Hedging Activity Is Picking Up

Stocks are holding up pretty well, especially in the broader market, yet options traders are getting nervous.

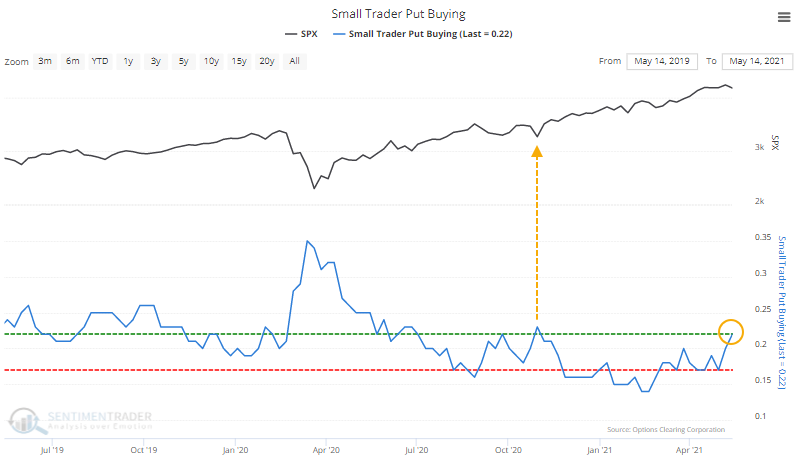

Small options traders have spent 22% of their volume buying put options to open, tied for the 2nd-largest amount since last July.

Granted, it's still low compared to past years, and large options traders are still buying relatively few puts.

HEAVY HEDGING...RELATIVELY

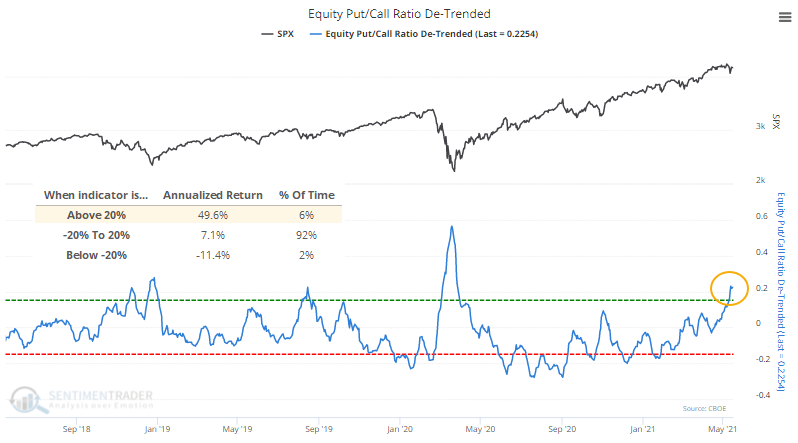

This rise in put volume - both buying and selling - has pushed the Equity Put/Call Ratio to one of its highest levels of the past year, even though losses on stocks have been minor. The De-Trended version of the ratio shows that a shorter-term moving average is more than 20% higher than a long-term moving average. This has preceded a very favorable annualized return since 1997.

Likewise, the Backtest Engine shows that forward returns were consistently positive when the ratio crosses above 20%.

PICKUP IN PUTS, DESPITE ONLY SMALL LOSSES

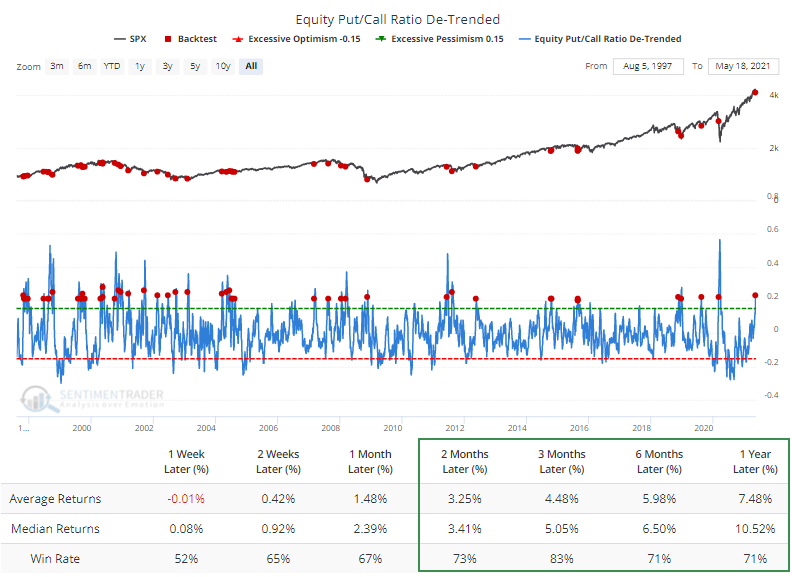

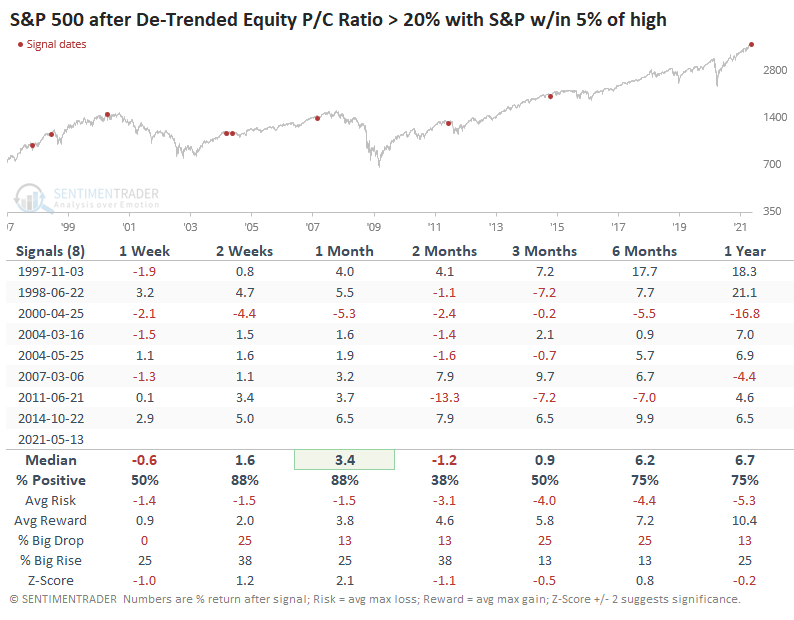

What's especially notable about the current instance is that it triggered while the S&P was within 1.5% of a 52-week high. The only other times that's happened were early December 1997 and late June 1998. The former preceded short-term weakness then medium-term strength. The latter showed the opposite.

Looking for times when the ratio got this high with the S&P within 5% of a peak, returns were mixed.

Every time but once, the S&P rallied over the next month, but then 4 of them failed and led to losses a month after that, preceding haircuts of more than 10% in 2000 and 2011.

Markets do better when optimism and speculation are rising, not falling. At least until it gets to an extreme, and even then, momentum can carry a market higher. A rising put/call ratio is generally not a good thing. Still, it's gotten to a point now where it's kinda-sorta extreme, at least relative to the past year or so, suggesting relatively heavy hedging activity that could be a short- to medium-term positive.

The biggest risk is that after the massive speculative bubble reached in February, we could be heading into a larger corrective phase, in which case a modestly high put/call ratio won't help at all. The biggest clue to that will be how markets react to the current display of modestly high hedging activity in options. If buyers aren't interested and stocks continue to struggle, it will increase the probability that there's a larger trend change afoot.