Small options traders are at it again

Key points:

- Small options traders are spending a lot of their volume on buying speculative call options

- Large traders are doing the same, and premiums paid on puts are plunging relative to calls

- Similar optimistic behavior tended to precede pullbacks, with the major exception of 2020-21

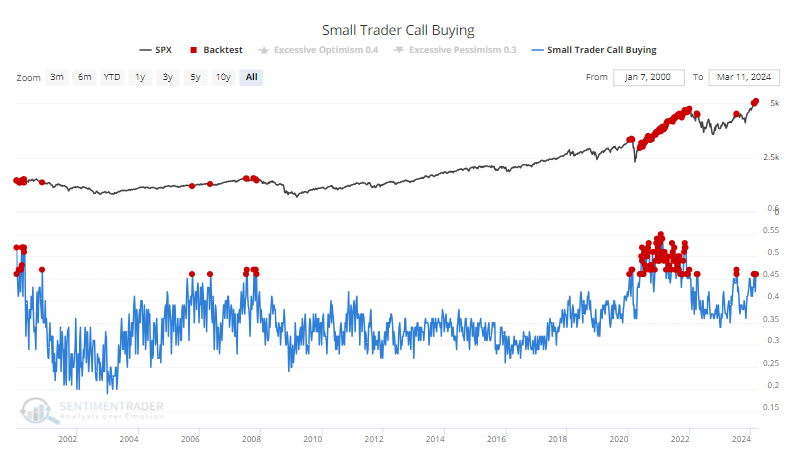

Small traders are buying lots of call options

A little over a year ago, small options traders were feeling pessimistic. Like really, really pessimistic. It was a natural overreaction following the mania they participated in the prior year.

Well, they're back. Mostly.

Last week, small options traders spent 46% of their total volume on buying call options to open. That's tied for the 2nd-highest amount in the past two years. Over nearly 25 years of history, the only time this level of speculative activity did not precede at least a pullback is during the options mania from the summer of 2020 through the fall of 2021.

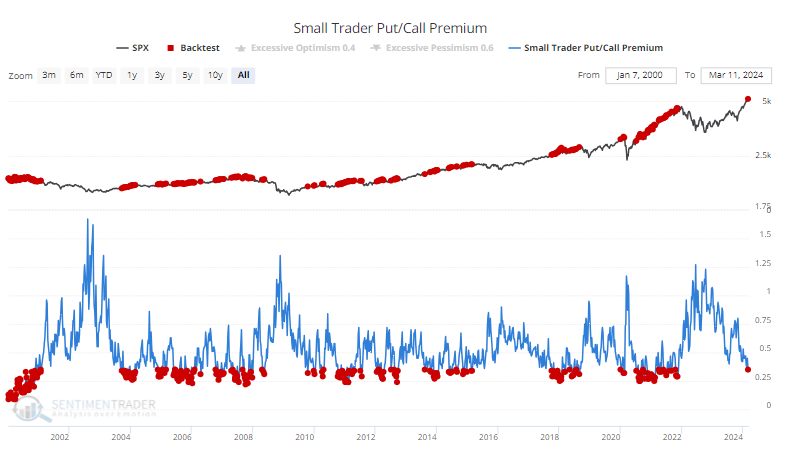

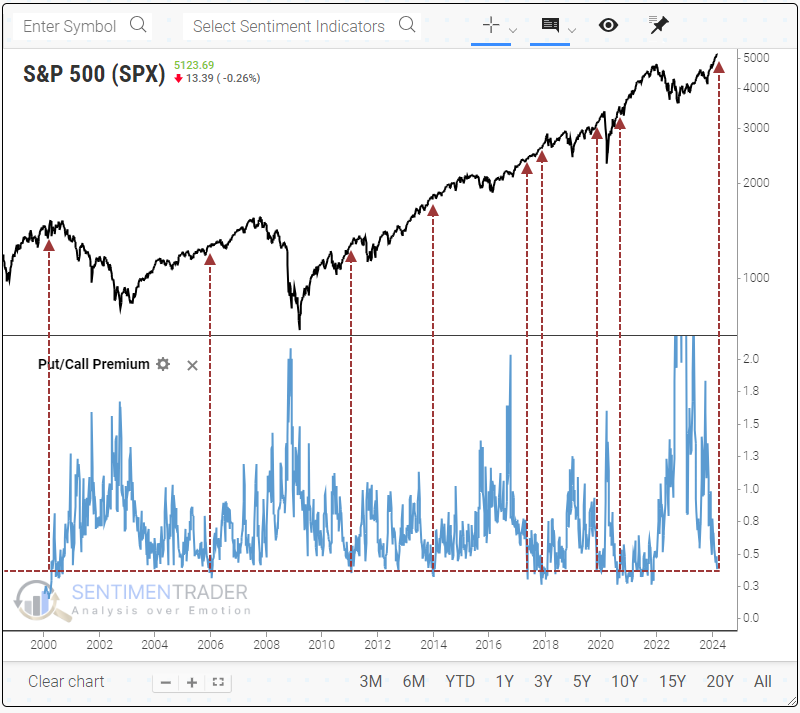

The demand for call options is pushing the premium differential out of whack. The amount that small traders spent buying put options relative to call options has melted to the lowest in more than two years. As of last week, small traders paid only $35 in premiums on puts for every $100 spent on calls.

This low a level has occurred more frequently, and the S&P 500 has managed to climb higher for weeks or even months after such low levels, but outside of 2020-21, those shorter-term gains tended to be erased in an eventual pullback.

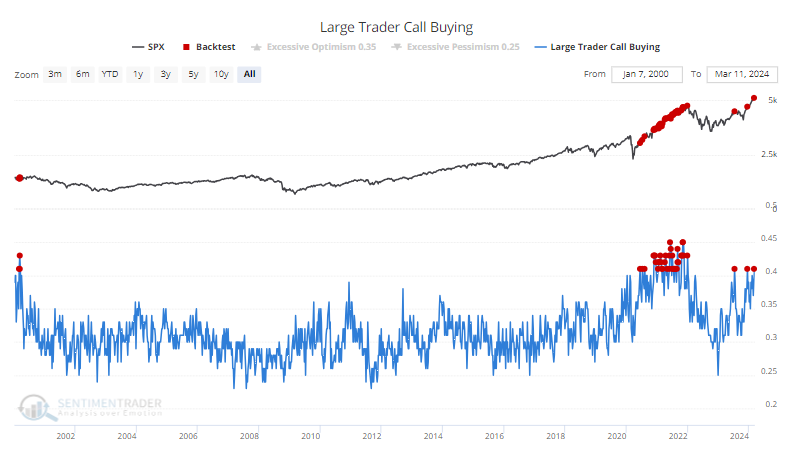

Large traders are buying calls, too

What's even more notable about last week's activity is that it wasn't just the smallest of traders snapping up speculative call options. The largest traders did so, too. They spent more than 40% of their volume on buying call options to open, one of the highest levels since 2000.

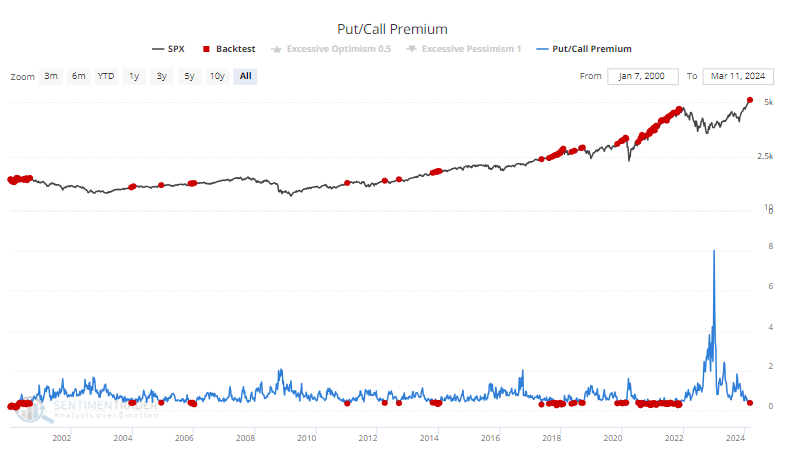

Because this speculative activity was evident across trader sizes, the overall ratio of premiums paid on puts relative to calls has plunged.

If we zoom in to highlight similar extremes, we can see that such a low premium ratio didn't have any negative impact in 2020-21 or 2014 during those creeper uptrends. There was one week in 2017 that also didn't lead to anything nefarious, but that was a one-off week that may be a data anomaly. The others saw some type of pullback or correction start within weeks.

If we combine all four indicators to find every week when all of them were this extreme simultaneously, only a handful of dates popped up, all in 2020-21 or 2000.

What the research tells us...

Pockets of speculative excess are bubbling in various parts of markets, not just stocks, and not just in the U.S. It's not a wholesale mania like 2021, of which there was overwhelming evidence. It's more like an isolated echo bubble. After all, traders large and small are still buying more put options than usual, so overall option sentiment doesn't look nearly as lopsidedly optimistic as 2021.

That doesn't mean it can't be dangerous, and it most likely means that future gains will be capped for a while, and recent ones will likely be erased at some point. So far, it seems most likely that any potential pullback should be relatively contained, with many breadth and momentum studies pointing to likely long-term gains during a mostly healthy market environment.