Consumer Price Index Risk On/Risk Off

Last week I wrote several pieces regarding the effects of inflation on stock prices (see here, here, and here). I made reference in one of the pieces to the fact that some people like to break out the action of various components that comprise the Consumer Price Index. The ones that most people refer to are food and energy, which they claim are "volatile" and should be stripped out in order to get down to "core inflation."

Does any of this really matter? When it comes to identifying the implications of inflation for the stock market it just might. Let's take a closer look.

The Data

The Federal Reserve of St. Louis reports a variety of CPI-related data series on their website. Among those are:

- Consumer Price Index for All Urban Consumers: All Items in U.S. City Average

- Consumer Price Index for All Urban Consumers: All Items Less Food and Energy in U.S. City Average

We will use these two components to create a simple "Risk On/Risk Off" model for stocks that we can test.

The Calculations

A = Consumer Price Index minus Food and Energy (https://fred.stlouisfed.org/series/CPILFESL)

B = Consumer Price Index (https://fred.stlouisfed.org/series/CPIAUCSL)

C = 12 month % change in A

D = 12 month % change in B

E = C - D (i.e., CPI less Food and Energy 12-month change minus CPI 12-month change)

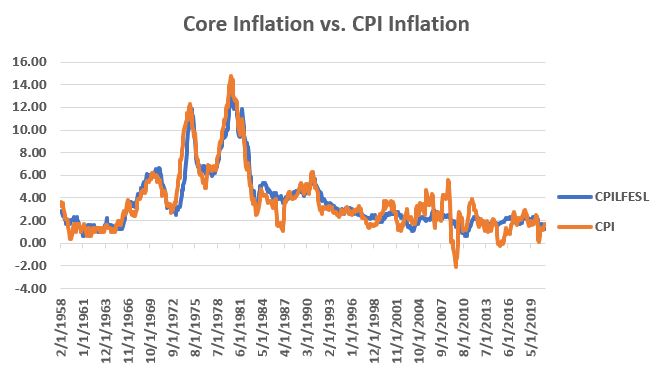

The chart below displays "core inflation" (C in blue) and standard CPI inflation (D in orange).

As you can see in the chart above, core inflation is in fact less volatile than CPI inflation. Not surprisingly, sometimes C (the blue line) is above D (the orange line) and vice versa.

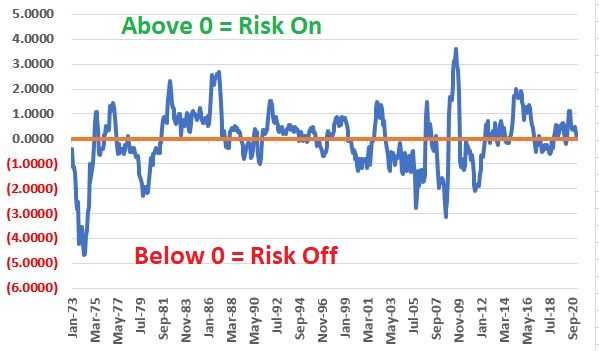

The chart below simply subtracts D from C each month to arrive at value E.

Again - and as you can see - Value E moves from positive to negative depending on whether "core inflation" is greater than or less than CPI inflation.

Now onto the real question - can any of this give us an "edge" in the stock market?

- If E > 0 we will refer to this as "Risk On" for stocks for the following month

- If E < 0 we will refer to this as "Risk Off" for stocks for the following month

Are these designations meaningful? Let's look at the performance of the stock market based on the reading for E from the prior month.

NOTES on Calculations and Testing:

- CPI and CPILFESL index values for this month are reported sometime early in the next month. For example, February 2021 data was reported on 3/10/2021.

- For the purpose of testing using a uniform approach all evaluation takes place at the end of each month using the latest data available

- So - for example - February data gets reported on March 10th. On the last day of March, we evaluate the variables above using the data published on March 10th

- If Value E > 0 at the end of March we will consider the environment to be "Risk On" for stocks in April

- If Value E < 0 at the end of March we will consider the environment to be "Risk Off" for stocks in April

- Our test period is January 1973 through February 2021 using monthly total return data for the S&P 500 Index

Results

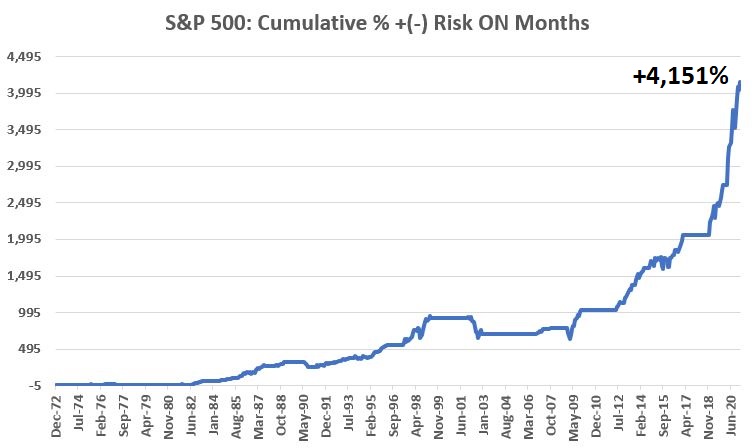

The chart below displays the cumulative growth from holding the S&P 500 Index ONLY during Risk On Months

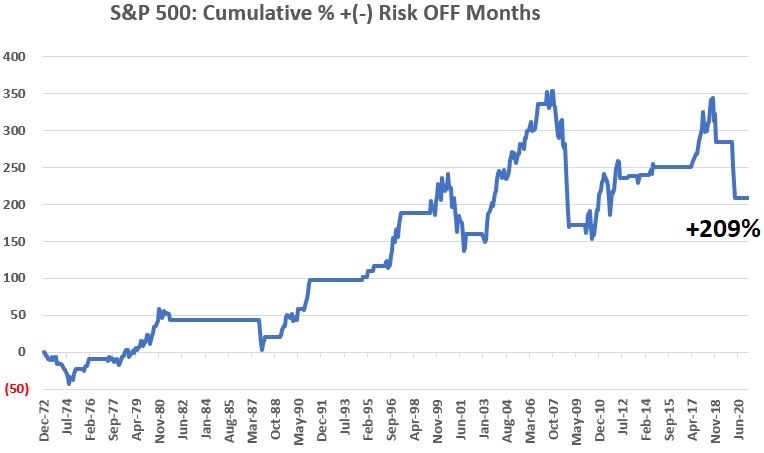

The chart below displays the cumulative growth from holding the S&P 500 Index ONLY during Risk Off Months.

It would be incorrect to refer to the Risk Off months as "bearish" since they do show a net gain over the full 48-year history. However, the differences in the two charts above are fairly striking. Likewise, we can note that the vast majority of severe market downturns in the last roughly 5 decades occurred while this particular indicator was flashing a "Risk Off" signal.

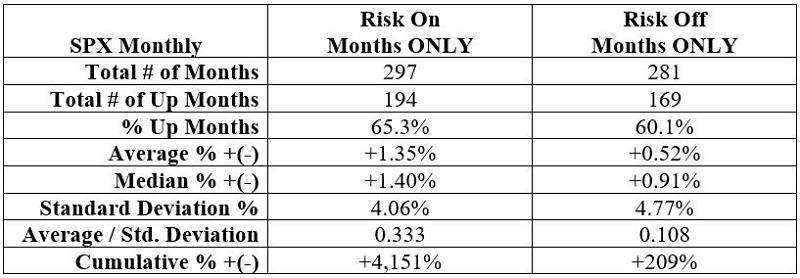

To quantify the statement above, the table below displays a number of comparative performance figures for the S&P 500 Index for Risk On months versus Risk Off months.

The key point to note is that the stock market performed exponentially better during Risk On months with a:

- Higher percentage of Up months

- Higher average and median monthly returns

- Slightly lower volatility

- Higher return to volatility

- A significantly higher cumulative return

Summary

When we consider that his particular model does not take into account market price action nor any fundamental information beyond simply the state of inflation, the best use of this particular model is probably as a "weight of the evidence" type of indicator, rather than as a standalone investment model. As I hinted at earlier, a "Risk Off" signal does not necessarily mean "sell everything and head for the hills." The bottom line is that this indicator strongly suggests more favorable stock market returns when it is Risk On than when it is Risk Off. Nothing more, nothing less.

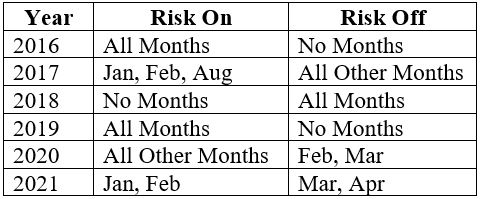

Recent Years

Current Status

March Data for Determining April Risk On/Risk Off Status:

- A = 270.299 (versus 266.786 12 months ago)

- B = 263.161 (versus 258.678 12 months ago)

- C = 1.28% (Core inflation)

- D = 1.73% (CPI inflation)

- E = (-0.4504)

- Status for April 2021 = Risk Off