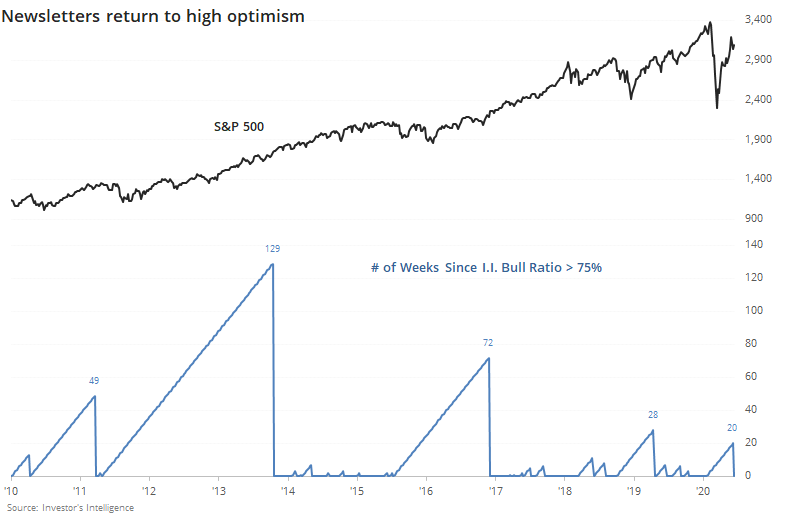

Newsletter writers return to optimism

Newsletter writers have seen the rise in speculation among options traders, Robinhood users, and Wall Street analysts, and don't want to get left behind. Not being fully invested in a bull market leads to an increase in cancellations - nobody wants to see their neighbor doing better than they are.

The latest Investor's Intelligence survey showed three times as many bullish newsletters as bearish ones, meaning a Bull Ratio (Bulls / (Bulls + Bears)) greater than 75%. This is the first week in five months that there were so many bulls relative to bears, ending one of the longer streaks of "not optimism" over the past decade.

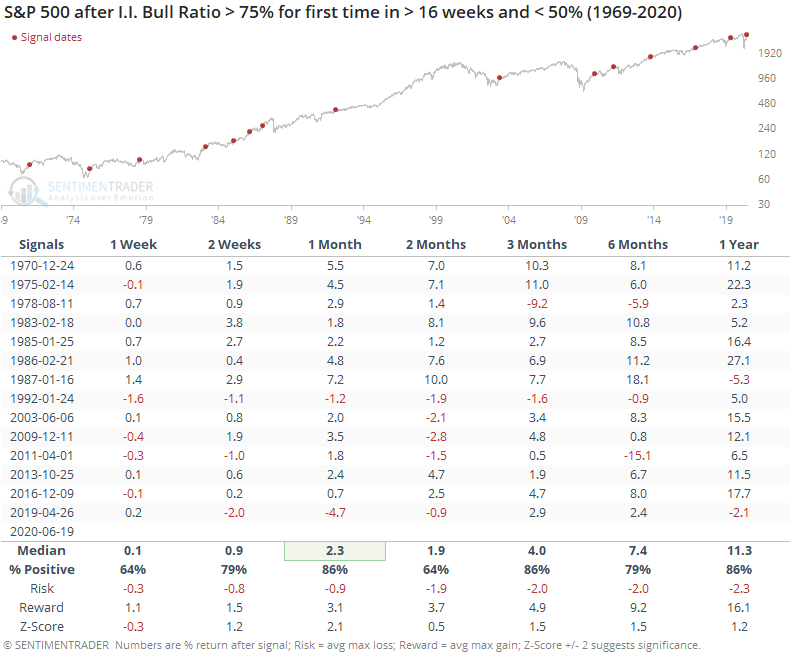

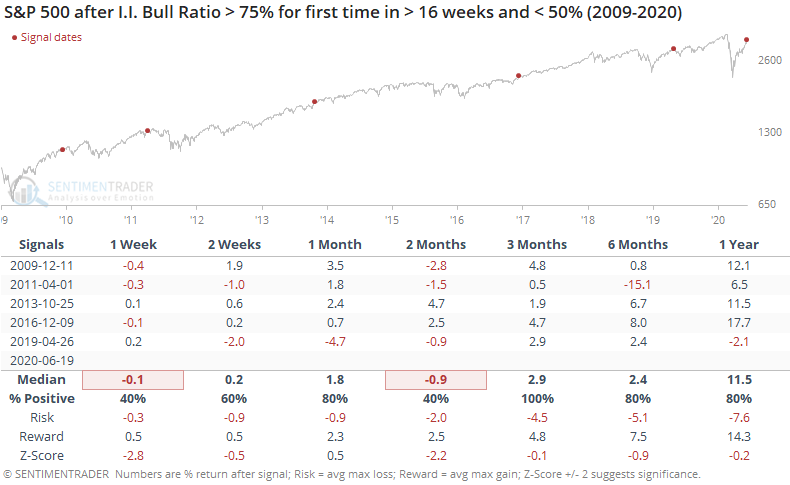

When long streaks with a Bull Ratio below 75% finally ended and included at least one week with more bears than bulls, it was mostly a good sign. There was some volatility over the medium-term, with more consistency longer-term. Over the next year, there were only two losses, and they were both small.

The most positive medium-term returns came in previous decades. More recently, stocks have tended to back off after optimism returned.

Over the next 2-3 months, the S&P either declined or showed a small gain, The biggest exception was late 2016, which showed a small gain a month later then built on that during the mo-mo market of 2017. In 2013, the S&P rallied strongly shorter-term, then gave quite a bit of that back 2-3 months later before rallying again.

Returning optimism is a good sign for stocks, as long as it's not extreme. The Investor's Intelligence data is just bordering on that. It's not extreme enough to be an outright negative, especially when it's the first reading after a period of pessimism. It's a mild concern that over the past decade, returning optimism led to a pause in the rally over the next 2-3 months.