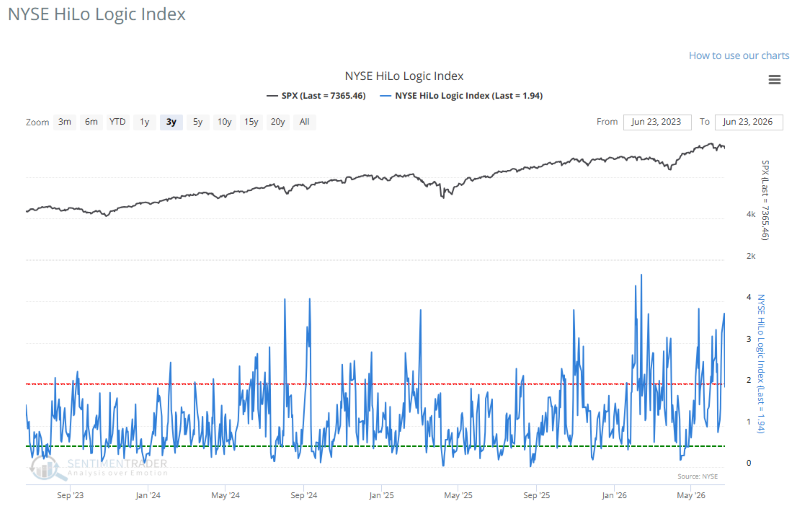

NYSE High Low Logic Risk-Off Model

Key points

- Following a tactical risk-off signal from the S&P 500 variant, the NYSE High Low Logic Risk-Off Model has now triggered, confirming a broader breadth divergence.

- When applying a filter-requiring the signal to trigger within 21 days of a 252-day high-forward returns deteriorate significantly, with the S&P 500 posting a dismal 16% win rate over the subsequent one-month window.

High-Low Logic NYSE with Spike

In Monday's report, I noted that the High-Low Logic S&P 500 with Spike model issued a tactical risk-off alert during the previous trading session on June 18. Following the close of that session, the broader NYSE High Low Logic Risk-Off Model triggered. For a more detailed explanation of the High Low Logic concept, please refer to Jay's note from March 4, 2021. As a reminder, the S&P 500 version uses the original 50-day exponential moving average, whereas our NYSE version uses a 40-day MA.