More big tech stocks fall into corrections and bear markets

Key points:

- With recent weakness, more than 60% of Nasdaq 100 stocks are in corrections, and 30% in bear markets

- During healthy bull markets, these thresholds are rarely breached and typically bring in buyers

- If buy-the-dip is no longer in force, the breach of these levels ushers in some ugly precedents

A market environment filter

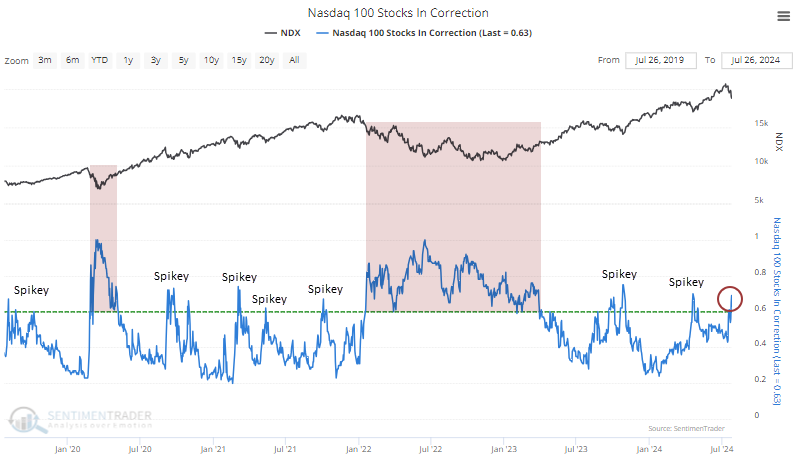

More and more tech stocks have been wobbling. In June, we saw how unusual it was to see the Nasdaq 100 (NDX) index hitting new highs while many of its stocks were in corrections, down more than 10% from their highs.

Now that the index has pulled back, we've seen more stocks getting hit, and the percentage of stocks in a correction has spiked above 60%. We'll usually see fewer than 60% of NDX stocks in corrections during healthy bull markets. If it reaches that level (like now), it's almost always "spiky" and quickly falls below that threshold as buyers step in.

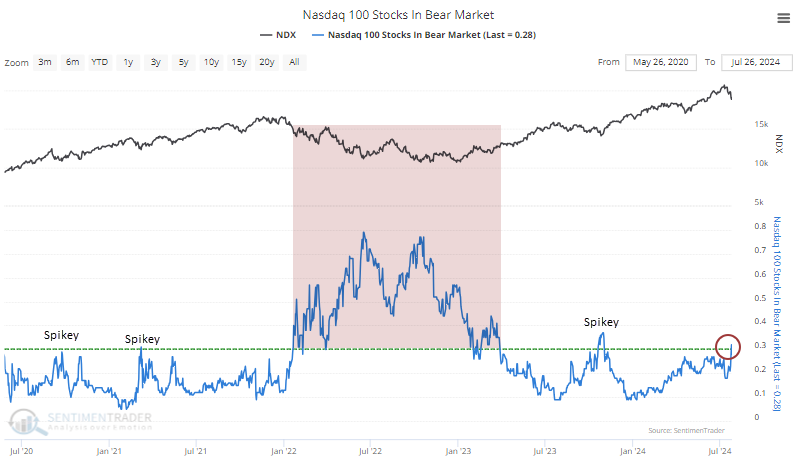

The same goes for stocks in deeper trouble. The percentage of stocks in bear markets has jumped as well, to the highest level in more than six months. During bull markets, this figure routinely stays below 30%, and if it nears or exceeds that threshold, it tends to be near the ends of pullbacks.

Watch for buy-the-dip

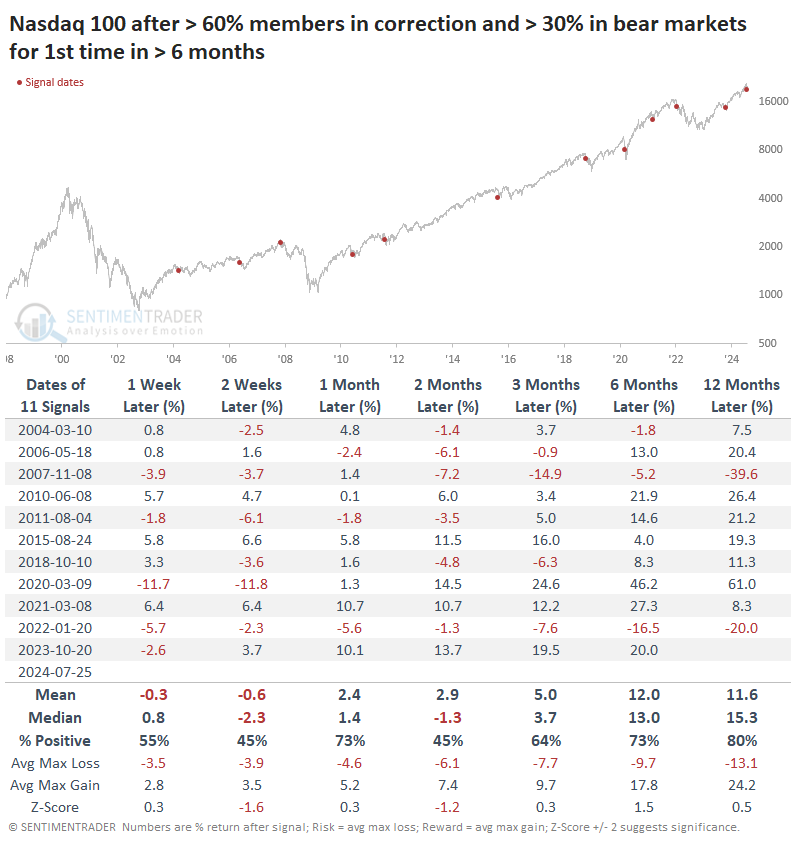

The table below shows each date when the Nasdaq 100 ended a streak of at least six months with fewer than 60% of its members in corrections and 30% in bear markets. Returns for the index were mixed over the next couple of months, with a few decent gains and a few moderate losses.

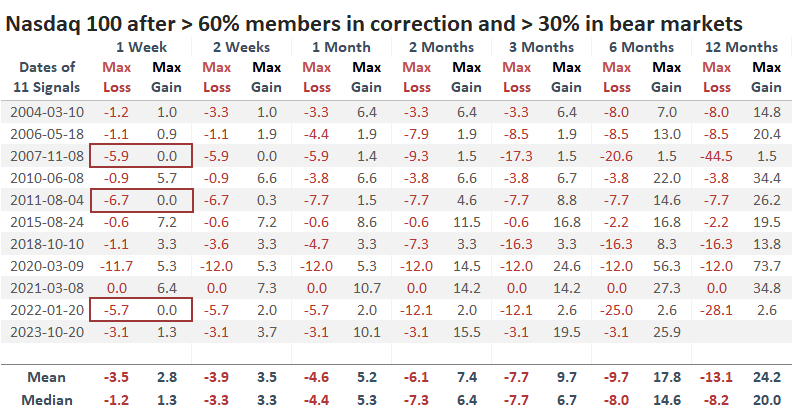

One thing that stands out is how traders behaved in the short term. There were three instances when there was absolutely no buy-the-dip mentality, and two of those preceded protracted bear markets. The other, in 2011, led to a bit more weakness then an impressive rally.

A fairly strong positive correlation existed between the maximum gain over the next week and the ending return one year later. There isn't a lot of data here, but it suggests that if we don't see any interest from dip-buyers in the days ahead, we should be wary.

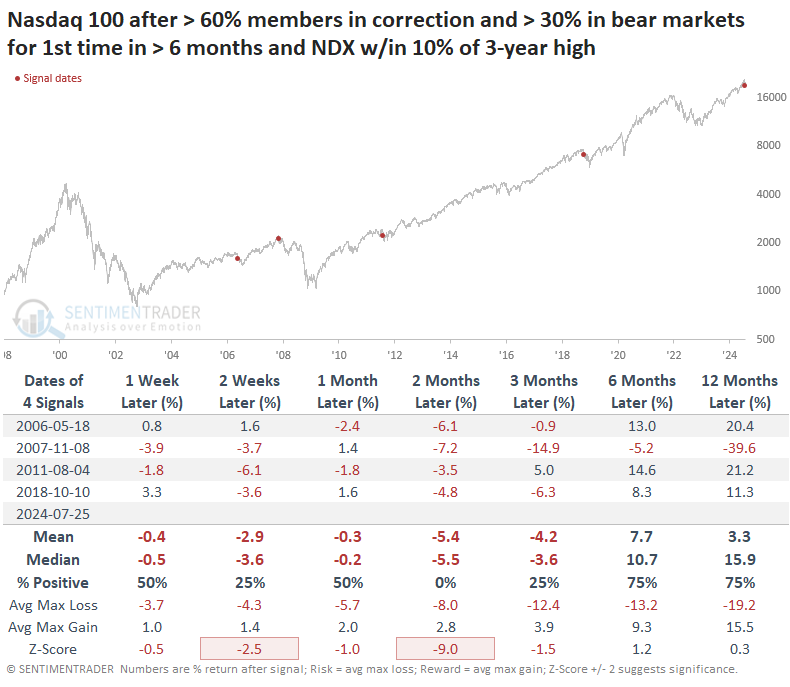

At the risk of making a small sample size even smaller, the table below filters the dates to only include those when the NDX index was within 10% of a multi-year high. These are times when the index was holding up relatively well compared to its component stocks.

One might think that these displays of relative strength were good, but two months later, the NDX sported a negative return all four times. That shorter-term weakness was about it for three of the instances, as they went on to show double-digit gains over the next ten months.

What the research tells us...

There is little doubt that risk appetite has been strong for a historically long time. That's not necessarily bad, as it usually suggests that investors have been conditioned to treat any pullback as a bargain, so they'll be more willing to commit funds the next time. Things tend to get hairy when that stops working, and a buy-the-dip mentality is no longer in vogue. After ends of streaks in the Nasdaq 100 and its components like we just saw, it should pay to watch how traders react. It ushers in some ugly precedents if they don't show much buy-the-dip eagerness.