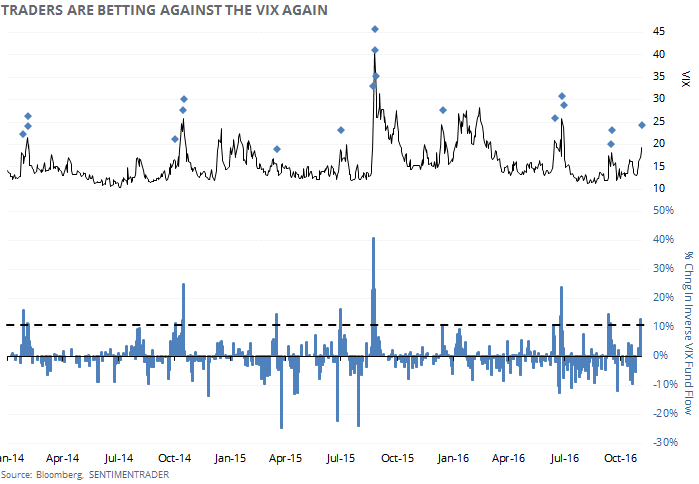

Traders Bet On A Lower VIX

In the October 24 report, we noted that traders had moved into exchange-traded products that bet on a higher VIX in a big way, and they cashed in their bets on a lower VIX.

These have been smart-money traders over the past several years, with an almost perfect record, so it was a sign that volatility should increase in the days ahead, which it did.

Longer-term moving averages that track these fund flows have not recorded extremes yet, because the moves in volatility have been too far, too fast. So the daily changes in the fund flows have been a better indicator.

And they just recorded another extreme.

On Wednesday, traders pulled money from funds betting on a higher VIX and, more importantly, shoved more than $126 million into the primary funds that bet on a lower VIX. That is more than 12% of those funds' total assets.

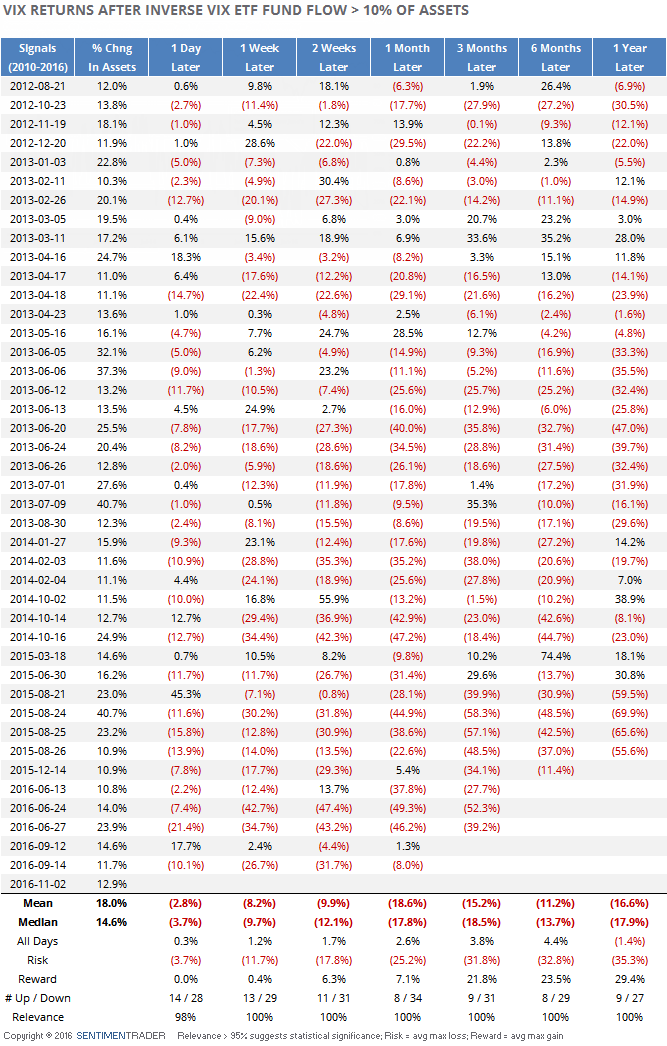

We can see from the chart that big inflows to these inverse VIX funds tend to coincide with short-term peaks in the VIX. We can see from the table below that during their history, inflows of 10% or more have, indeed, consistently led to a decline in the VIX and a heavily skewed risk/reward ratio over the next couple of weeks. That has especially been the case over the past two years.

It seems like these smart-money traders just made a big bet that the recent jump in uncertainty among options traders is overdone. Of course, taking any big positions during wild election gyrations is risky, so personally I am looking at any further jump in the VIX over the next several days, accompanied by more flows into these inverse VIX funds, to be a good multi-week opportunity for a fund like SVXY.