Headlines

|

|

Stocks' Internal Momentum Has Turned Up:

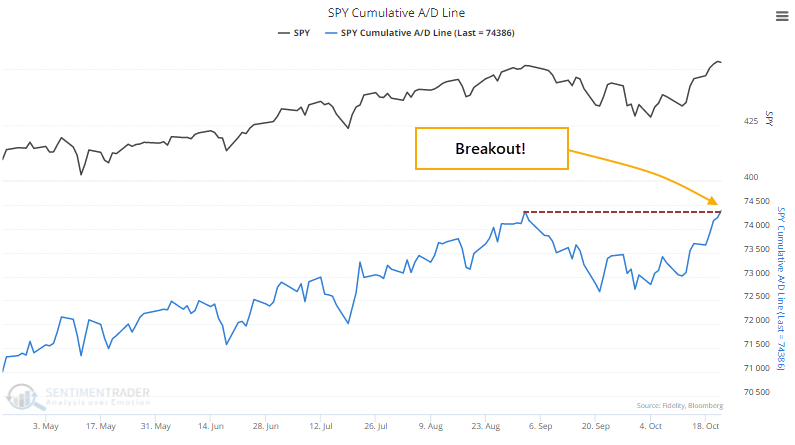

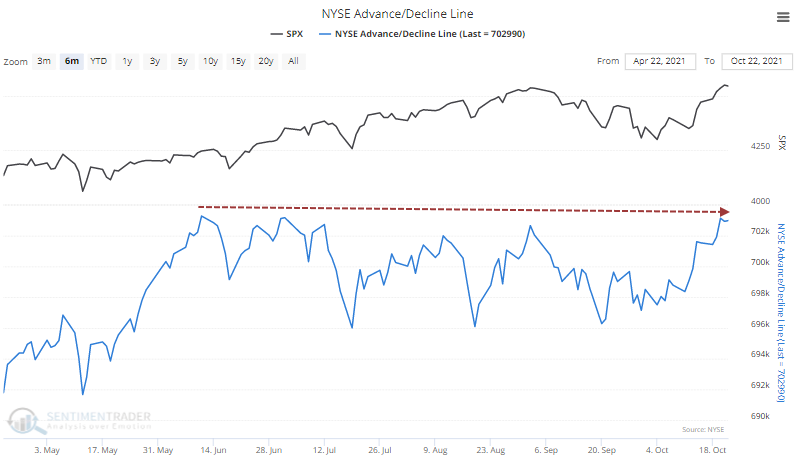

The Advance/Decline Line for the S&P 500 has broken out to a new multi-year high. Since the inception of the index, a new high in its breadth has been a positive development, with the index showing a much lower probability of a major decline within the next three months.

Bottom Line:

STOCKS: Weak buy

The speculative frenzy in February is wrung out. There are some signs of pessimism, but the most compelling data show that buyers consistently tend to return once the first signs of extreme momentum end, especially as we head into a seasonally positive time of year. See the Outlook & Allocations page for more. BONDS: Hold

Various parts of the market got hit in March, with the lowest Bond Optimism Index we usually see during healthy environments. Bond prices have modest recovered and there is no edge among the data we follow. GOLD: Hold

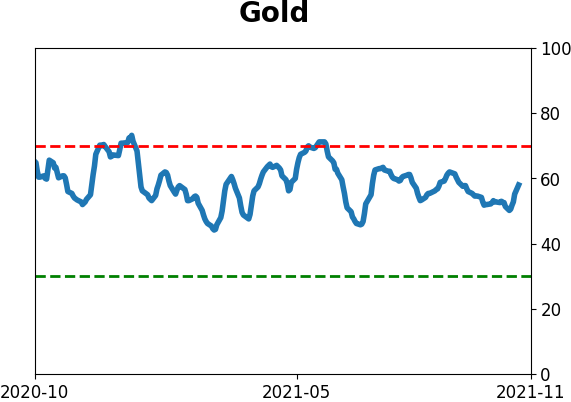

Gold and miners were rejected after trying to recover above their 200-day averages in May. Lately, some medium-term (not long-term) oversold extremes in breadth measures among miners have triggered.

|

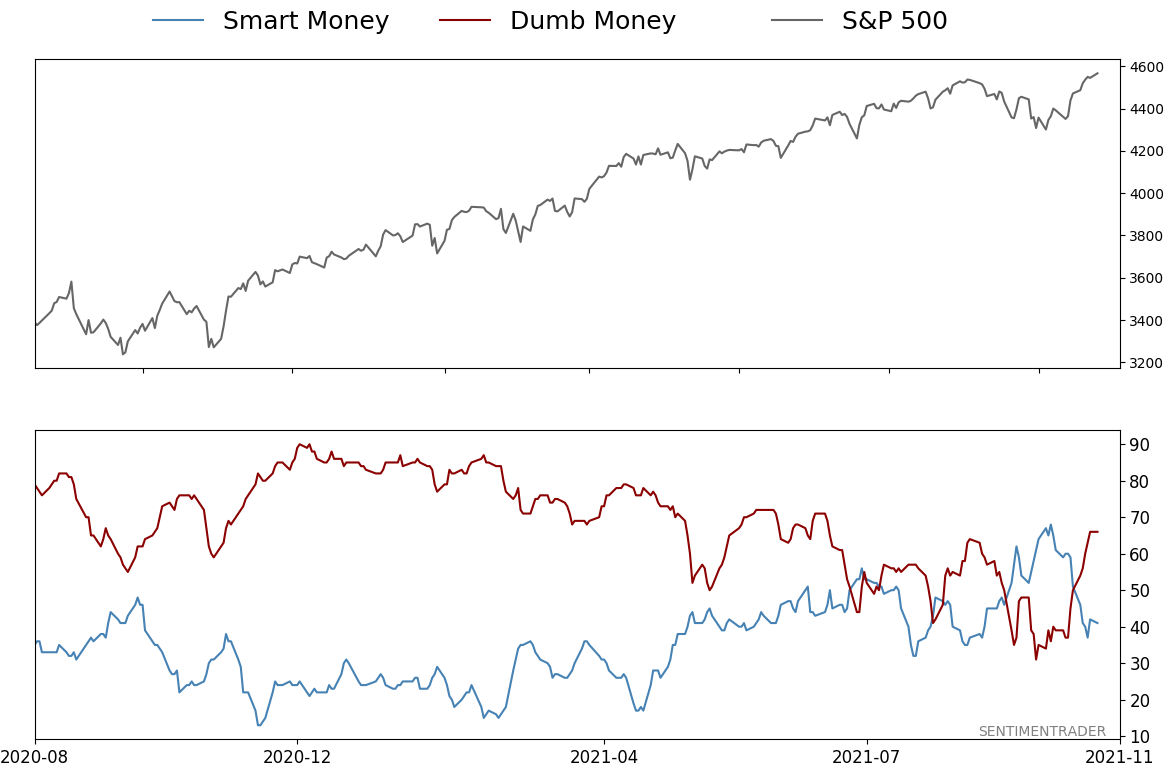

Smart / Dumb Money Confidence

|

Smart Money Confidence: 41%

Dumb Money Confidence: 66%

|

|

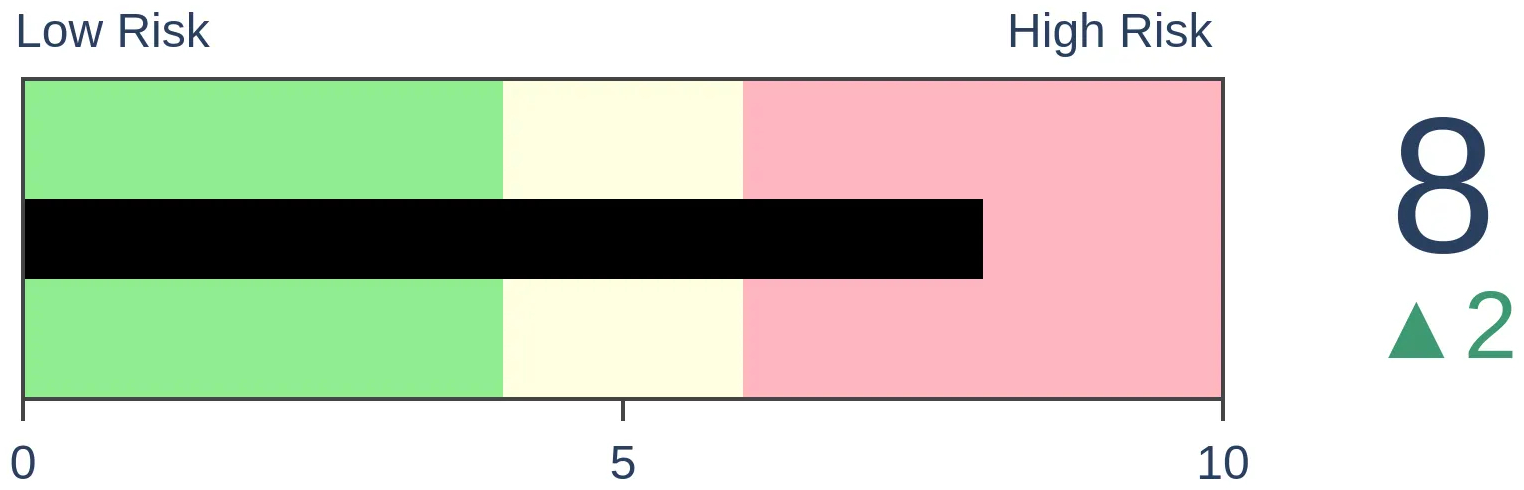

Risk Levels

Stocks Short-Term

|

Stocks Medium-Term

|

|

Bonds

|

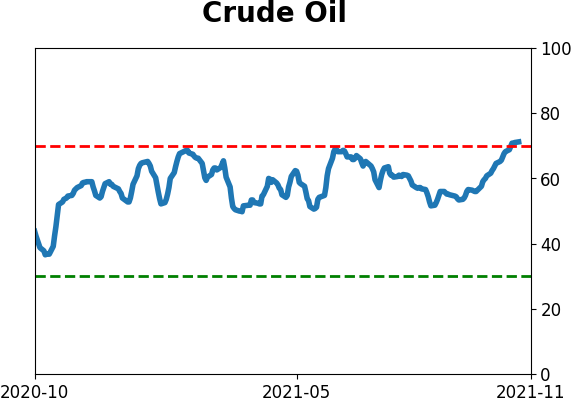

Crude Oil

|

|

Gold

|

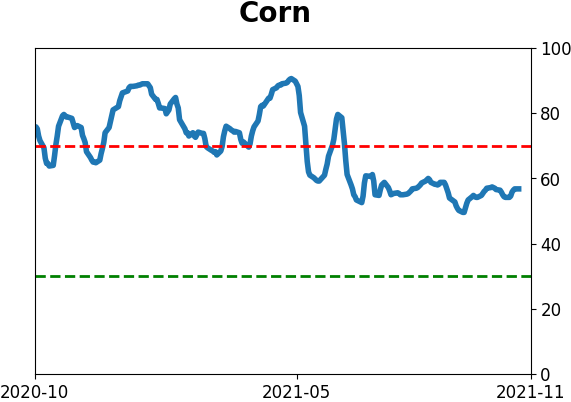

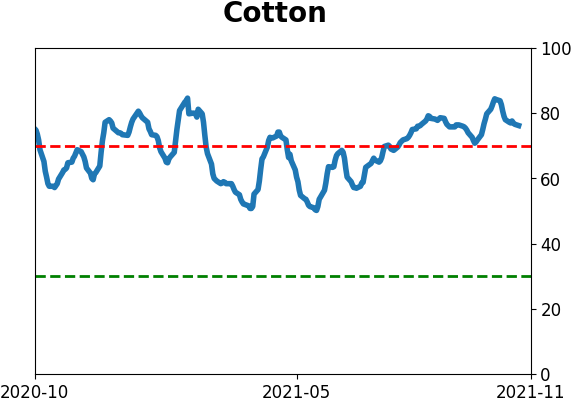

Agriculture

|

|

Research

By Jason Goepfert

BOTTOM LINE

The Advance/Decline Line for the S&P 500 has broken out to a new multi-year high. Since the inception of the index, a new high in its breadth has been a positive development, with the index showing a much lower probability of a major decline within the next three months.

FORECAST / TIMEFRAME

None

|

The most benchmarked index in the world is trying to hold a breakout to record highs. Supporting its case is the fact that most of its stocks have been rising, and breadth within the index confirms its good performance.

Even though the S&P 500 settled back a bit on Friday, most of the stocks in the index gained ground. That was enough to push the S&P's Cumulative Advance/Decline Line to a new high, the first in more than 30 sessions.

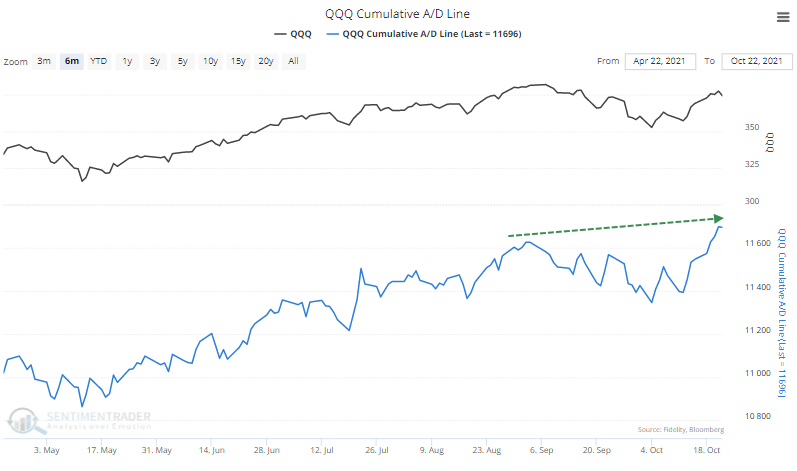

Among other major indexes, the Nasdaq 100 has also seen a breakout in its Advance/Decline Line.

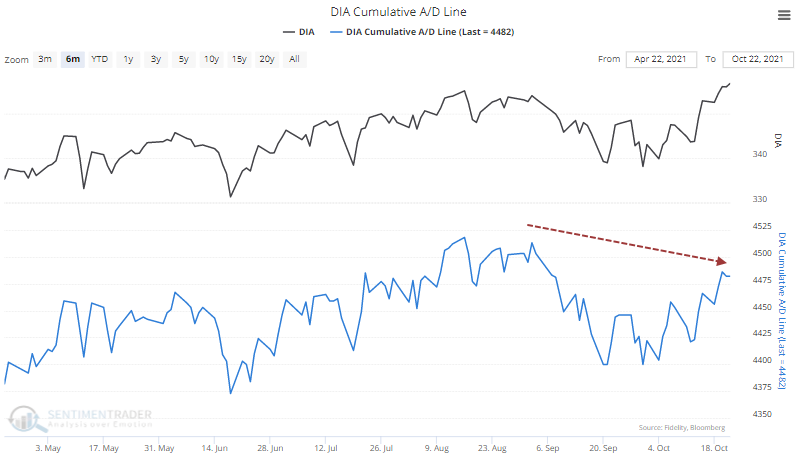

The Line for the Dow Industrials isn't quite there.

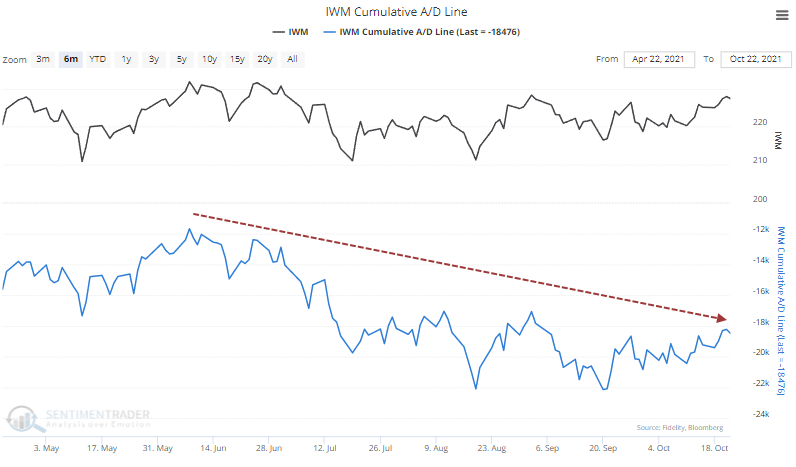

The biggest laggard, by far, is the small-cap Russell 2000.

Small-caps have a significant influence on the granddaddy of them all, for every security traded on the NYSE. That has also been lagging but is within spitting distance of a new high.

LESS CHANCE OF A BIG DECLINE

Many times over the past couple of decades, we've discussed the idea that stocks are less likely to suffer a large drawdown in the following months when the advance/decline line breaks out to a new high. We typically use the NYSE Advance/Decline Line, but our version of that indicator hasn't quite made it over the hump. It very well might on Monday if stocks have a good day.

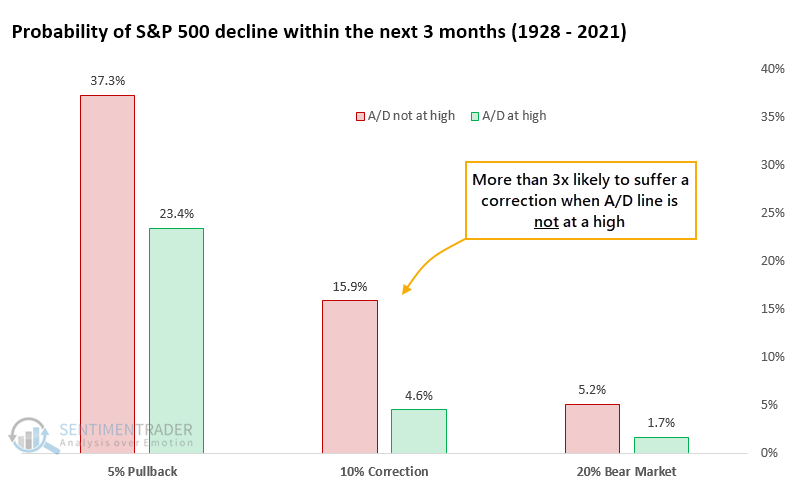

Below, we can see that since 1928, the S&P 500 was three times more likely to suffer a 10% decline at some point within the next three months if the S&P's Advance/Decline Line was not at a multi-year high. When it did break out to a new high, as it did on Friday, there was only a 4.6% probability of a 10% or greater decline within the next few months and less than a 2% chance of a 20% decline.

The S&P 500 can suffer a significant decline shortly after a breakout to a new high in the Advance/Decline Line. But it's exceptionally rare and comes quickly out of the blue. Since 1928, the only two instances were the Black Monday crash in October 1987 and the pandemic crash in March 2020.

OTHER INDICATORS TURNING UP

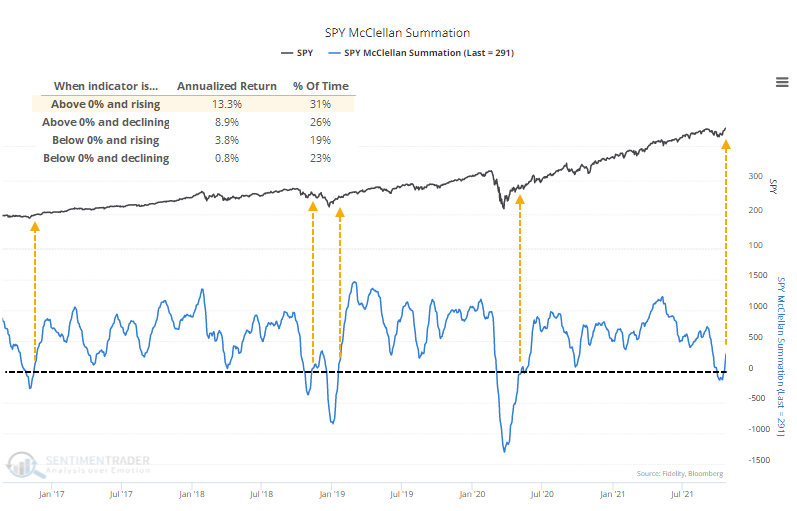

Thanks to last week's rally in most stocks, the McClellan Summation Index for the S&P 500 is now above zero, rising, and far from overbought - the best possible combination. That reverses the dip that we noted a couple of weeks ago.

Stocks within the S&P witnessed a short-term breadth thrust entering last week, and buyers have been persistent enough that it is positively influencing some of the more critical, longer-term breadth indicators. Again, that doesn't mean the index can't suffer a big decline in the months ahead - we should know by now that anything can happen at any time - but we try to focus on base rates and probabilities, and those argue for mostly clear sailing ahead.

Active Studies

| Time Frame | Bullish | Bearish | | Short-Term | 1 | 0 | | Medium-Term | 8 | 0 | | Long-Term | 11 | 5 |

|

Indicators at Extremes

Portfolio

| Position | Description | Weight % | Added / Reduced | Date | | Stocks | RSP | 10.5 | Added 6.4% | 2021-10-01 | | Bonds | 23.9% BND, 6.9% SCHP | 31.5 | Reduced 7.1% | 2021-05-19 | | Commodities | GCC | 2.6 | Reduced 2.1%

| 2020-09-04 | | Precious Metals | GDX | 4.2 | Reduced 4.2% | 2021-05-19 | | Special Situations | 9.8% KWEB, 4.7% XLE, 2.9% PSCE | 17.3 | Added 9.78% | 2021-10-01 | | Cash | | 34.0 | | |

|

Updates (Changes made today are underlined)

Much of our momentum and trend work has remained positive for several months, with some scattered exceptions. Almost all sentiment-related work has shown a poor risk/reward ratio for stocks, especially as speculation drove to record highs in exuberance in February. Much of that has worn off, and most of our models are back toward neutral levels. There isn't much to be excited about here. The same goes for bonds and even gold. Gold has been performing well lately and is back above long-term trend lines. The issue is that it has a poor record of holding onto gains when attempting a long-term trend change like this, so we'll take a wait-and-see approach. Momentum has ebbed quickly in recent weeks, and nearing oversold levels in some indicators. This can be a dangerous area, with a lot of short-term volatility, but we'd be more inclined to add medium- to long-term exposure rather than sell on much more of a decline, thanks to already rock-bottom exposure. Other areas look more attractive, including some overseas markets. RETURN YTD: 12.1% 2020: 8.1%, 2019: 12.6%, 2018: 0.6%, 2017: 3.8%, 2016: 17.1%, 2015: 9.2%, 2014: 14.5%, 2013: 2.2%, 2012: 10.8%, 2011: 16.5%, 2010: 15.3%, 2009: 23.9%, 2008: 16.2%, 2007: 7.8%

|

|

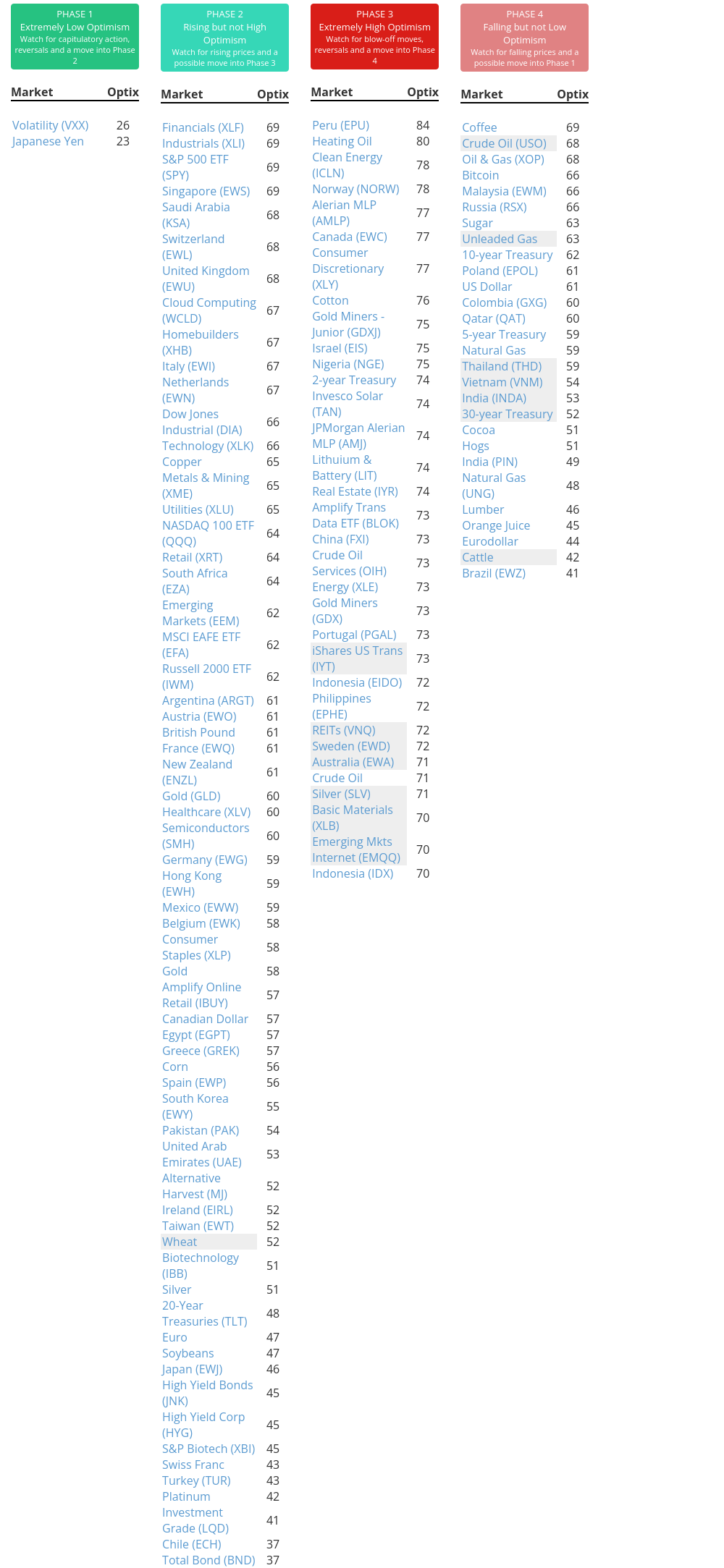

Phase Table

Ranks

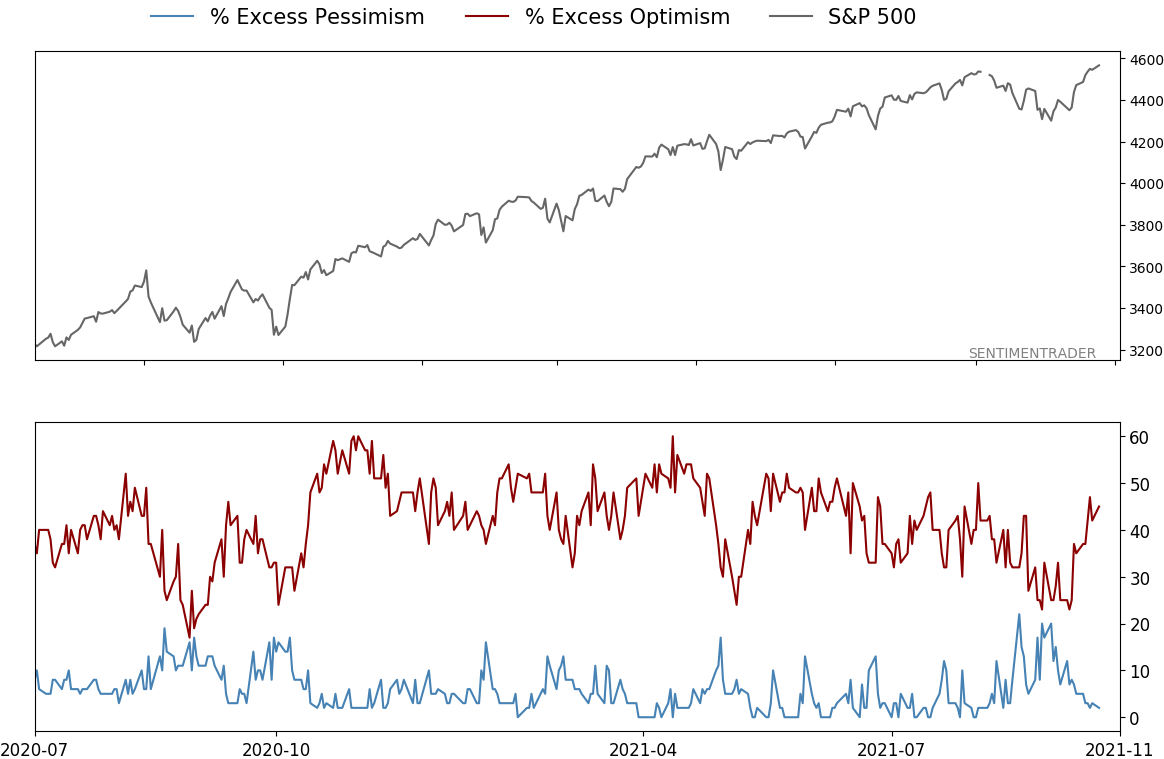

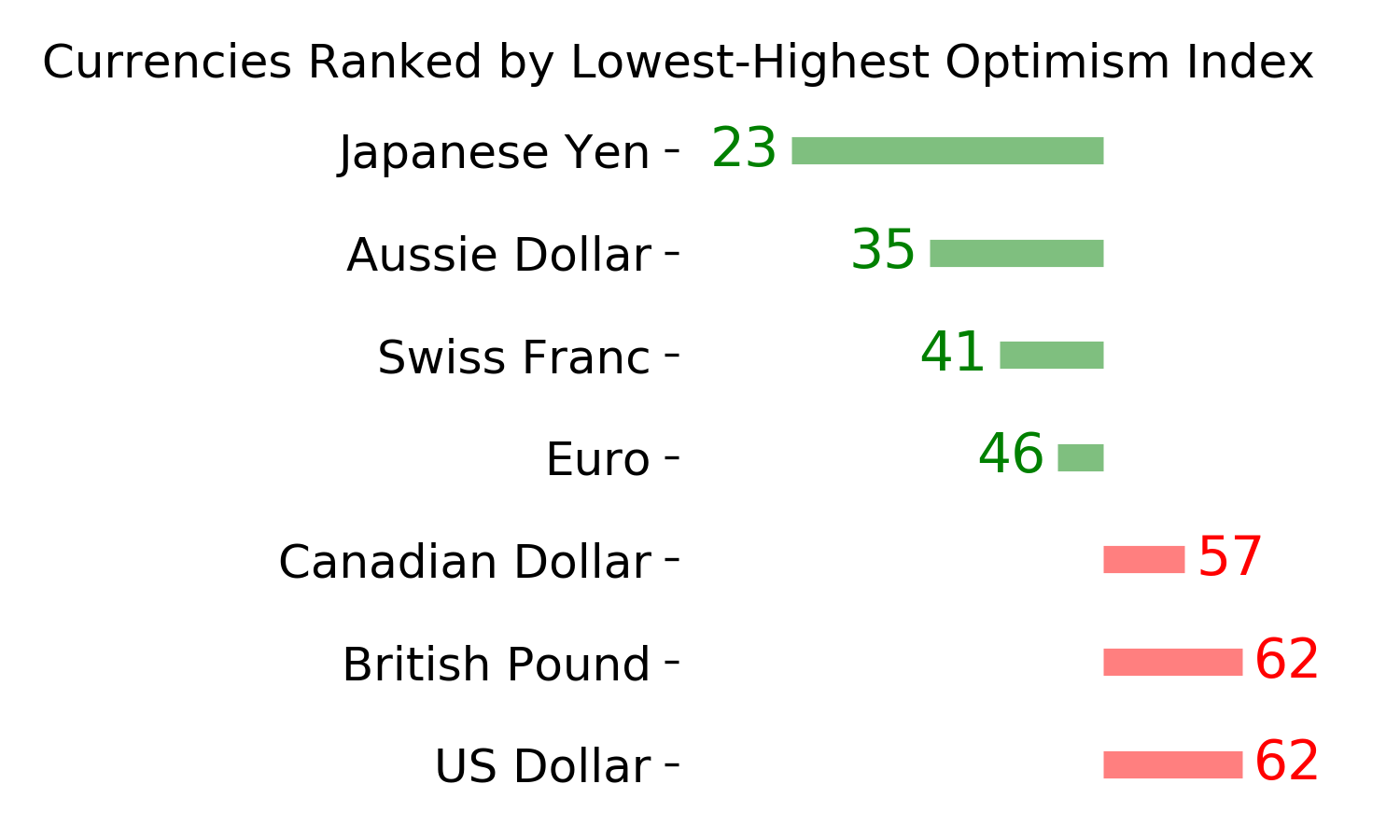

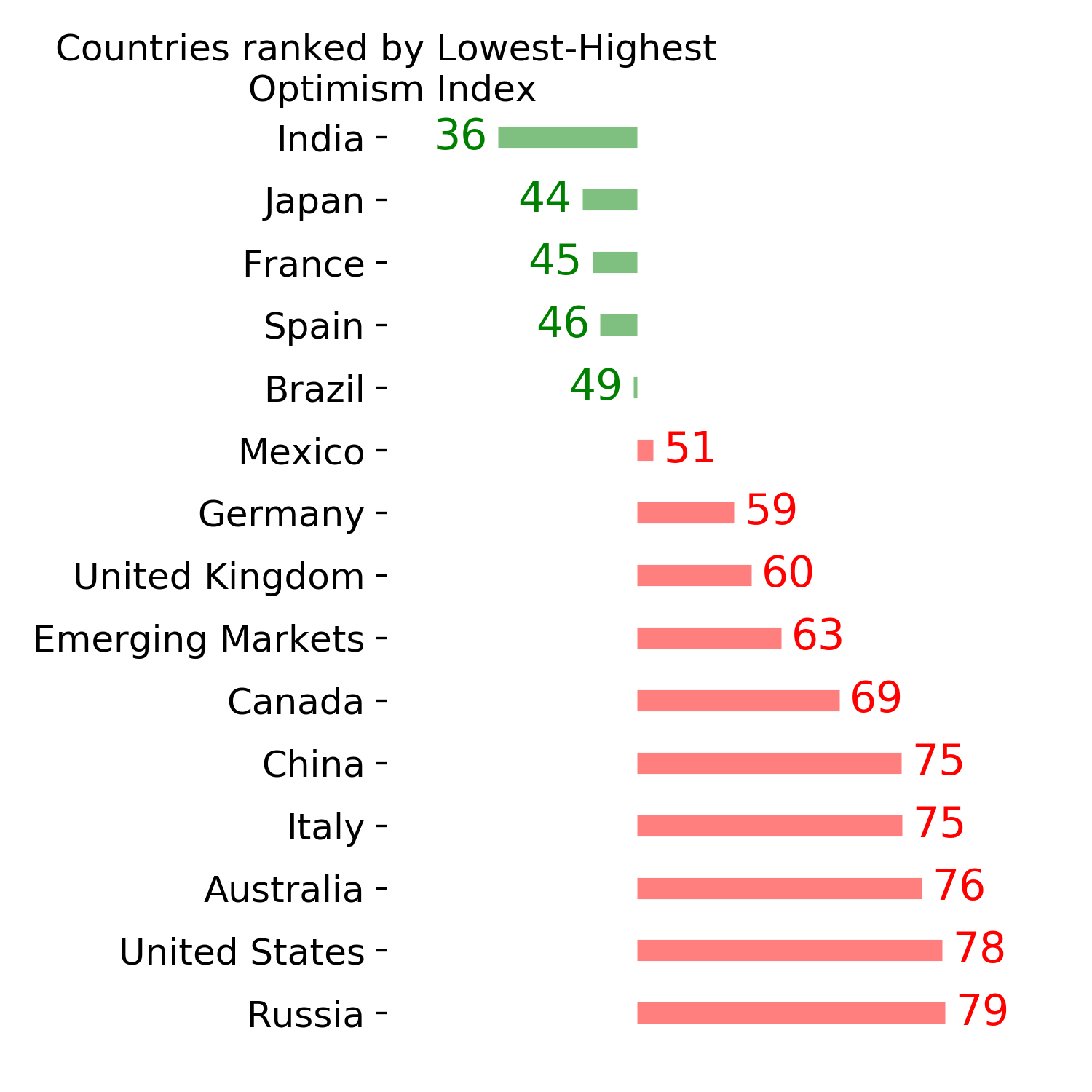

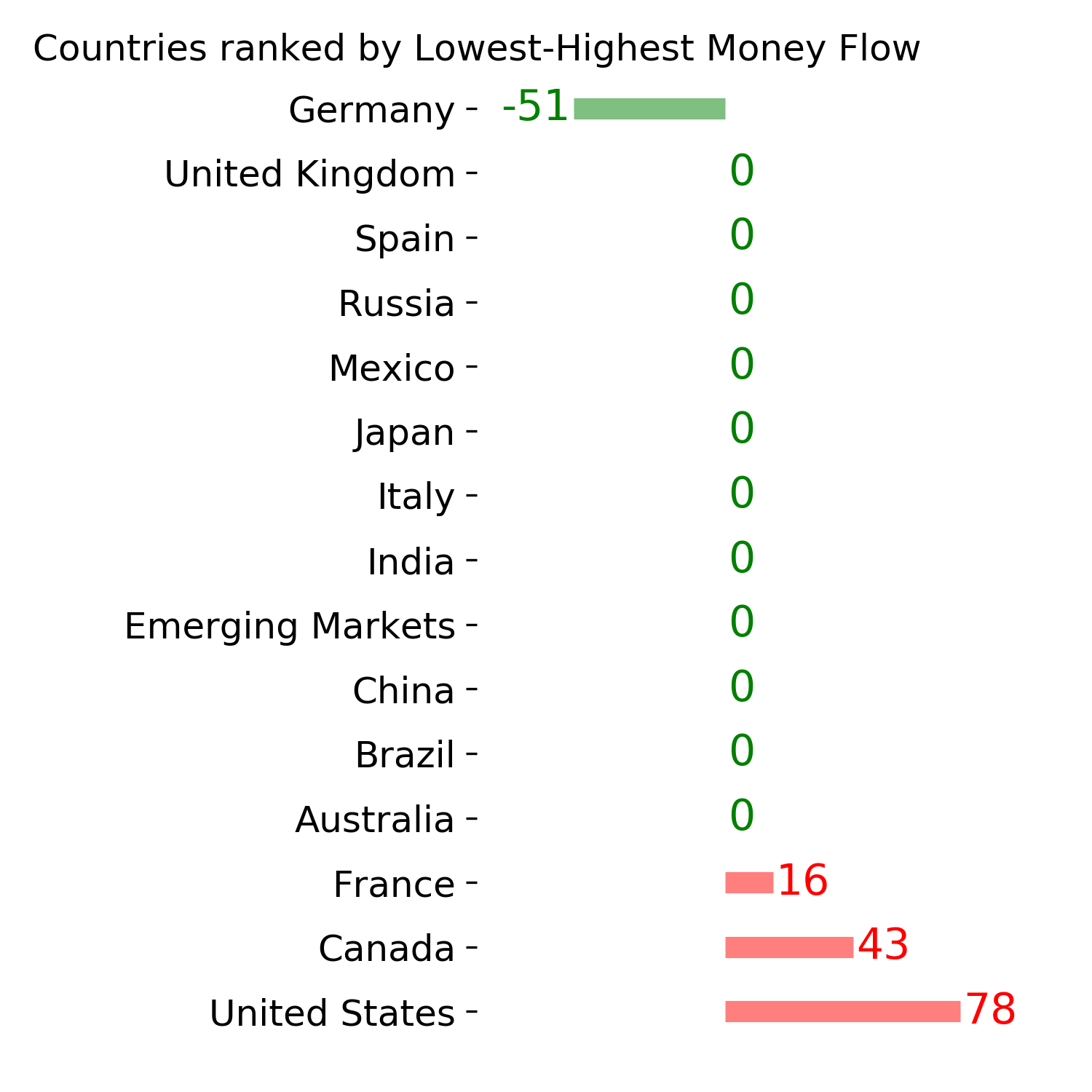

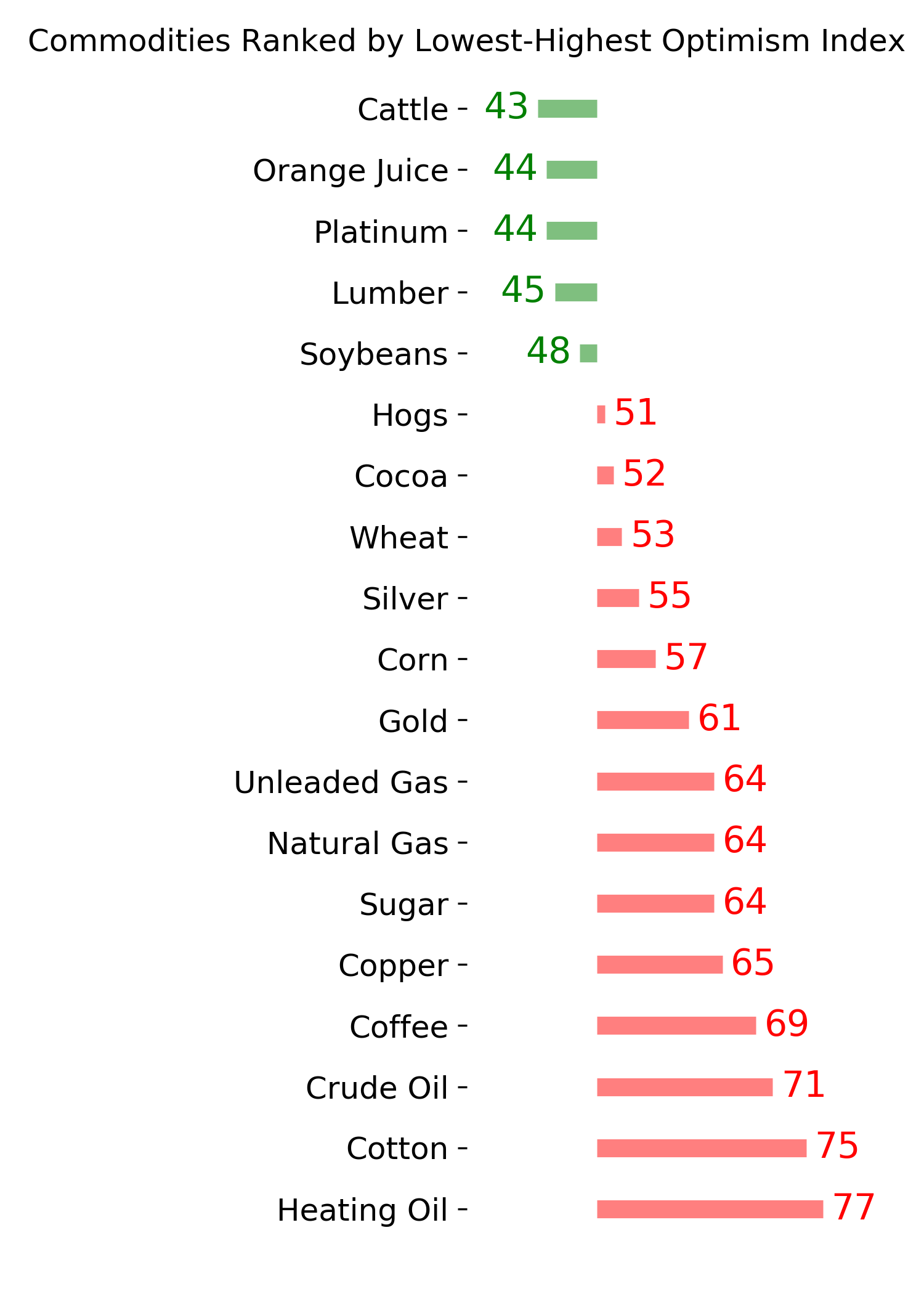

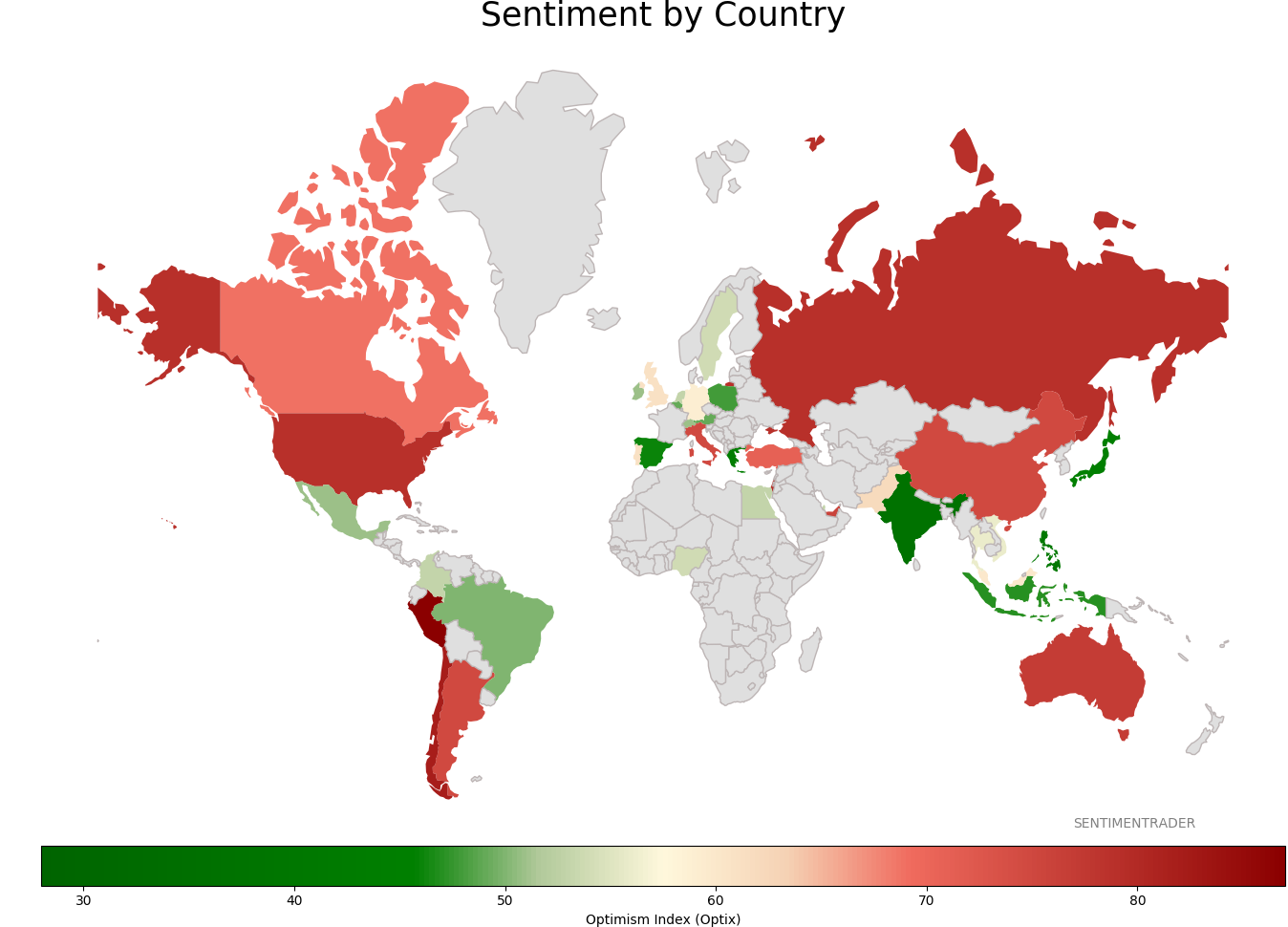

Sentiment Around The World

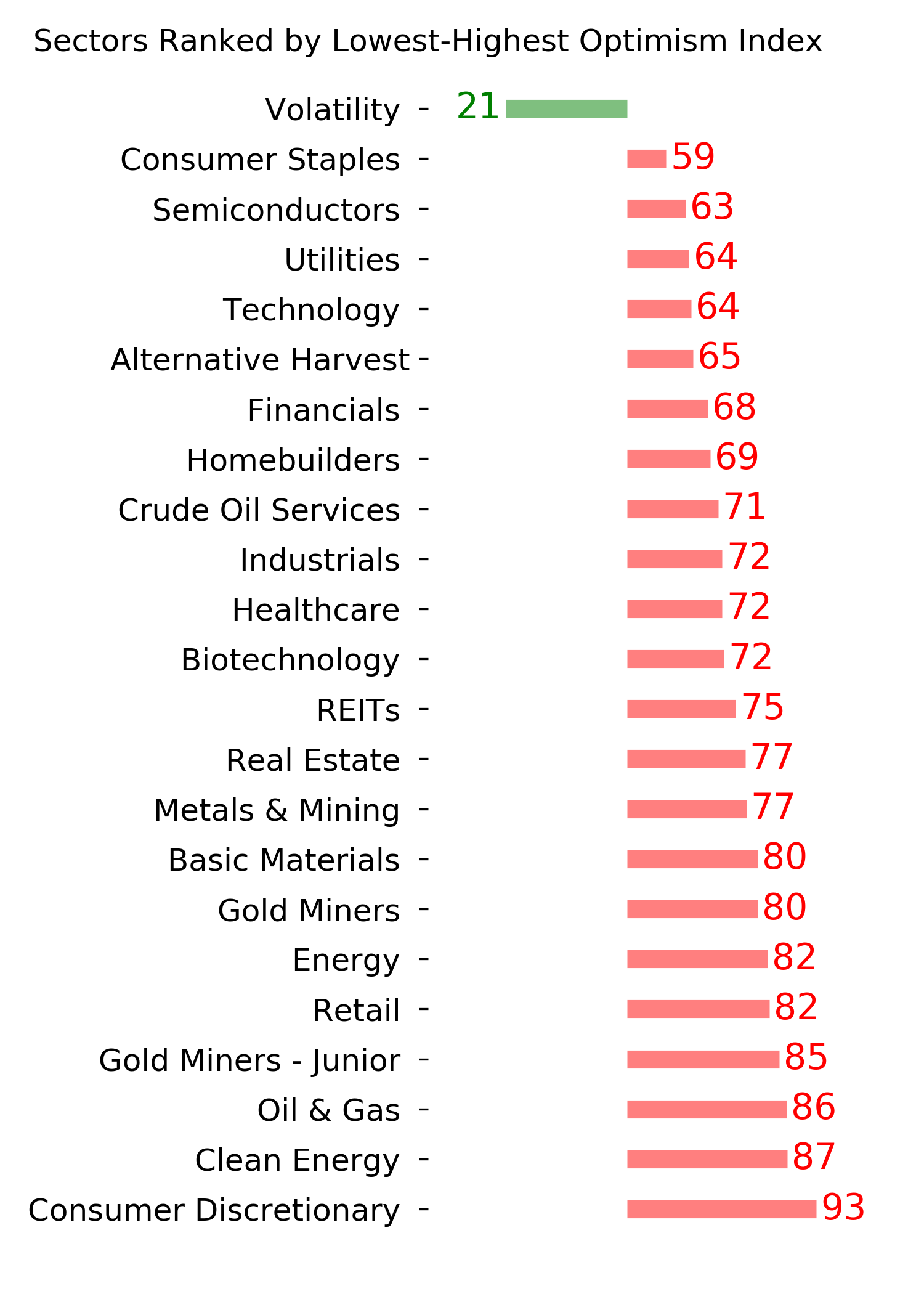

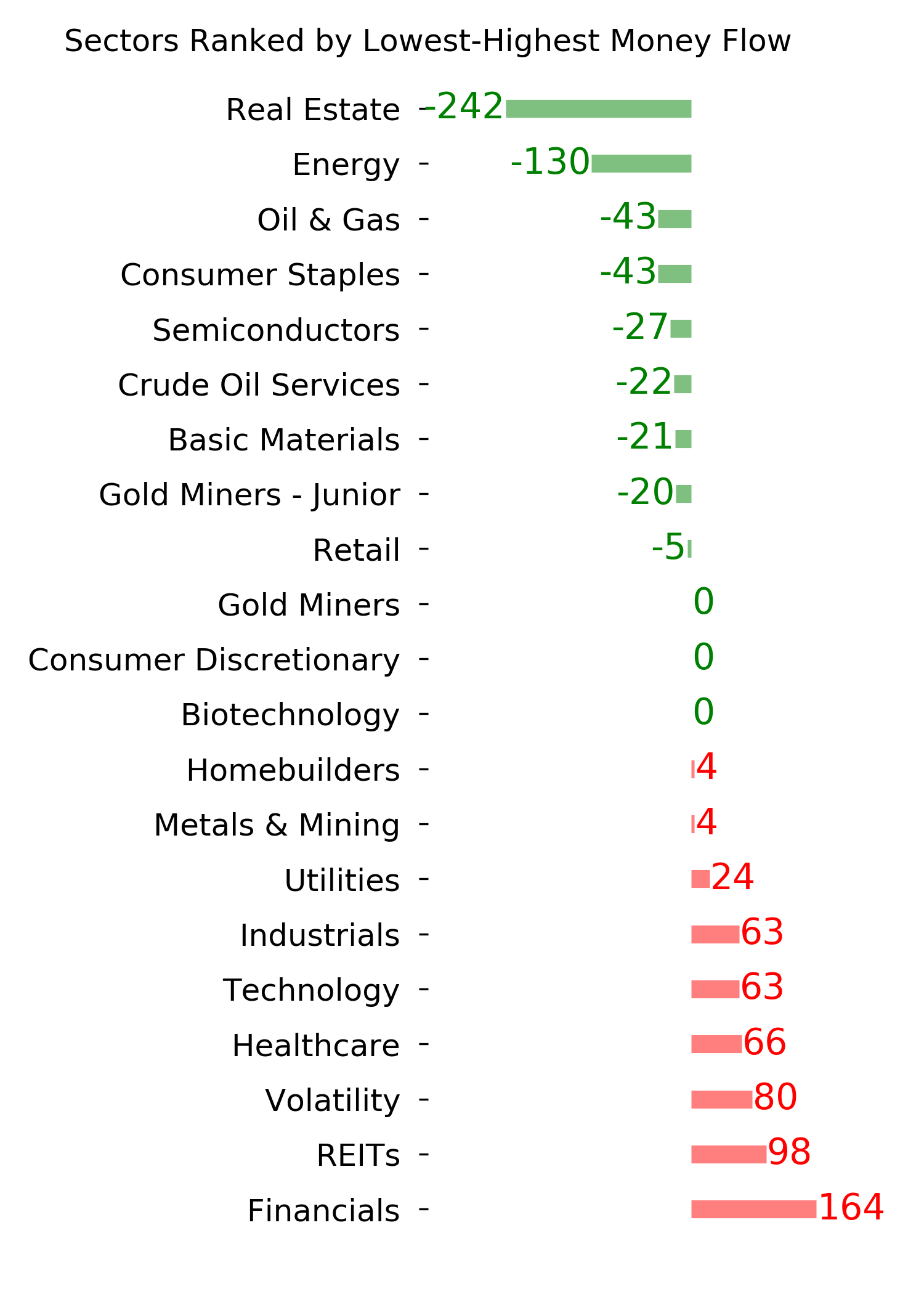

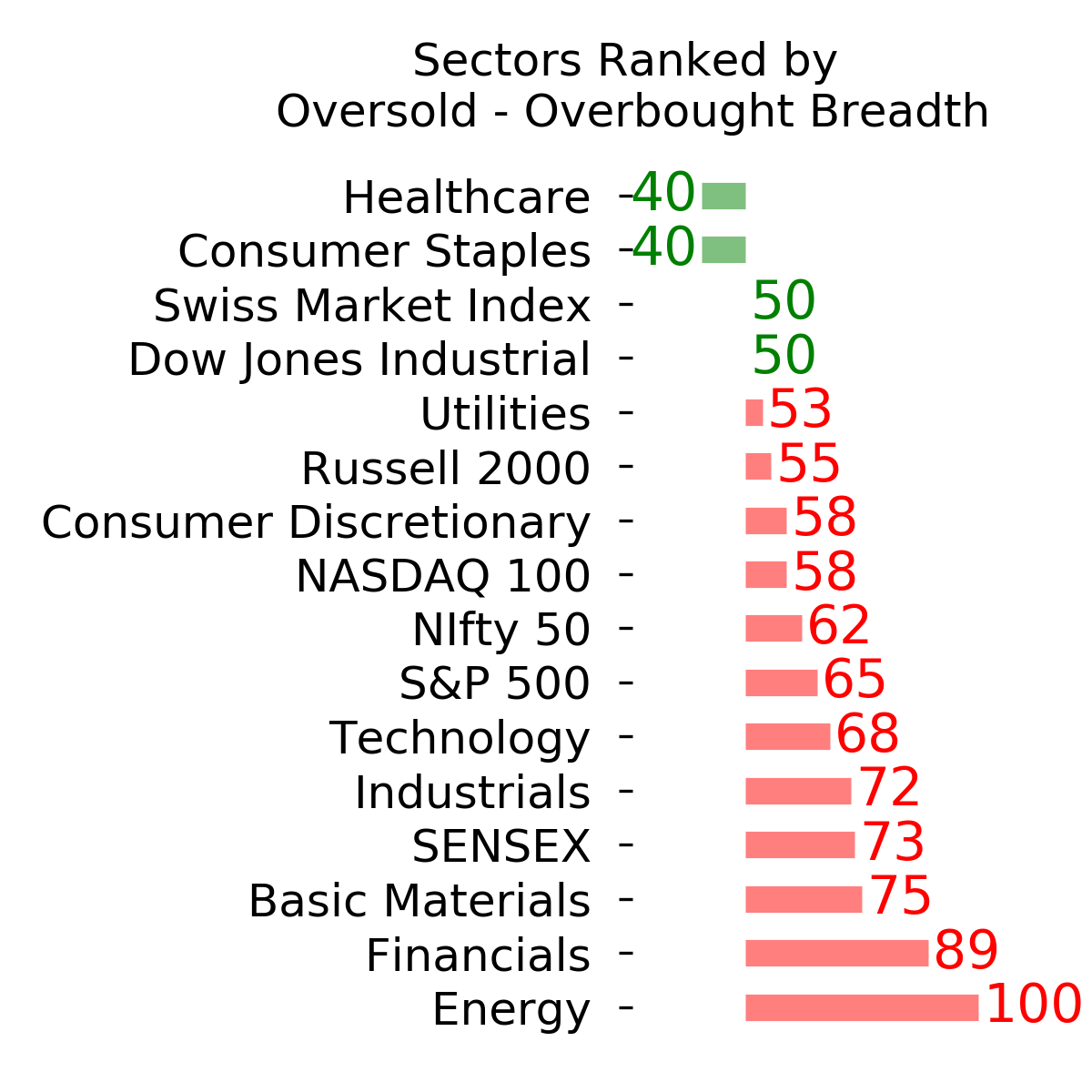

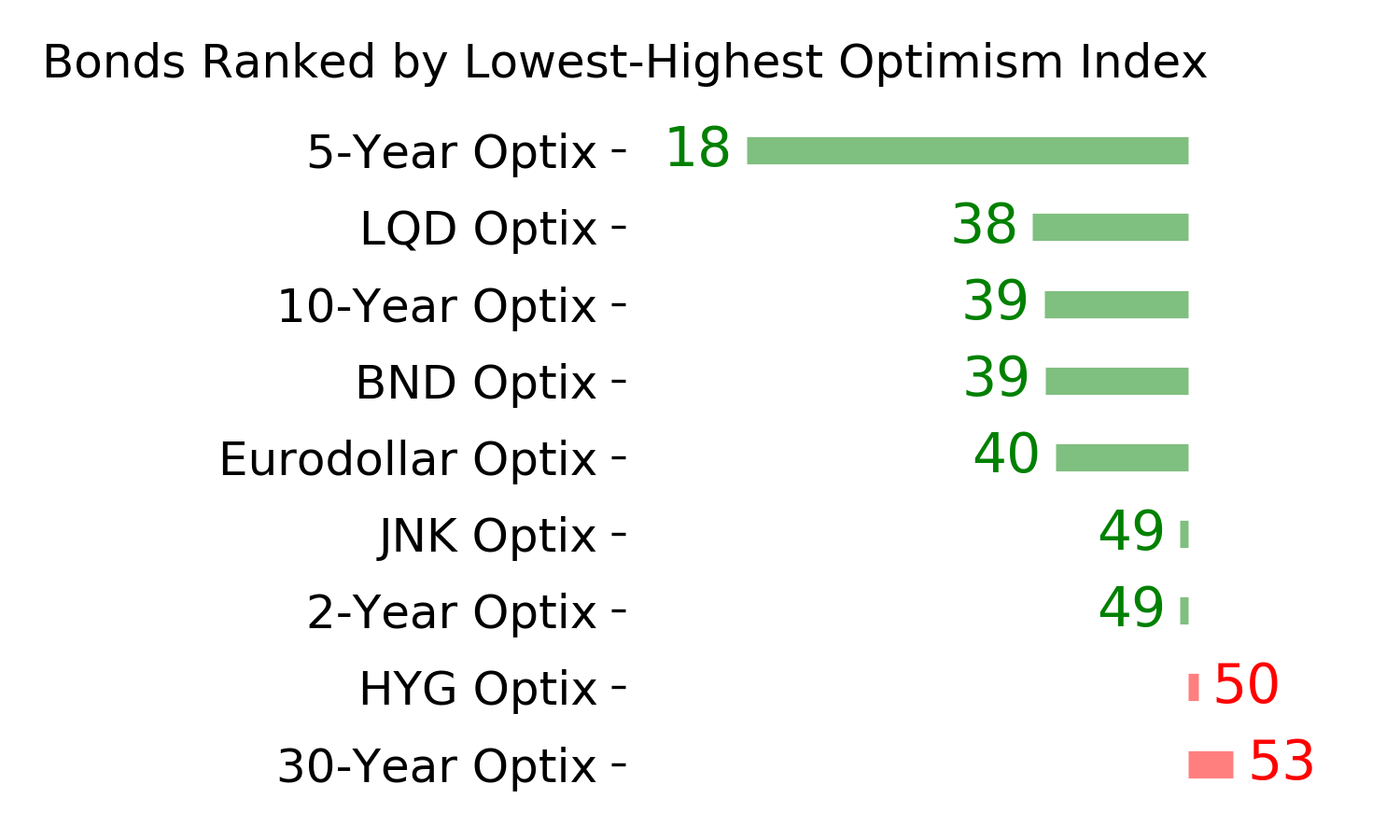

Optimism Index Thumbnails

|

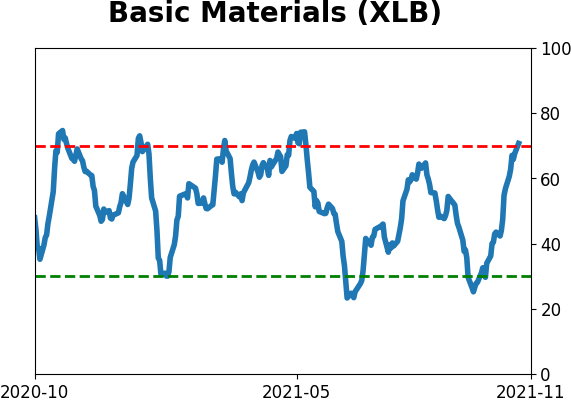

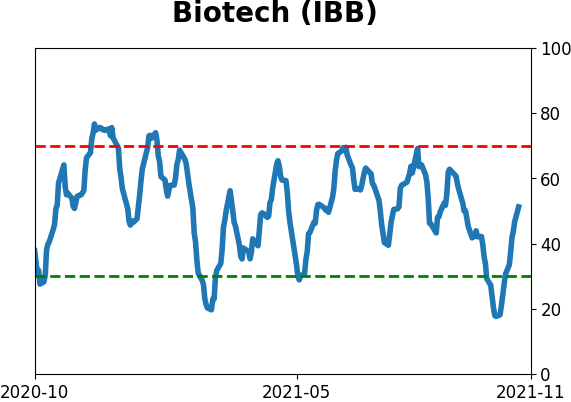

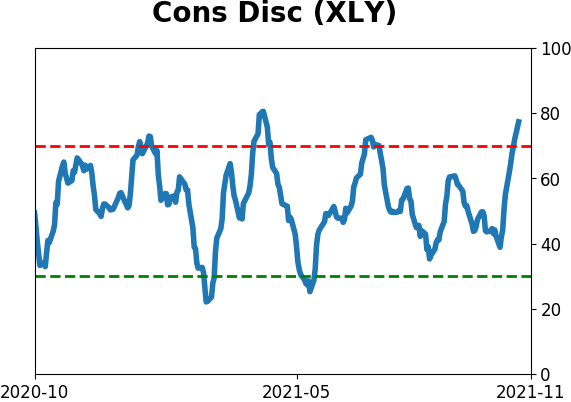

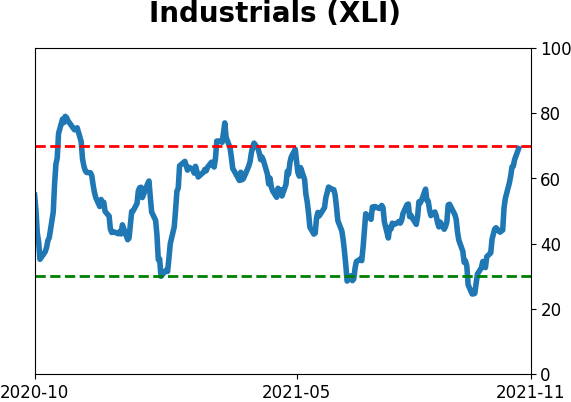

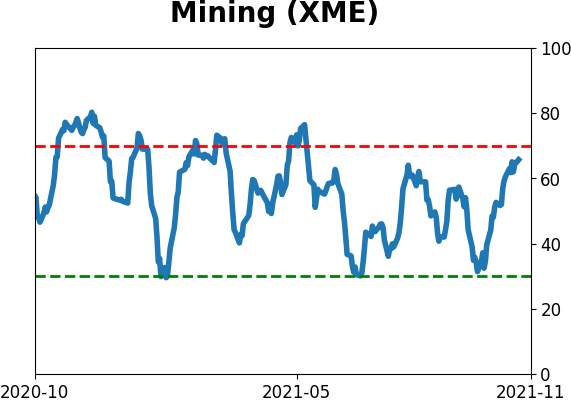

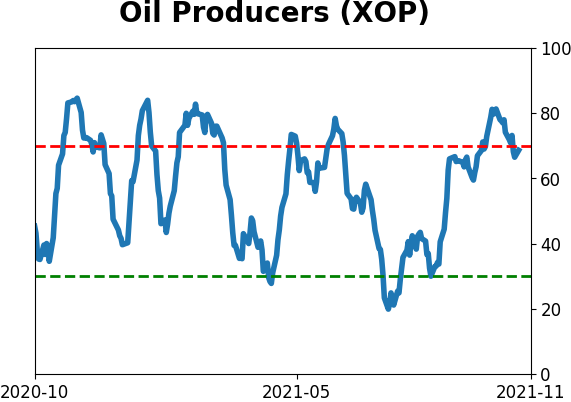

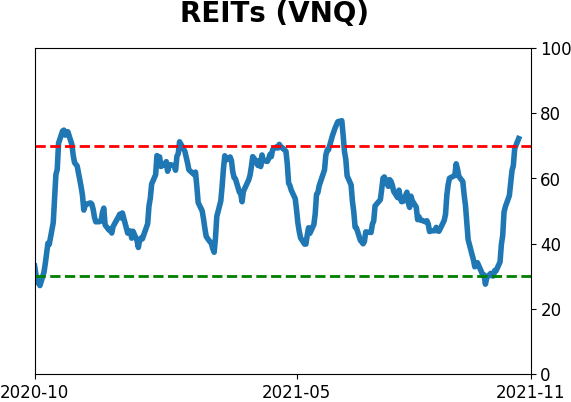

Sector ETF's - 10-Day Moving Average

|

|

|

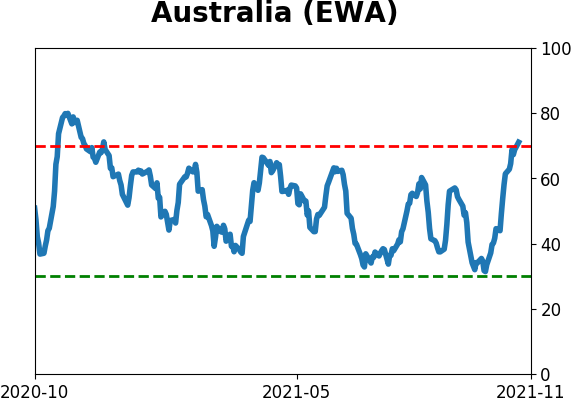

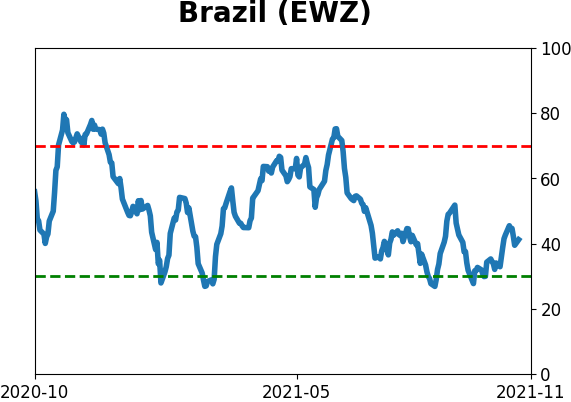

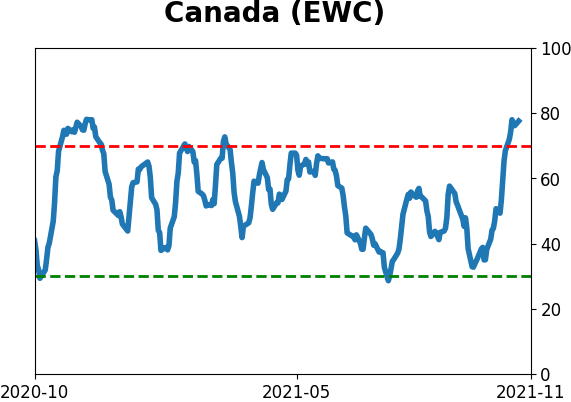

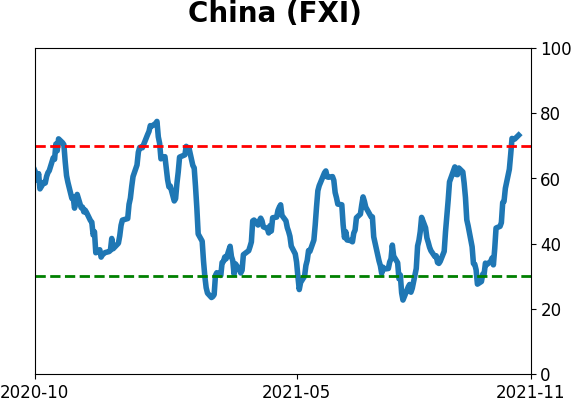

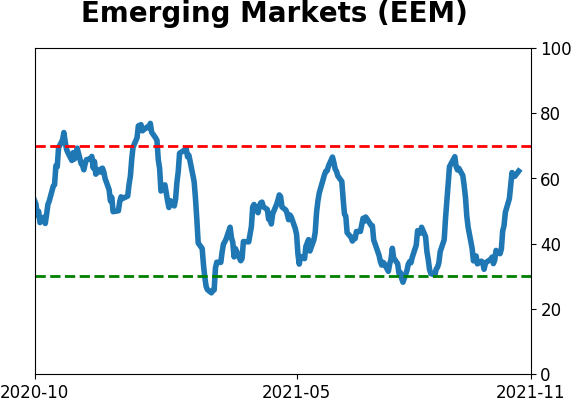

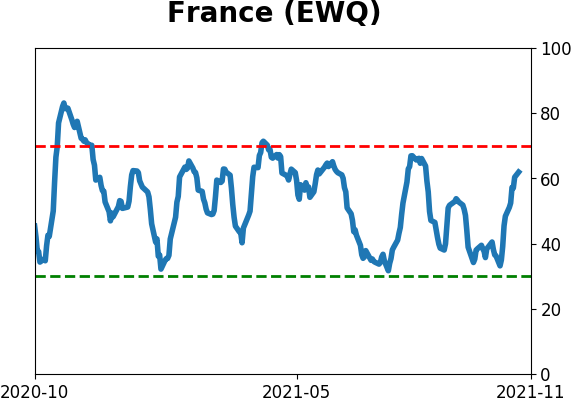

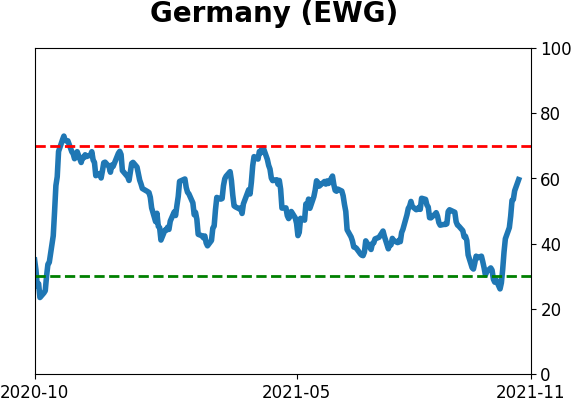

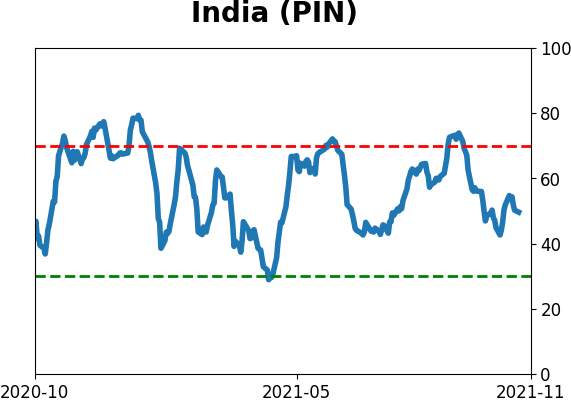

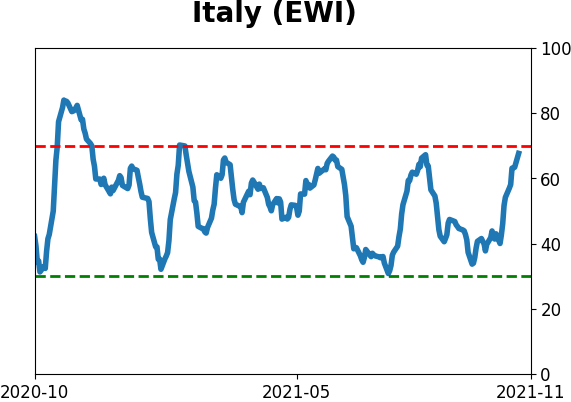

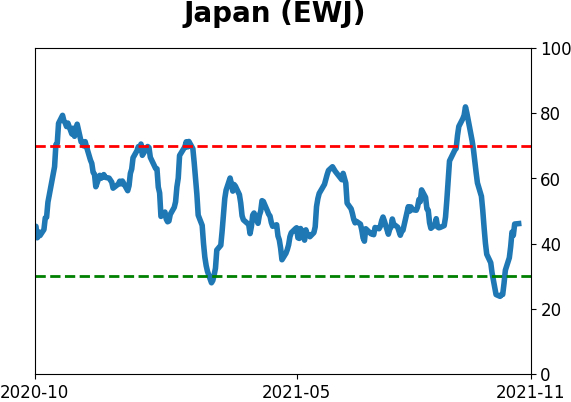

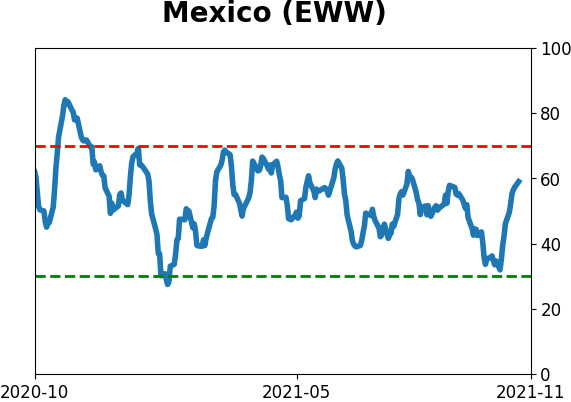

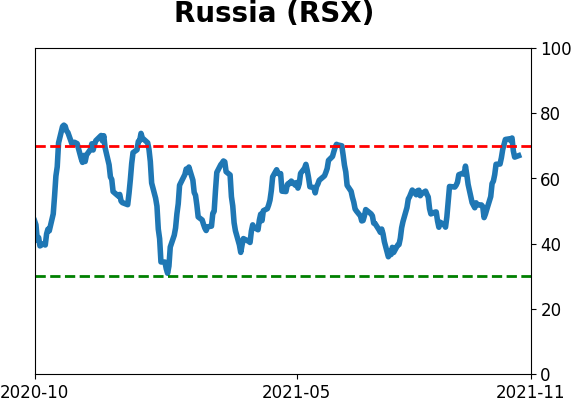

Country ETF's - 10-Day Moving Average

|

|

|

Bond ETF's - 10-Day Moving Average

|

|

|

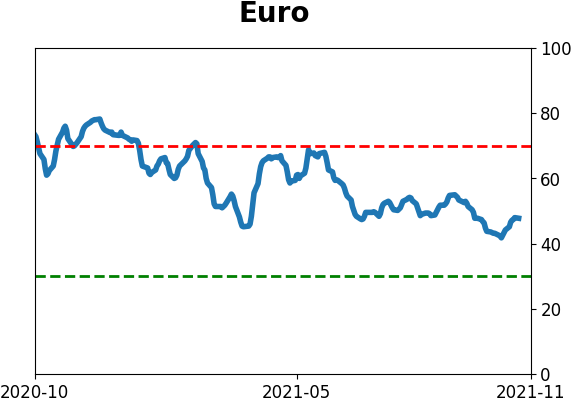

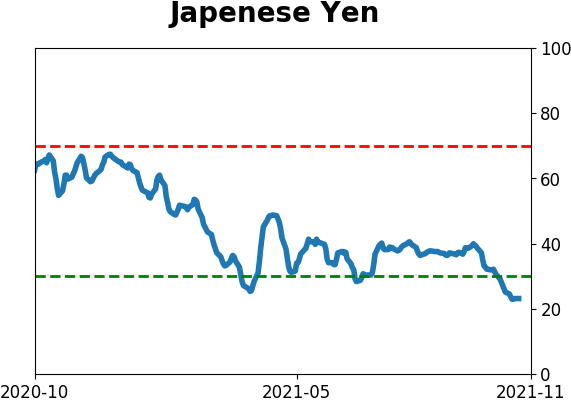

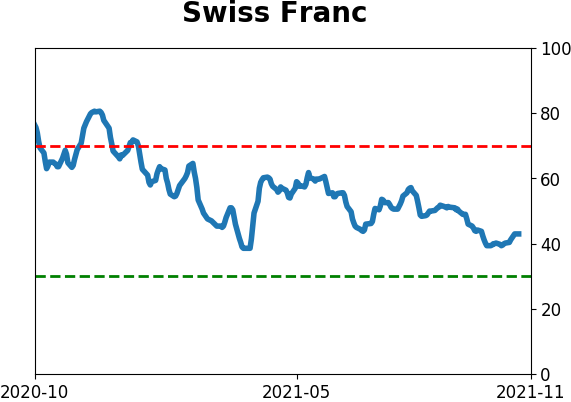

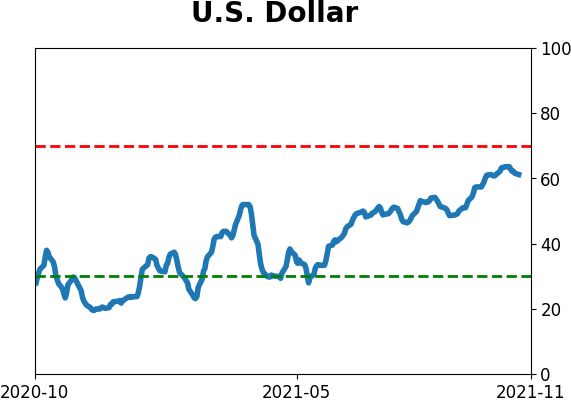

Currency ETF's - 5-Day Moving Average

|

|

|

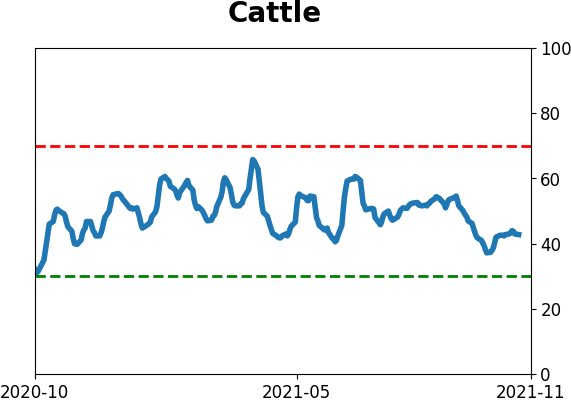

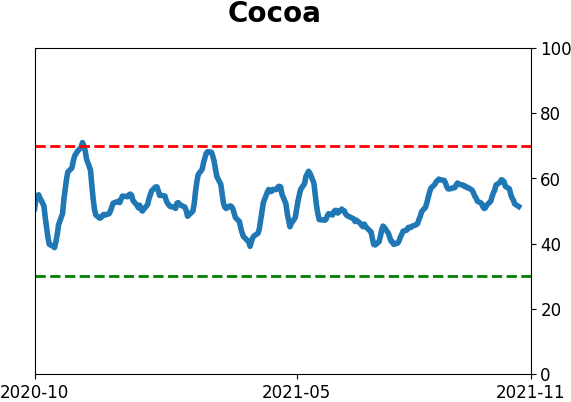

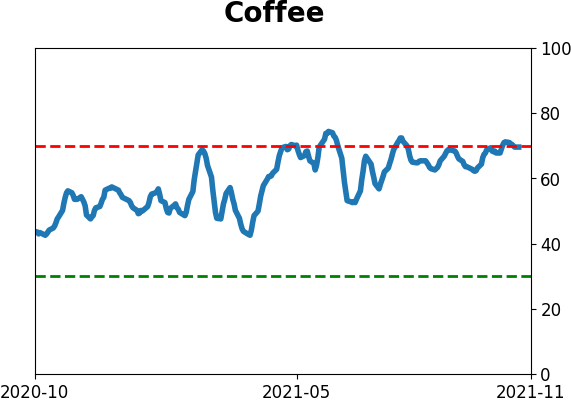

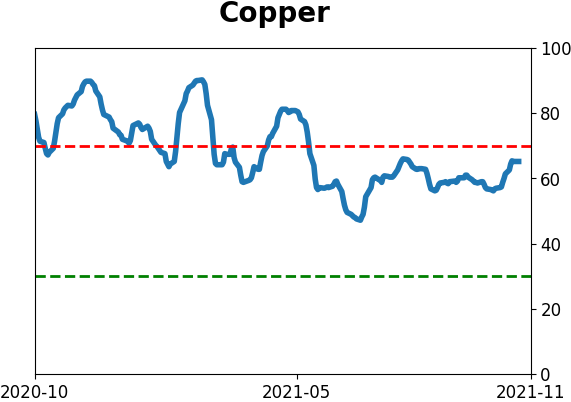

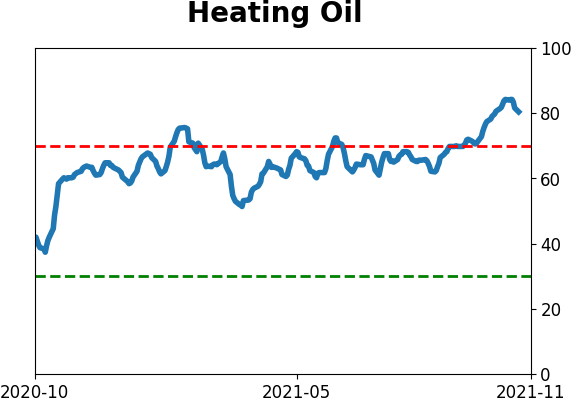

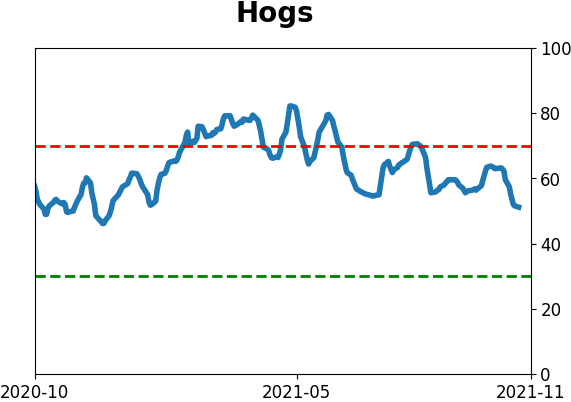

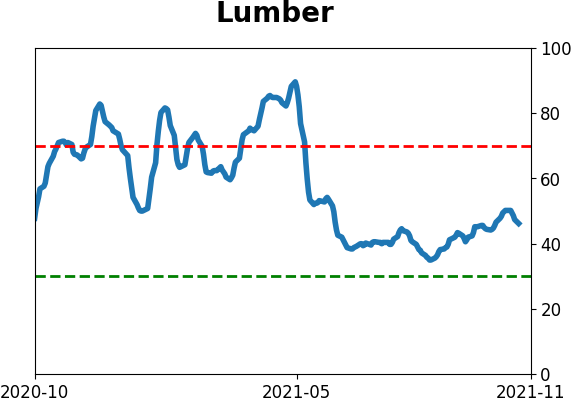

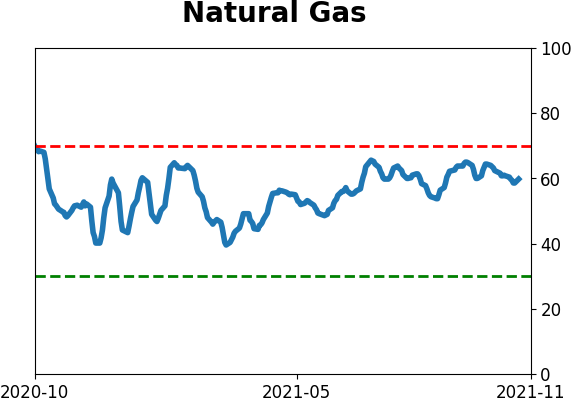

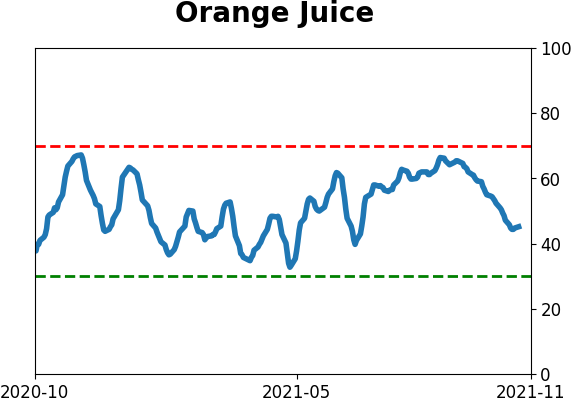

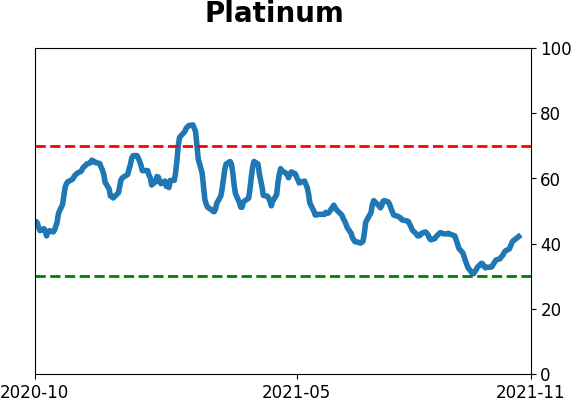

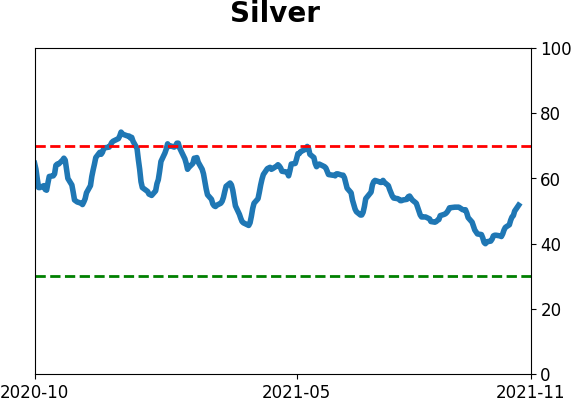

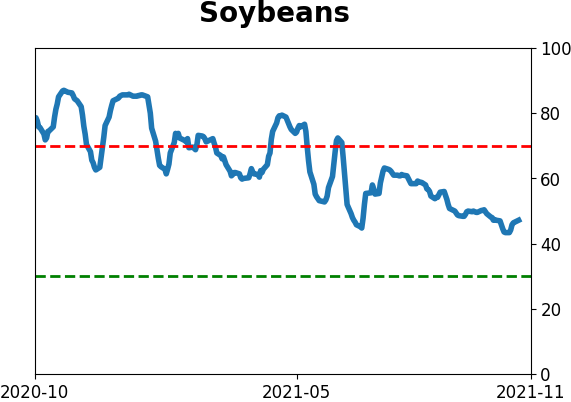

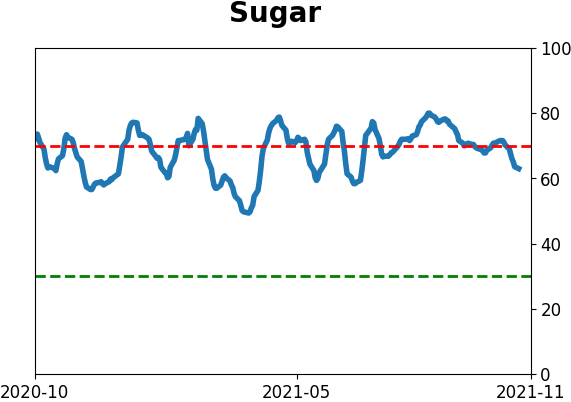

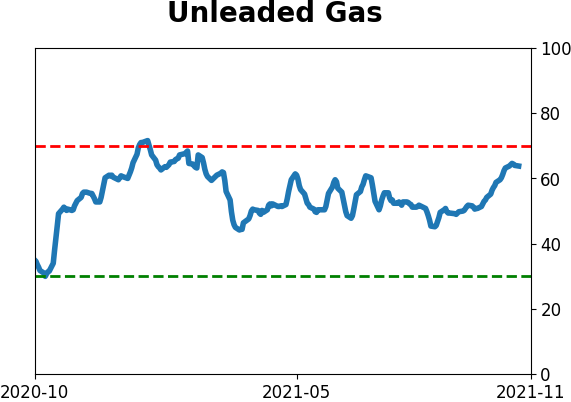

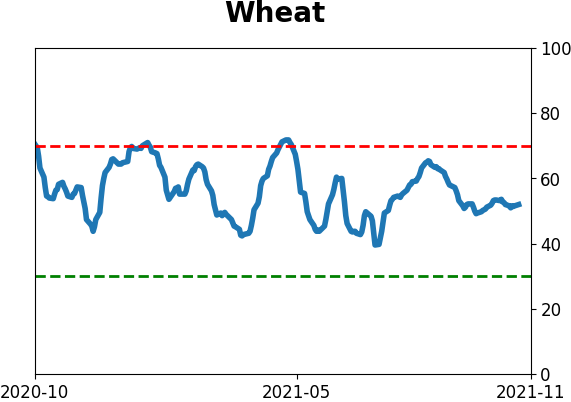

Commodity ETF's - 5-Day Moving Average

|

|