Daily Report : Weekly Wrap for Jul 30 - Lagging Russell and Financials, Commodity Concerns

| View/Print a PDF version of this Report |

Headlines

|

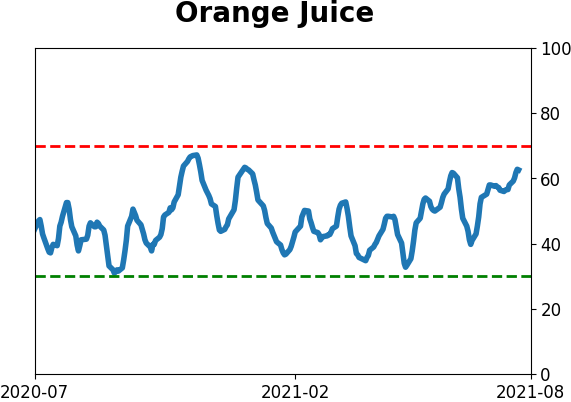

Weekly Wrap for Jul 30 - Lagging Russell and Financials, Commodity Concerns: This week, we saw major indexes hitting records again, but with less participation in small-cap stocks and some sectors like financials. Overseas stocks are struggling relative to the U.S. as well. Some commodities have taken off but sentiment is starting to turn lower. The latest Commitments of Traders data was released, covering positions through Tuesday: The 3-Year Min/Max Screen shows that "smart money" commercial hedgers only established one new multi-year extreme this week, with heavy short exposure to orange juice. The Backtest Engine shows that any time hedgers held 55% or more of open interest net short over the past 20 years, three months later OJ was positive after only 14 out of 47 weeks. In major equity index futures, hedgers are holding about $30 billion in contracts net short. The 10-week average is now below -$30 billion, the lowest in 2 years. They've also been selling 10-year Treasury futures and are close to moving back to a net short position for the first time since December. Bottom Line: See the Outlook & Allocations page for more details on these summaries STOCKS: Hold BONDS: Hold GOLD: Hold |

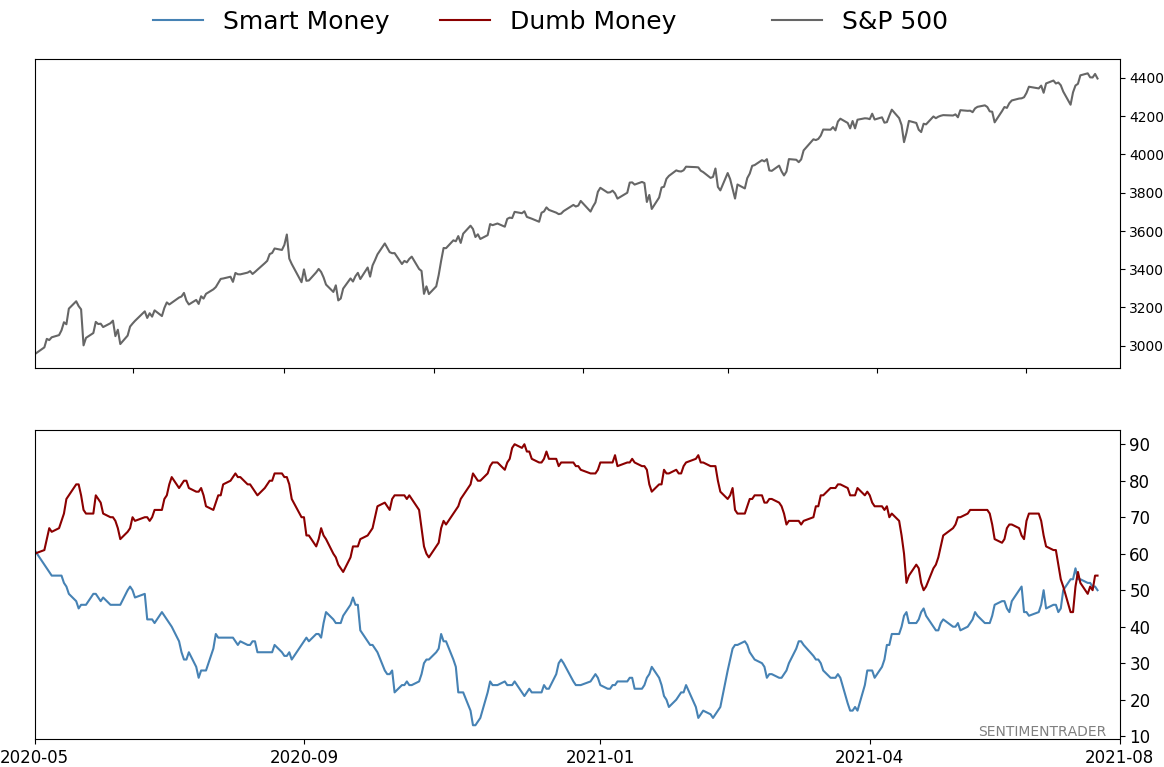

Smart / Dumb Money Confidence

|

|

Risk Levels

|

|

|

Research

Weekly Wrap for Jul 30 - Lagging Russell and Financials, Commodity ConcernsBy Jason GoepfertBOTTOM LINEThis week, we saw major indexes hitting records again, but with less participation in small-cap stocks and some sectors like financials. Overseas stocks are struggling relative to the U.S. as well. Some commodities have taken off but sentiment is starting to turn lower. FORECAST / TIMEFRAME |

The goal of the Weekly Wrap is to summarize our recent research. Some of it includes premium content (underlined links), but we're highlighting the key focus of the research for all. Sometimes there is a lot to digest, with this summary meant to highlight the highest conviction ideas we discussed. Tags will show any symbols and time frames related to the research.

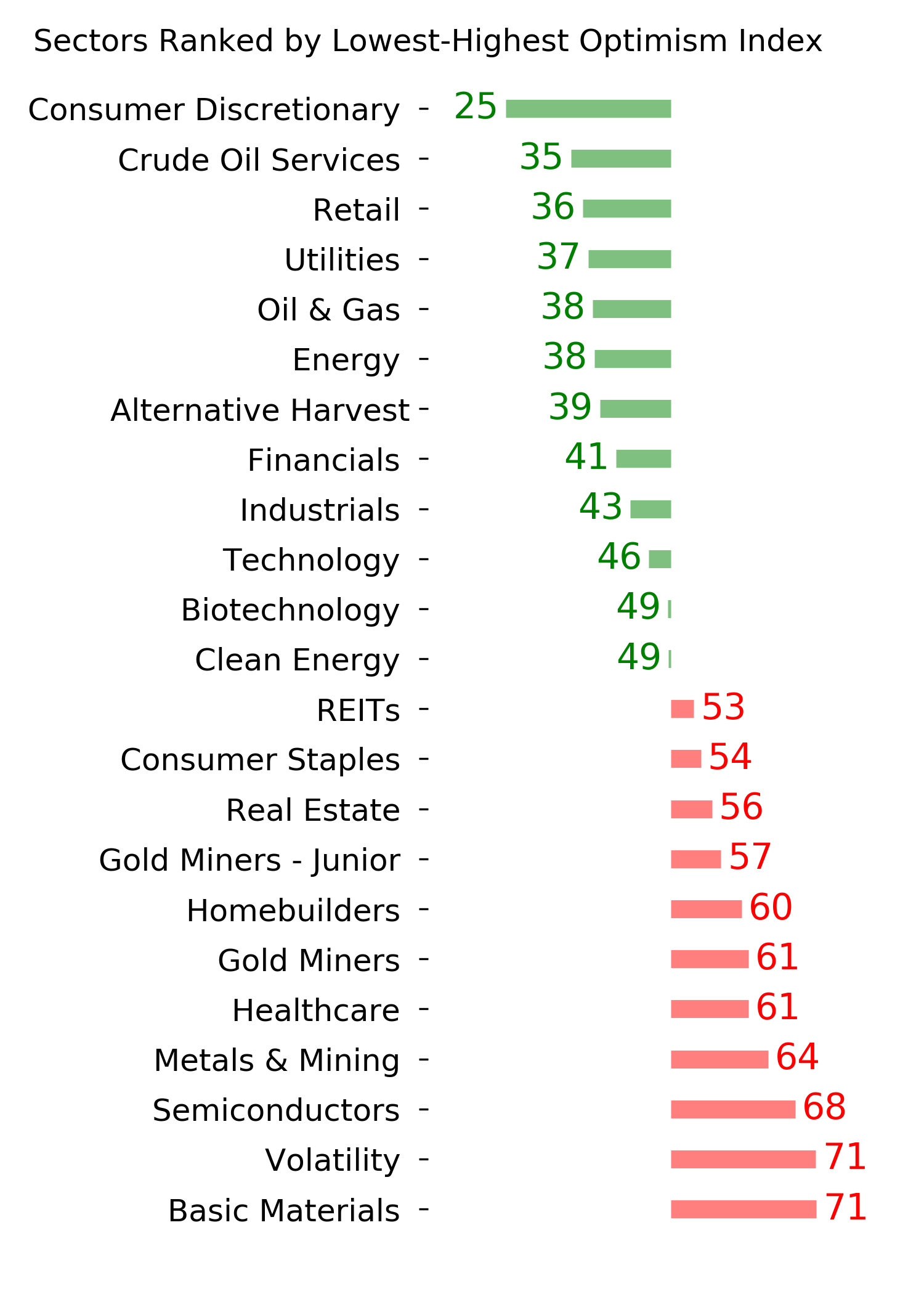

| STOCKS | ||

|  | |

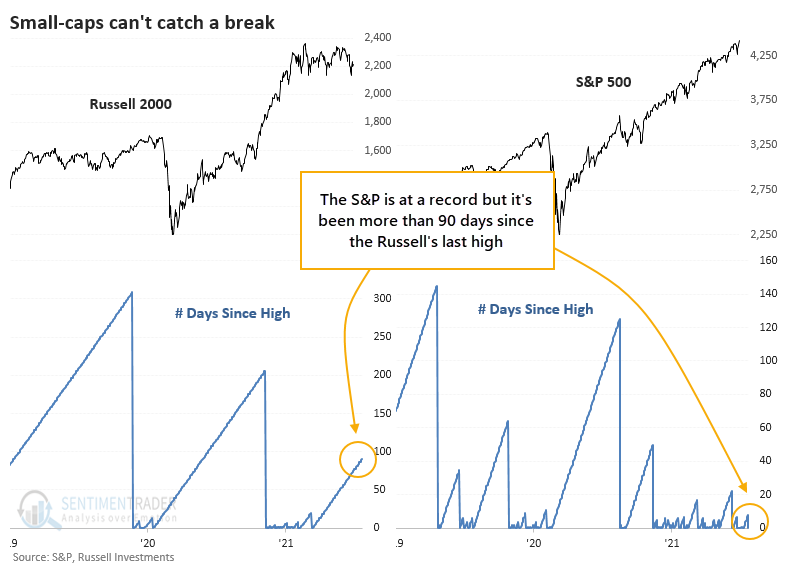

It was a historically persistent and consistent rally for the S&P 500 in the first half of 2021, and things aren't changing much. After a blip on Monday, the index is right back to a record high.

For smaller stocks, it's been much more of a struggle. The Russell 2000 hasn't set a new high for more than 90 days now.

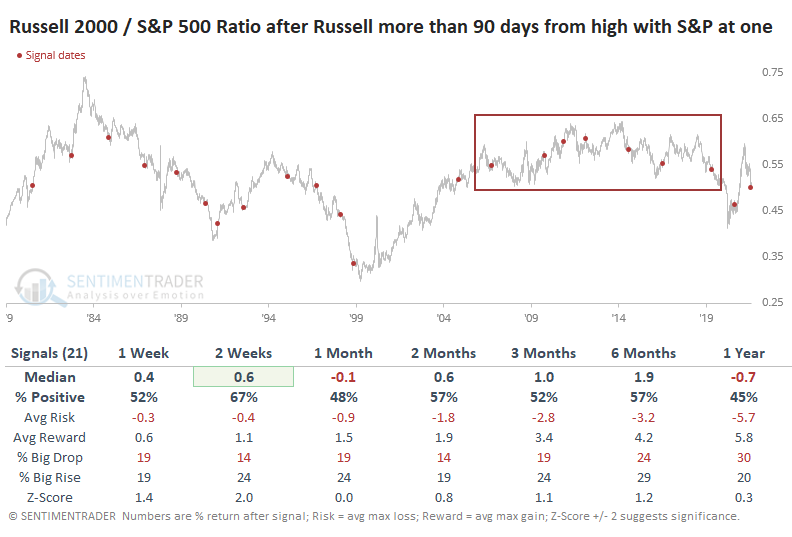

If we focus on the interplay of the two indexes and look for times when the S&P set a new high with the Russell not having done so for at least 90 days, it wasn't a bad sign at all.

Looking at the ratio between them, it was a mixed picture. Over the medium- to long-term, the Russell underperformed over a couple of time frames and outperformed slightly after a few others. Since the 2008 financial crisis, there was more of a tendency to underperform over the medium-term.

FINANCIALS STRUGGLING, TOO

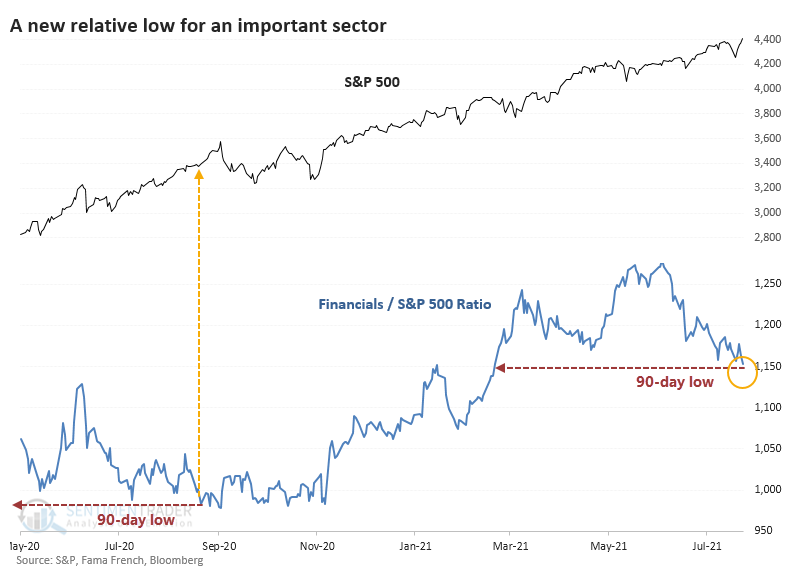

Small-Cap stocks aren't the only ones struggling to keep up with the S&P 500's torrid pace.

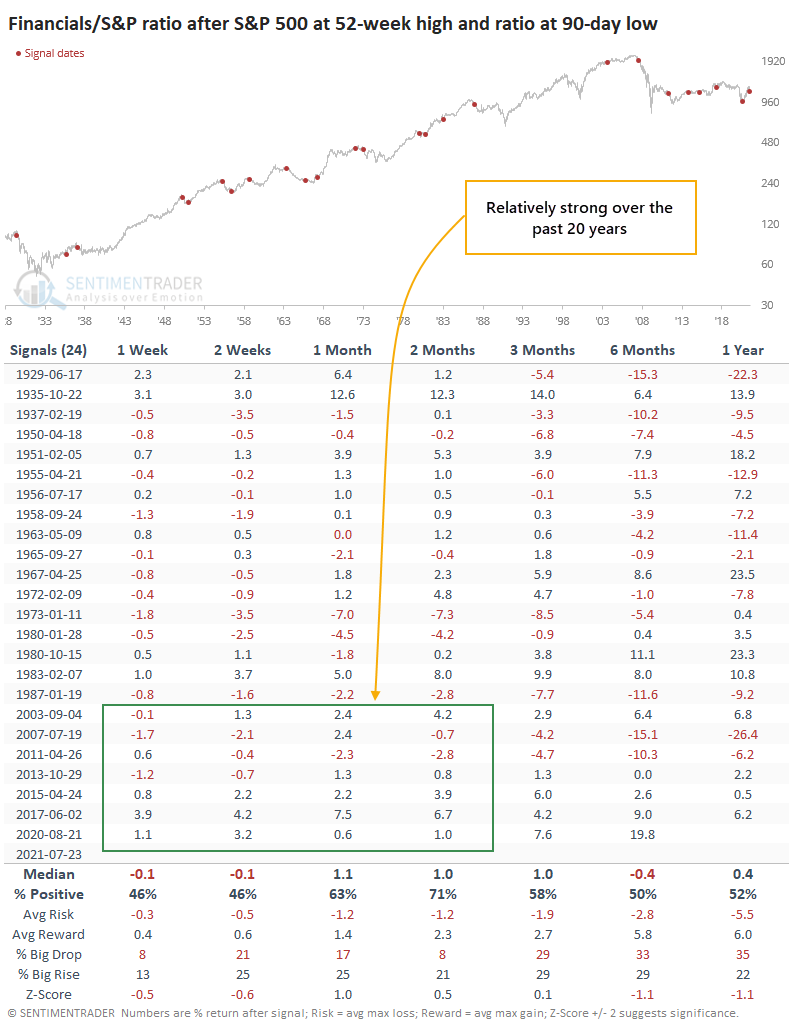

Financial stocks have been lagging, too, going more than 30 days without setting a fresh high. Even more notably, the ratio of Financials to the S&P 500 just sagged to its lowest point in more than 90 days. The last time the two diverged to this wide of a degree was last August.

Since the Great Financial Crisis in 2007-08, this kind of relative divergence has preceded weakness in the S&P each time over the next 2-4 weeks.

Relative to one another, Financials mostly outperformed after the very short-term. During the past 20 years, Financials outpaced the S&P during the next month after 6 out of 7 signals. The medium-term time frame of 1-3 months saw the biggest outperformance.

Ideally, bulls would see sectors, industries, and individual stocks mostly trading in line with major indexes like the S&P 500. That has been shaky in recent weeks, and that's a warning, though the overwhelming buying pressure mid-week last week alleviates some of that concern.

SUMMER SWOON

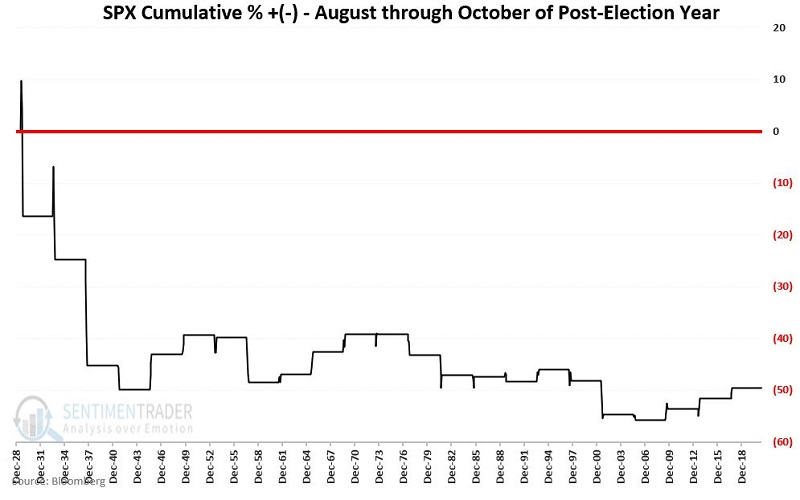

With August looming, it would seem to be a good time to highlight what Jay refers to as the Post-Election Year "Dead Zone." You've heard of the "Dog Days of Summer?" Well, welcome to them.

The chart below displays the cumulative % price change for the S&P 500 Index if held long ONLY during August, September, and October of each post-presidential election year starting in 1929.

The net result is a cumulative decline of -49.5%. The bulk of this decline took place in 1929, 1933, 1937, and 1941 - a period which some might reasonably argue was far different from the environment today or even in the post-WWII era.

But before dismissing the "Dead Zone" theory, also note that since 1941there have been 19 post-election years, and the cumulative gain for the S&P 500 Index during Aug-Oct of these 19 years is +0.73%.

It doesn't get much more "dead" than that.

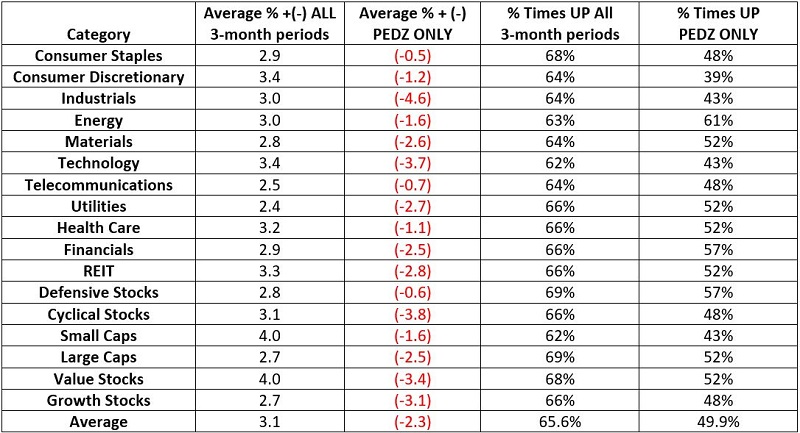

Jay then took a closer look at market performance during this period compared to typical market performance but specifically in regard to sectors and factors instead of the broader market.

For the sake of brevity, we will refer to this 3-month period as "PEDZ" (Post-Election Dead Zone).

The table below displays:

- The average 3-month % gain or loss across all rolling 3-month periods starting in 1929

- The average 3-month % gain or loss across all "Post-Election August through October" periods since 1929

- The % times a 3-month gain was shown across all rolling 3-month periods starting in 1929

- The % times a 3-month gain was shown across all "Post-Election August through October" periods since 1929

It shows that during these summer swoons, higher-beta areas like Discretionary and Growth stocks tended to have a lower win rate and average return than others.

Given that the stock market has had little more than a minor pullback so far in 2021, investors should recognize that if trouble is going to come to the market this year, history suggests that the impending three months is as likely a time as any.

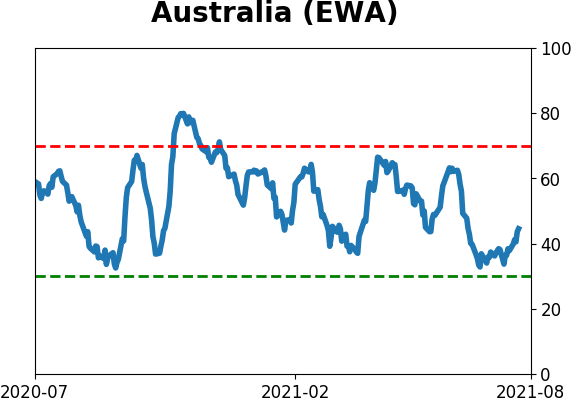

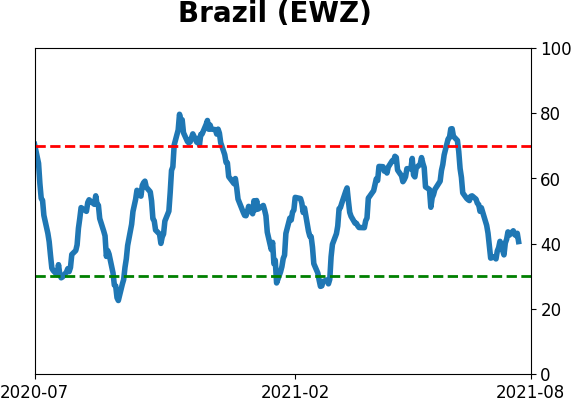

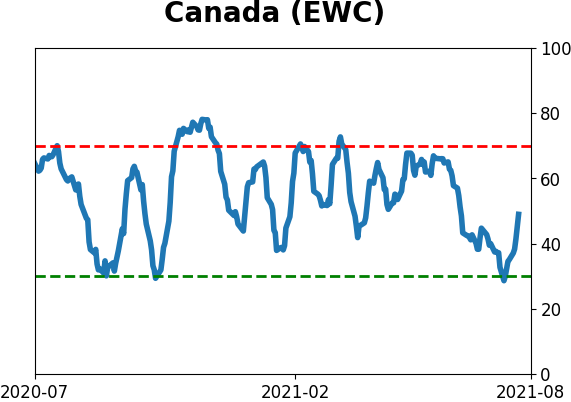

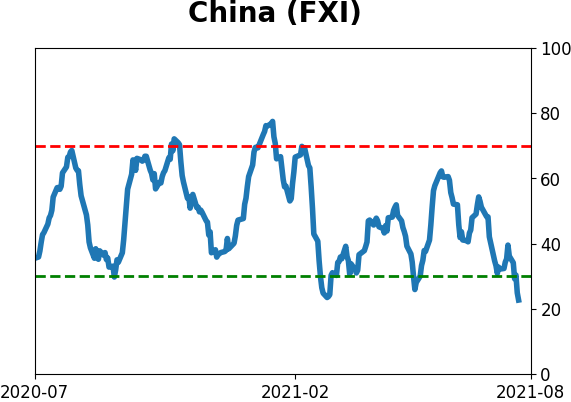

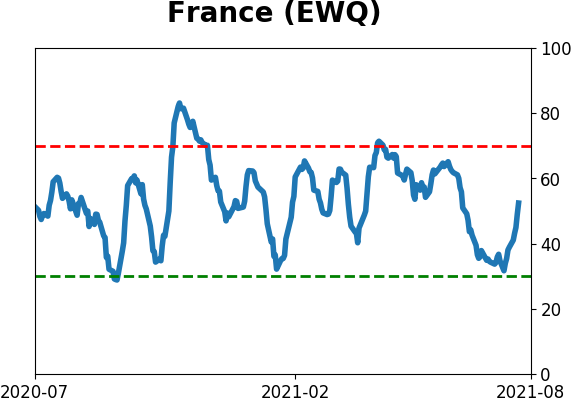

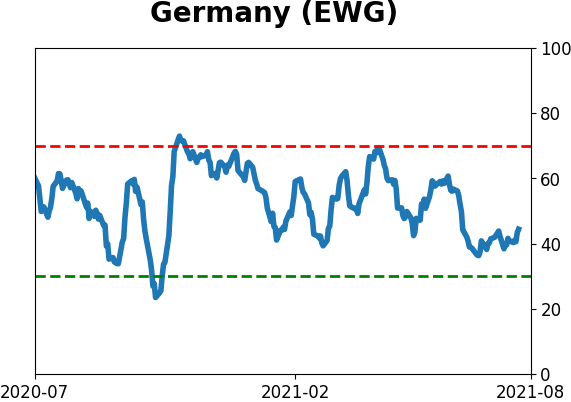

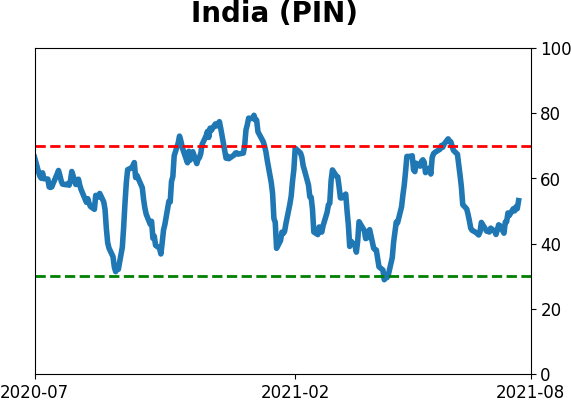

STOCKS AND SECTORS - OVERSEAS INDEXES

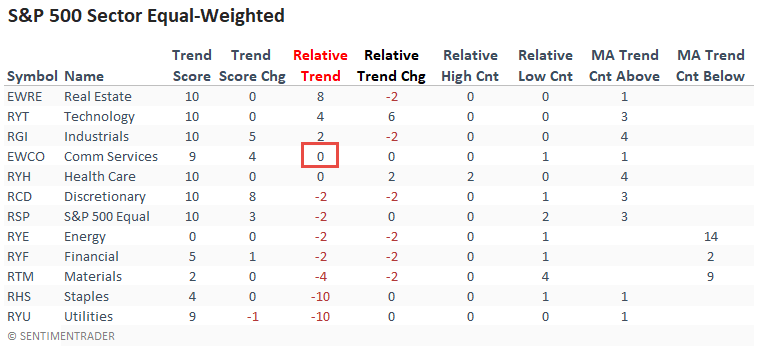

Dean updated his absolute and relative trend following indicators for domestic and international ETFs.

The equal-weighted communication services sector shows a relative trend score of zero. In contrast, the cap-weighted version increased to a perfect ten last week. Once again, we see how mega-cap issues are dominating the cap-weighted benchmarks and driving overall market performance.

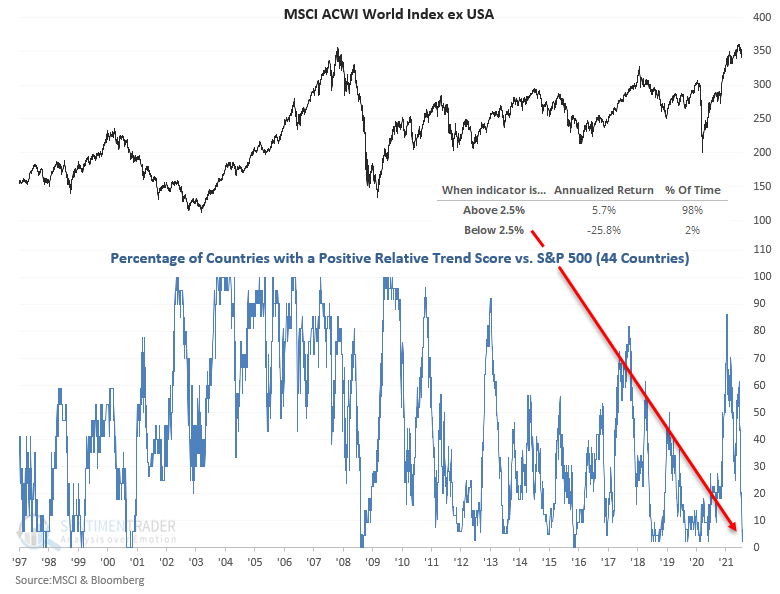

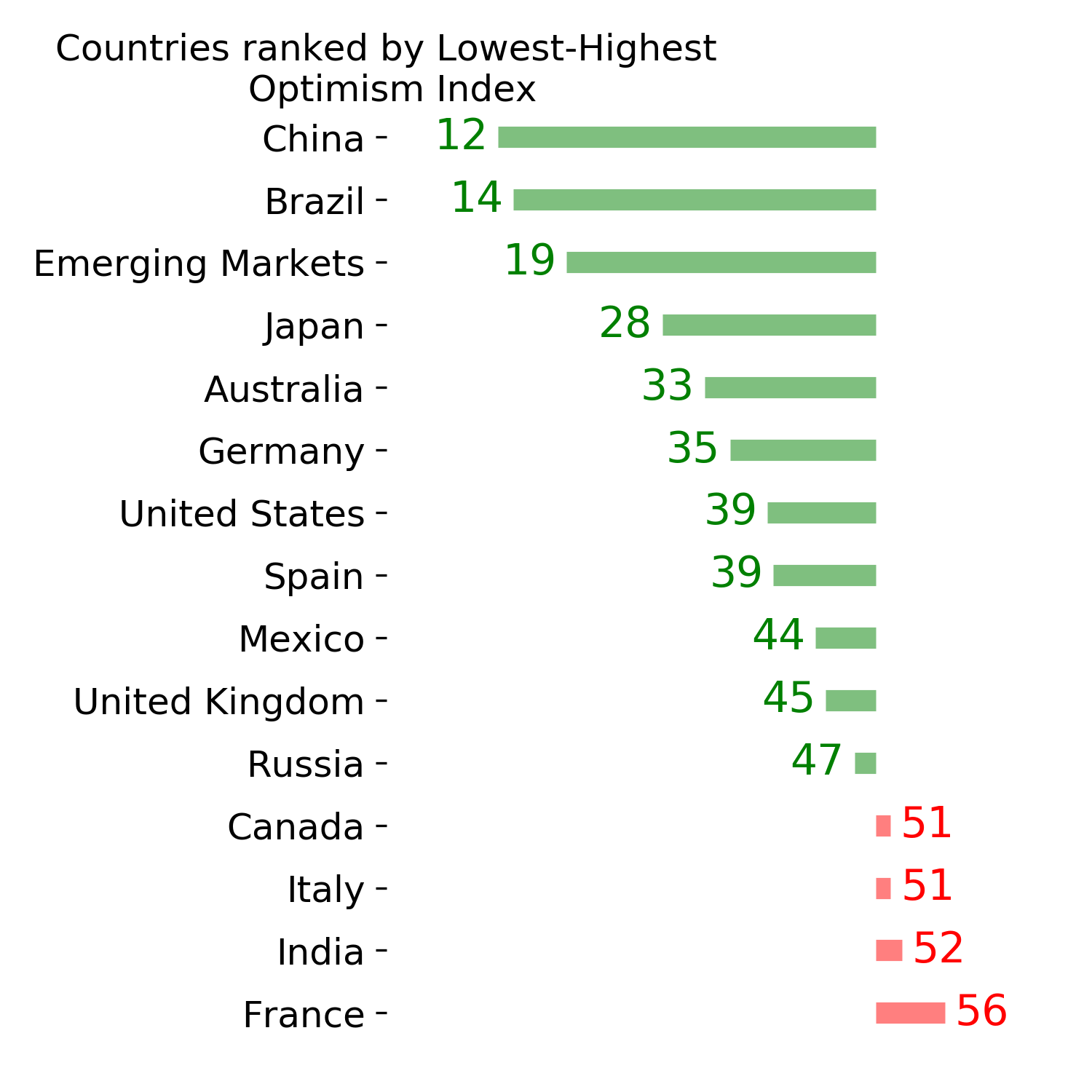

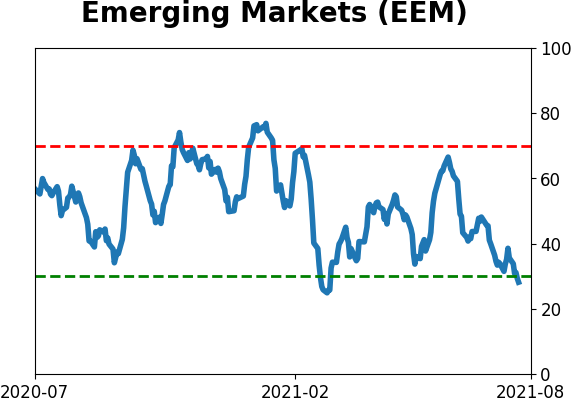

Chinese companies continue to drive the underperformance in the Emerging Markets Internet and Ecommerce ETF. Due in part to that, the percentage of countries with a positive relative trend score versus the S&P 500 continues to worsen. It has now fallen to the lowest level since May 2020.

The outlook for the MSCI ACWI World Index ex USA is concerning.

STOCKS AND SECTORS - EMERGING MARKETS

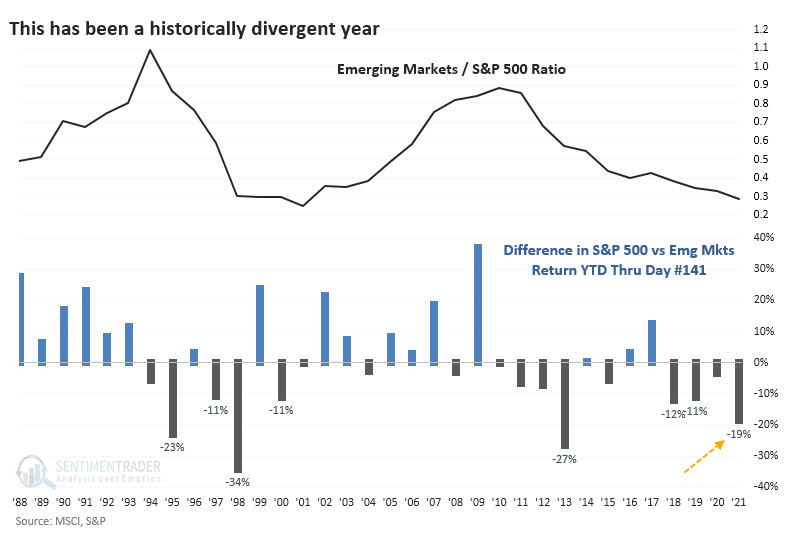

Even while the S&P 500 has set record after record, stumbles in some Chinese stocks have helped to drag down emerging market indexes. The MSCI Emerging Markets Index has now turned negative for the year.

Through the end of July (or close to it, anyway), this is the 4th-widest difference in returns between the S&P and emerging markets.

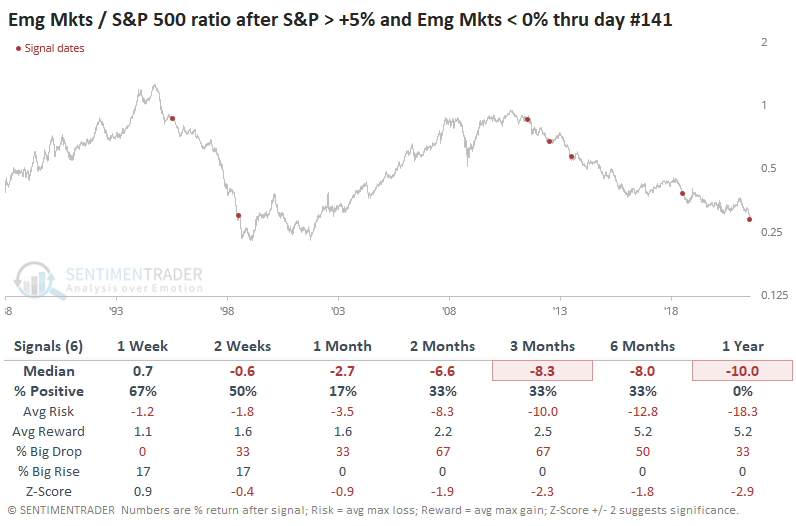

Across all time frames, the three precedents underperformed random returns for the ratio between the two markets with a risk / reward that was heavily skewed to the "risk" side.

It's really had to put much weight on a sample size of three, so if we expand the sample by looking at 5% or larger YTD gains in the S&P while emerging markets showed losses, we do generate more signals, but the sample is still tiny. And the conclusion was the same.

Pessimism is building in emerging markets and Chinese stocks in particular. It may soon reach capitulative levels, which may help turn the current trend favoring the U.S. Until we see more signs of that, however, this momentum and seasonal bias toward the U.S. has solid historical backing.

| BONDS | ||

| ||

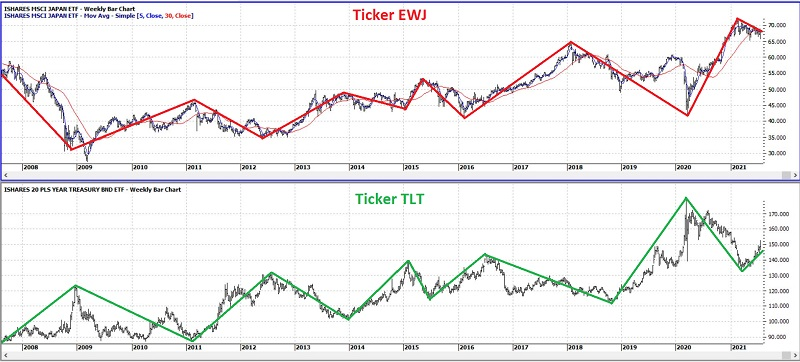

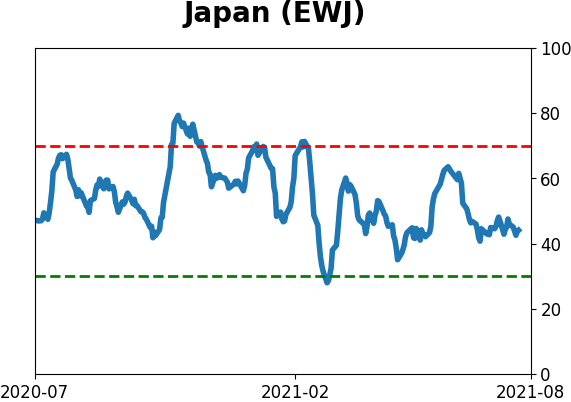

In the financial markets, certain relationships hide in plain sight. For instance, Jay pointed out that there is a noticeable inverse relationship between U.S. treasury securities and the Japanese stock market. Most investors are unaware of this relationship because it simply "does not compute" for many individuals.

In the charts below (courtesy AIQ TradingExpert):

- The top clip displays a weekly chart of EWJ (iShares MSCI Japan ETF) - the iShares ETF that tracks a broad index of Japanese stocks - with a 5-week and 30-week moving average drawn

- The bottom clip displays a weekly chart of ticker TLT (iShares 20+ Year Treasury Bond ETF) - the iShares ETF that tracks the long-term U.S. Treasury bond

Note that - speaking in something less than highly technical terms - when one "zigs," the other tends to "zag."

For testing purposes:

- If EWJ 5-week MA < EWJ 30-week MA = BULLISH for US treasuries

- If EWJ 5-week MA > EWJ 30-week MA = BEARISH for US treasuries

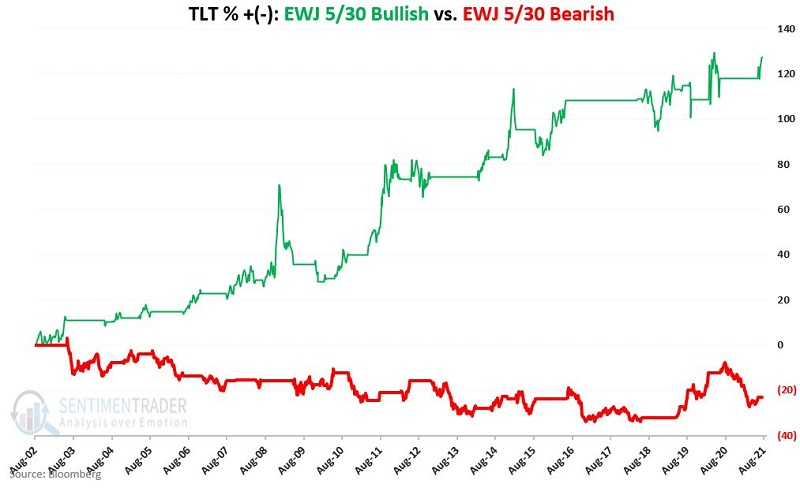

In the chart below, the green line displays the hypothetical cumulative percentage price gain or loss achieved by holding a long position in ticker TLT when the EWJ indicator is BULLISH (for U.S. bonds). The red line displays it when the EWJ indicator is BEARISH (for U.S. bonds)

A long position held in TLT (with no slippage, commissions, or dividends) held ONLY when the EWJ 5-week average was below the EWJ 30-week average gained +128% since inception. That contrasts with a loss of 23% when the EWJ 5-week average was above the EWJ 30-week average.

Bond bulls should watch EWJ and start to worry more if its long-term trend turns up.

| COMMODITIES | ||

|  | |

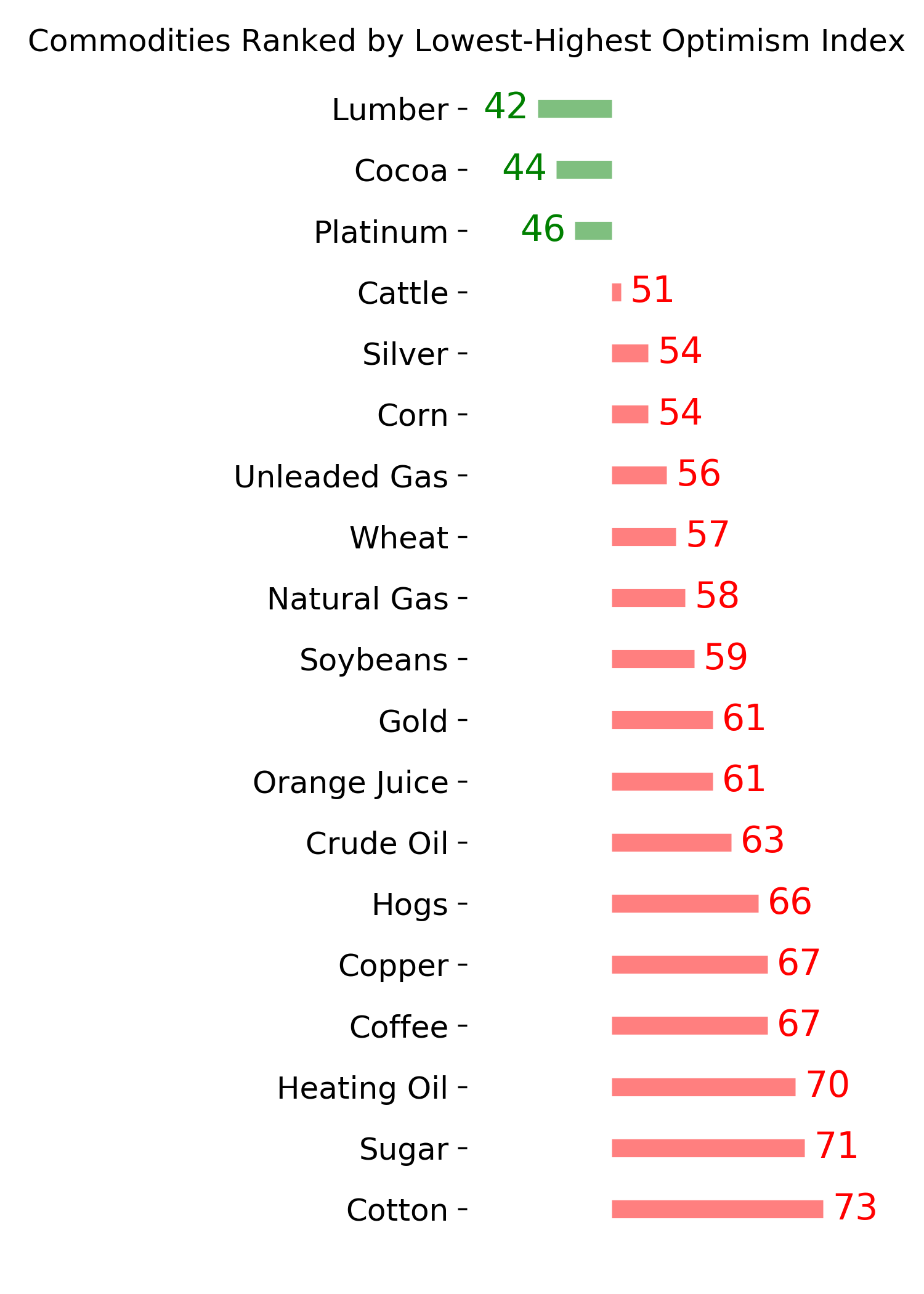

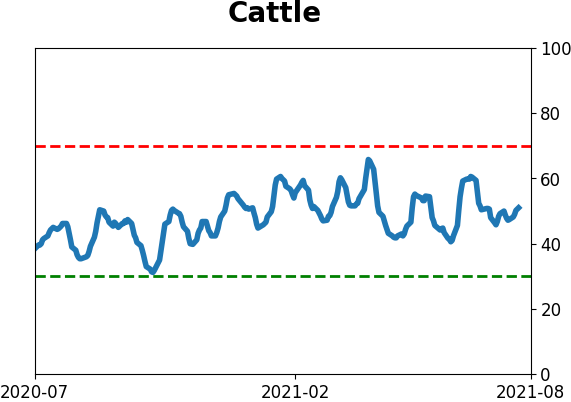

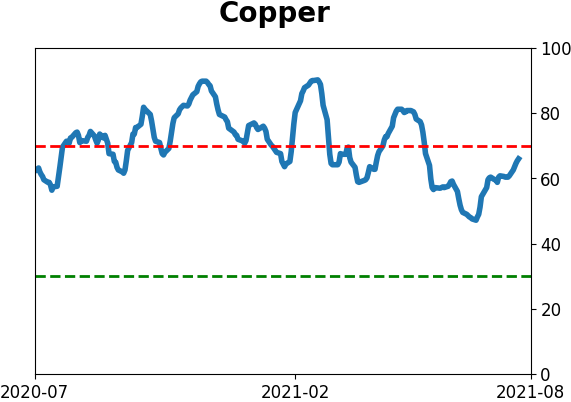

A lot of people consider copper to be one of the most important commodities in the world. Several factors appear to be coming together soon, affecting the future price direction for this key commodity. Jay took a closer look.

Copper is flirting with its 70-day exponential moving average. There is nothing magic about a 70-day EMA; that said, it should be noted that since 1959, copper has gained +3,678% when above its 70-day EMA and lost 61.2% when below its 70-day EMA.

The chart below displays the Annual Seasonal Trend for copper.

All this chart tells us is that the second half of the year tends to be much more difficult for copper and that any new rally from current levels will have to come into a stiff seasonal headwind.

In addition, the 50-day average of our Optimism Index for Copper has dropped from above to below 65%. The table below displays the summary of results following previous signals. Six months out, the average and median results are negative, and the median 1-year result has been a double-digit loss.

Price is always the most important factor. As long as copper continues to trend higher, there is no reason to "fight the trend." However, if price, seasonality, and sentiment all line up on the wrong side, traders might consider steering clear of copper or playing it from the short side.

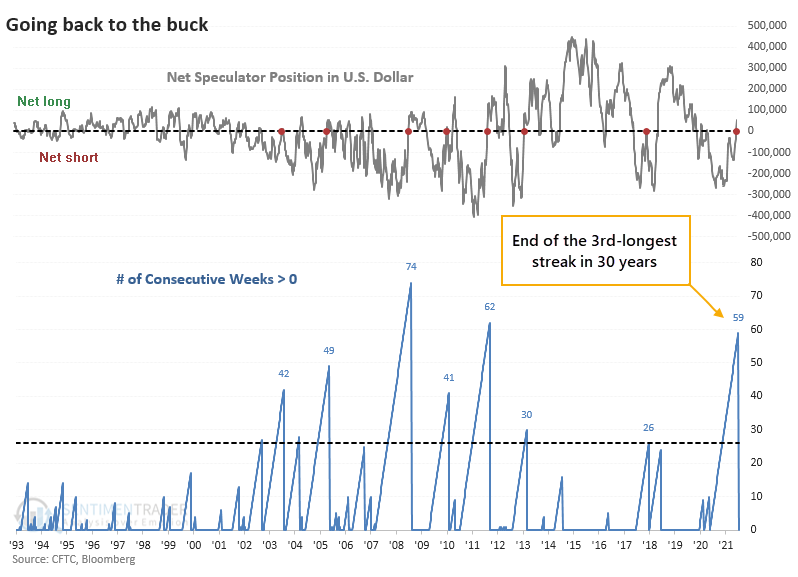

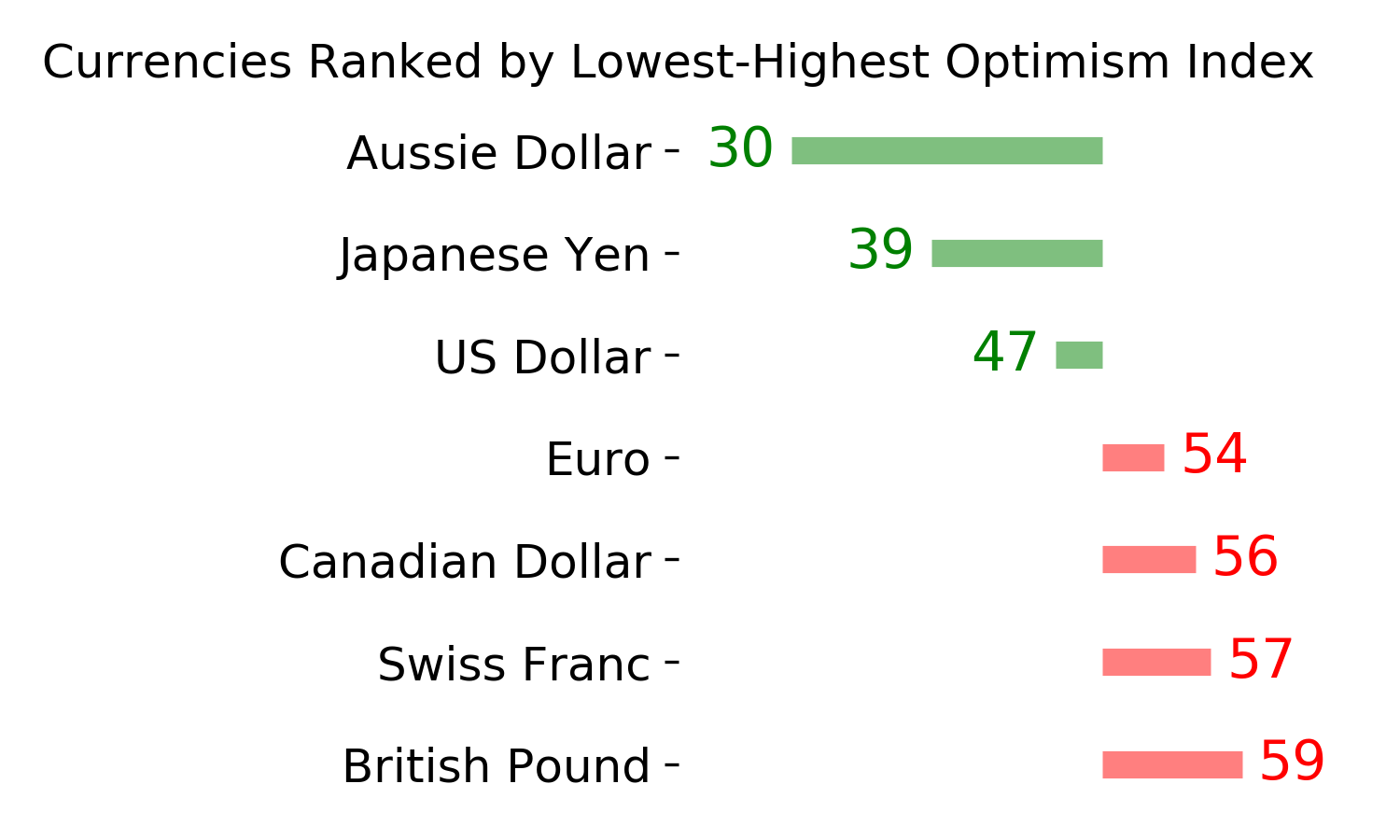

SPECULATORS TURN POSITIVE ON THE DOLLAR

The U.S. is the place to be. Might as well bet on the dollar, too.

Bloomberg notes that speculators in the dollar versus its major peers have flipped to a net long position for the first time in months, meaning they're shorting other currencies against the buck. This just ended the 3rd-longest streak of shorting the dollar in 30 years.

For 59 consecutive weeks, well over a year, speculators had been short the dollar. That's just below the streak of 62 weeks that ended in September 2011, which happened to mark the end of a long period of a declining dollar.

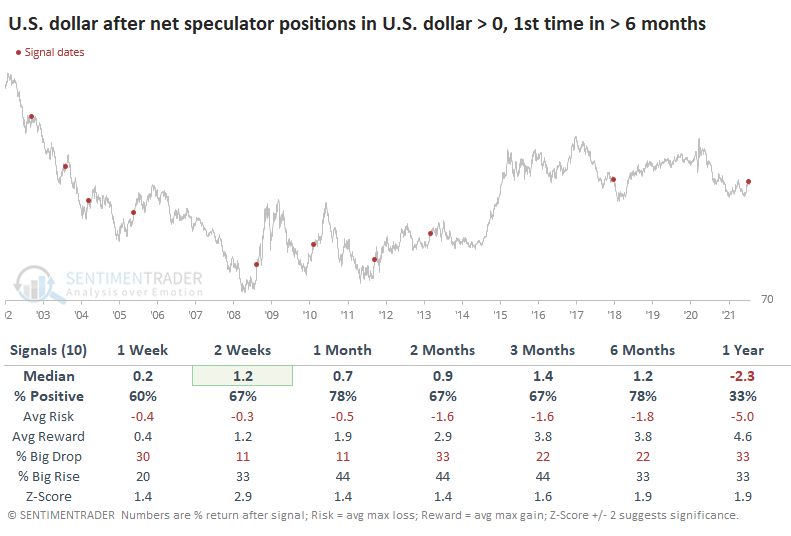

For the dollar, it was a good sign when speculators decided to start betting on the currency again after a long period of shorting it. All of the signals triggered in the past 20 years.

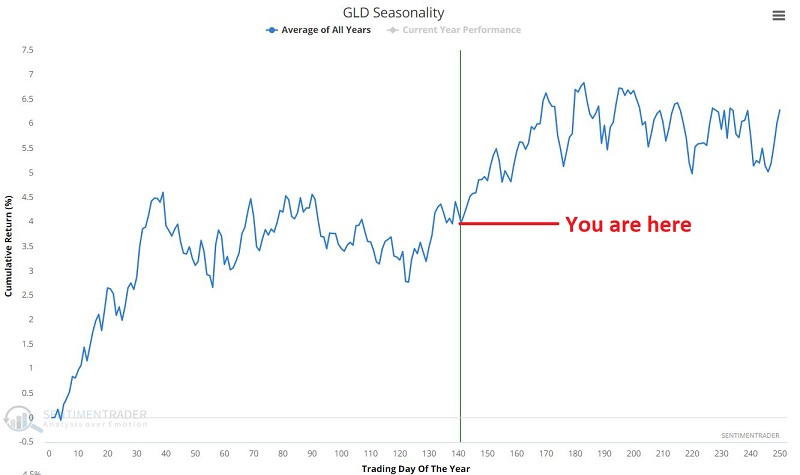

GOLD TAILWIND

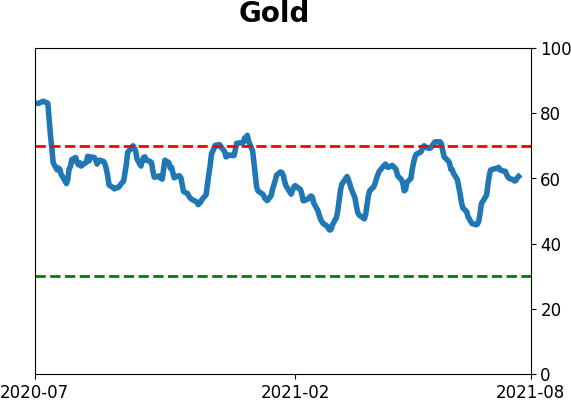

Even though the dollar tended to rally after speculators turned positive, it wasn't a terrible sign for gold due to many signals triggering during the mid-2000s. Jay looked at another potential positive, with gold's seasonal trend.

One can objectively argue that the price of gold is in a downtrend at this exact moment in time. The "Good News" should probably be labeled (more accurately) as "Potential Good News." In the chart below, we see the Annual Seasonal Trend for ticker GLD (VanEck Vectors Gold Miners ETF) - and we can note that we are entering a typically favorable period.

The price of gold if HELD ONLY from the close on Trading Day of the Year #141 through the close on Trading Day of the Year #153 since 1975 was UP 30 times and DOWN 15 times.

This sets up a scenario for a potential options trade.

In this scenario, we are not necessarily looking to bet on GLD going up. Instead, we are betting on GLD to do something other than decline -2.7% or more in the next several weeks. To make this play, we will use a strategy known as a "bull put spread," which involves:

- Selling a put option at a higher strike price (typically at a strike price below the current price of the underlying security)

- Buy another put option at a lower strike price

We can see the expected P/L as of a given date and price for GLD of this potential trade in the chart below that (courtesy of Optionsanalysis.com).

As long as GLD does not drop from $168.46 to $163.83 or lower in the next 10 days, we stand to earn 9.3% on capital risked. Mathematically there is better than an 80% probability of profit.

The MOST important thing to note about our example trade is that the maximum risk far exceeds the maximum profit. This is fairly typical for this type of trade. However, what it means is that this is NOT a "set it and forget it" kind of trade. In other words, a trader who enters into this position MUST be prepared to act if and when the time comes to cut a loss.

KEEPING AN EYE ON COFFEE

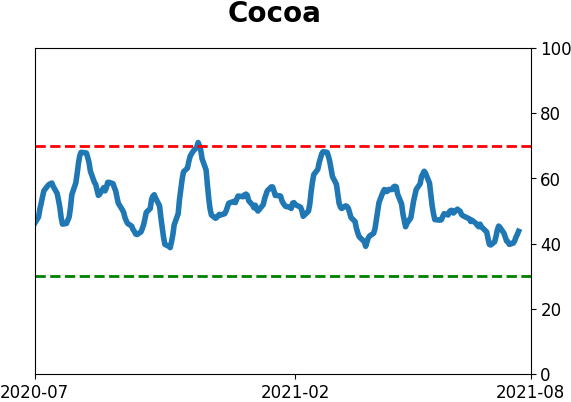

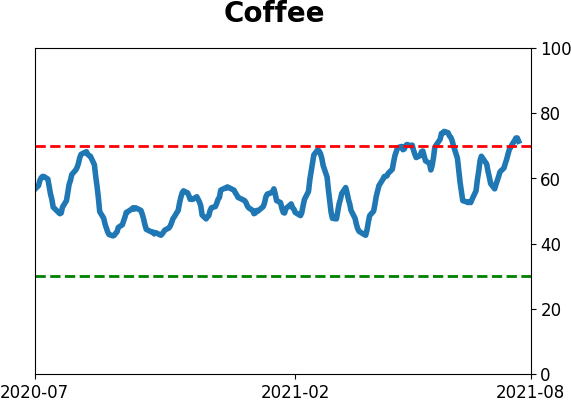

The last 12 months have witnessed a strong resurgence in the price of commodities. Jay noted that the most recent to "blast off" is coffee.

Even as prices go parabolic, he identified days when the 20-day average for Coffee's Optimism Index dropped from above to below 60. This looks for sentiment to reach a high level over a period of time AND for a reversal in that sentiment. The goal is to identify when "the thrill is gone" and the rally may be over, rather than trying to pick the top.

The chart below displays the signal days, and the table below displays the summary results.

After these signals, every time frame shows a Win Rate below 50%, with 3 and 6 months winning % of 37%, and every time frame shows negative Median Returns.

Coffee has achieved "take off." Once this happens, coffee is capable of running up a very long way, and a great deal of money can be made by those who have the fortitude to withstand the ride (and who are willing to cut a loss if things go the wrong way). Likewise, selling short into a sharp advance is often the easiest way to lose a lot of money quickly.

That said, both sentiment and seasonality remind us that if coffee is going to run this time around, it will likely only run so high and for so long before gravity takes hold.

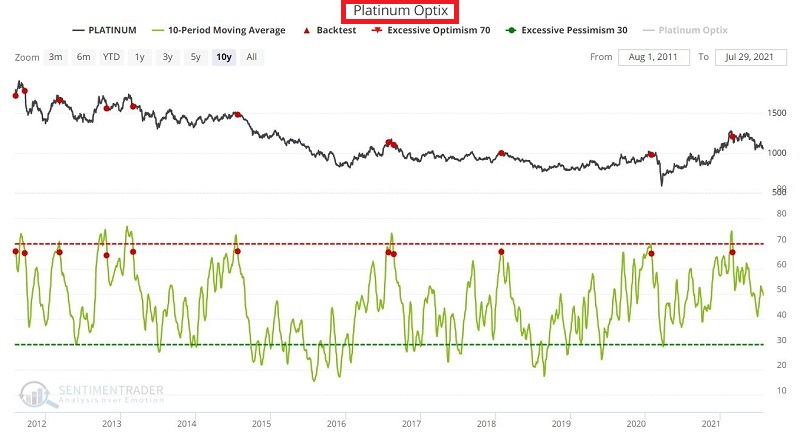

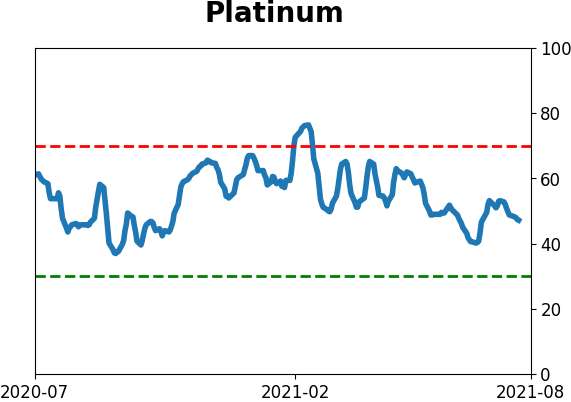

AN EYE ON PLATINUM, TOO

Similar to coffee, Jay noted that it should pay to keep an eye on platinum, too. The chart below displays the Annual Seasonal Chart, showing that platinum is entering a seasonally weak time of year.

The problem is not so much that platinum always declines during this period. The problem is that when it does decline, it tends to go down a lot.

In addition, during the past 10 years (not so much in prior years), platinum price performance has been weak following a break by the 20-day average of its Optimism Index from above to below 67%.

All 11 signals showed a decline in platinum prices over the next 2-6 months.

Active Studies

|

|

|

|

|

|

Indicators at Extremes

|

|

|

Portfolio

|

|

|

|

Phase Table

|

|

|

Ranks

|

|

|

|

|

|

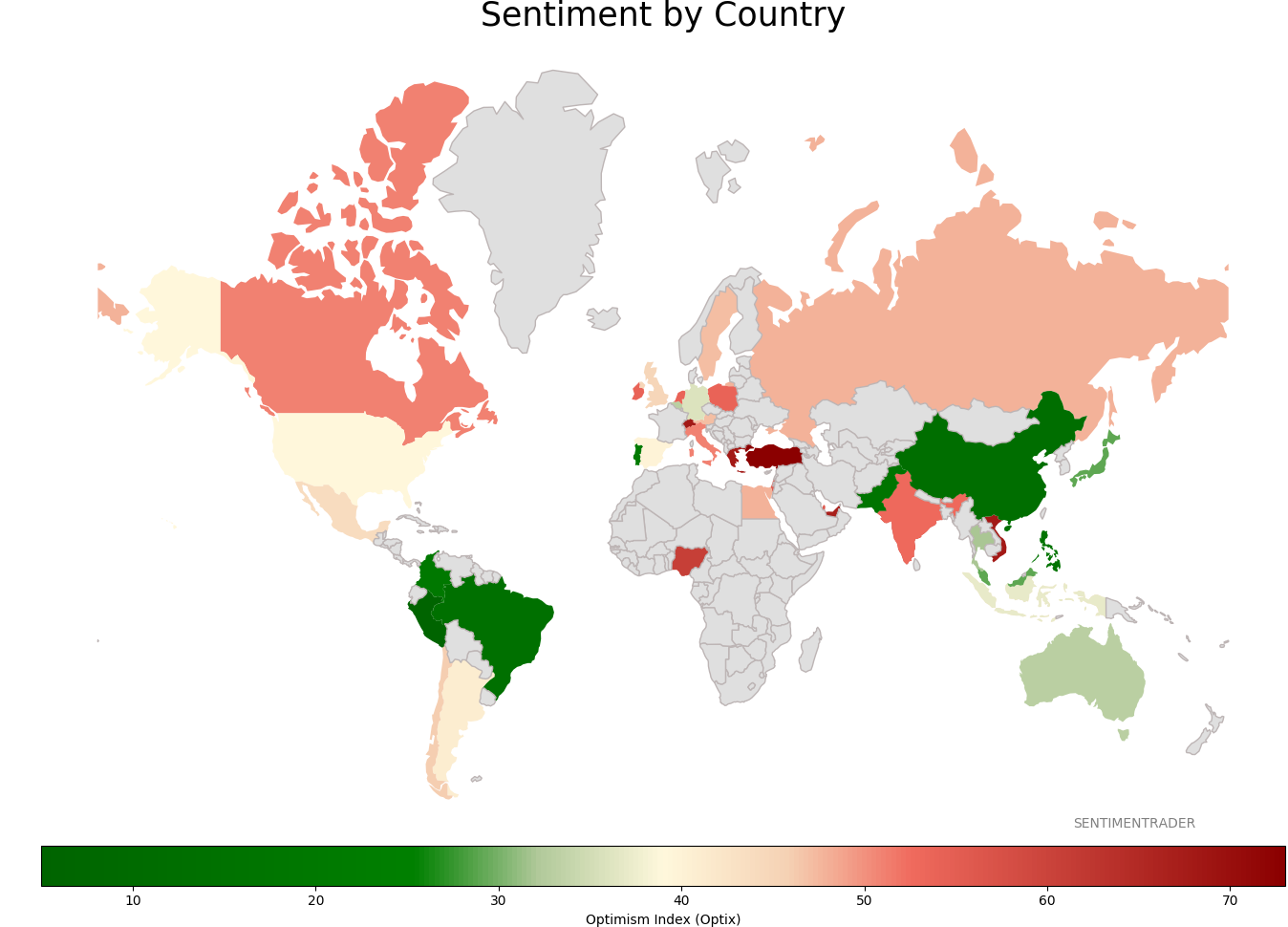

Sentiment Around The World

|

|

|

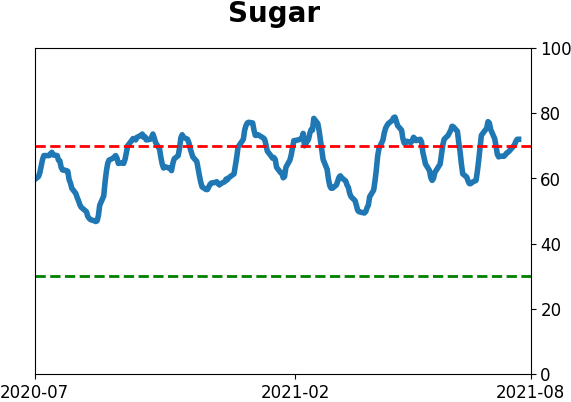

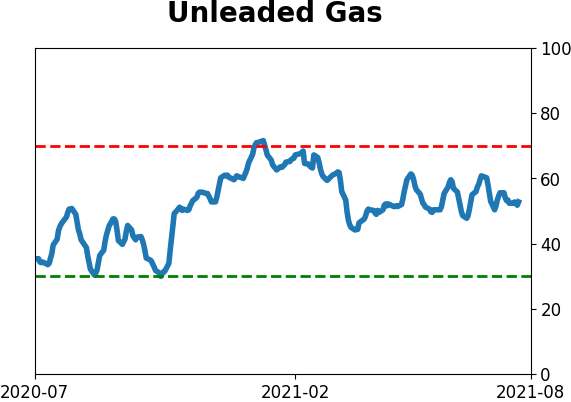

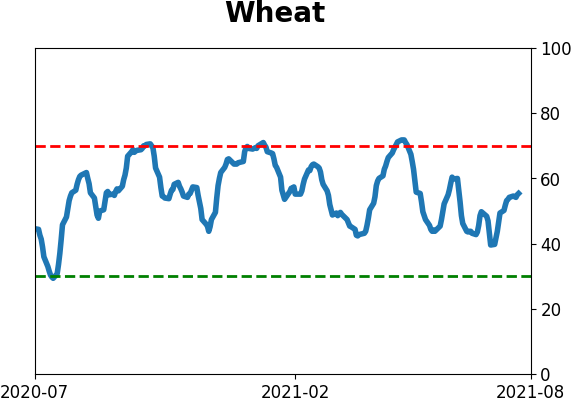

Optimism Index Thumbnails

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|