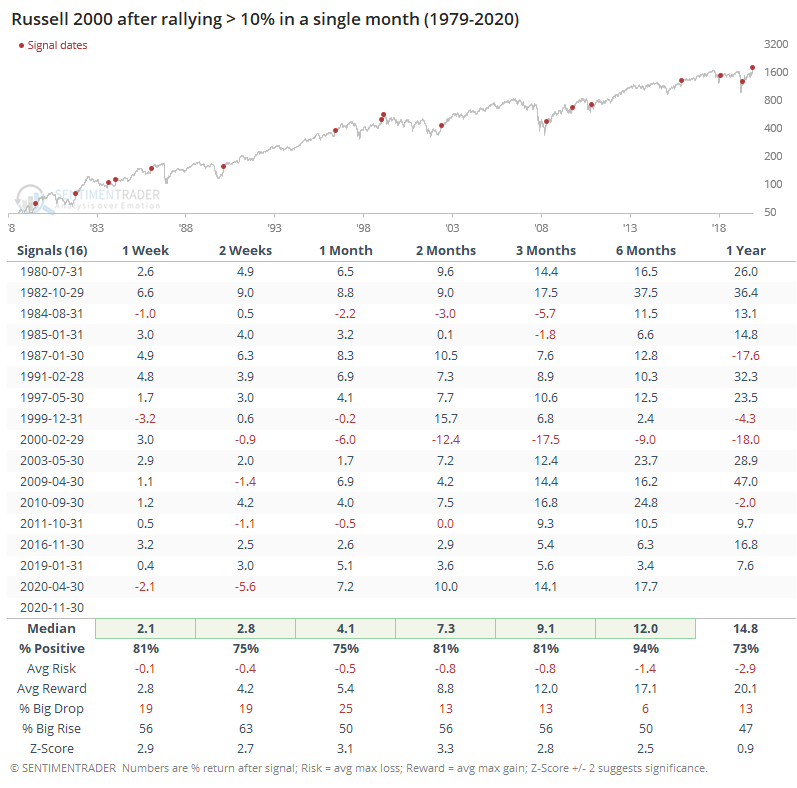

It wasn't just the large-caps in the S&P 500 that have been rallying, of course. The impressive breadth figures throughout much of November reflected broad participation, which means smaller-cap stocks. The Russell 2000 is on track for its best month ever, but even rallies half as large have preceded further gains almost without exception.

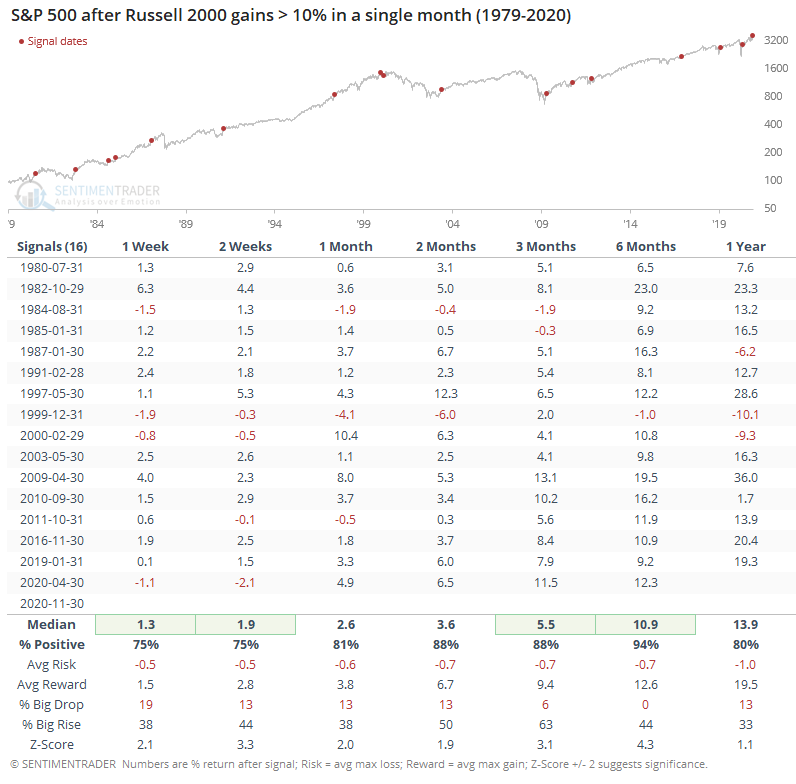

In some respects, big months for small-caps have been even more positive for the S&P 500.

When the Russell jumped 10% or more in a single month, over the next 6 months, the S&P suffered only a single (small) loss, and the risk/reward skew was tilted heavily to the upside, as was the probability of a big rise versus big drop (see here for definitions).

Volatility drip

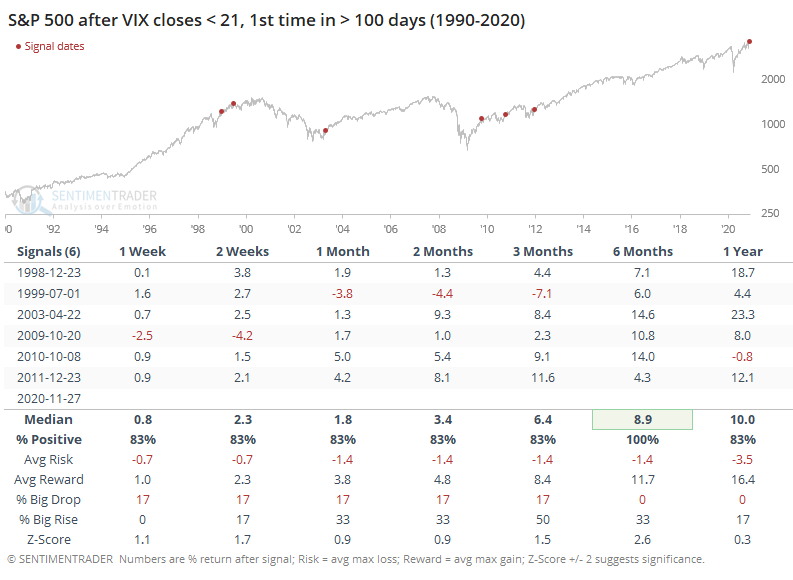

The consistent rally, coupled with what is usually lower volume and volatility during the holiday season, has caused traders to price in lower daily moves over the next 30 days. The VIX finally closed below 21, which we pointed out on Twitter would end the 3rd-longest streak since 1990.

Other times the VIX ended a streak above 21 that lasted more than 100 sessions, the S&P 500 continued to rally over the next 6 months.

Piecing it together

In years past, we used to be able to see a true sentiment extreme and be reasonably confident that it would soon be reflected in forward stock returns. When investors became too pessimistic, then buy; when too optimistic, then sell. In recent years, that has become much less consistent. Sometimes, an extreme will help trigger a counter-move in the market almost immediately, other times it will take months. It's never been 100% reliable, but more and more, prices have continued to move for weeks or even months before reacting.

I don't really care about the reason, since it's all conjecture and nobody really knows anyway. Maybe it's the trend toward passive funds, or Federal Reserve intervention, or a new cadre of investors. Who knows, it is what it is. Considering recent history, it has usually been a mistake to sell just because sentiment is overly optimistic, which it clearly is. A reasonable, and simple, trigger to become more defensive in the face of sentiment like this watching for indexes to fall below their 20-day moving averages. When that happens, following a sentiment extreme, then we've typically entered a much more choppy environment. Given the momentum and breadth we've seen, however, the probability that a move like that will lead to a large and sustained breakdown seems remote for now.

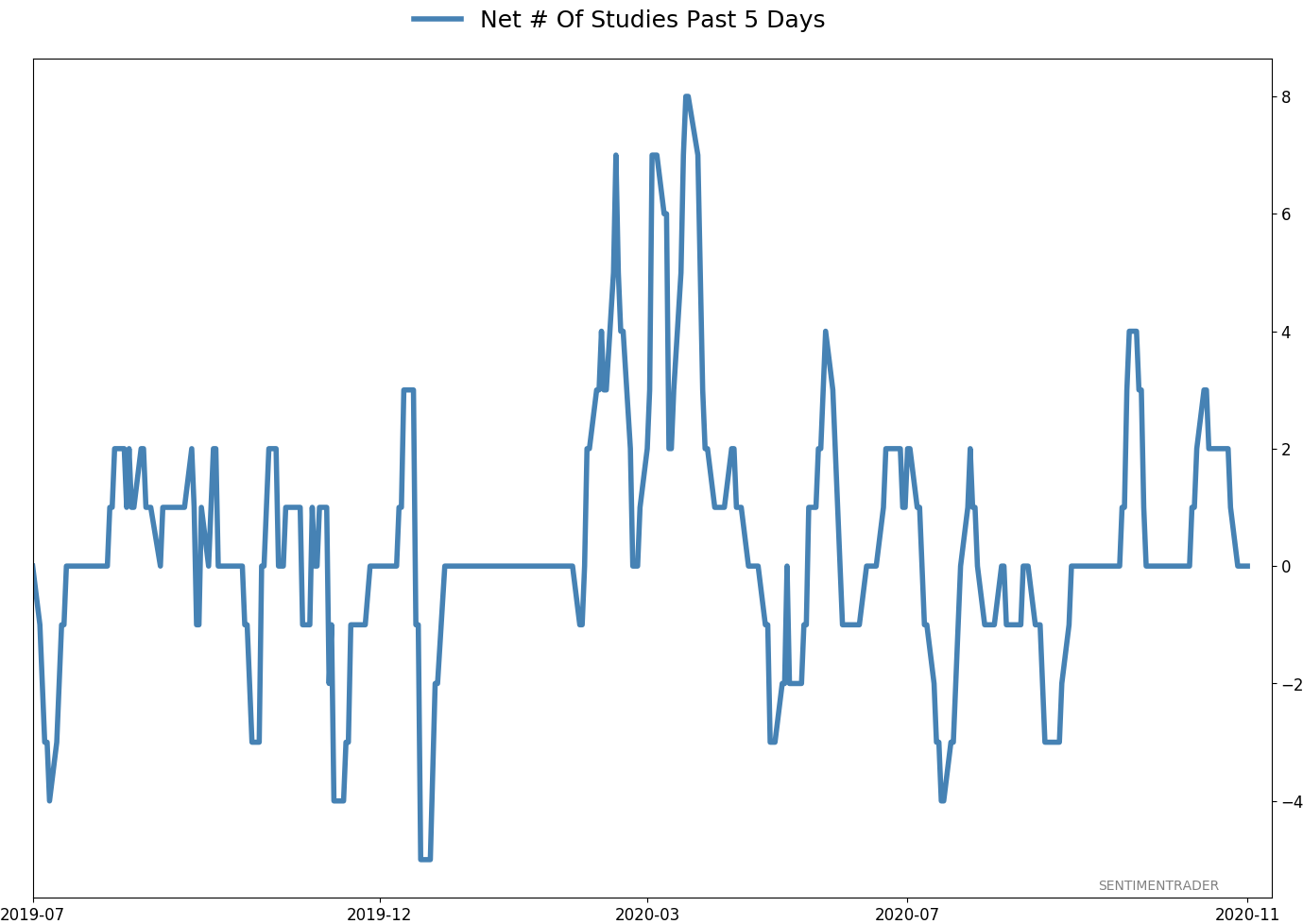

Active Studies

| Time Frame | Bullish | Bearish | | Short-Term | 0 | 0 | | Medium-Term | 5 | 8 | | Long-Term | 51 | 2 |

|

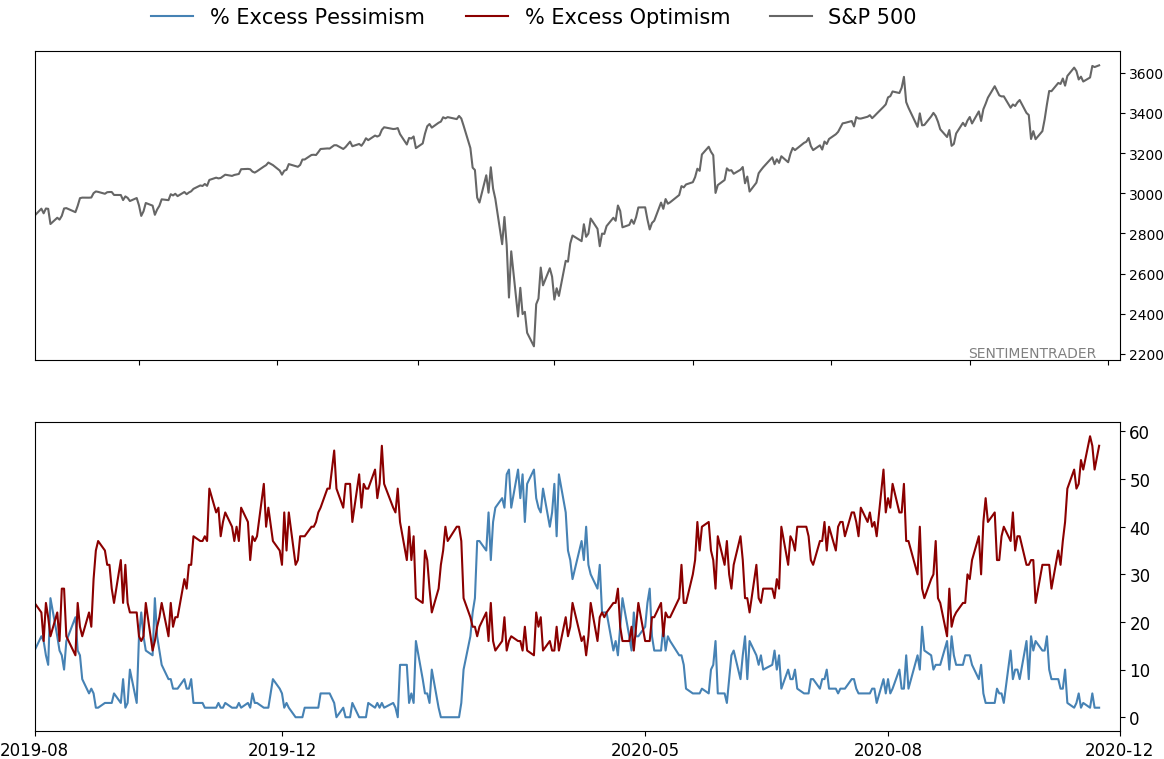

Indicators at Extremes

% Showing Pessimism: 2%

Bullish for Stocks

VIX

|

|

Portfolio

| Position | Description | Weight % | Added / Reduced | Date | | Stocks | 15.6% RSP, 10.1% VWO, 7.5% XLE, 5.1% PSCE | 38.2 | Added 5% | 2020-10-15 | | Bonds | 10% BND, 10% SCHP, 10% ANGL | 29.7 | Reduced 0.1% | 2020-10-02 | | Commodities | GCC | 2.4 | Reduced 2.1%

| 2020-09-04 | | Precious Metals | GDX | 4.7 | Added 5% | 2020-09-09 | | Special Situations | | 0.0 | Reduced 5% | 2020-10-02 | | Cash | | 25.0 | | |

|

Updates (Changes made today are underlined)

After the September swoon wrung some of the worst of the speculation out of stocks, there are some signs that it's returning, especially in the options market. It's helped to push Dumb Money Confidence above 70%. A big difference between now and August is that in August, there was a multitude of days with exceptionally odd breadth readings. Some of the biggest stocks were masking underlying weakness. Combined with heavy speculative activity, it was a dangerous setup. Now, we've seen very strong internal strength, in the broad market, as well as tech and small-cap stocks. Prior signals almost invariably led to higher prices. That's hard to square with the idea that forward returns tend to be subdued when Confidence is high, but that's less reliable during healthy market conditions, which we're seeing now (for the most part). I added some risk with small-cap energy stocks, due to an increasing number of positive signs in both small-caps and energy. This is intended as a long-term position.

RETURN YTD: 4.6% 2019: 12.6%, 2018: 0.6%, 2017: 3.8%, 2016: 17.1%, 2015: 9.2%, 2014: 14.5%, 2013: 2.2%, 2012: 10.8%, 2011: 16.5%, 2010: 15.3%, 2009: 23.9%, 2008: 16.2%, 2007: 7.8%

|

|

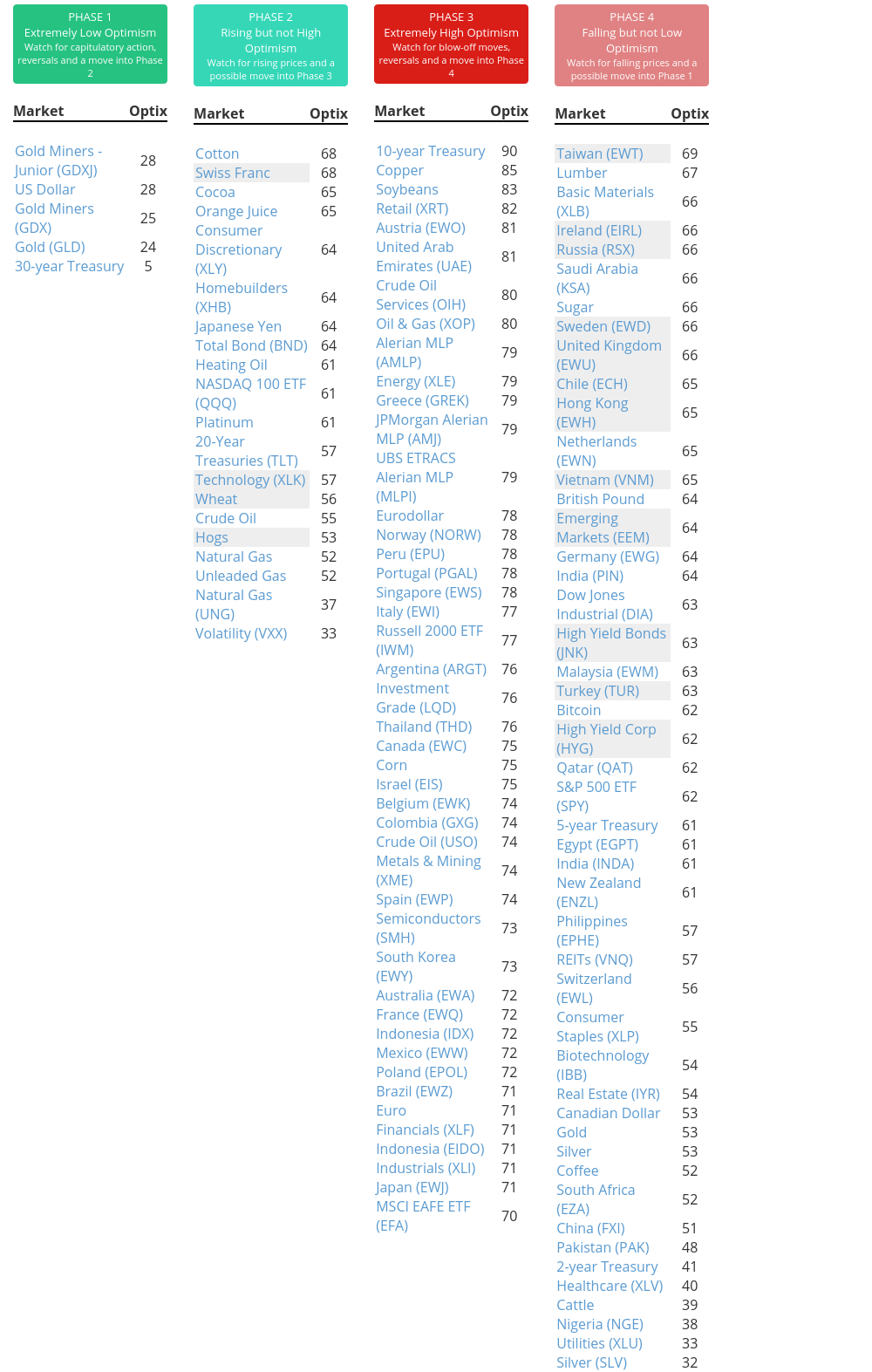

Phase Table

Ranks

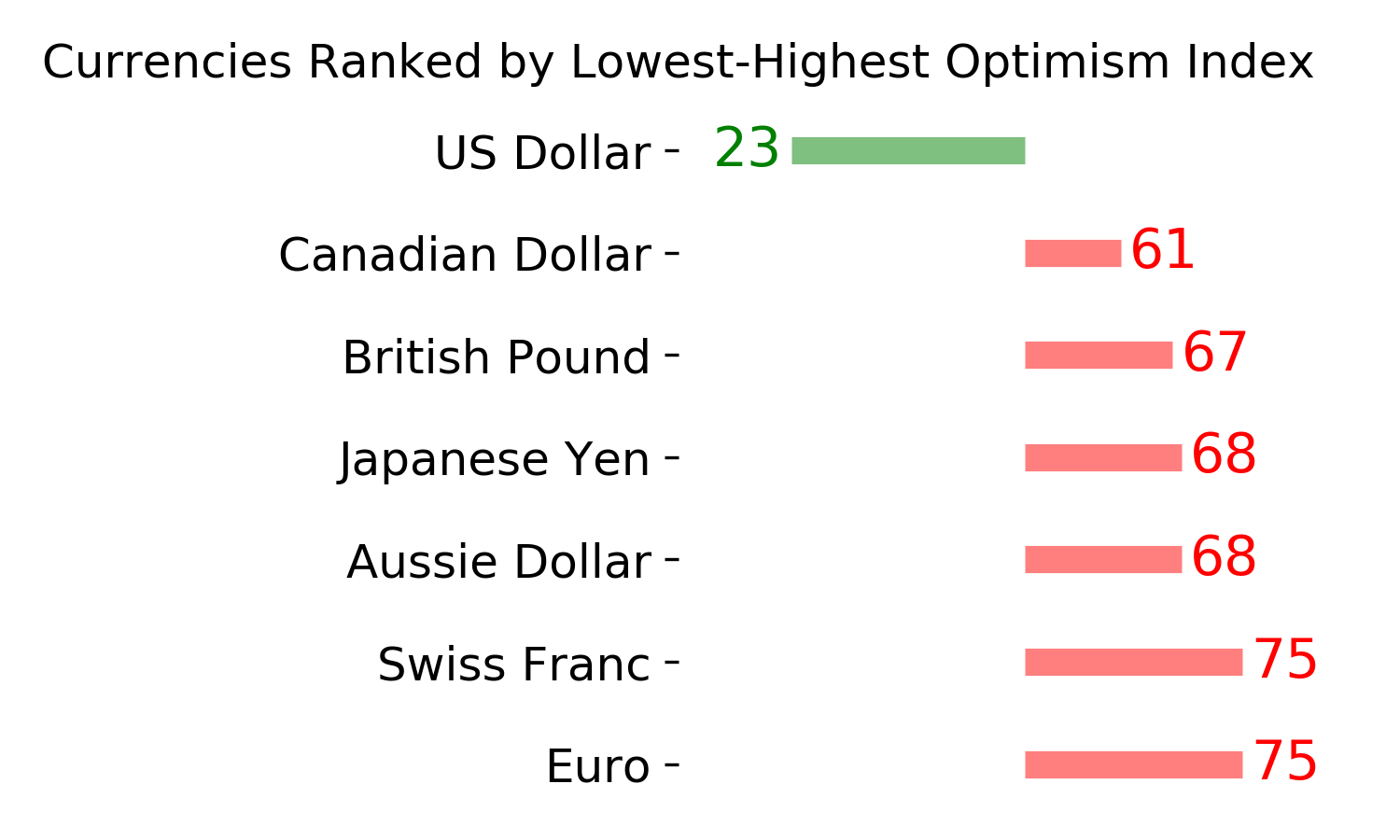

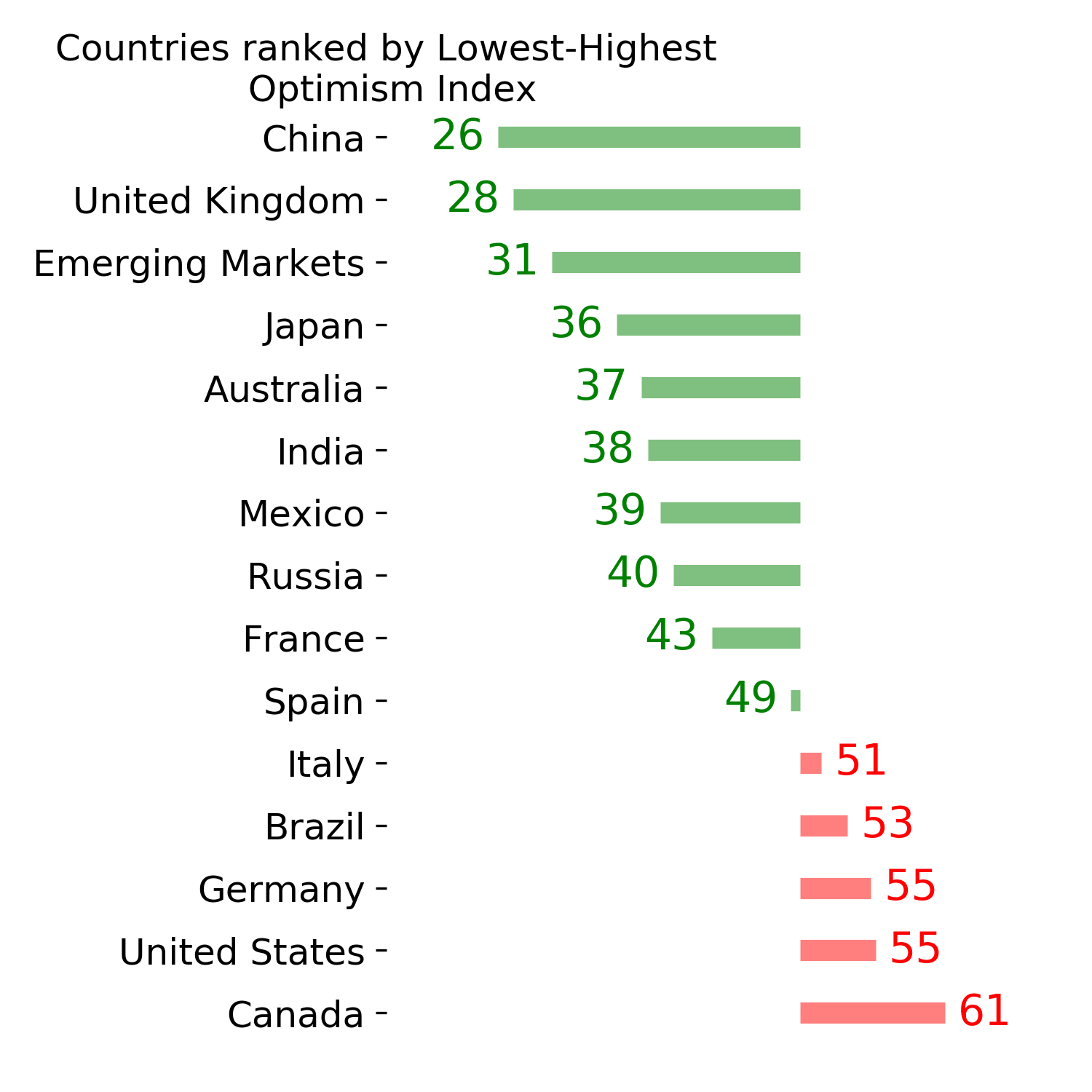

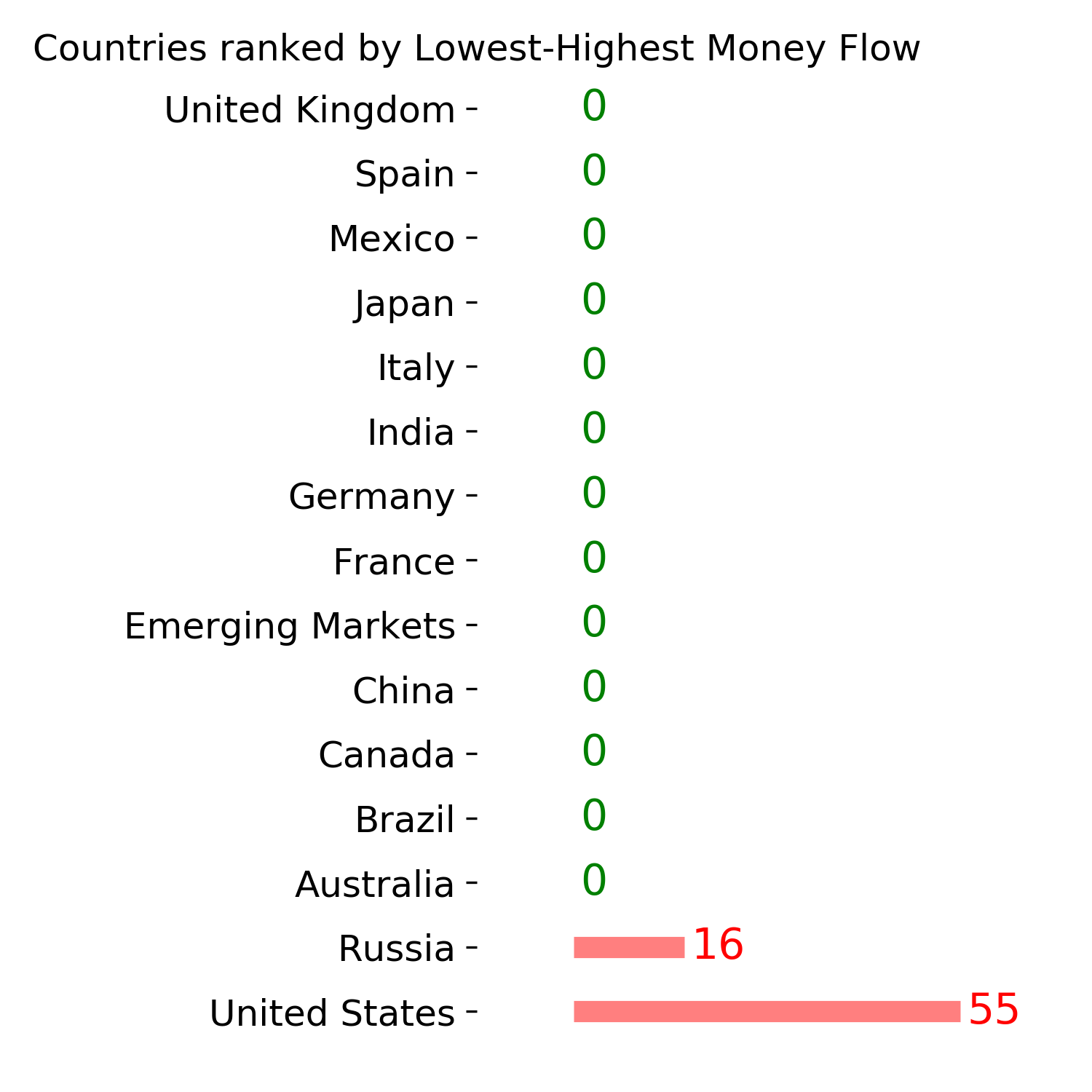

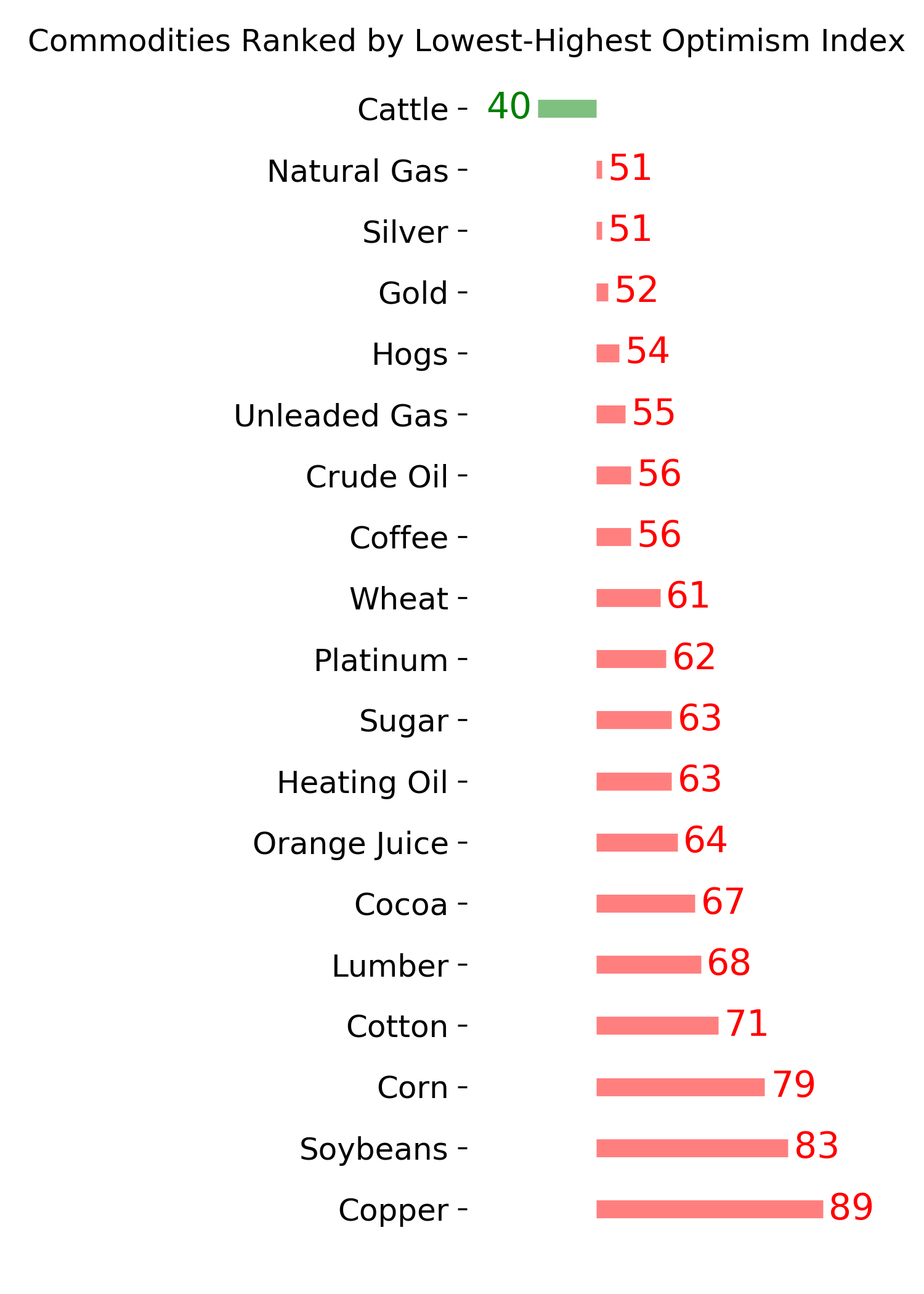

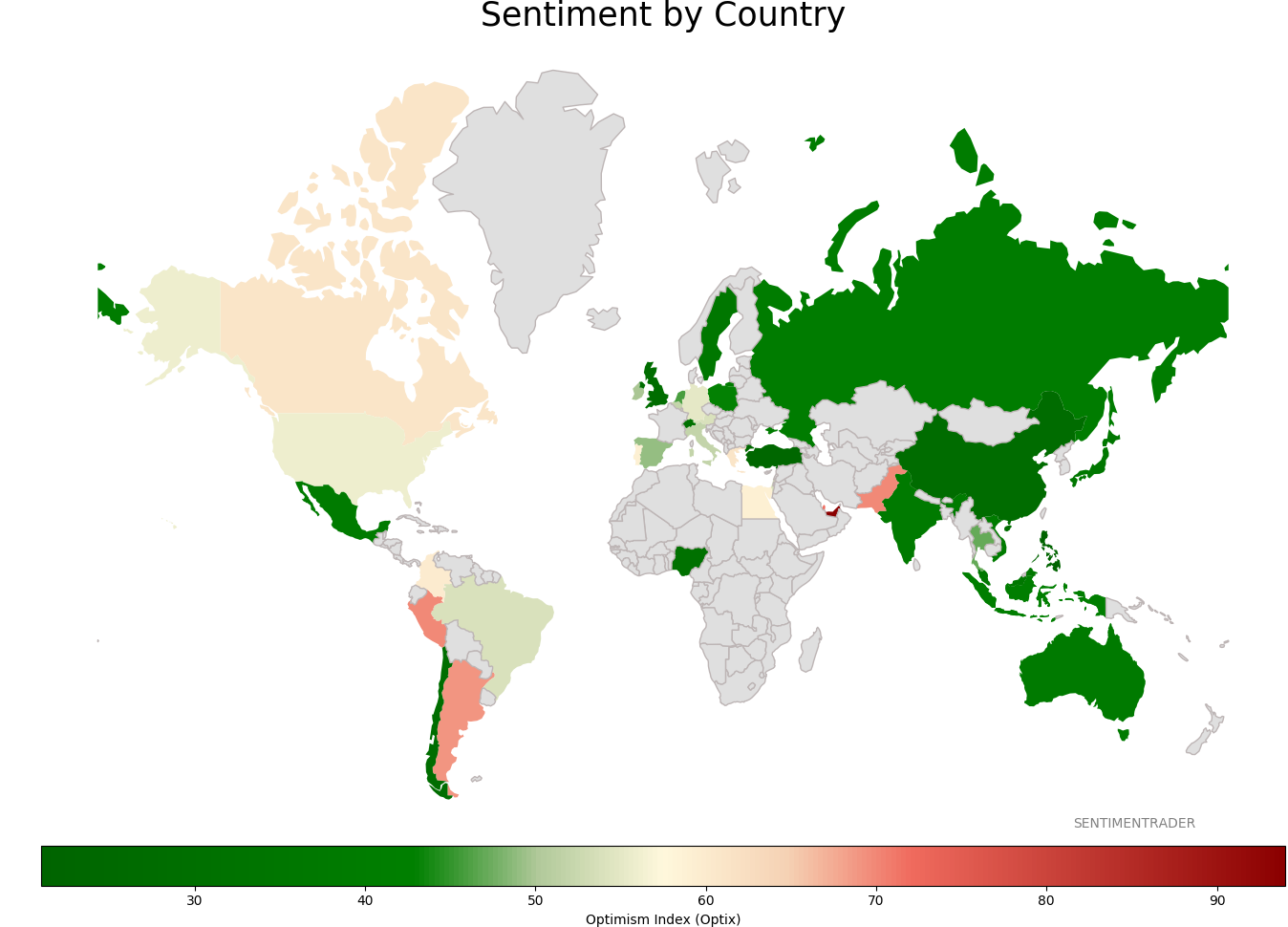

Sentiment Around The World

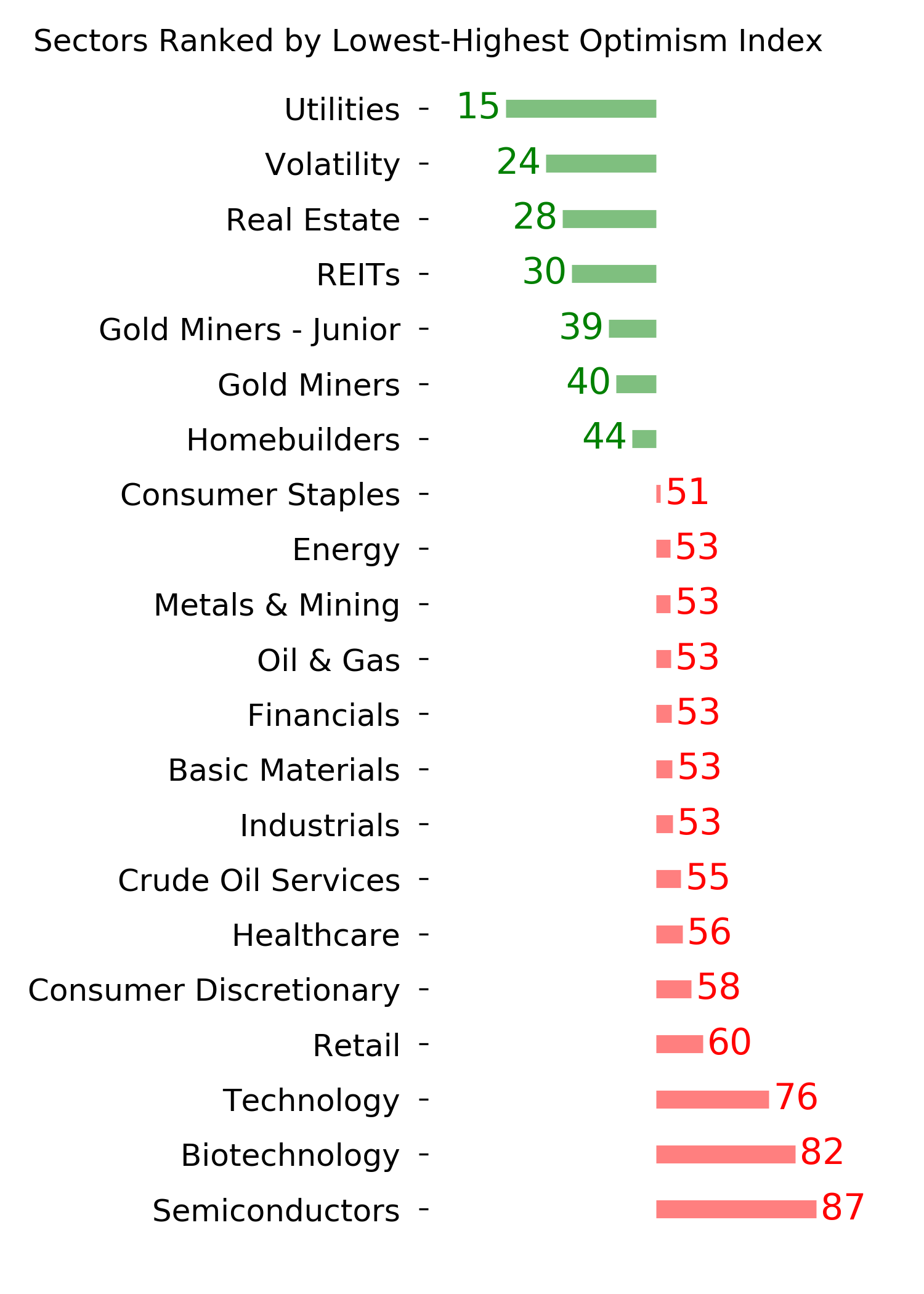

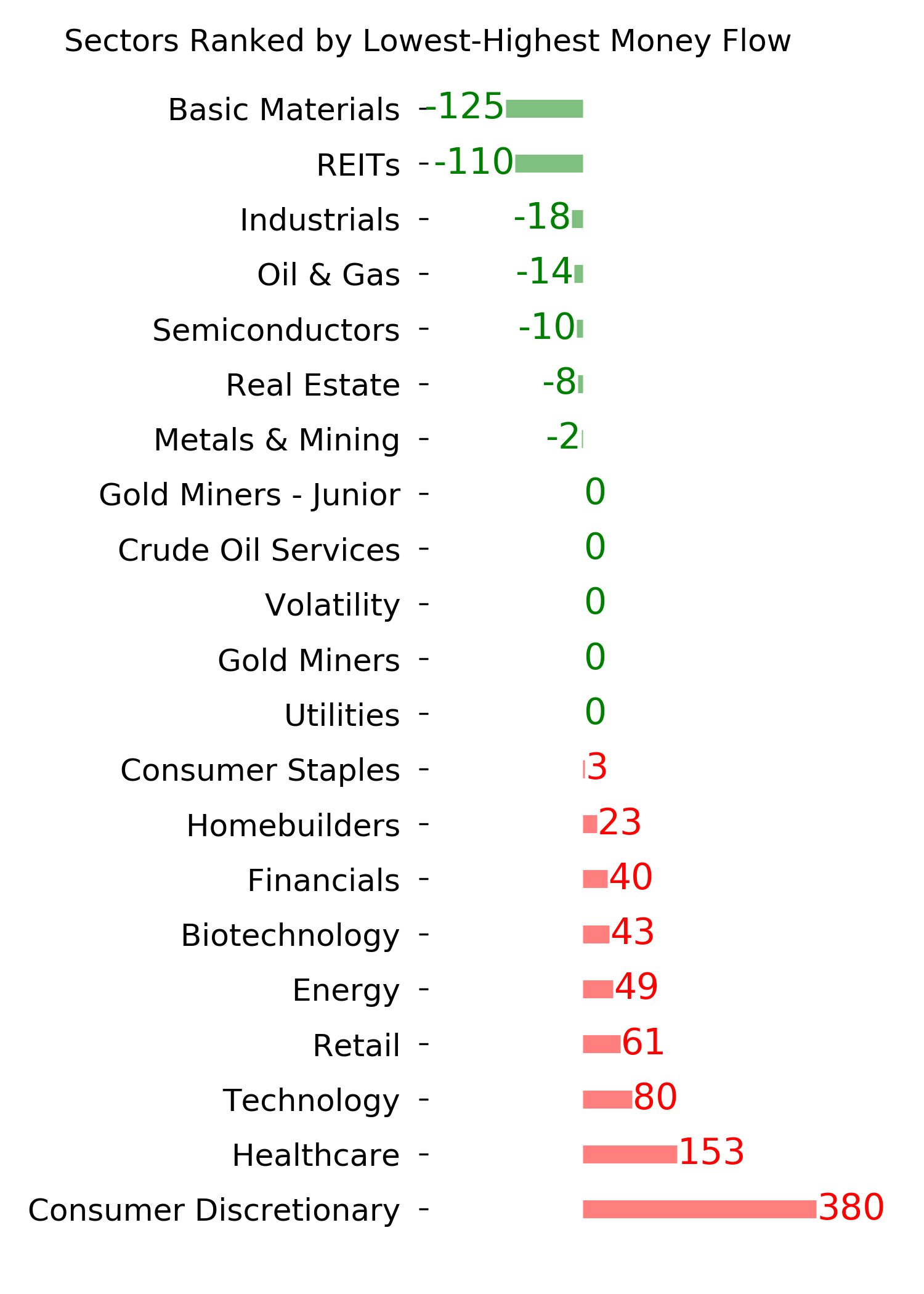

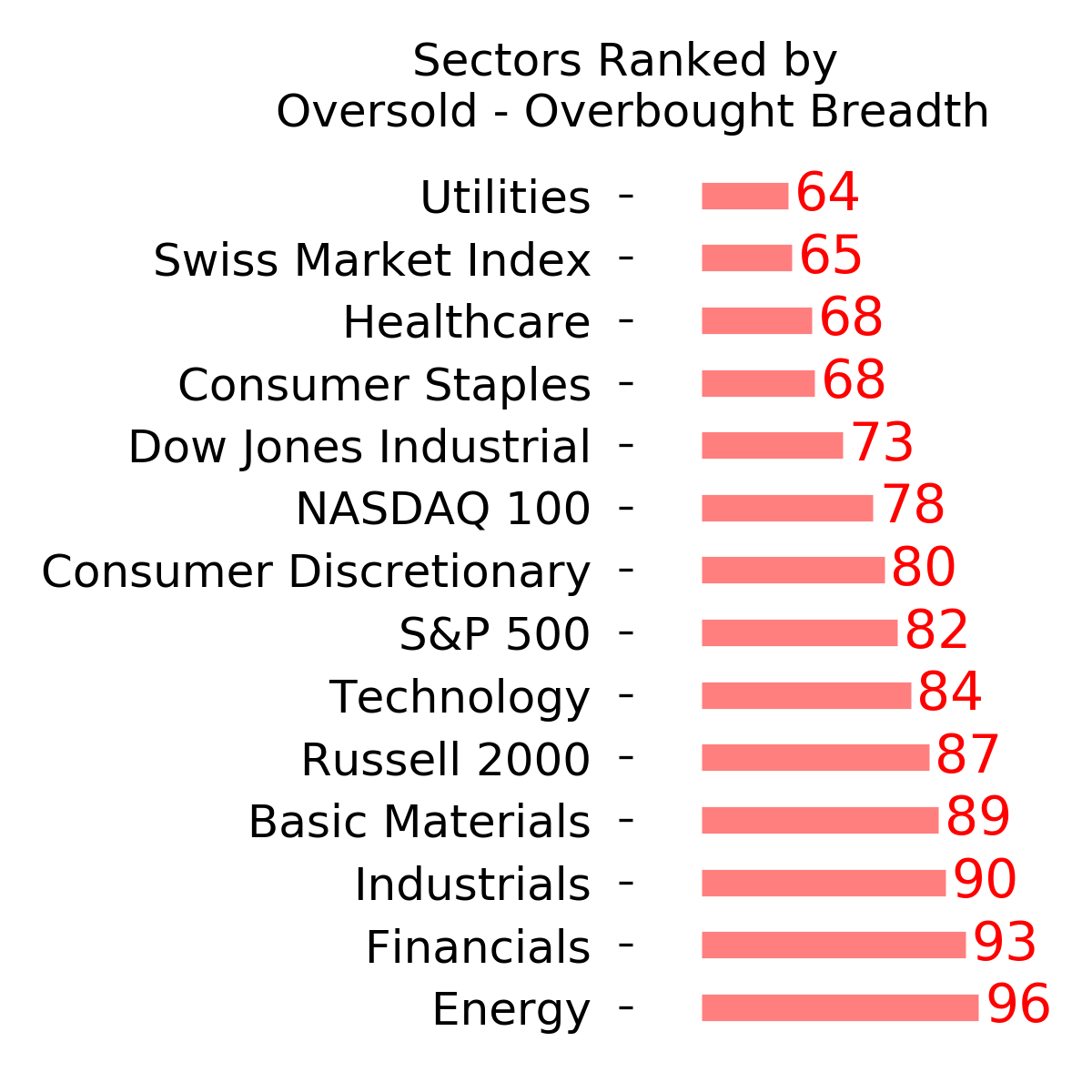

Optimism Index Thumbnails

|

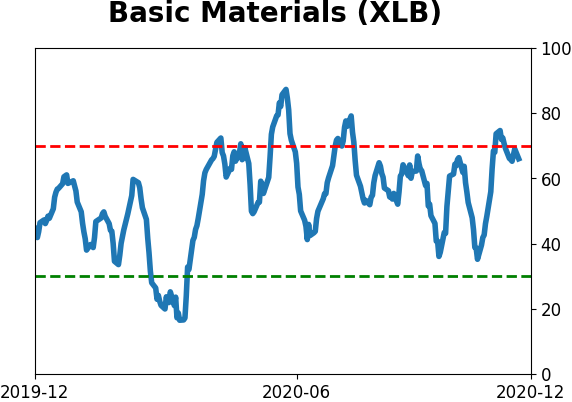

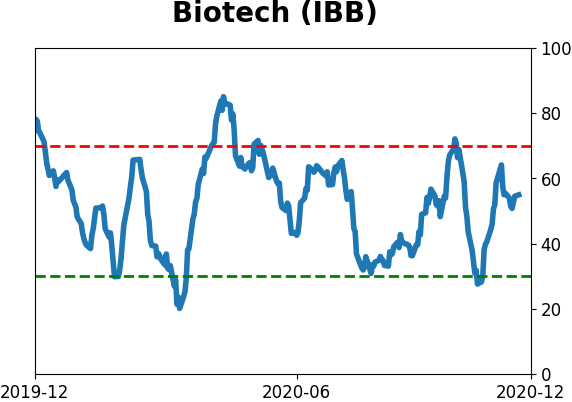

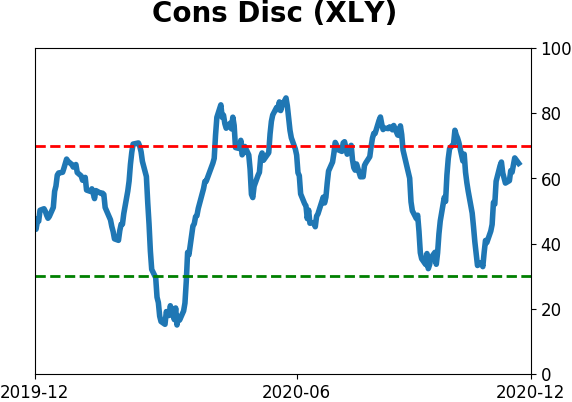

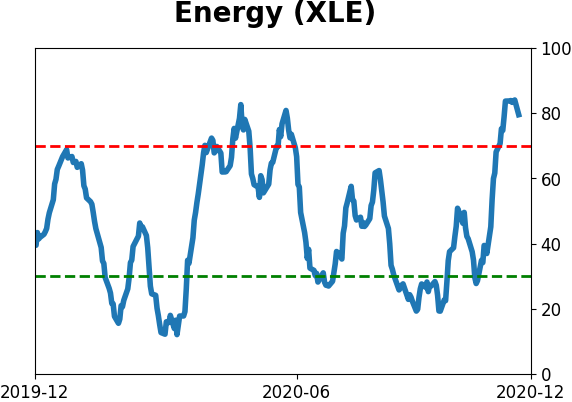

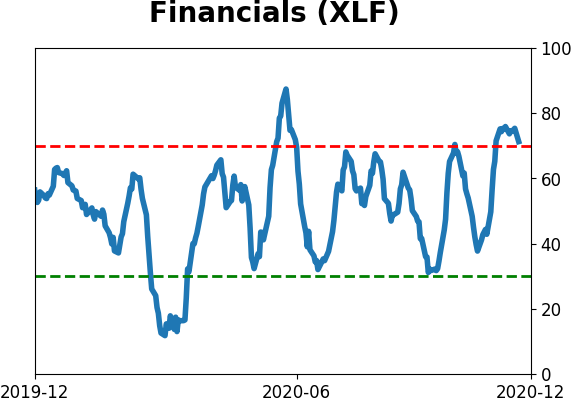

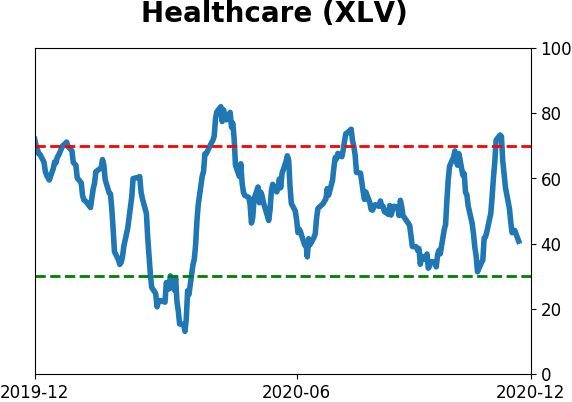

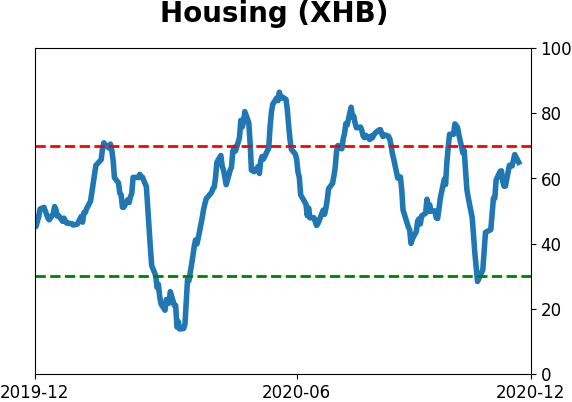

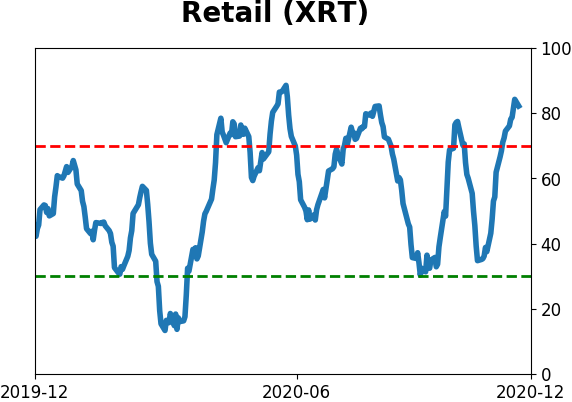

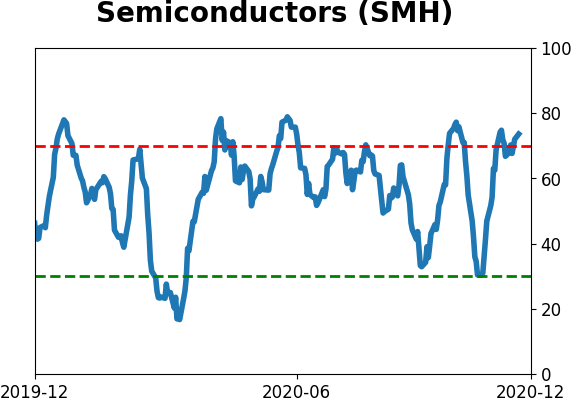

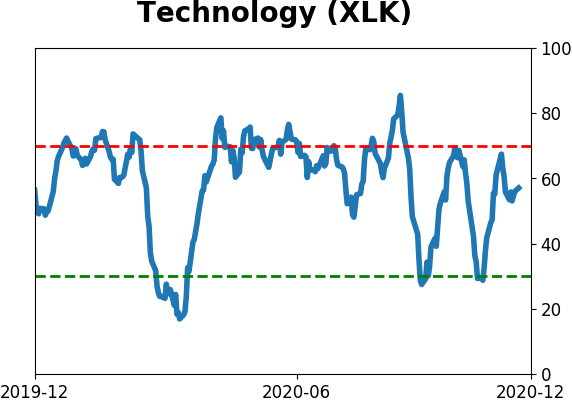

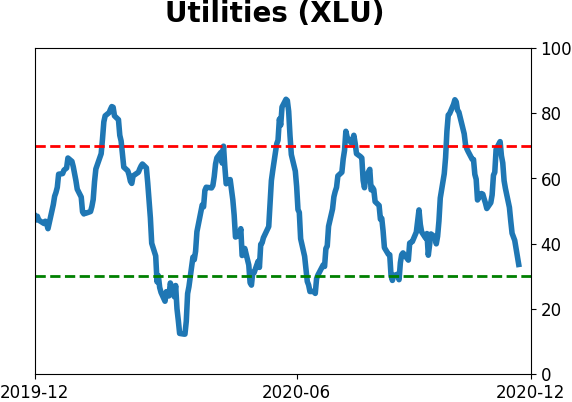

Sector ETF's - 10-Day Moving Average

|

|

|

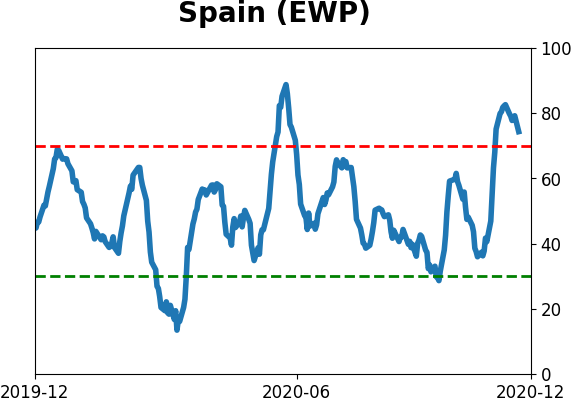

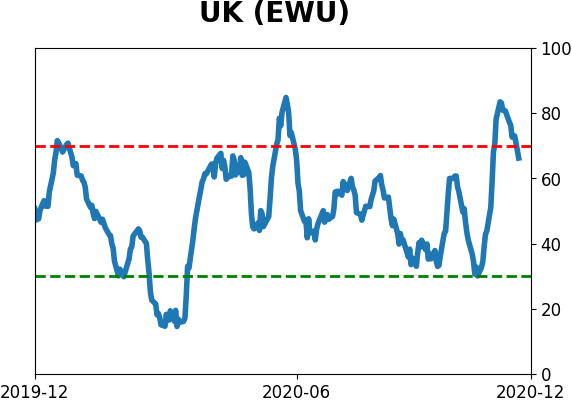

Country ETF's - 10-Day Moving Average

|

|

|

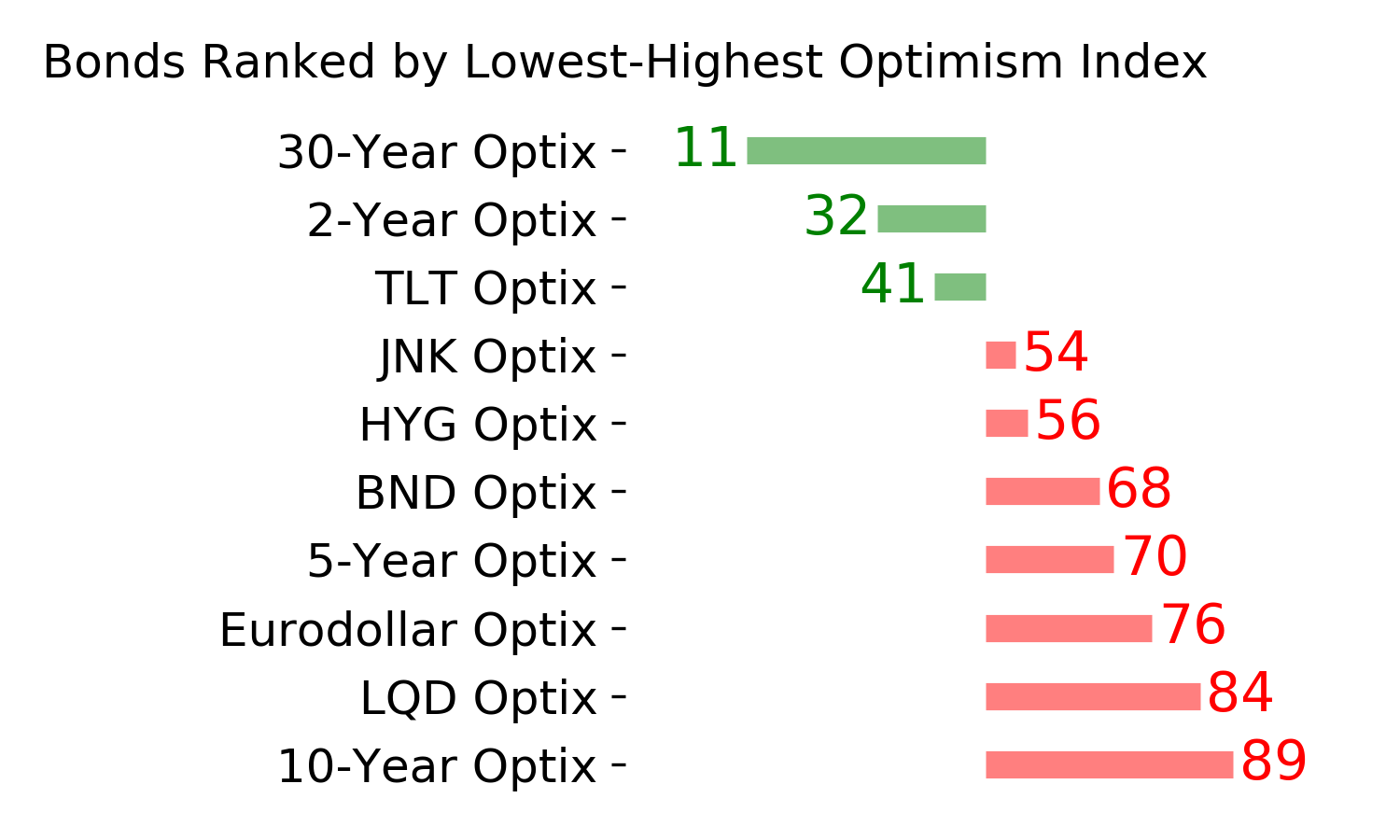

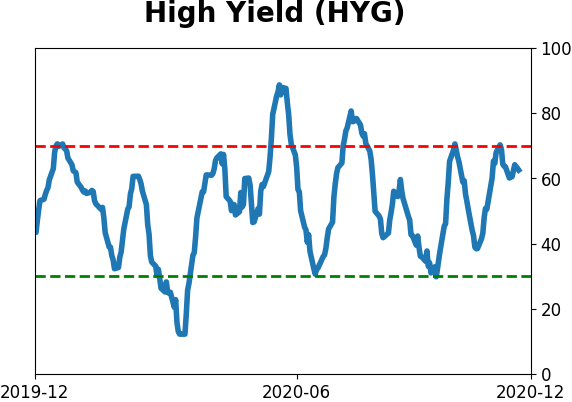

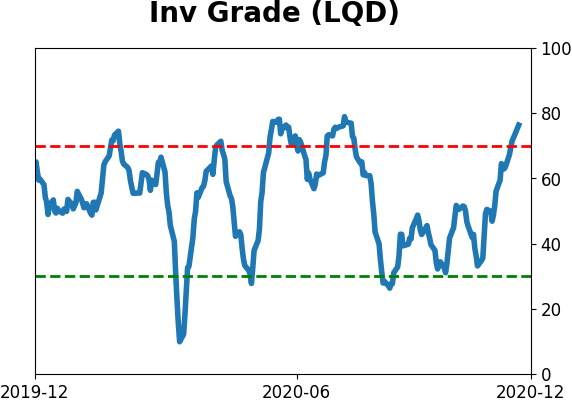

Bond ETF's - 10-Day Moving Average

|

|

|

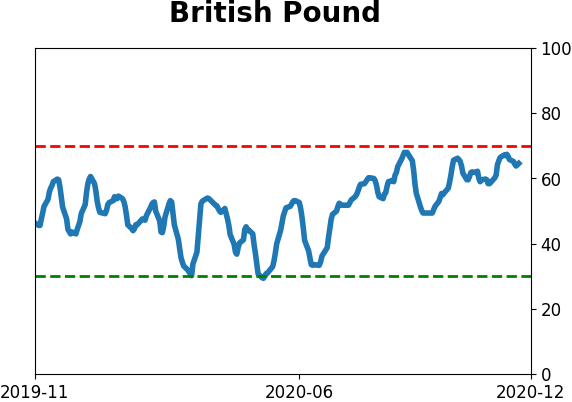

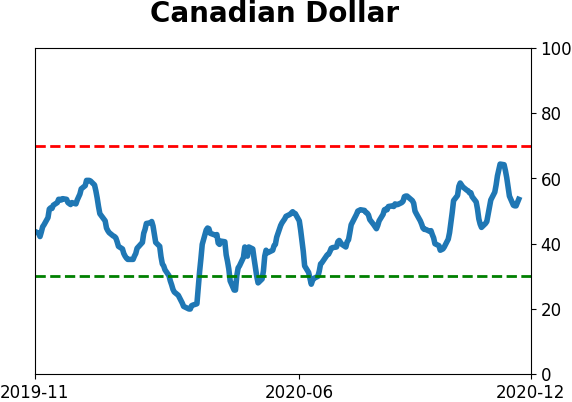

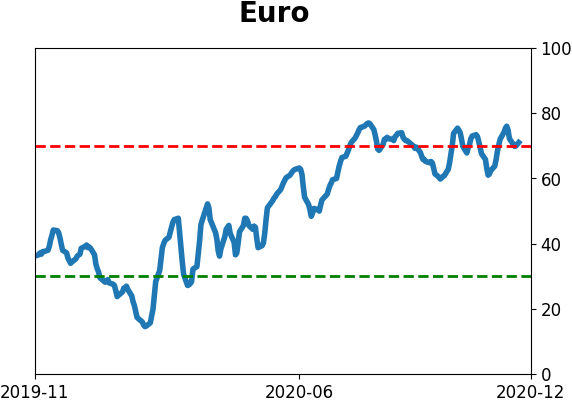

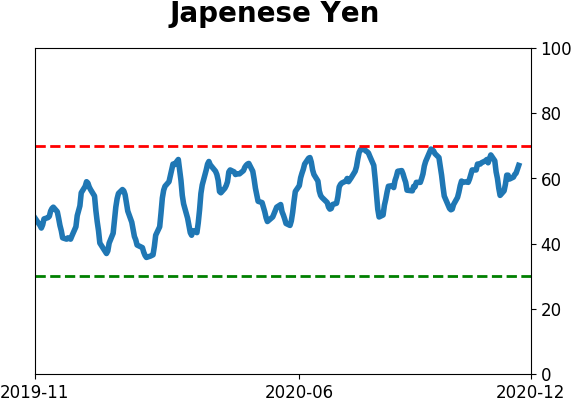

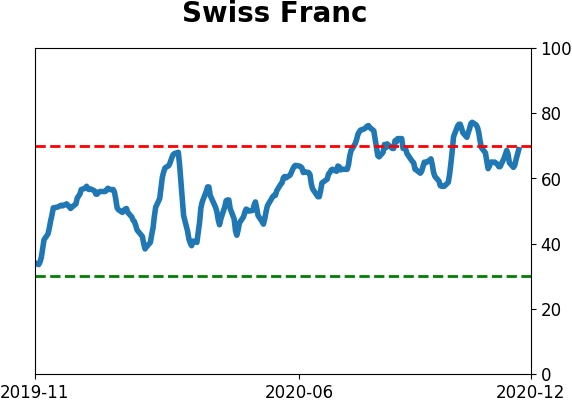

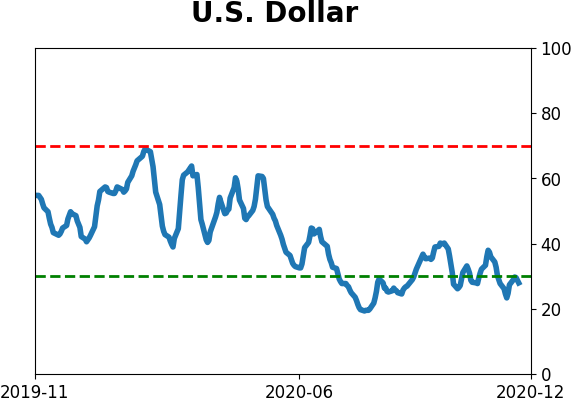

Currency ETF's - 5-Day Moving Average

|

|

|

Commodity ETF's - 5-Day Moving Average

|

|