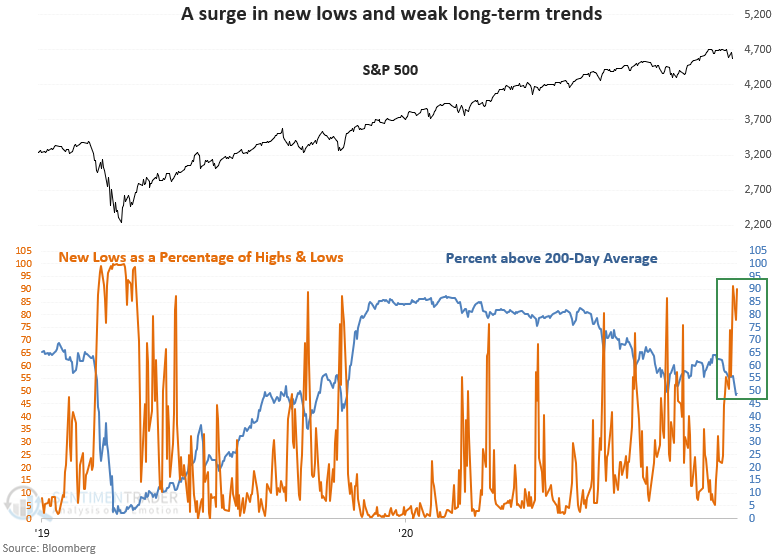

NYSE breadth signals risk-off

Key points:

- NYSE new lows as a percentage of high and lows are surging

- Long-term NYSE stock trends are weak

- The S&P 500 is down less than 3% from its recent high

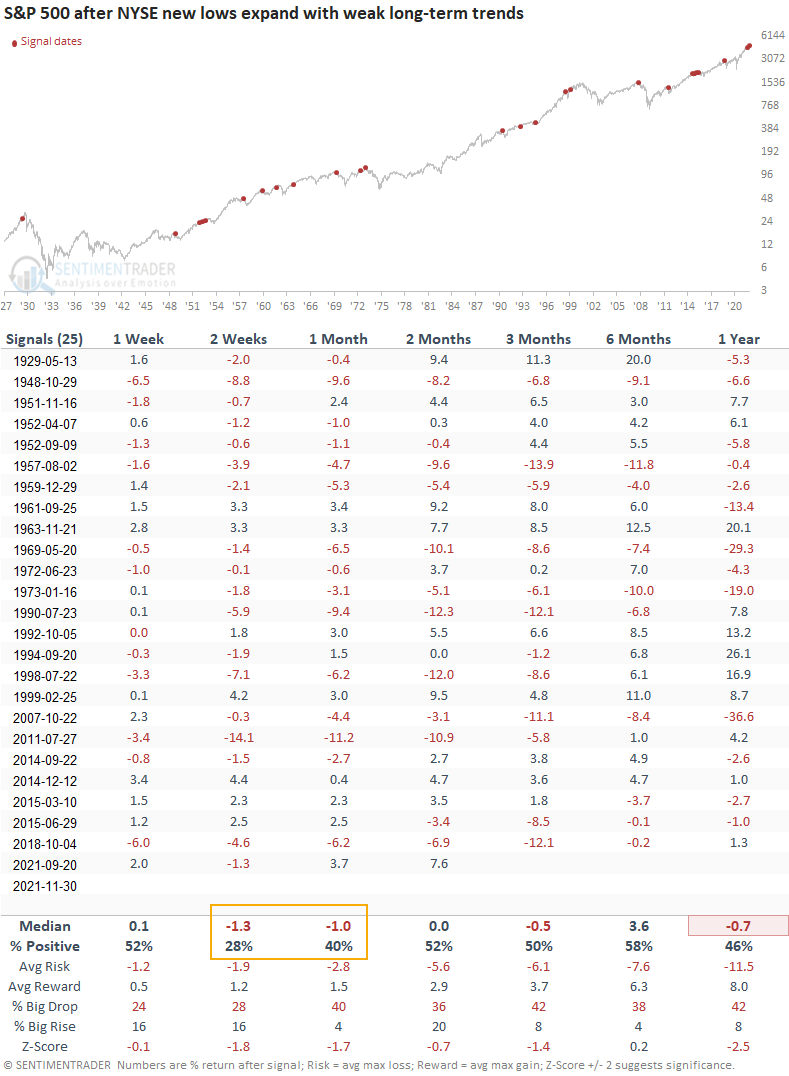

- Similar conditions preceded negative returns from 2-4 weeks later

52-week lows are surging and trends are weak, triggering a new risk-off signal

A new signal from a voting member in the TCTM Risk Warning Model registered an alert on Tuesday. The component is called the 52-Week Low with Percent above 200-Day model.

The model identifies when NYSE lows as a percentage of highs and lows exceed 79% and when NYSE common stock members above their 200-day average are less than 49.75%. At the same time, the S&P 500 must be down 4.5% or less from its most recent high.

Please click here for the TCTM live updates page on the website.

The market breadth backdrop looks unhealthy

As a percentage of highs and lows, new lows have risen to the highest level since the pandemic crash. At the same time, the percentage of NYSE common stock members above their 200-day moving average has deteriorated to the lowest level in more than a year. When we compare the long-term stock trends to the price of the S&P 500, the divergence is noteworthy.

Similar signals preceded weak returns in the near term

This signal triggered 25 other times over the past 93 years. After the others, future returns and win rates were weak in the 2-4 week time frame. The 1-year results look unfavorable. However, I would note that most of the negative signals occurred before 1973.

What the research tells us...

When NYSE lows as a percentage of highs and lows are surging and long-term stock trends are weak, the market risk outweighs the reward. Similar setups to what we're seeing now have preceded weak returns and win rates in the 2-4 week time frame.