December Tends To Peak...Now

In the last couple of reports, we've touched on the fact that the spread between Smart and Dumb Money Confidence is at a level that has preceded flat market returns at best over the short- to medium-term.

Same goes for the percentage of our indicators showing an optimistic vs pessimistic extreme, and short- and medium-term risk levels. They are highly correlated ways of looking at the same thing.

We noted heading into the month that December is known for positive seasonality, but less known is that the month has often struggled in the first half and rallied in the latter half. So far it's done nothing but rally.

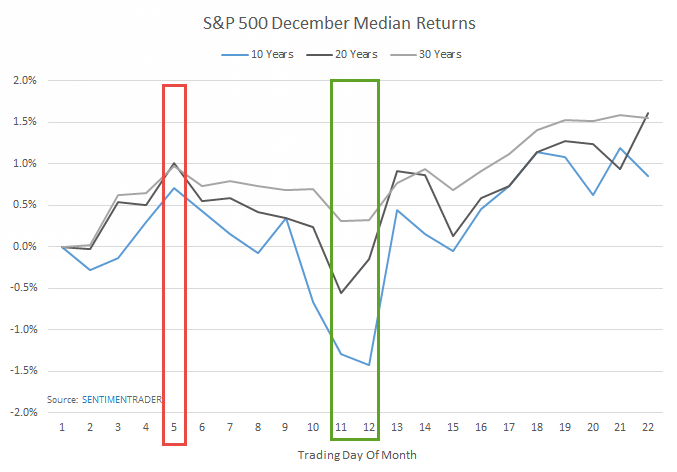

If we look at the month's median returns over the past 10, 20, and 30 years, we can see that it has peaked on the 5th trading day of the month, which was Wednesday.

On average, it has declined between 1%-2% from the 5th trading day through the 11th trading day, and didn't surpass its peak from the 5th trading day until the 17th trading day.

This is very short-term, but it does suggest that if the sentiment and momentum extremes are going to have an impact, then the next week or so has the highest probability of showing some weakness, however moderate it may be for this time of year.