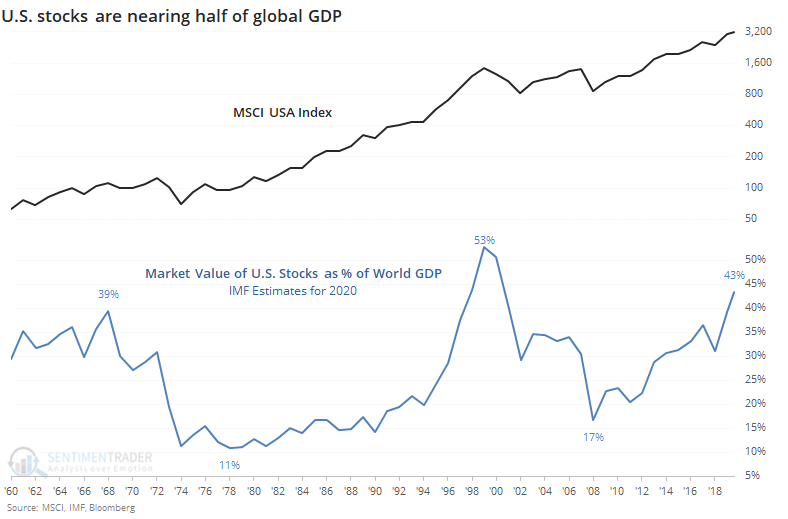

Stocks are worth more than the whole economy

Stocks have disconnected from the economy, and that's not news. The divergence has been going on for months, with a relentless rally in stocks juxtaposed against terrible economic numbers and even more horrendous anecdotes about job losses, business closures, and bankruptcies.

While stocks generally follow the economy, the two are not linked to any tight degree. They can decouple for months at a time, as investors are much more forward-looking than economic reports. Still, this has been a standout year when it comes to trying to use one to forecast the other.

As Bloomberg notes, the capitalization of equities across the world has surpassed global gross domestic product.

{kind=link}

"The market value of the world’s equities has risen above the dollar value of the global economy, which some investors say is a sign of overheated markets. Total stock-market capitalization reached $87.83 trillion on Sunday, compared with the 2019 gross domestic product of all countries at $87.75 trillion."

With the stunning rise in big American tech stocks, the U.S. portion of this global equity market capitalization is nearing all-time highs. While there isn't necessarily a connection between stock values and economic output, it is a way to estimate sentiment and valuations.

While stocks' value as a share of U.S. GDP has taken a hit, the total market cap of all U.S. stocks relative to the latest IMF estimate for global GDP in 2020 is now above 40% for only the 2nd time in 60 years.

If stocks continue their gains into year-end and GDP craters more than feared, then there's a chance we could eclipse the 1999 peak, but that would be tough to do. Even so, we've already eclipsed the other peak from 1968.

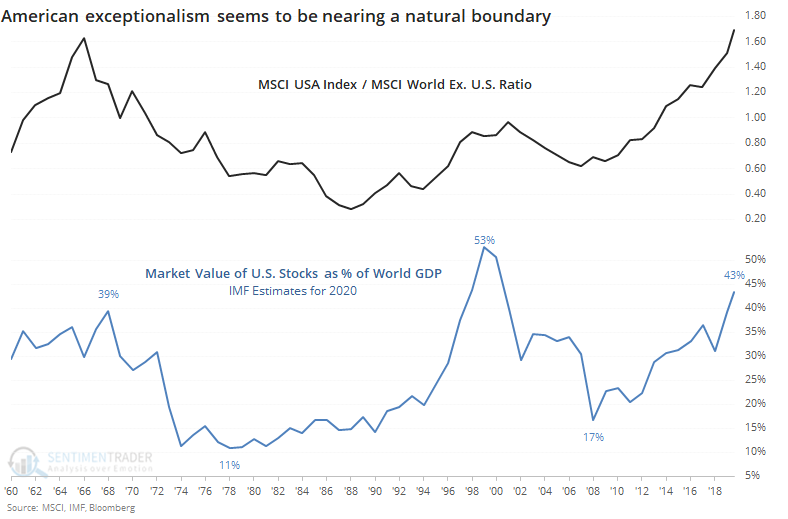

Whatever the theories behind the recent run of American exceptionalism (in stock valuations, anyway), by the time it nears 40% of global GDP, the run in U.S. stocks versus the rest of the world has been near its end, at least judging by the tiny sample size we have.

In the late 1960s, U.S. stocks had already started to underperform indexes in other parts of the world by the time this ratio peaked. In 1999, there was a bit more room to go before rolling over. Both times, equity values in the U.S. greatly trailed those outside the U.S. over the next five years at least.

It's hard for some investors to imagine what could knock U.S. stocks off their pedestals, but history is clear that something, somewhere, for some reason, will do it. Relying on the top 5 stocks to continue to carry the rest of the market is getting increasingly risky.