Key points:

"This swelling proportion of battered stocks within a highly pro-cyclical sector highlights peak pessimism. At this juncture, the bearish macroeconomic narrative has been discounted by the market. This sets up a textbook asymmetric risk/reward scenario for investors willing to step in while sentiment is washed out."

- SentimenTrader researchers, as cited by Bloomberg (March 23, 2026)

In its March 23, 2026 market analysis, Bloomberg drew on SentimenTrader research to make the case that extreme pessimism in consumer discretionary stocks may be signaling a contrarian buying opportunity rather than the beginning of a prolonged decline.

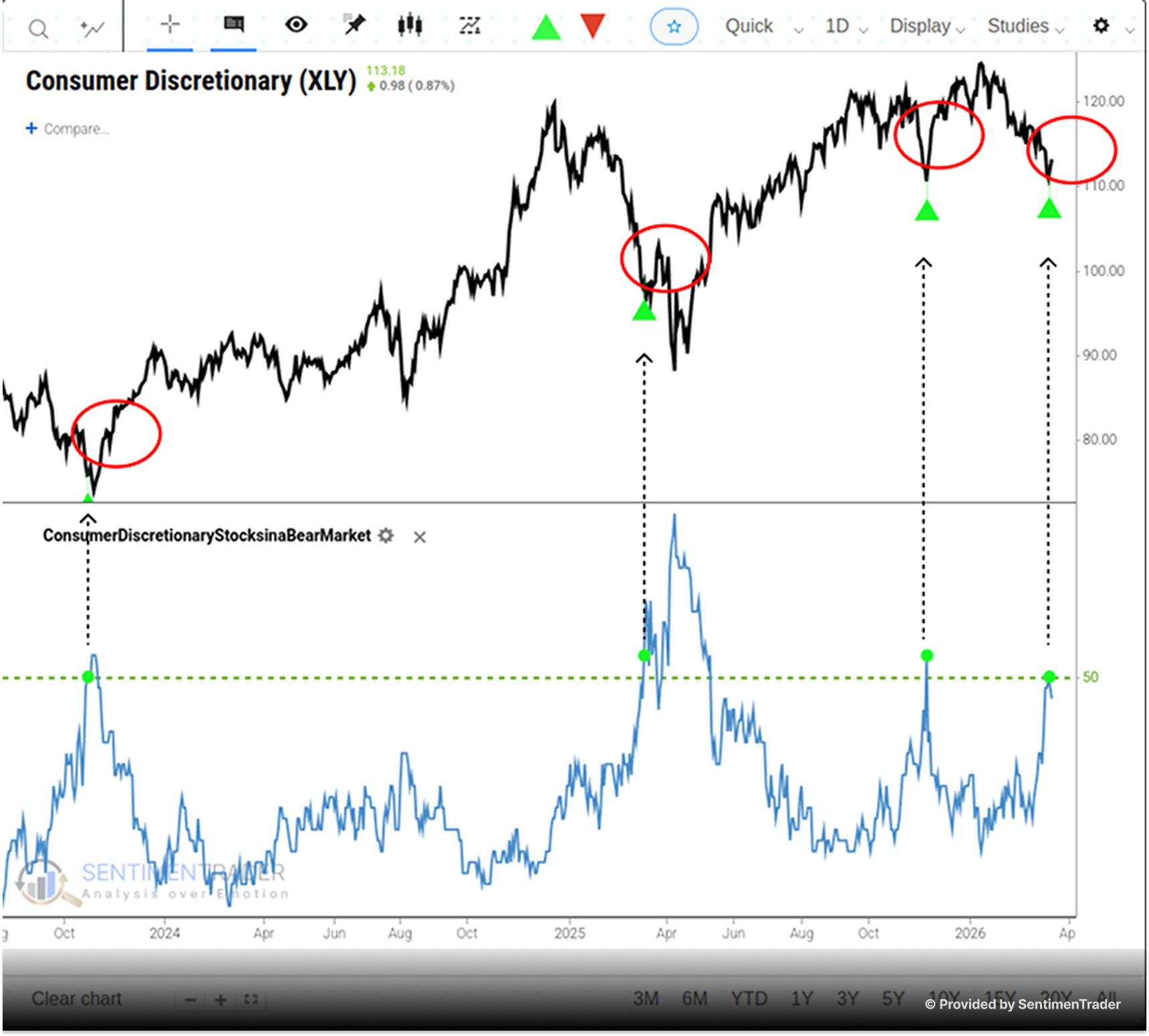

The S&P 500 Consumer Discretionary Index had fallen roughly 8% year-to-date, making it the second-worst performing sector among the 11 S&P 500 sectors, behind only financials. The selloff reflected two-sided pressure: rising energy costs squeezing both production margins and consumer wallets, compounded by lingering labor market concerns.

But SentimenTrader's data pointed to a different interpretation.

What the Breadth Data Showed

SentimenTrader found that more than 50% of stocks within the S&P 500 Consumer Discretionary Index were trading at least 20% below their 252-day highs. This level of broad internal damage is significant not just as a measure of how far stocks have fallen, but as a historically reliable sentiment signal.

Across 28 prior instances of this setup in historical data going back decades, the Consumer Discretionary Index rallied an average of 14% over the following year, advancing in 23 of those 28 cases. That is an 82% win rate with a substantial average return, a combination that SentimenTrader's researchers characterized as a textbook asymmetric risk/reward scenario.

The logic is straightforward: when a majority of stocks within a highly cyclical, sentiment-driven sector reach this level of compression simultaneously, it reflects indiscriminate selling rather than stock-specific deterioration. Indiscriminate selling tends to overshoot fair value, and history suggests that the subsequent mean reversion can be significant.

Why the Timing Mattered

At the time of Bloomberg's coverage, the bearish case for consumer discretionary stocks was well-documented and widely held. Energy price shocks, labor market softness, and trade war concerns had all been extensively covered. SentimenTrader's counterargument was precisely that: when a negative macro narrative becomes consensus and is reflected in extreme breadth compression, the incremental risk of further downside diminishes while the potential for a recovery increases.

This is the core of sentiment-based contrarian analysis. It does not predict when the recovery will begin, but it does identify when the conditions for one are in place.

Bloomberg noted that the sector was among the first to respond when geopolitical tensions briefly eased, jumping 3% in a single session while the broader S&P 500 gained roughly 1.7%, consistent with the asymmetric recovery pattern SentimenTrader's historical data had flagged.

What This Indicator Measures

The 252-day high breadth measure tracks what percentage of stocks within a given index or sector are trading significantly below their one-year highs. When this figure rises above 50% in a pro-cyclical sector like consumer discretionary, it indicates that the majority of the sector's constituents have experienced bear-market-level drawdowns, even if the index itself has not fallen that far.

SentimenTrader applies this type of internal breadth analysis across sectors, asset classes, and individual ETFs to identify when pessimism has become statistically extreme and historically actionable.

Explore the Data

→ Explore SentimenTrader's Breadth Indicators → Read the full Bloomberg article