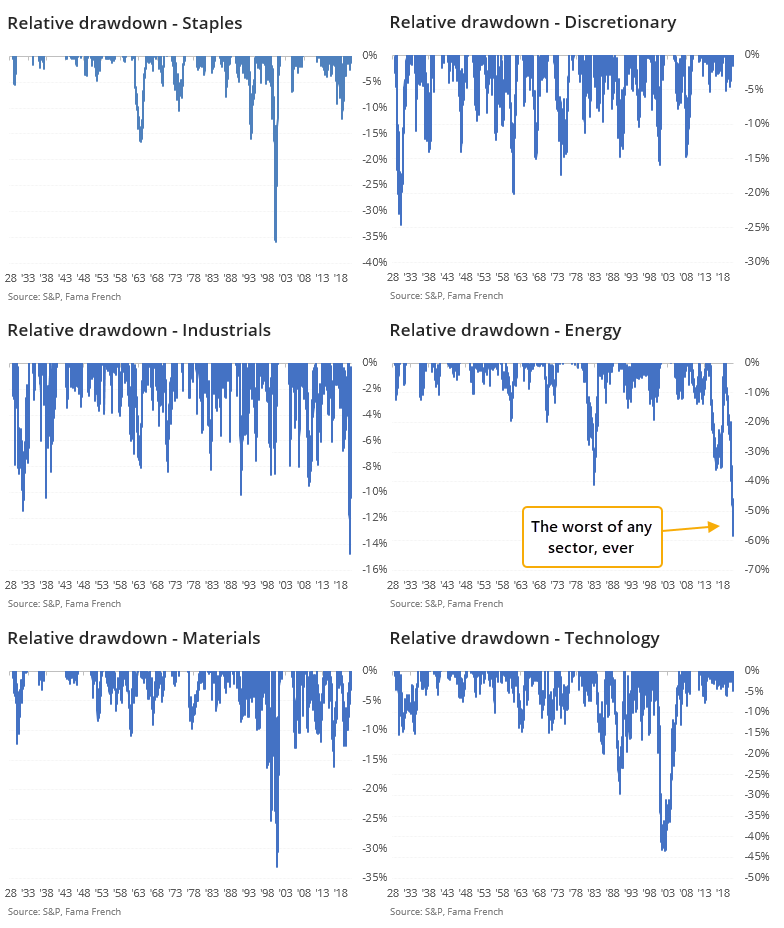

Drawdown in energy stocks is the worst of any sector, ever

There have been two themes that got renewed interest this week, both dealing with drawdowns. The energy sector, and the value factor, have suffered massive losses relative to other sectors and factors, respectively.

We've already seen that energy has been one of the most consistently losing sectors out of any sector since 1928. It's also suffered one of the largest drawdowns. Looking at each sector's maximum loss from its latest multi-year peak can be instructive, but it's better to look at it relative to the drawdown of the broader S&P 500 index.

The charts below show just that. To be clear, this is each sector's maximum decline from a 3-year high, minus the drawdown in the S&P 500 index. So, it shows losses that investors suffered beyond what they would have been exposed to in the broader market.

From the charts, we can see that it's unusual for any sector over the past 90 years to suffer a drawdown that was 35% more than the drawdown in the S&P...except for energy's current malaise.

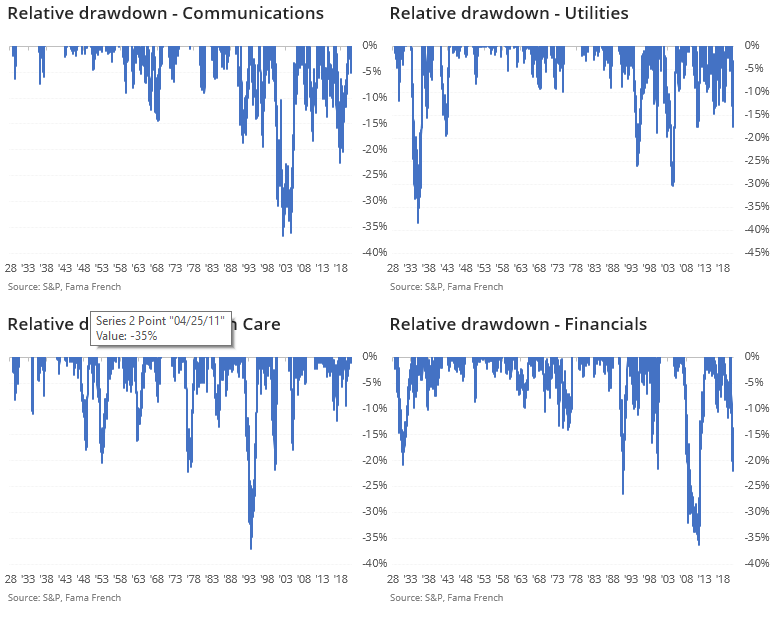

The current drawdown in energy is now about 60% more than the S&P's, by far the worst of any sector in history. It exceeds the relative losses in tech after the internet bubble burst and devastation in financials following the Great Financial Crisis. Below, we zoom in on each individual sector once its relative drawdown neared or exceeded -35%.

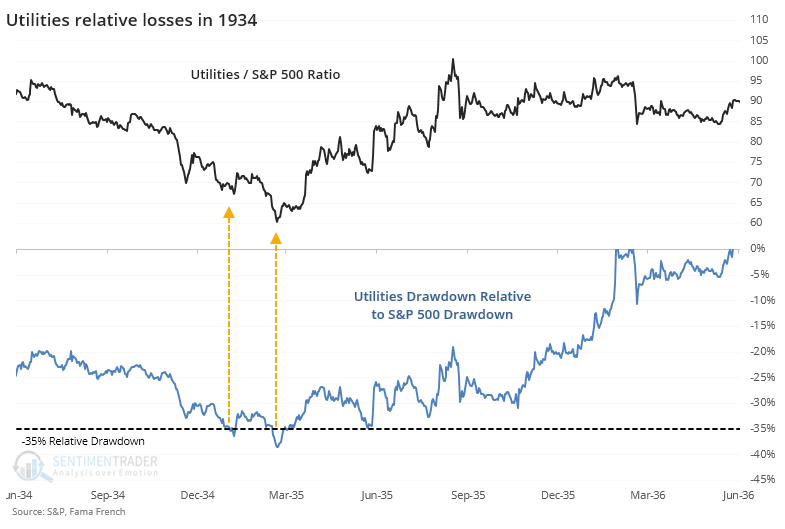

When utilities suffered this much in 1934, the ratio of that sector to the broader S&P turned and went on a year-long recovery.

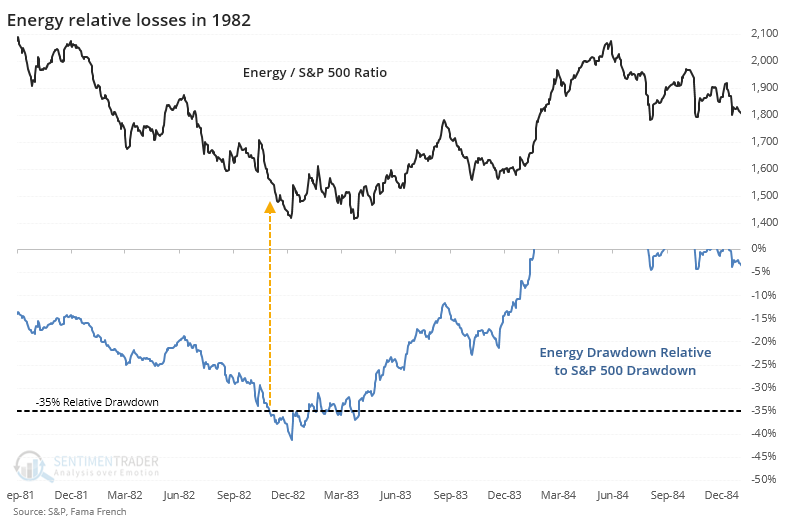

The only other time when energy dropped 35% more than the broader market was in 1982, which preceded a little more weakness, then years of outperformance.

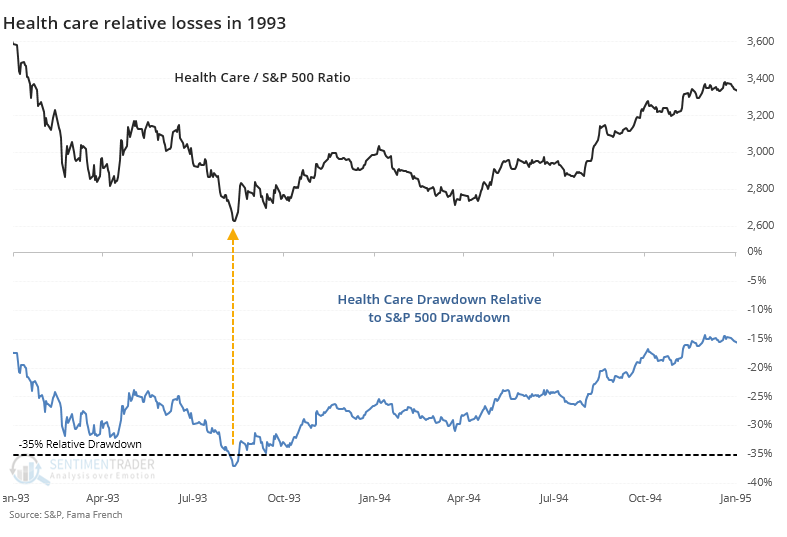

Health care stocks suffered relative devastation in 1993, which marked the bottom for that sector versus the broader market.

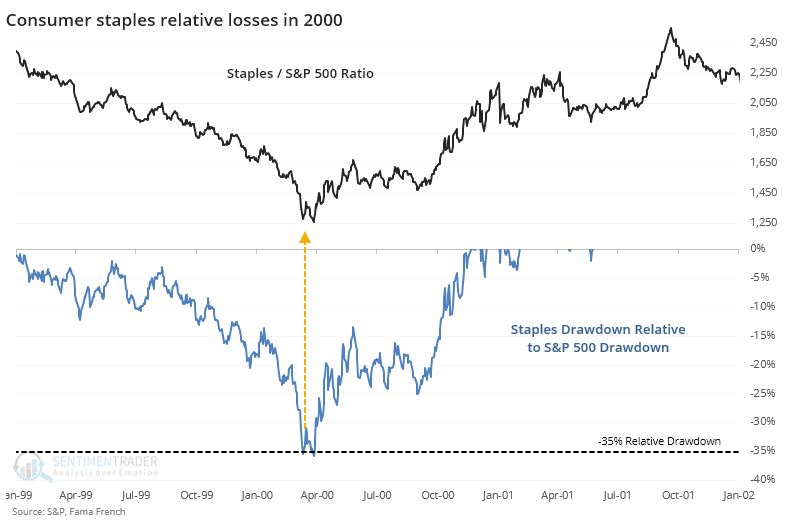

When staples fell this much relative to the broader market in 2000, they turned immediately and enjoyed massive outperformance.

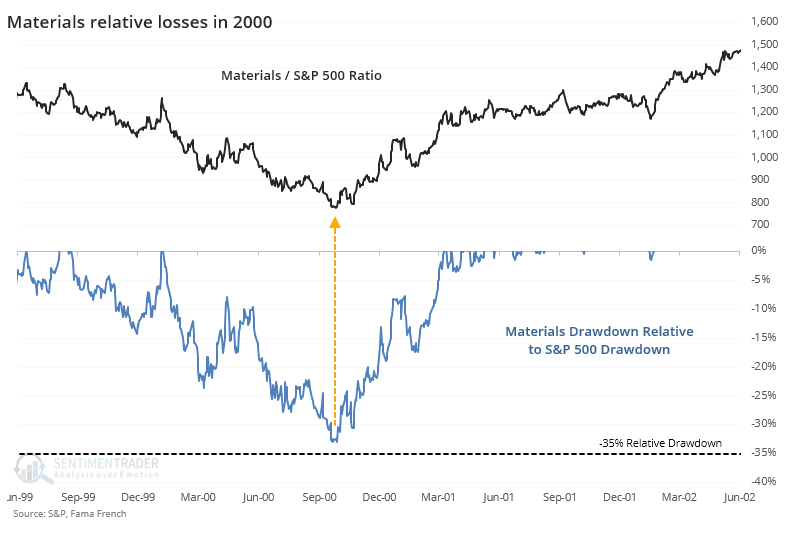

Materials stocks didn't quite fall more than 35% than the broader market in 2000, but got close, and then outperformed.

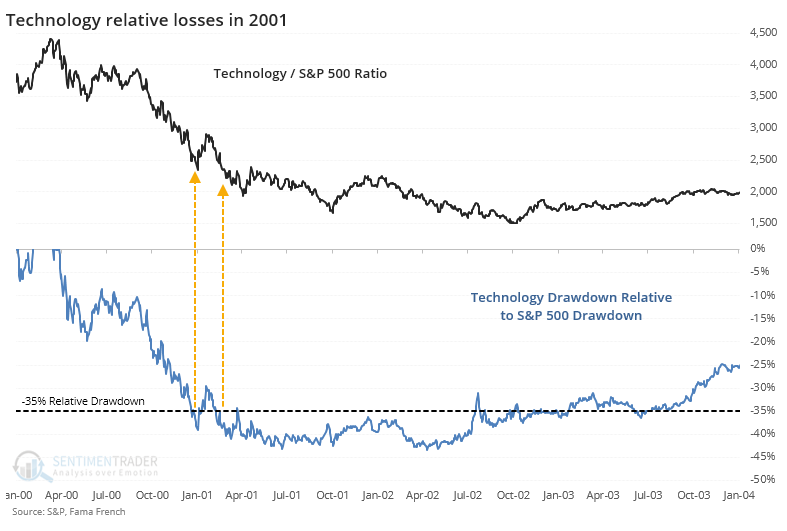

When tech stocks first dropped 35% more than the broader market in 2001, they briefly rebounded, then fell into a much more prolonged malaise.

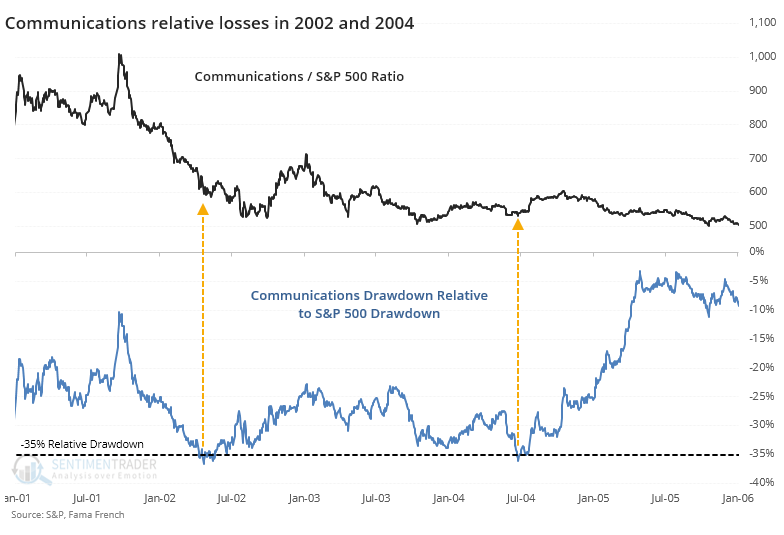

Communication stocks mostly stabilized or outperformed once their relative drawdowns exceeded 35%.

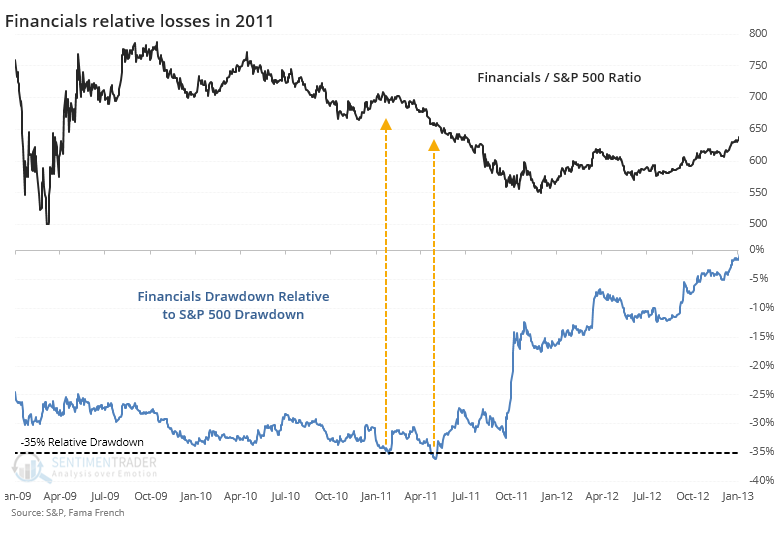

Financials got hit hard during the financial crisis, but their relative losses weren't 35% worse than the broader market's until 2011. Unlike other sectors, this did not lead to outperformance in the year(s) ahead.

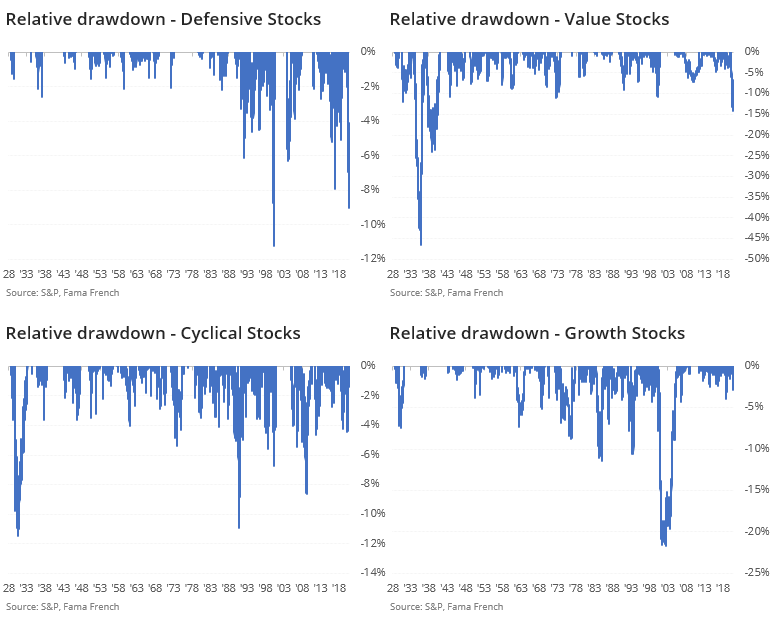

We can see this big shift in investor preferences in the past year among defensive and value stocks relative to cyclical and growth stocks. Defensive stocks dropped about 9% more from their highs than did the S&P, and value stocks about 15% more. Both are among the worst relative losses in 90 years for any of the factors.

The rout in energy stocks is historic, and maybe that's enough of a warning sign. No other sector has seen as much selling pressure in 90 years. Other times that selling pressure reached a lesser extreme, those sectors had a very strong tendency to outperform over the next 1-3 years. Energy hasn't done that and has only gone on to even further extremes.

That raises the chance of a "this time is different" scenario, the biggest extreme-can-always-get-more-extreme risk that contrary investors face. It seems unlikely that investors could suffer further relative losses in energy stocks, but that same thing could have been said 15% ago. The complete give-up in this sector should be a long-term positive, it just needs to see some stabilization for investors to realize things are morphing from bad to less bad.