In a recent MarketWatch article, SentimenTrader's senior analyst Jay Kaeppel highlighted that September has historically been the calendar's worst month for stocks, with risk rising especially after the third trading day.

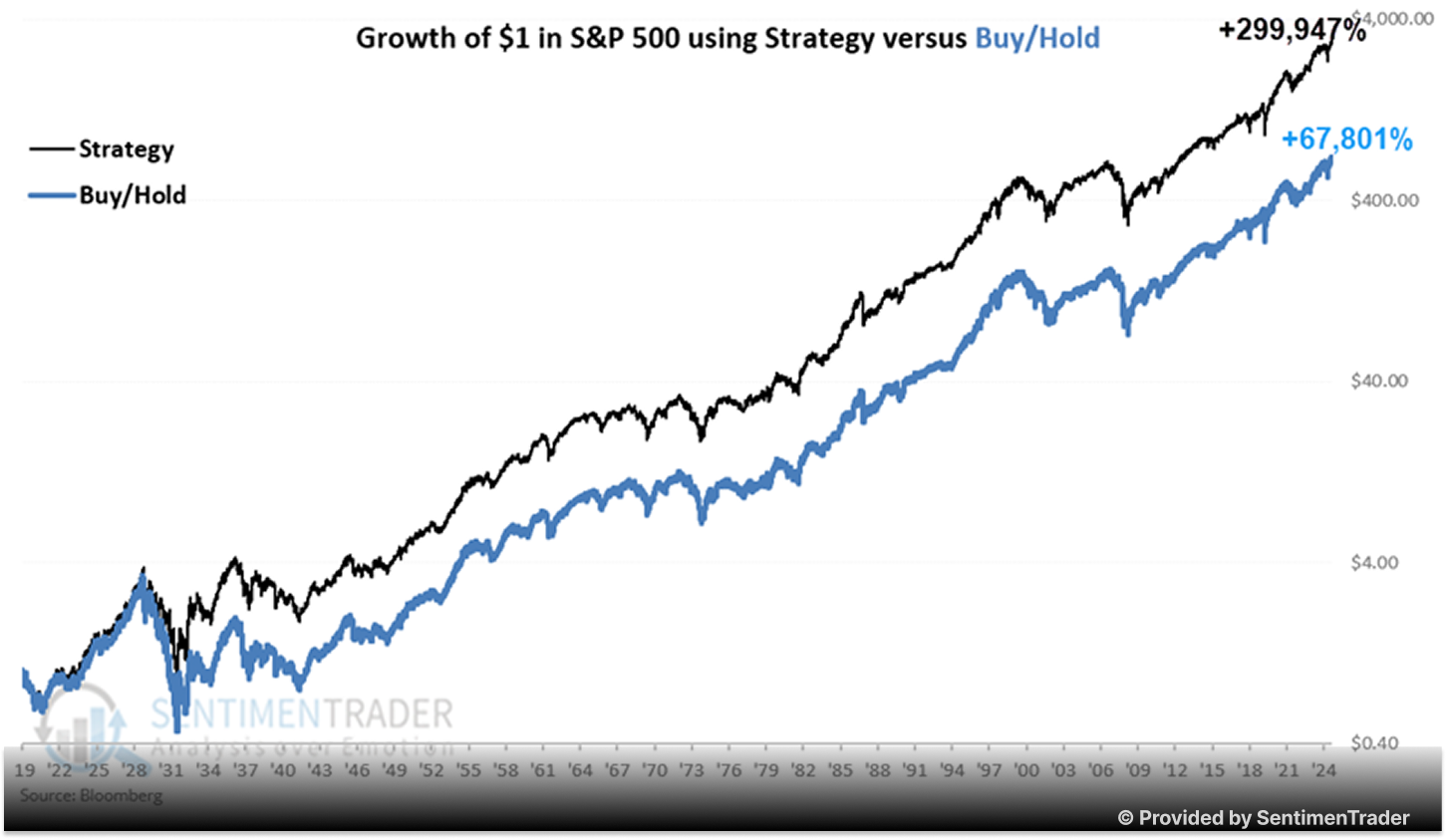

According to Jay Kaeppel's analysis, dating back more than 100 years, the S&P 500 has managed a modest cumulative gain of about 20% during the first three trading days of September. But from the fourth day onward, the picture shifts sharply, with a cumulative loss of roughly 78%. To address this pattern, he introduced the "September Strategy": exit positions at the close of the third trading day, and re-enter at the end of the month. Backtests show this simple rule would have produced a cumulative gain of nearly 300,000% since 1920, compared with about 68,000% for buy-and-hold.

MarketWatch also noted that September has earned its poor reputation for a reason. The S&P 500 has averaged a 1.1% decline in the month since 1928, with a win rate of just 44.9%. The Dow Jones Industrial Average shows a similar pattern. By contrast, investors who step aside after the first three days have historically avoided the brunt of the month's downside.

While no strategy is flawless, Kaeppel emphasized that for short-term traders, "risk is about to ratchet higher according to the calendar." A disciplined approach to avoiding September's weakest stretch has consistently outperformed long-term buy-and-hold returns, even before accounting for trading costs.

To access Jay Kaeppel's full research note and other market insights, visit sentimentrader.com.