Options Traders Don't Trust the Calm Conditions

Options traders don't trust the calm conditions.

The S&P 500 declined for 5 consecutive sessions, but the overall loss was tiny. Historically, that combination has preceded a rebound - calm conditions tend to persist until that one moment when they don't, and the trend changes.

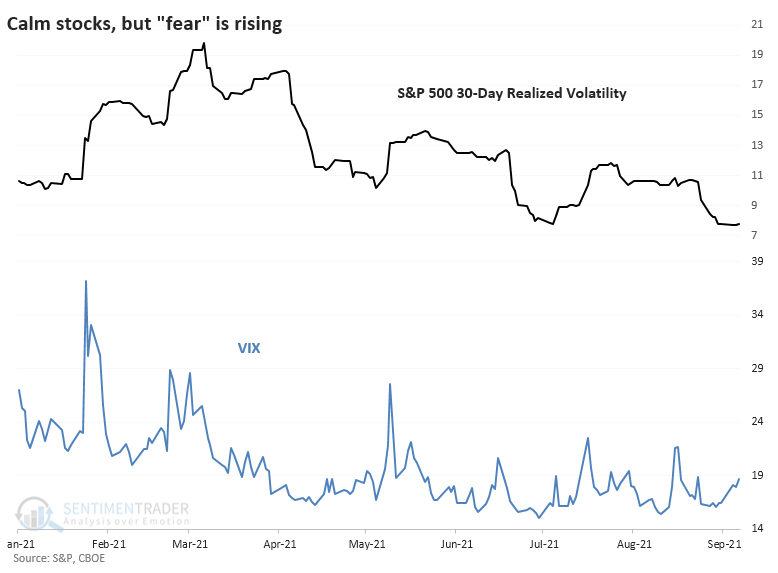

Conditions have been pretty much perfect for stock investors all year. A slow, steady drumbeat of gains is nirvana. But the VIX "fear gauge" of implied future volatility has been holding up for weeks, which is unusual since it's occurring at the same time that actual, realized volatility in the S&P 500 index has dripped close to all-time lows. The action late last week didn't change things much.

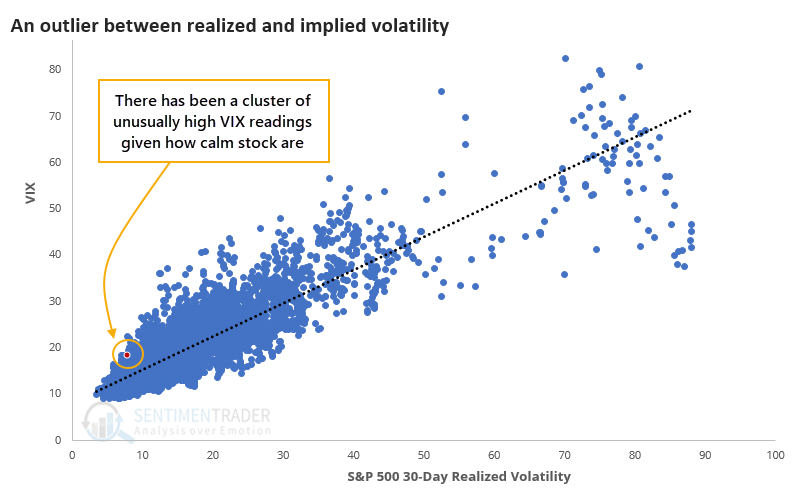

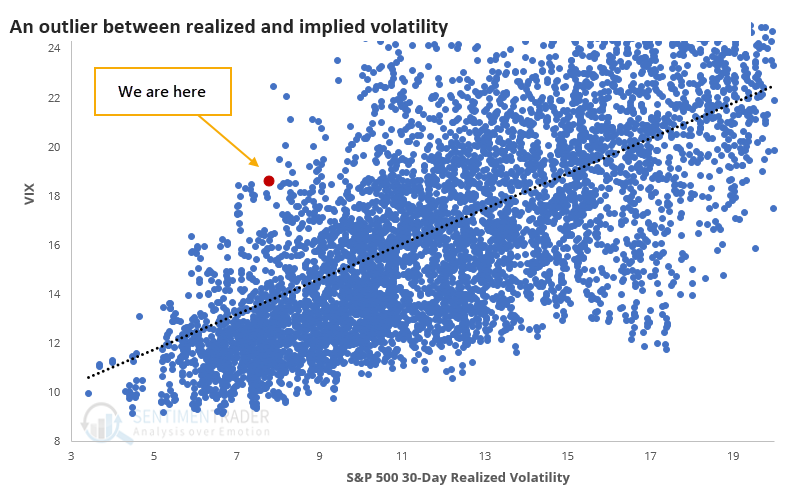

There is a clear positive correlation between realized and expected volatility. Traders rely on the recent past (realized volatility) to predict the near future (implied volatility).

If we zoom in on smaller readings, we can see just how much last week stands out versus all historical readings.

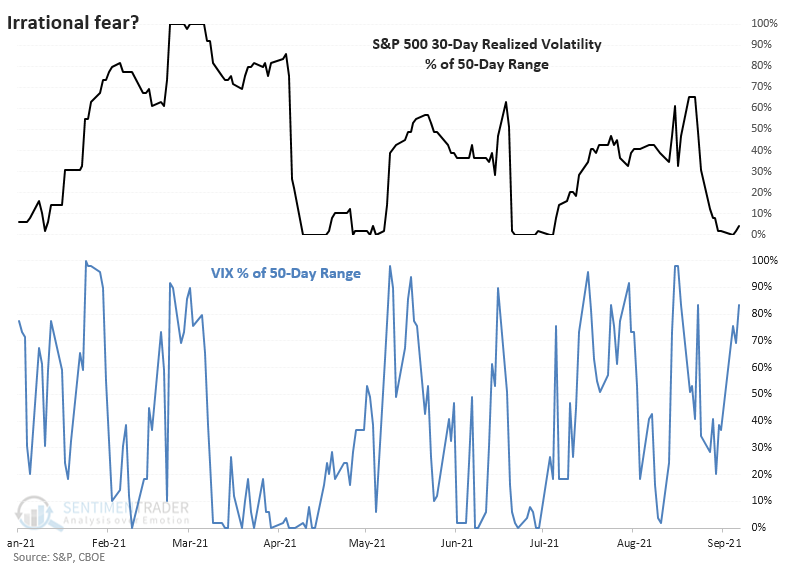

This becomes clearer when we look at realized volatility versus its 50-day trading range. It's scraping the bottom of it. But the VIX has been priced at the upper end of its own range.

So who knows more, equity investors or volatility traders? The table below suggests that in the short-term, options traders are "smarter," while in the medium-term, investors have been.

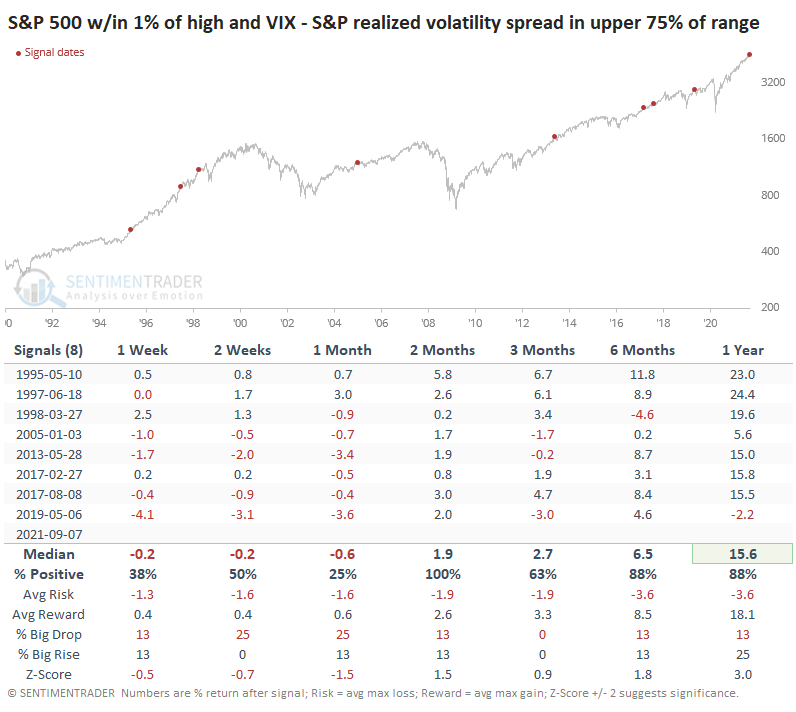

Over the next 1-4 weeks, the S&P had great difficulty holding any meaningful gains when this signal triggered while the index was hovering within 1% of its prior highs, as it was last week. Even so, over the next two months, it rallied every time. And longer-term, there were no major losses.

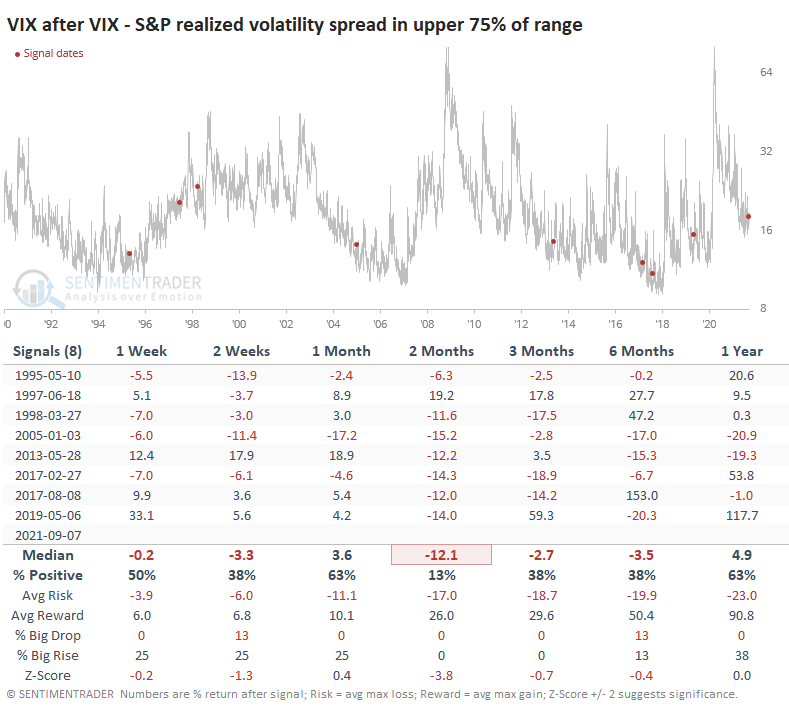

Even though stocks were rocky in the immediate aftermath of these signals, the VIX didn't pop higher very often. And only one of the signals showed any gain at all over the next couple of months.

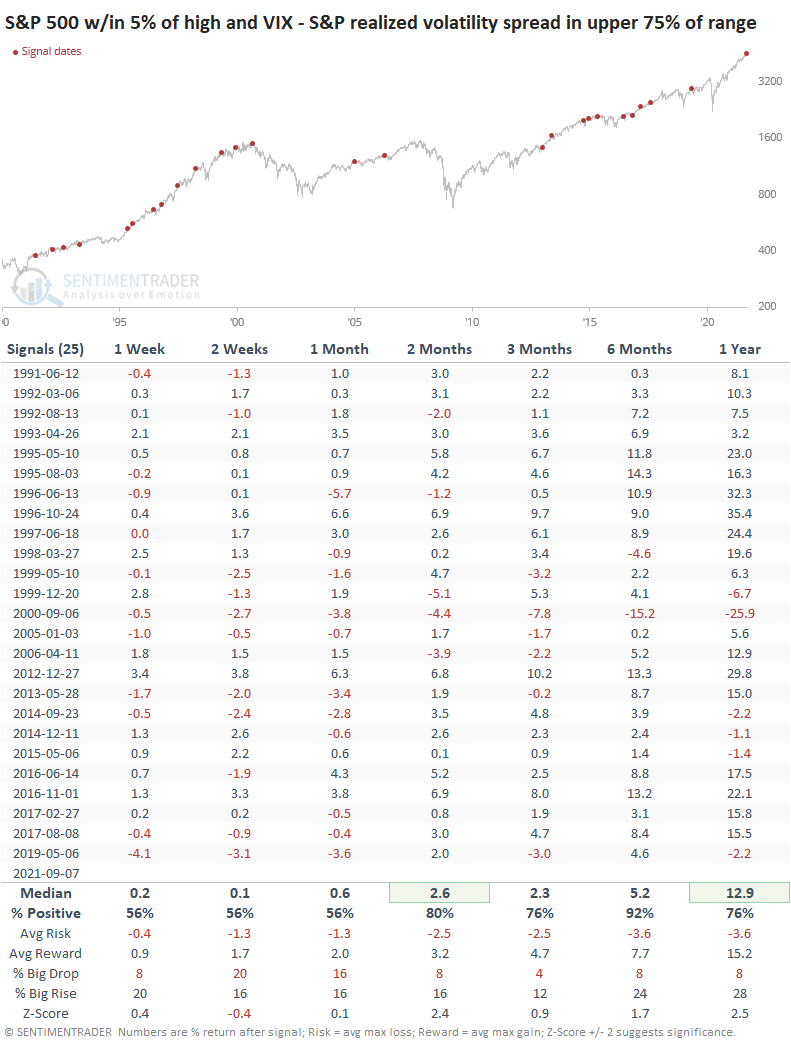

If we allow the S&P to be within 5% of its peak (instead of 1%), then the sample size increases dramatically. But the overall suggestion was the same - questionable shorter-term returns but decent medium- to long-term ones.

Stocks in 2021 have shrugged off every imaginable concern, and it has resulted in one of the most remarkable market environments in history. Maybe that means history is no guide whatsoever here, and a decent argument could be made that that's the case.

We're always looking for times when markets don't do what they should, and we got indications of that on the upside as early as January. Now we should be watching for signs that stocks aren't doing what they should on the downside, and if we see any material follow-through weakness after last week's small but persistent declines, it would suggest that the momentum run of 2021 is entering a shakier stretch.