Headlines

|

|

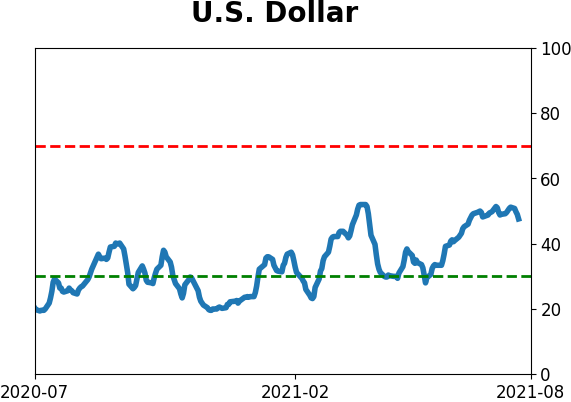

For the First Time in a Year, Speculators Bet on the Dollar:

For the first time in over a year, speculators in the U.S. dollar are betting that it will rally. Speculators are shorting other currency futures relative to the dollar, ending one of the longest streaks in 30 years of doing the opposite.

Bottom Line:

See the Outlook & Allocations page for more details on these summaries STOCKS: Hold

The speculative frenzy in February is wrung out. Internal dynamics have mostly held up, with some exceptions. Many of our studies still show a mixed to poor short-term view, with medium- and long-term ones turning more positive. BONDS: Hold

Various parts of the market got hit in March, with the lowest Bond Optimism Index we usually see during healthy environments. After a shaky couple of weeks, the broad bond market has modestly recovered. Not a big edge here either way. GOLD: Hold

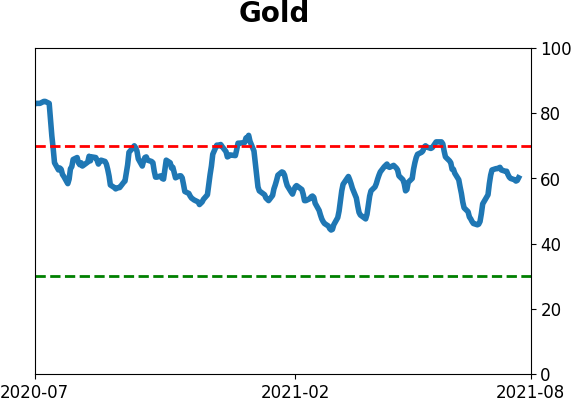

Gold and miners have done very well, recovering above long-term trend lines. The issue is that both have tended to perform poorly after similar situations - will have to wait and see how it plays out.

|

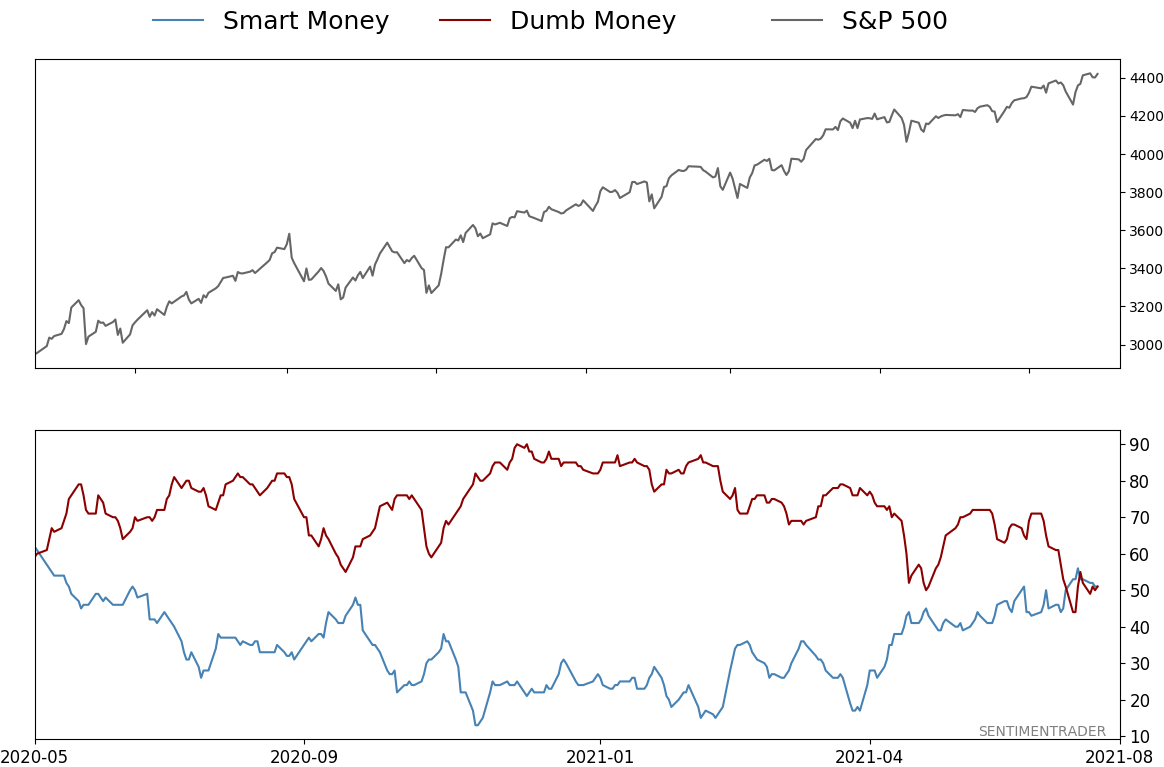

Smart / Dumb Money Confidence

|

Smart Money Confidence: 51%

Dumb Money Confidence: 51%

|

|

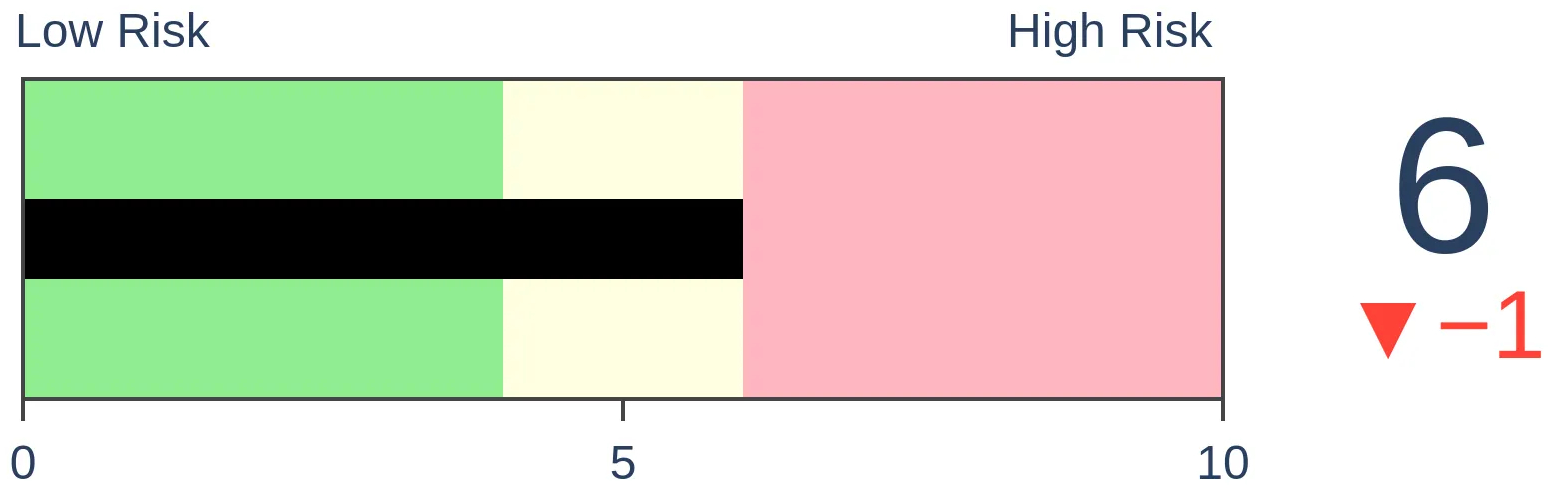

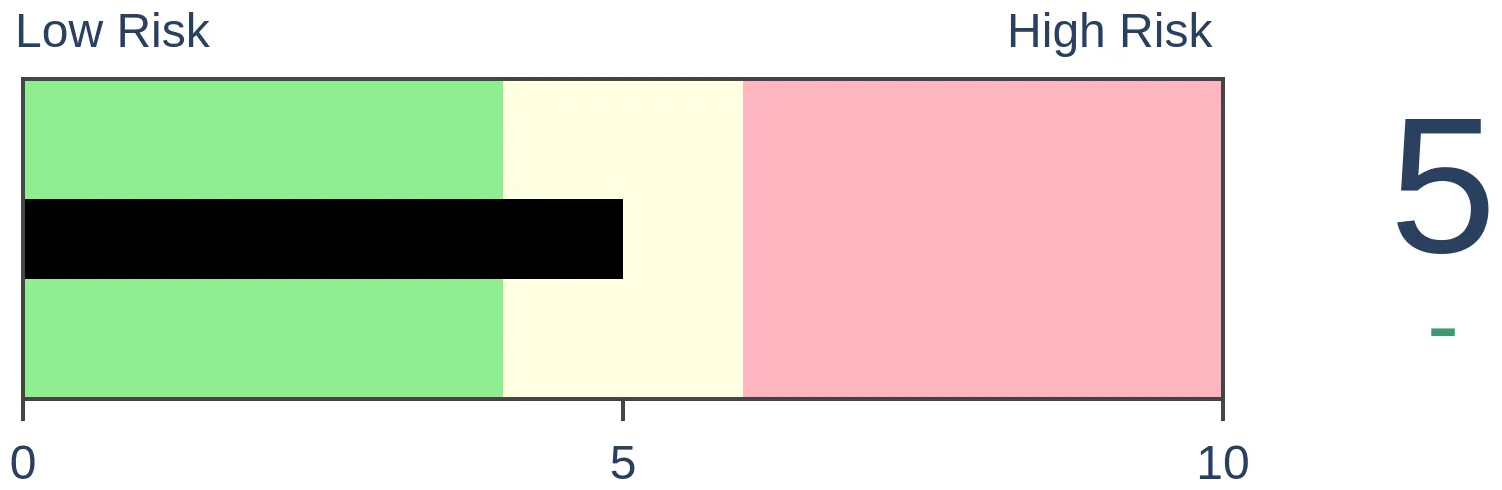

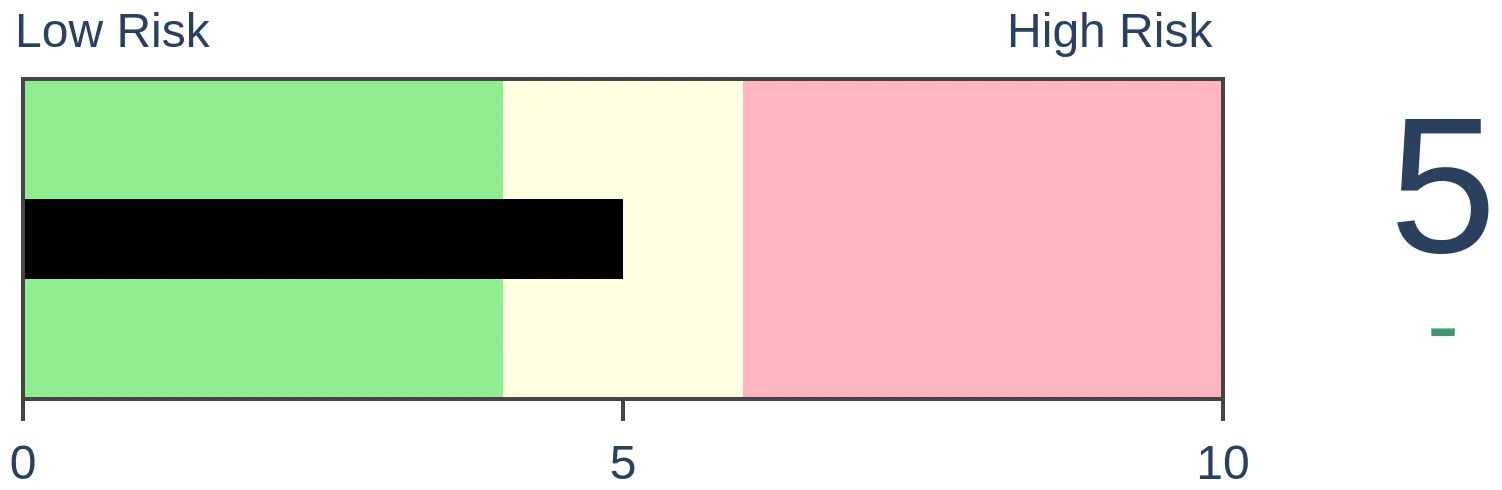

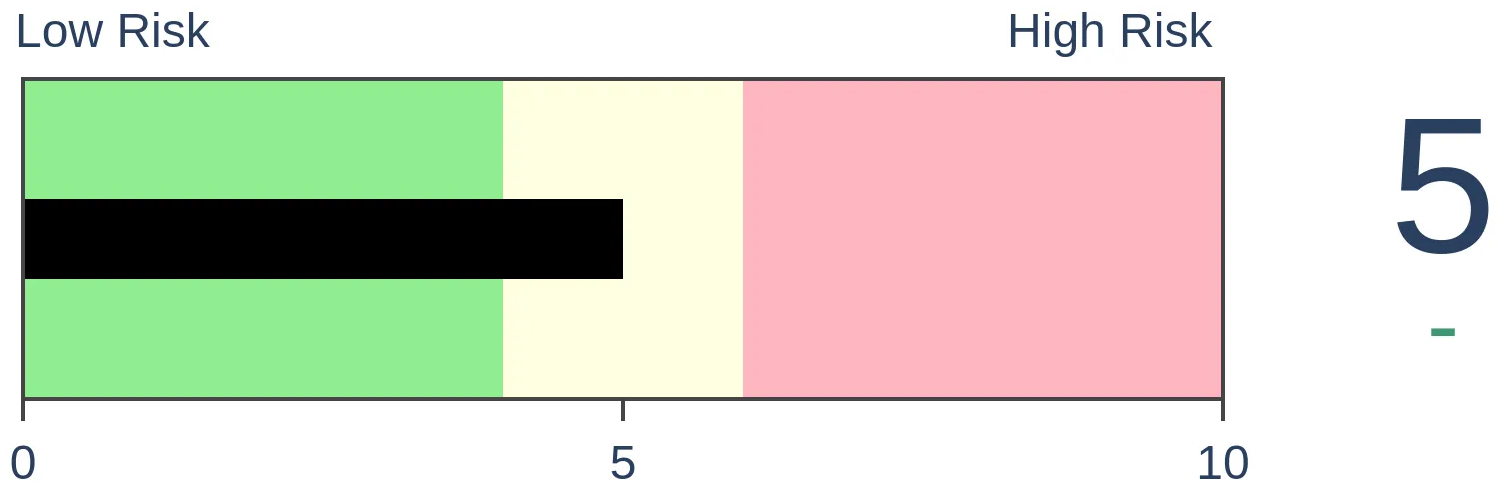

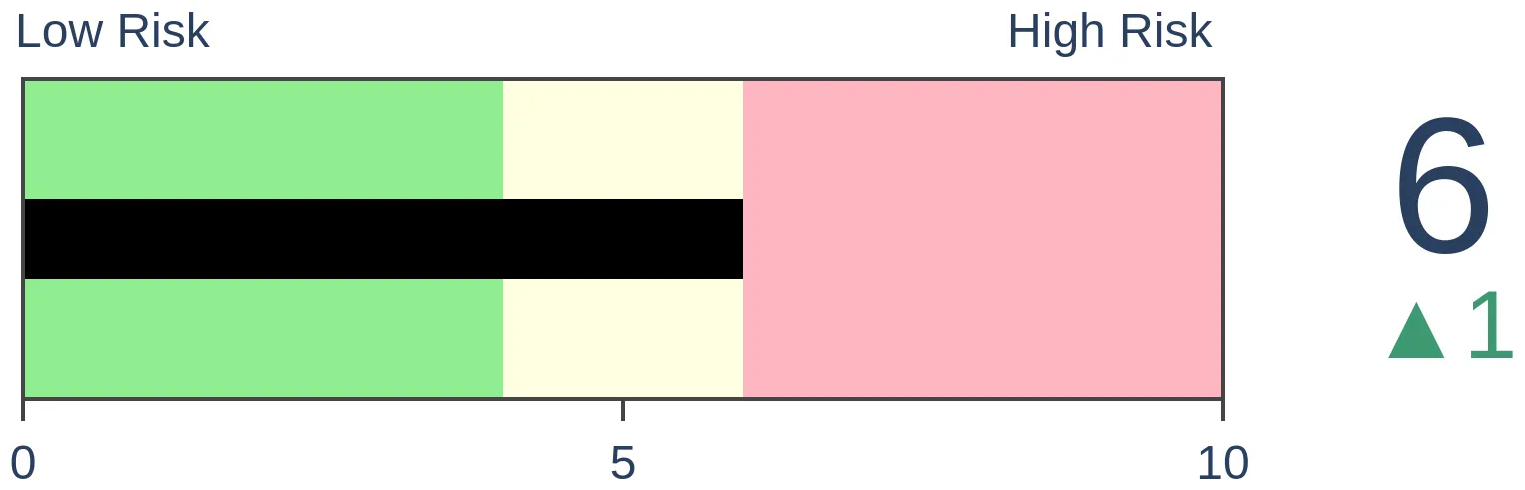

Risk Levels

Stocks Short-Term

|

Stocks Medium-Term

|

|

Bonds

|

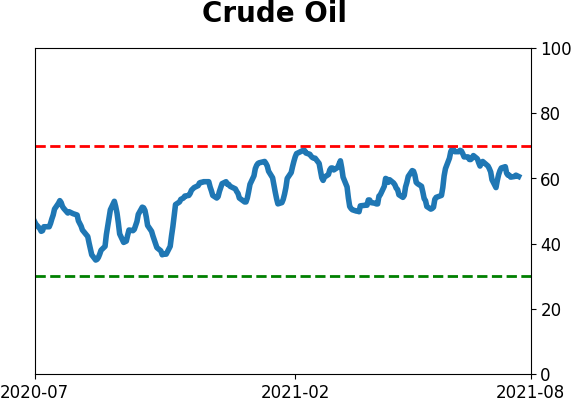

Crude Oil

|

|

Gold

|

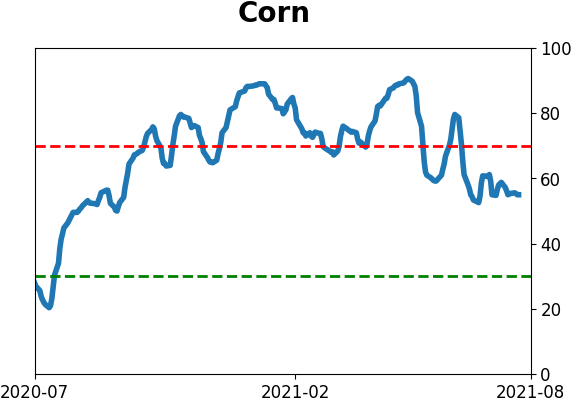

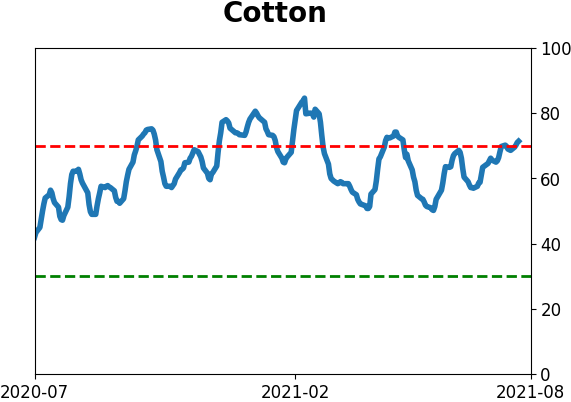

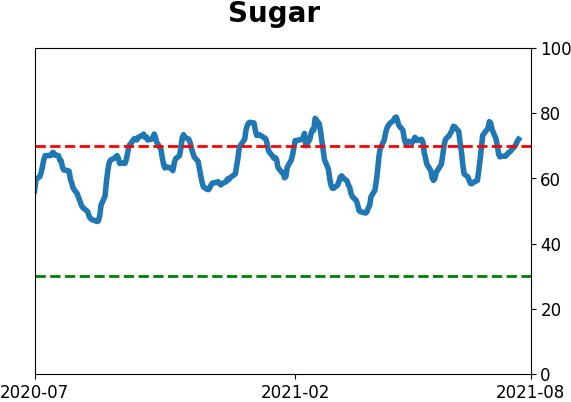

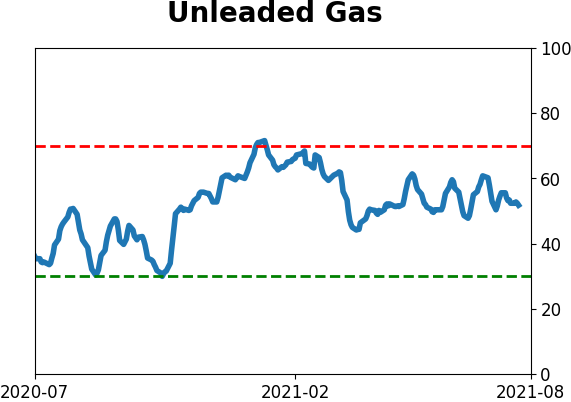

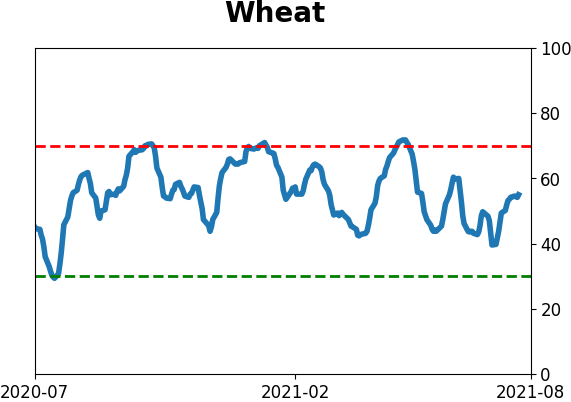

Agriculture

|

|

Research

By Jason Goepfert

BOTTOM LINE

For the first time in over a year, speculators in the U.S. dollar are betting that it will rally. Speculators are shorting other currency futures relative to the dollar, ending one of the longest streaks in 30 years of doing the opposite.

FORECAST / TIMEFRAME

None

|

The U.S. is the place to be. Investors have been betting on domestic stocks and bonds to continue soaring. Might as well bet on the dollar, too.

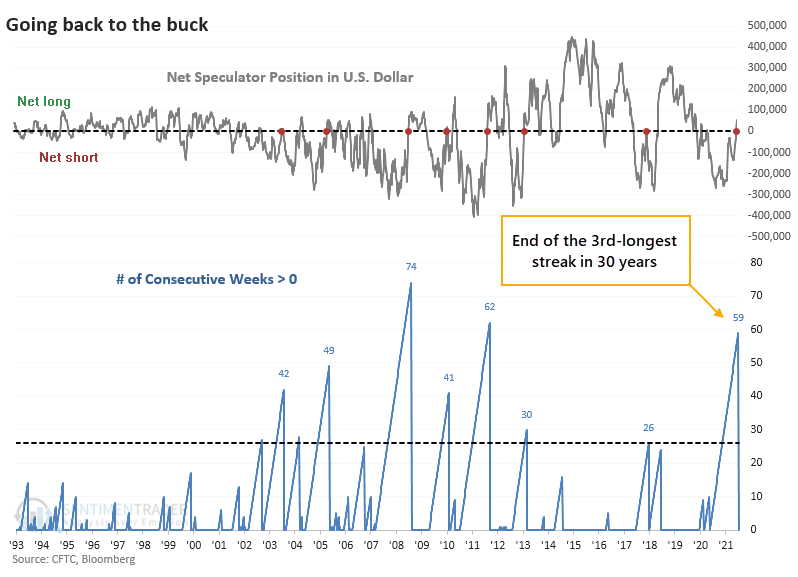

Bloomberg notes that speculators in the dollar versus its major peers have flipped to a net long position for the first time in months, meaning they're shorting other currencies against the buck. This just ended the 3rd-longest streak of shorting the dollar in 30 years.

For 59 consecutive weeks, well over a year, speculators had been short the dollar. That's just below the streak of 62 weeks that ended in September 2011, which happened to mark the end of a long period of a declining dollar.

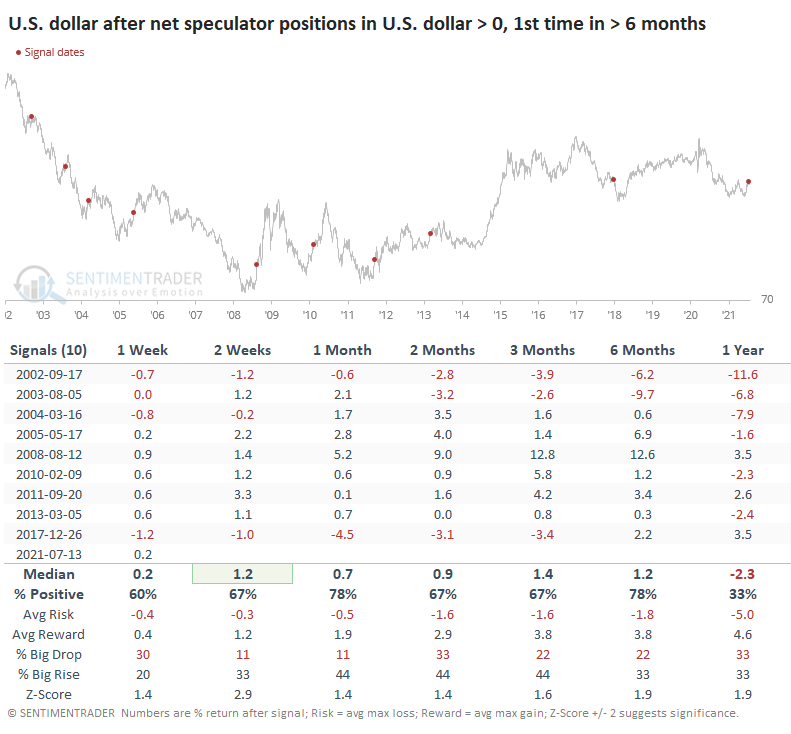

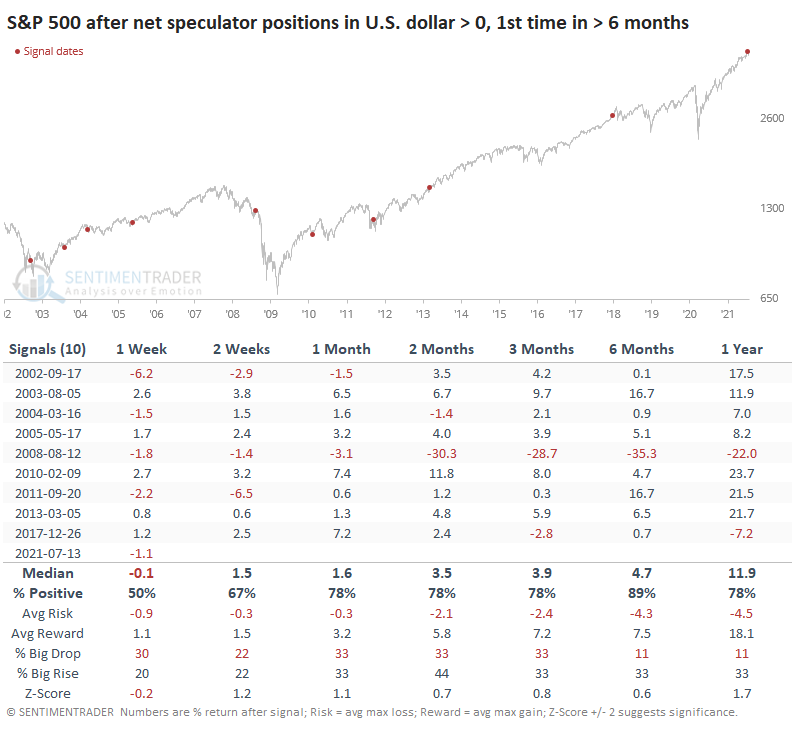

BETTING ON THE BUCK WAS A GOOD SIGN

For the dollar, it was a good sign when speculators decided to start betting on the currency again after a long period of shorting it. All of the signals triggered in the past 20 years.

Over all time frames up to six months later, the dollar performed well on average. There were a few losing periods, including the most recent one. But generally, the return of these trend-following traders tended to keep pushing the buck higher in the months ahead.

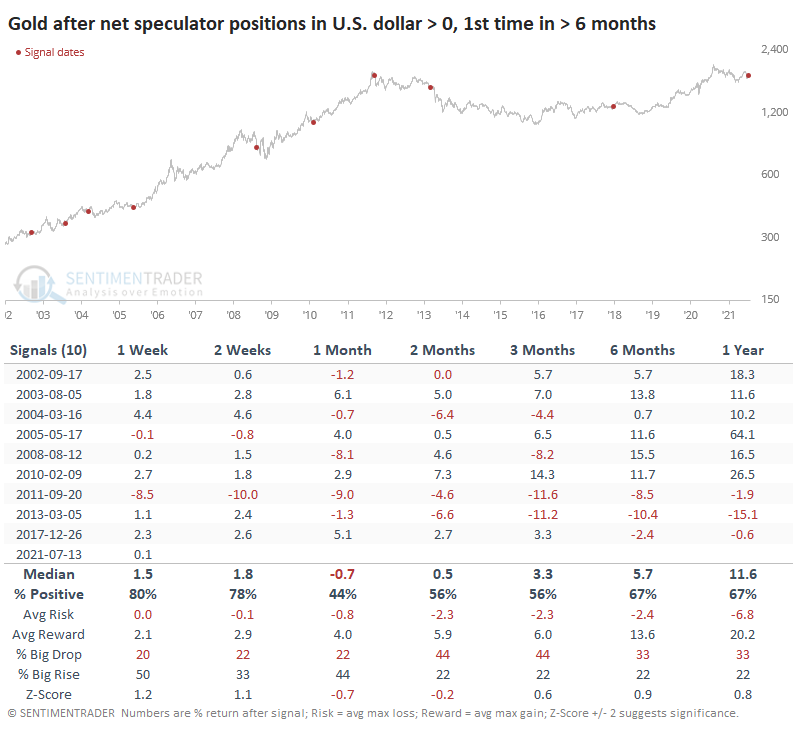

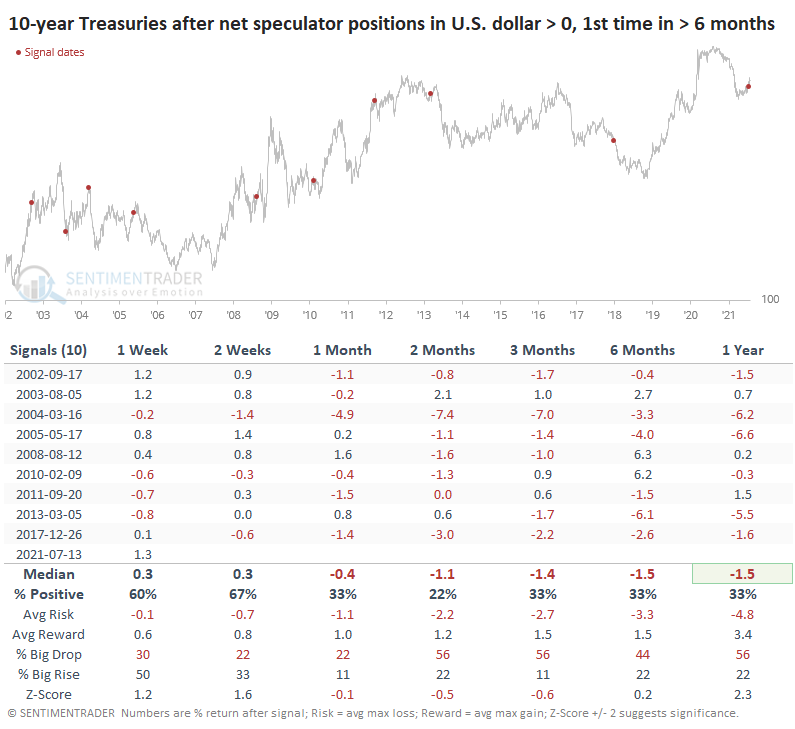

OTHER MARKETS MIXED, EXCEPT FOR BONDS

Gold did okay despite the mostly rising dollar. Thanks to most of these signals triggering during the mid-2000 run-up in gold, it did not suffer consistent losses. There were some big ones in there, and it's not like this was a good buy signal for gold, it's just that it didn't consistently plunge due to a rising dollar.

For U.S.-based large-cap stocks, the rising dollar mostly preceded higher returns. The last 20 years have been overwhelmingly dominated by bull markets, so we should fully expect positive returns. Even so, the ones after these signals were better than random, with the glaring exception of August 2008.

Bond futures did not react well to speculators returning to the dollar. Every signal showed a loss in 10-year Treasury note futures at some point between one and three months later.

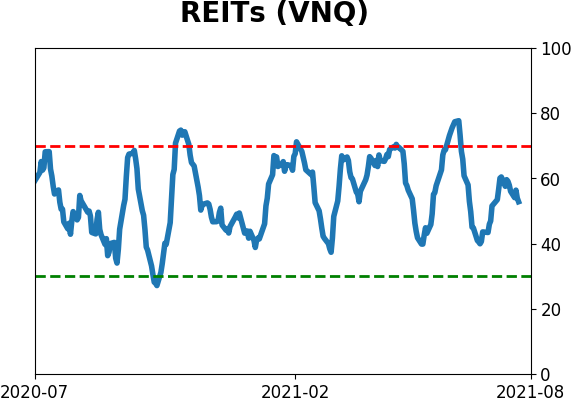

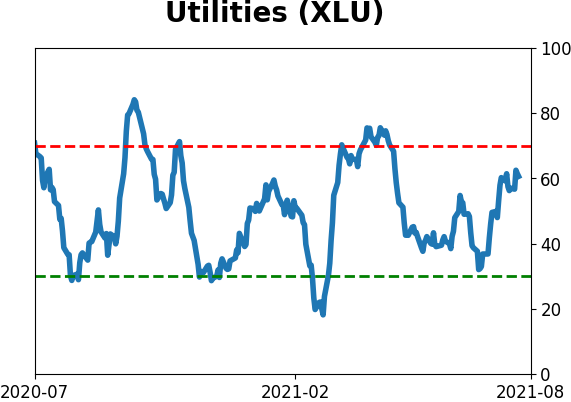

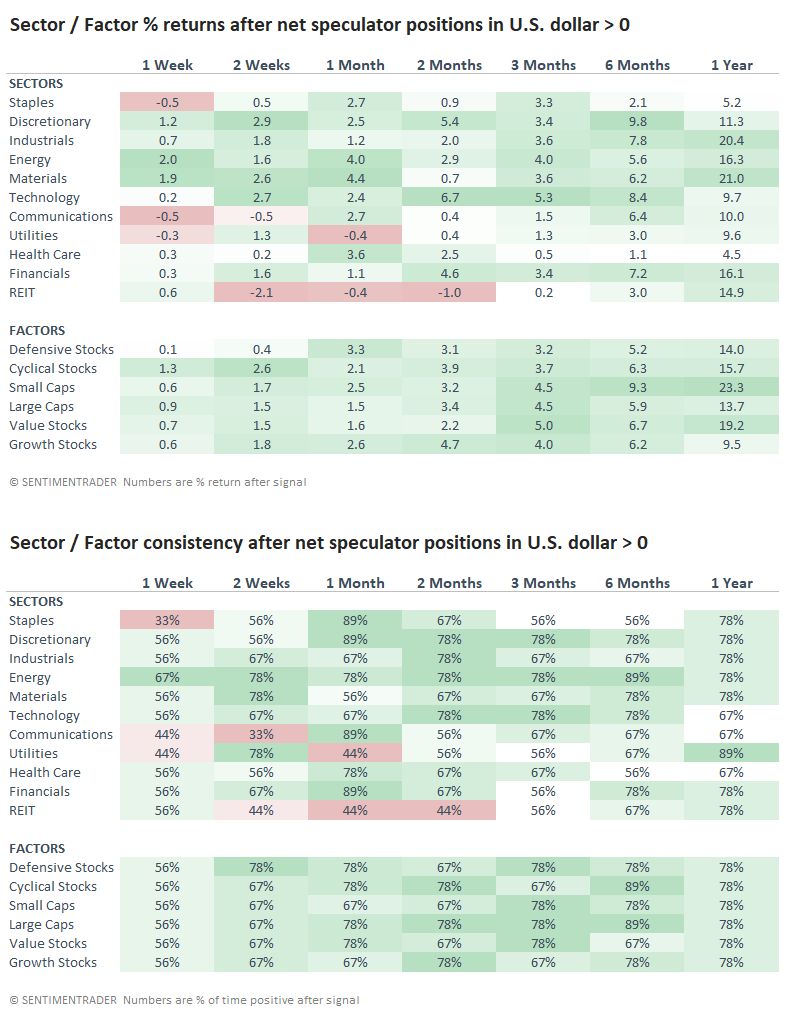

For sectors and factors, the tendency for bonds to decline (and interest rates rise) meant that rate-sensitive sectors like Utilities and REITs struggled over the short- to medium-term.

The dollar is trying to overcome a long-term downtrend, and a persistent tendency for speculators to short every rally doesn't help. That behavior has been changing lately, however, and if these traders now have the mentality of buying dips, it could be enough to at least temporarily change the risk/reward in the dollar back to the positive side.

Active Studies

| Time Frame | Bullish | Bearish | | Short-Term | 0 | 4 | | Medium-Term | 4 | 3 | | Long-Term | 10 | 5 |

|

Indicators at Extremes

Portfolio

| Position | Description | Weight % | Added / Reduced | Date | | Stocks | RSP | 4.1 | Added 4.1% | 2021-05-19 | | Bonds | 23.9% BND, 6.9% SCHP | 30.7 | Reduced 7.1% | 2021-05-19 | | Commodities | GCC | 2.6 | Reduced 2.1%

| 2020-09-04 | | Precious Metals | GDX | 5.6 | Reduced 4.2% | 2021-05-19 | | Special Situations | 4.3% XLE, 2.2% PSCE | 7.6 | Reduced 5.6% | 2021-04-22 | | Cash | | 49.4 | | |

|

Updates (Changes made today are underlined)

Much of our momentum and trend work has remained positive for several months, with some scattered exceptions. Almost all sentiment-related work has shown a poor risk/reward ratio for stocks, especially as speculation drove to record highs in exuberance in February. Much of that has worn off, and most of our models are back toward neutral levels. There isn't much to be excited about here. The same goes for bonds and even gold. Gold has been performing well lately and is back above long-term trend lines. The issue is that it has a poor record of holding onto gains when attempting a long-term trend change like this, so we'll take a wait-and-see approach. RETURN YTD: 9.1% 2020: 8.1%, 2019: 12.6%, 2018: 0.6%, 2017: 3.8%, 2016: 17.1%, 2015: 9.2%, 2014: 14.5%, 2013: 2.2%, 2012: 10.8%, 2011: 16.5%, 2010: 15.3%, 2009: 23.9%, 2008: 16.2%, 2007: 7.8%

|

|

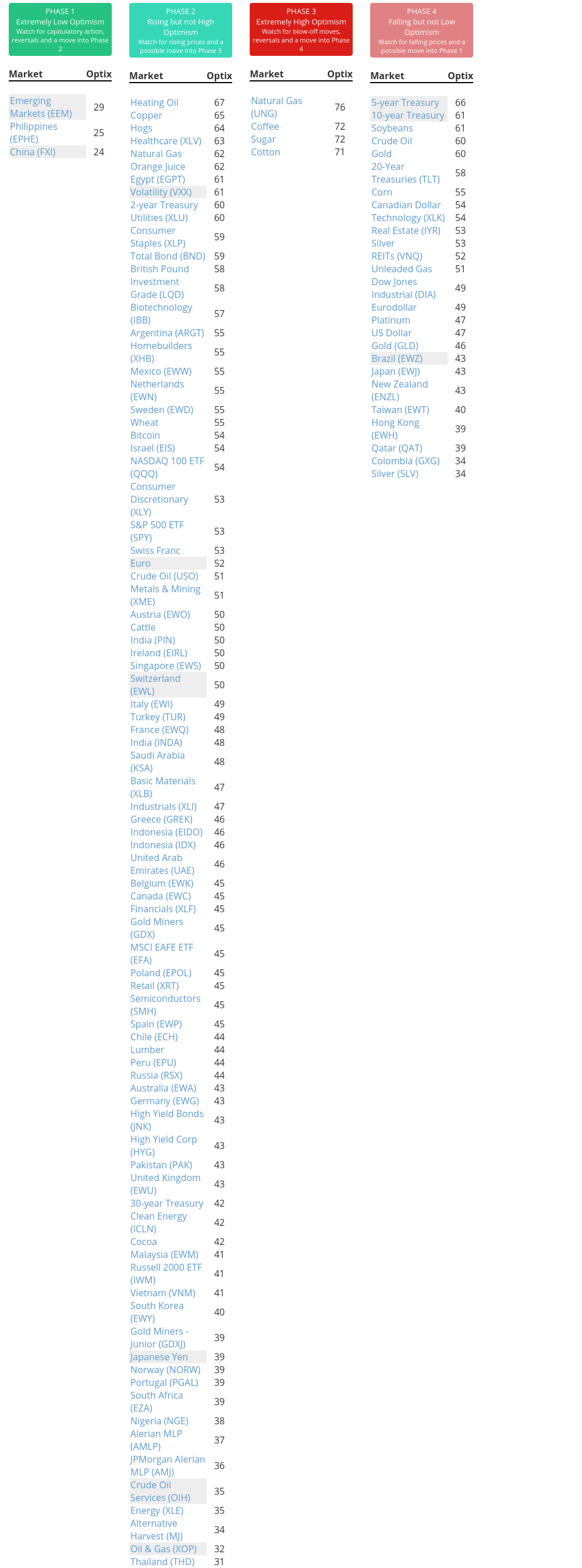

Phase Table

Ranks

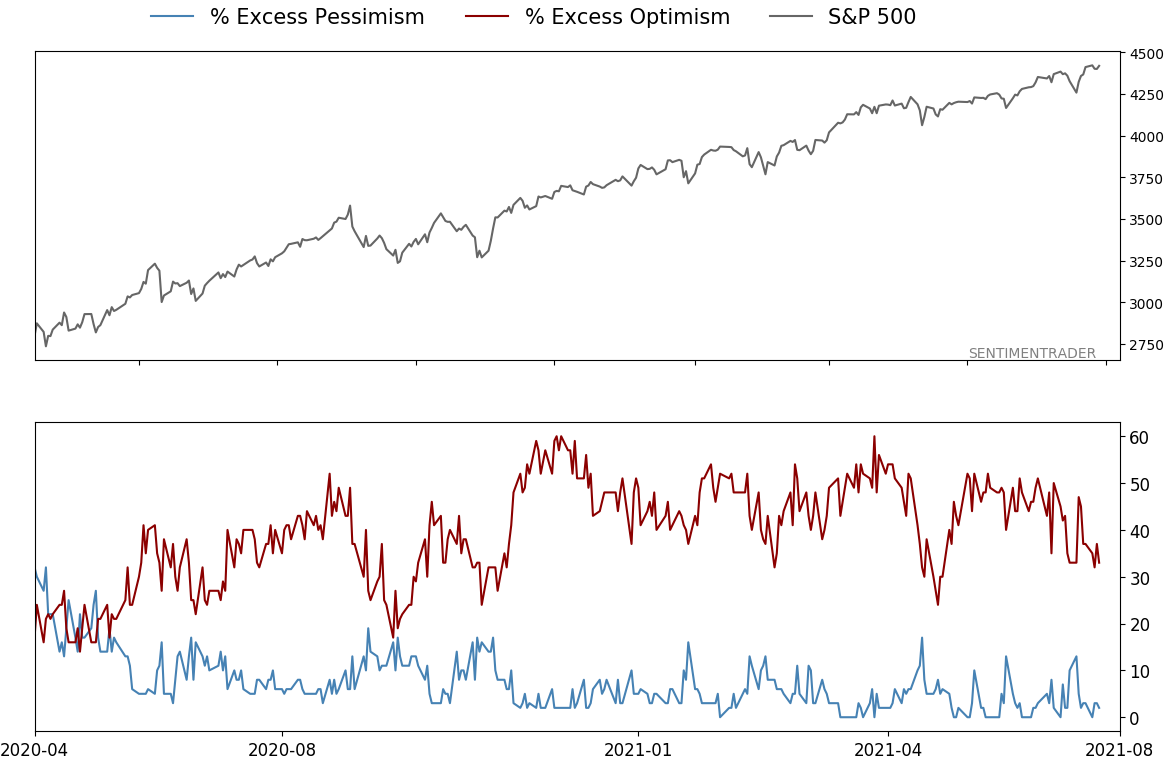

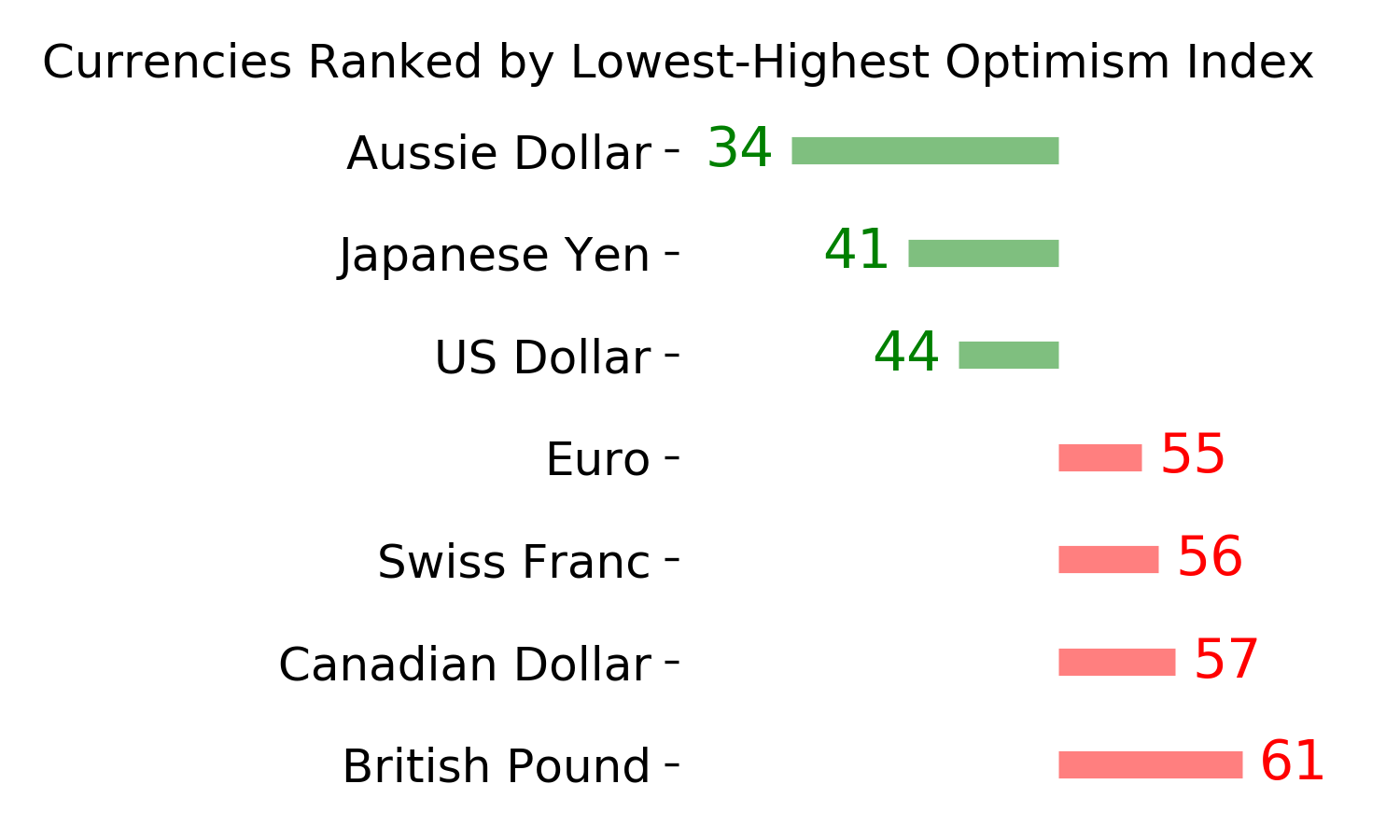

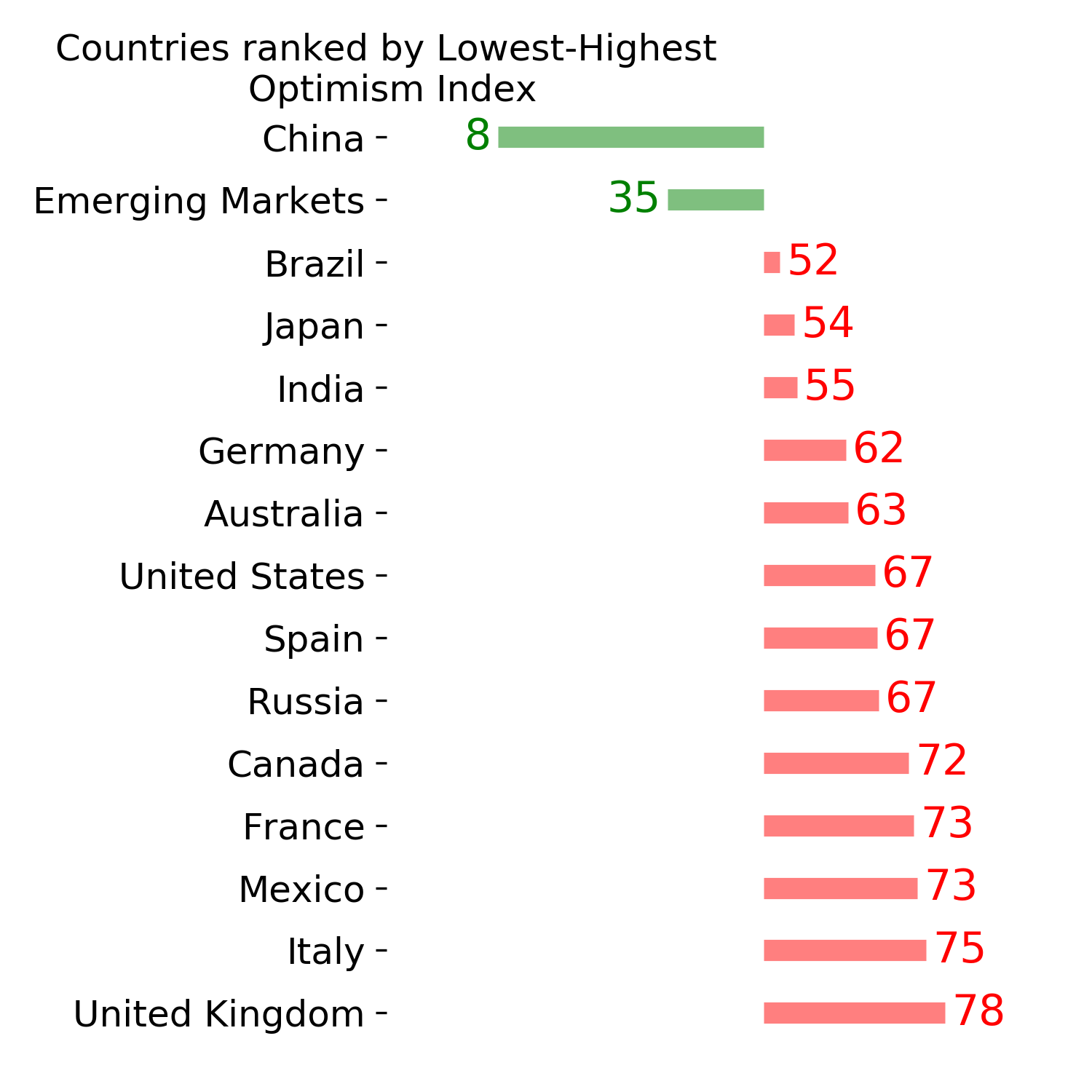

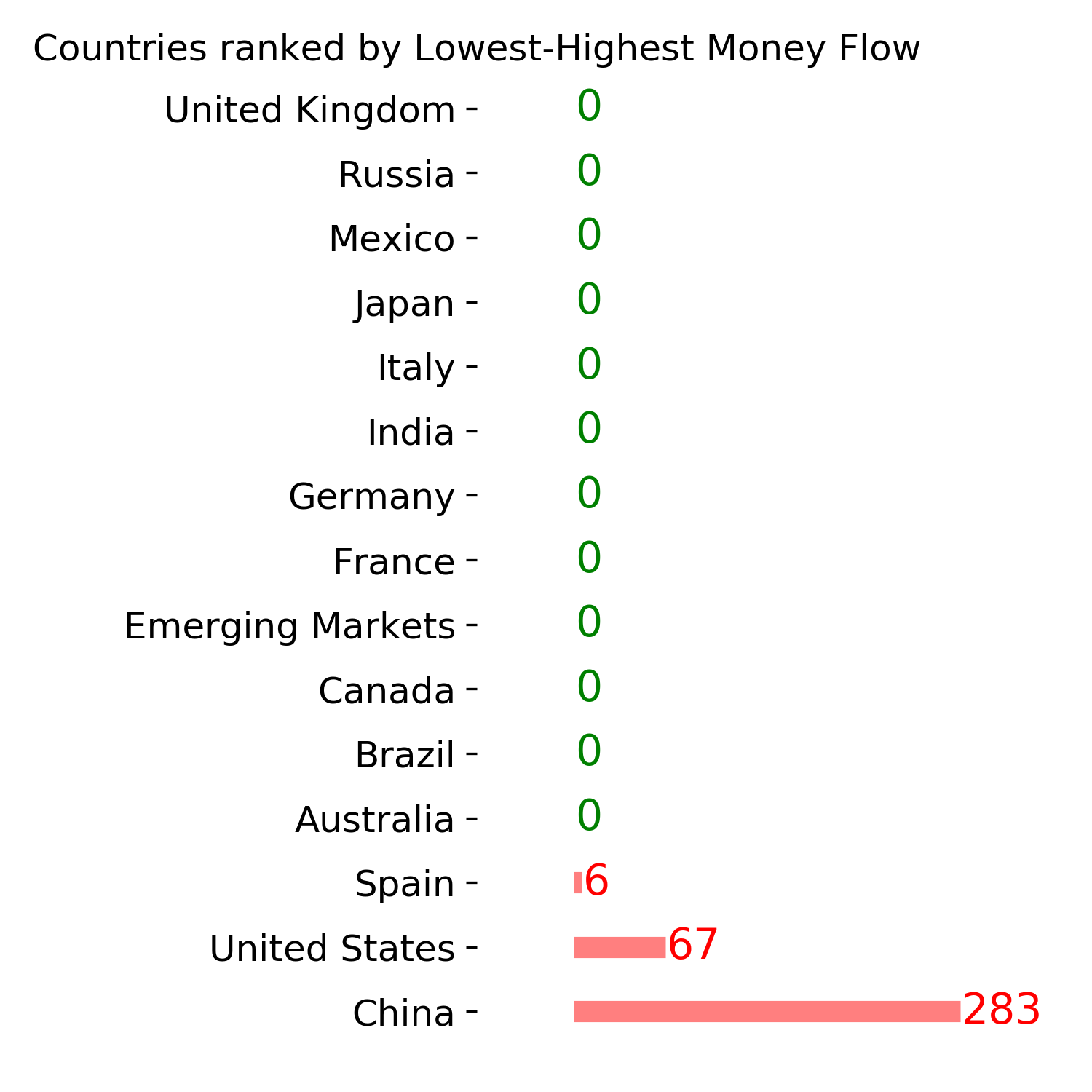

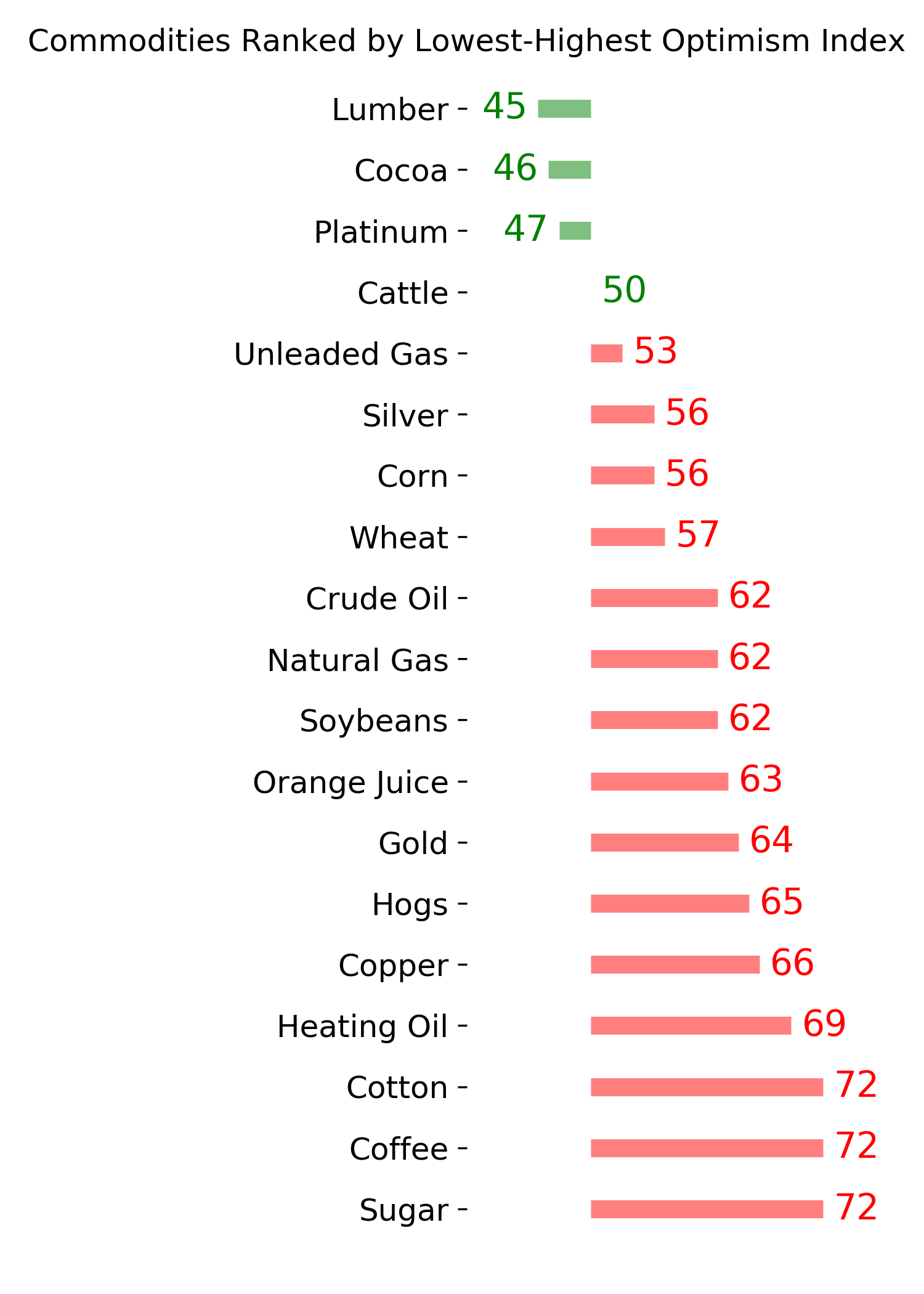

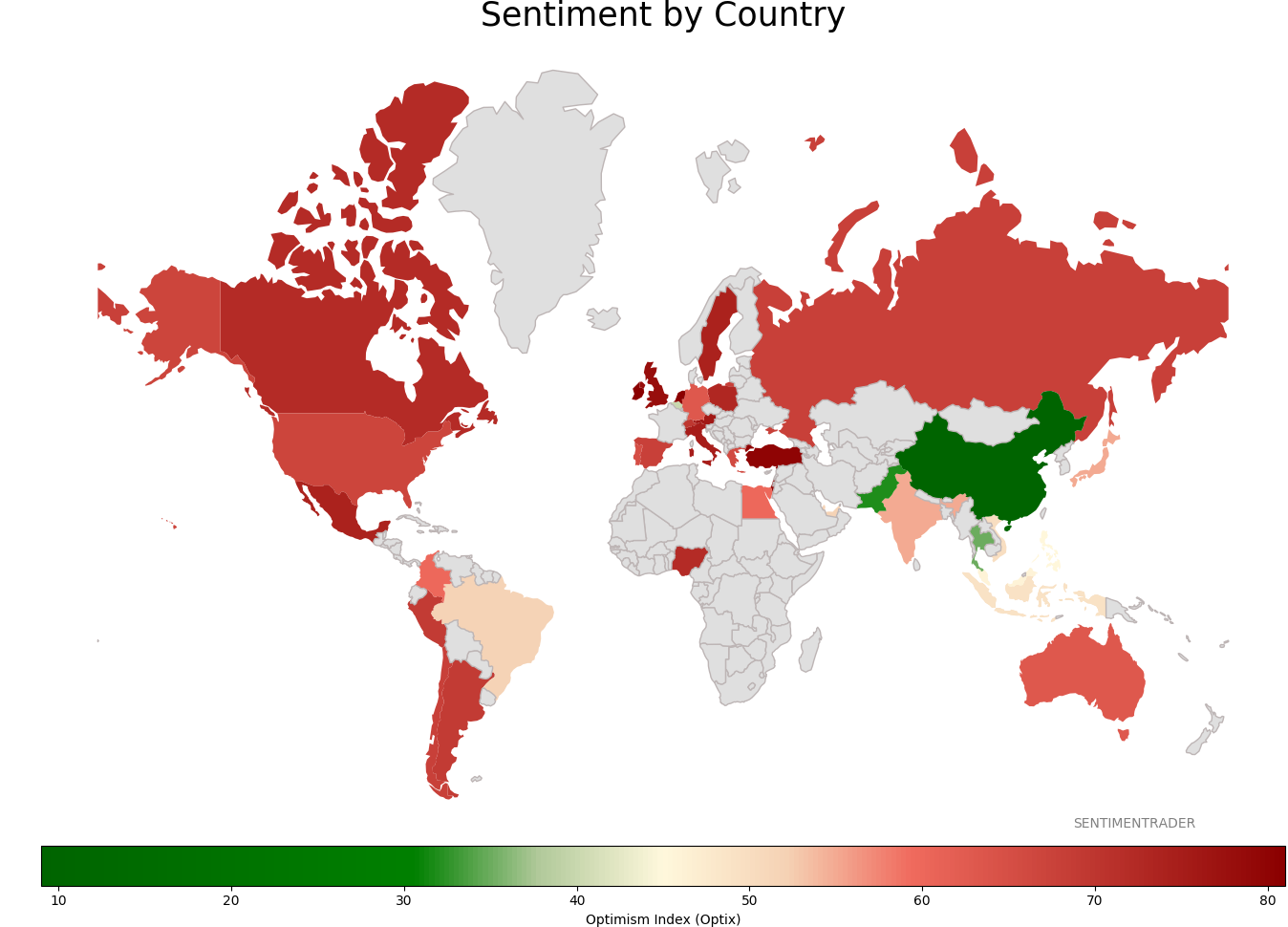

Sentiment Around The World

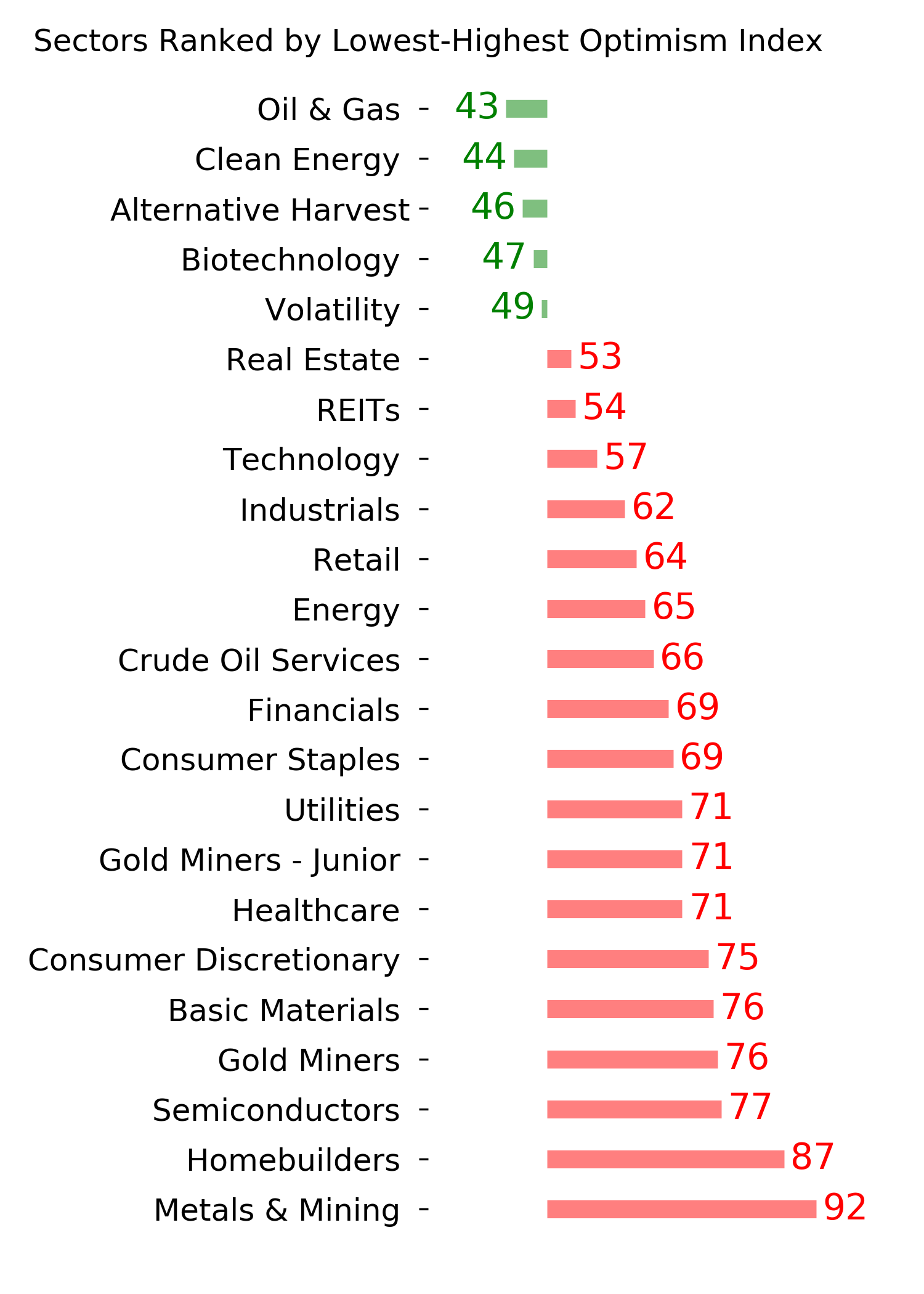

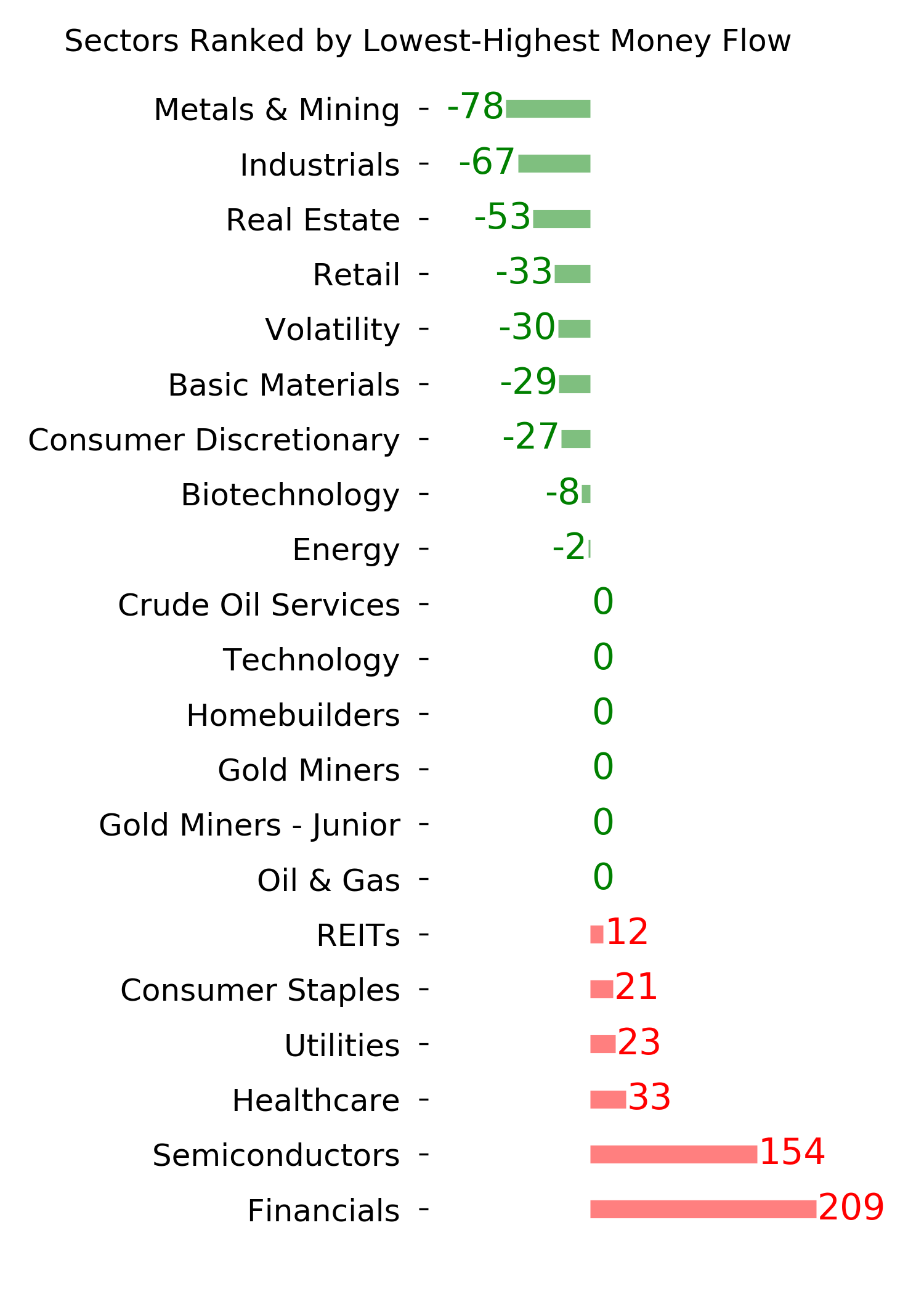

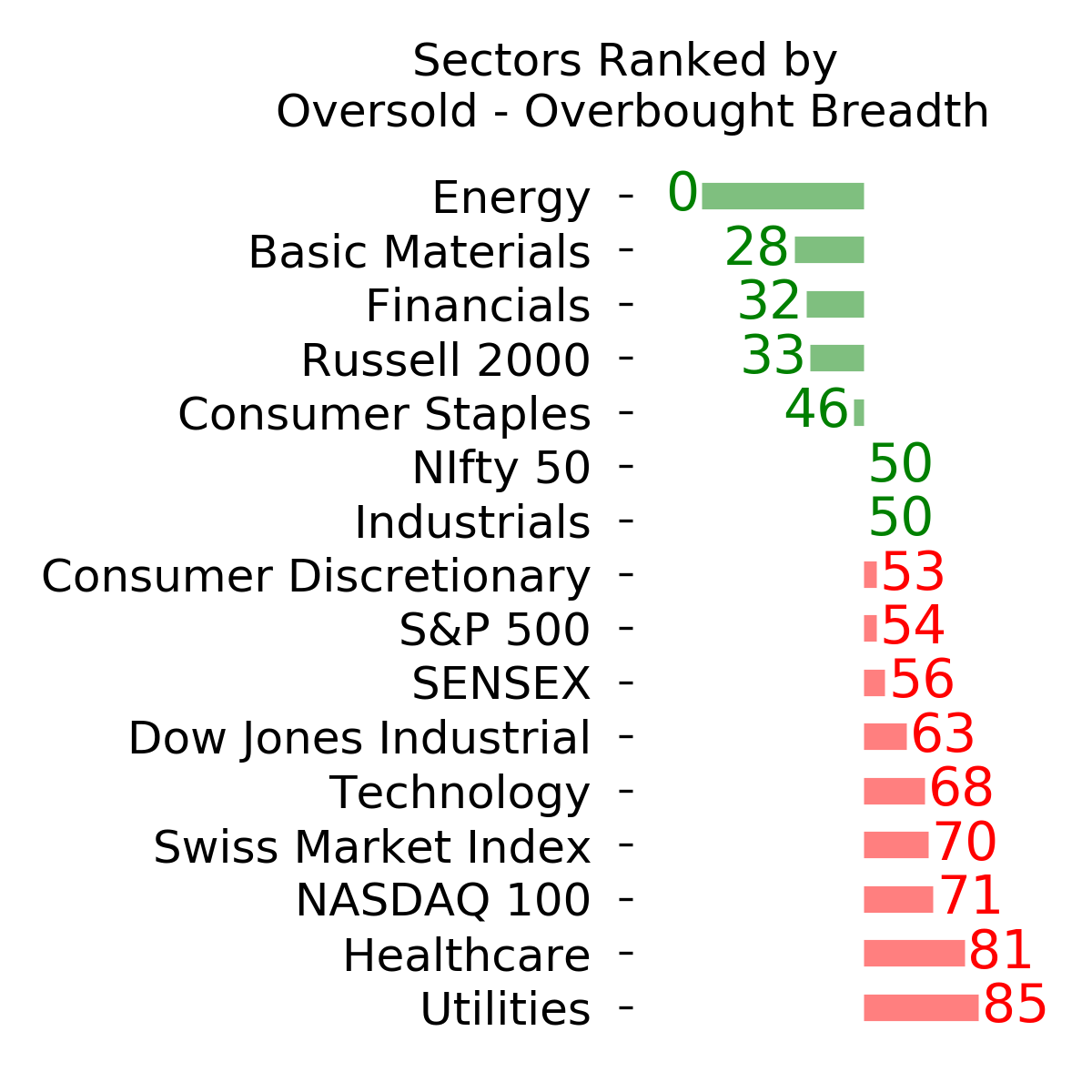

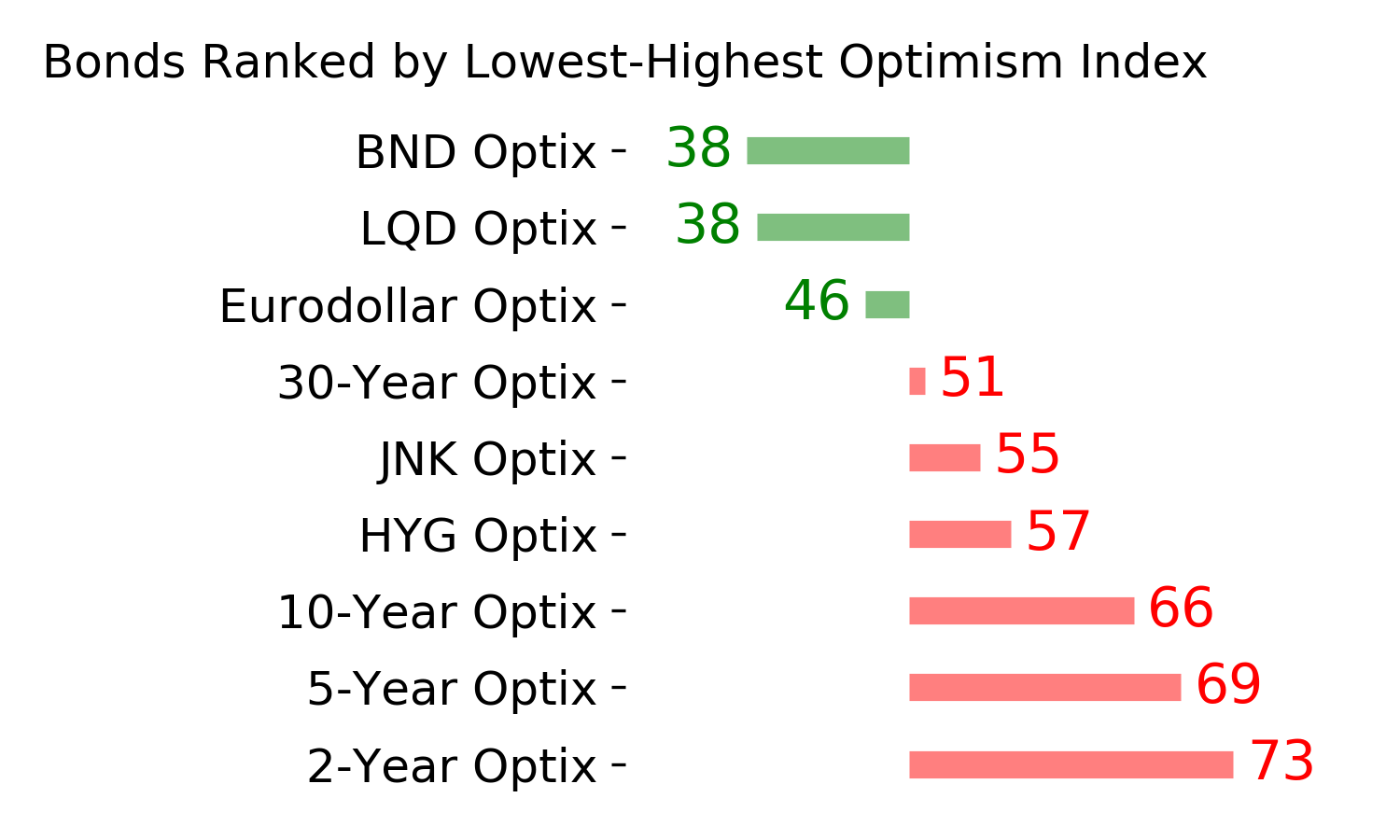

Optimism Index Thumbnails

|

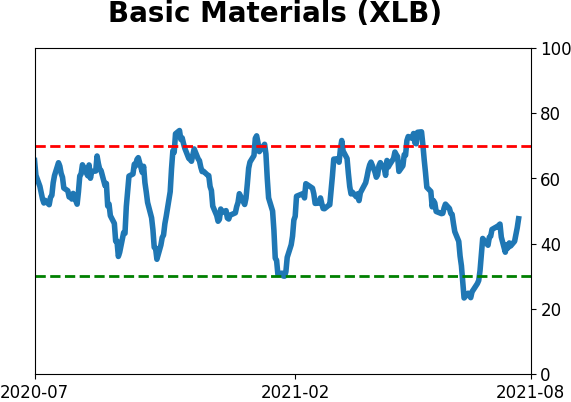

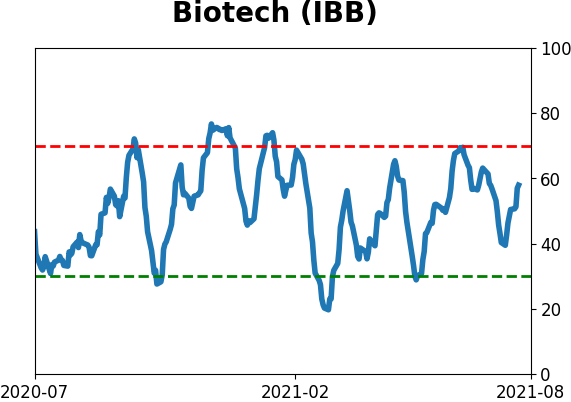

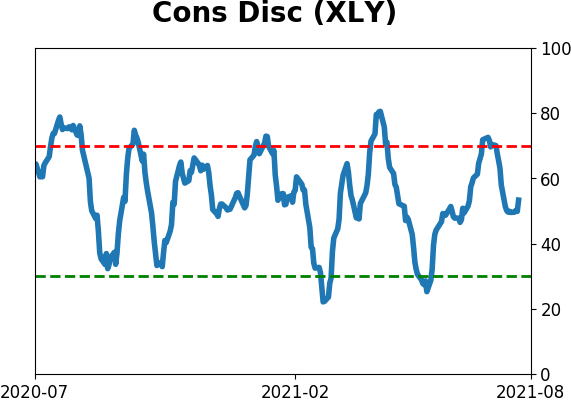

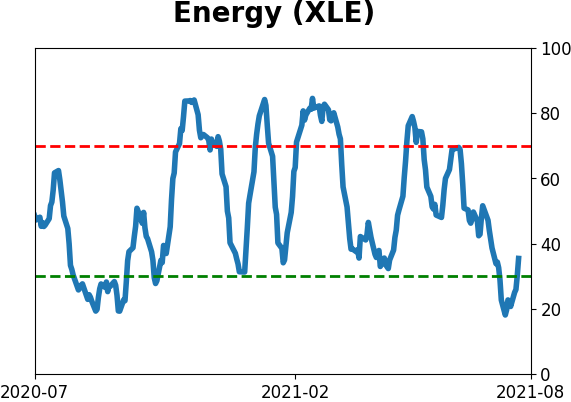

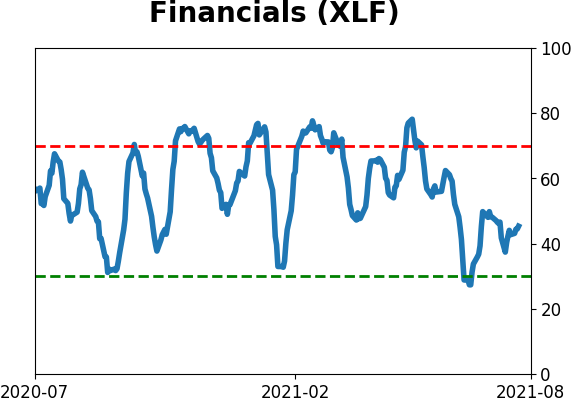

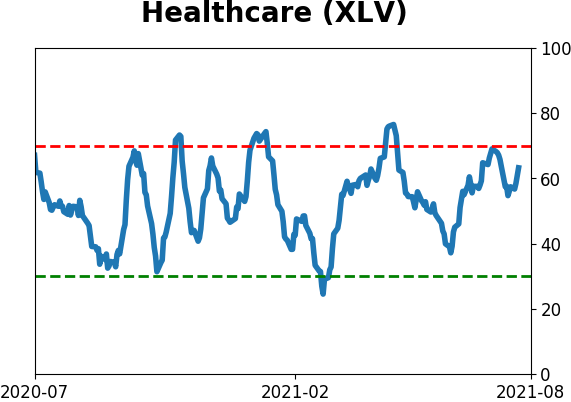

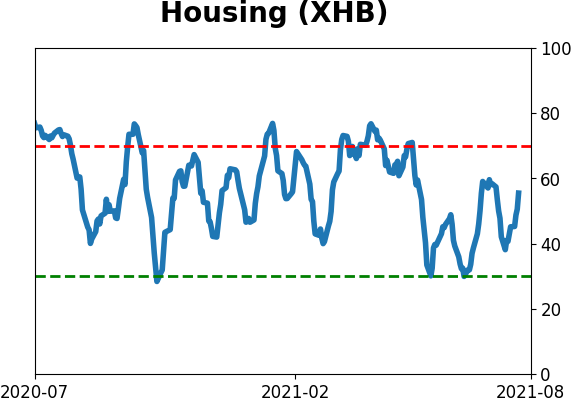

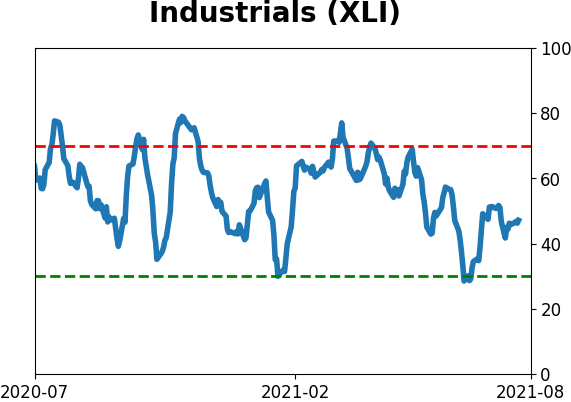

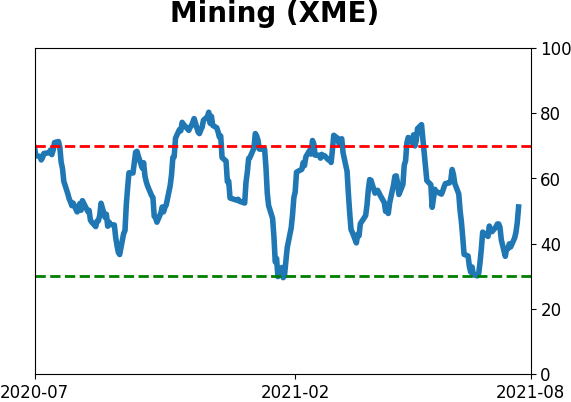

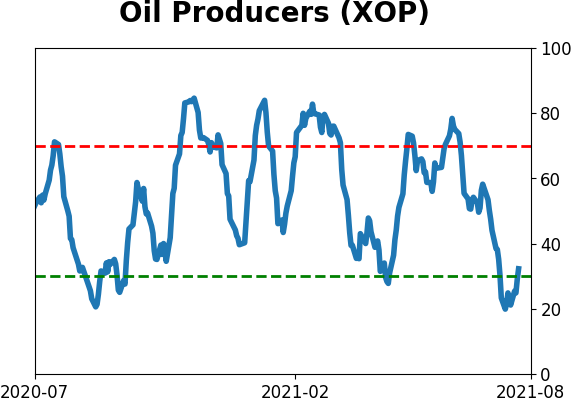

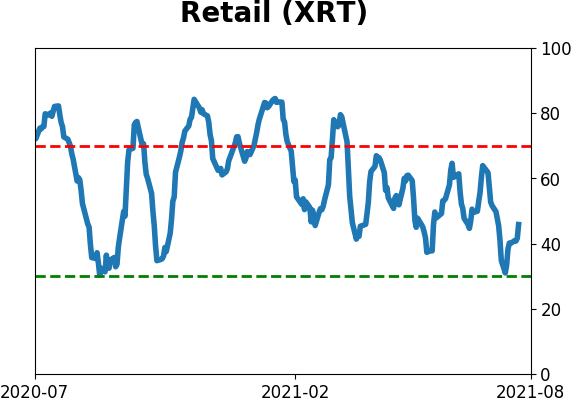

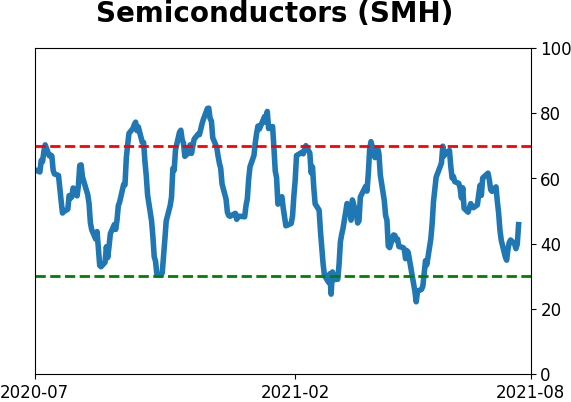

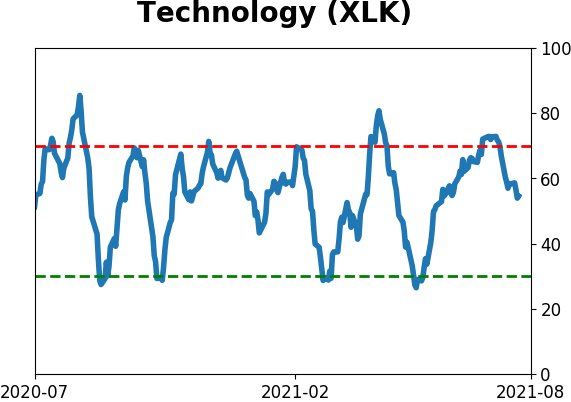

Sector ETF's - 10-Day Moving Average

|

|

|

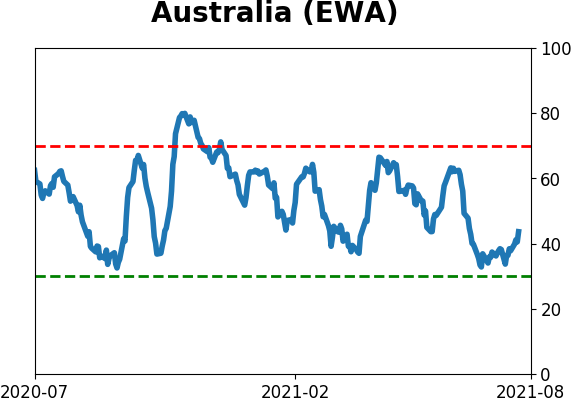

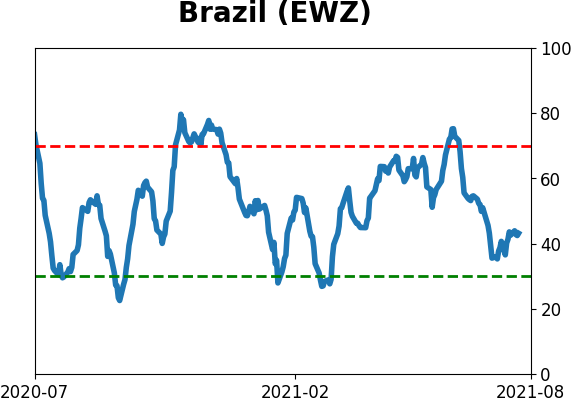

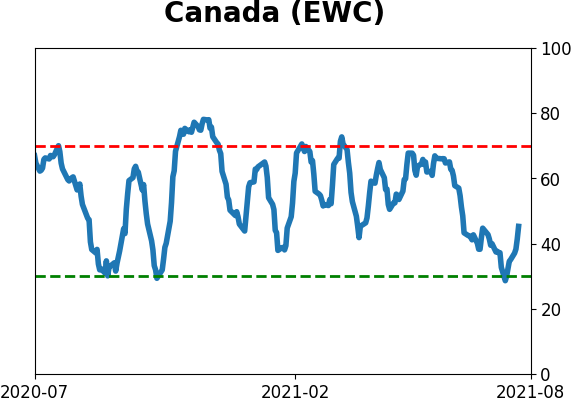

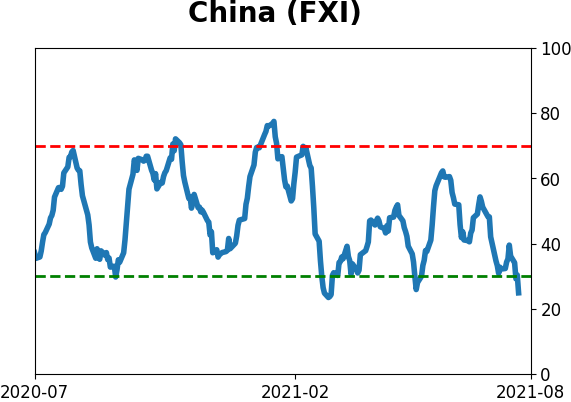

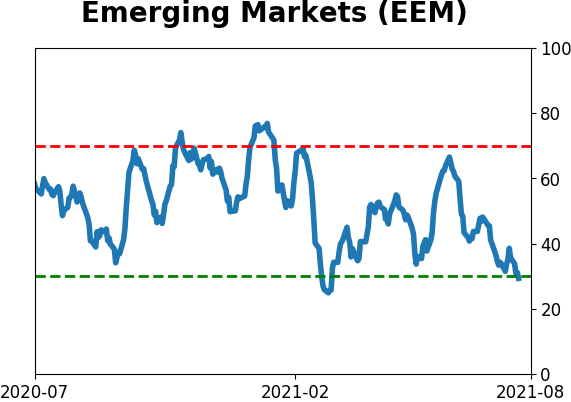

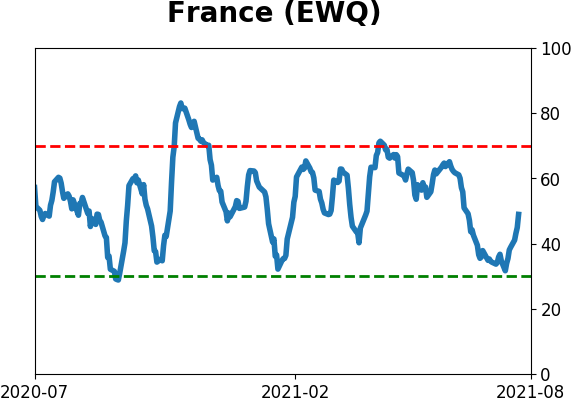

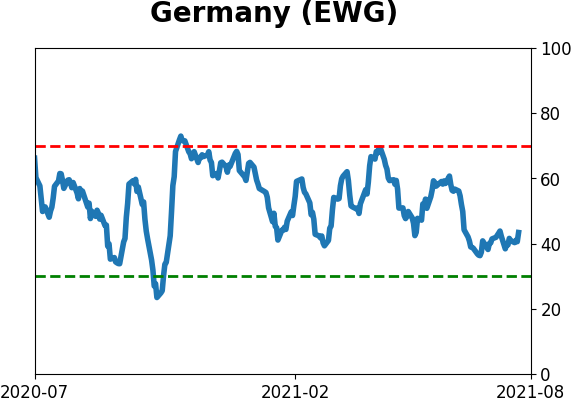

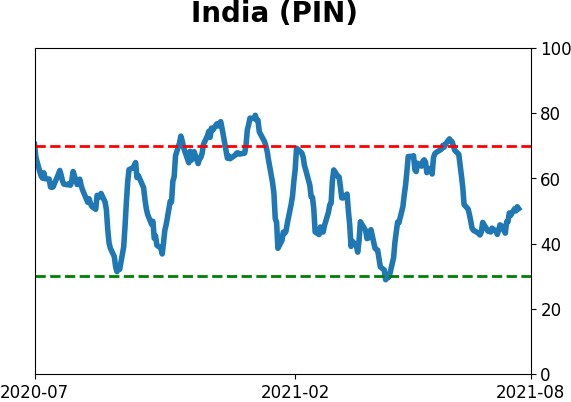

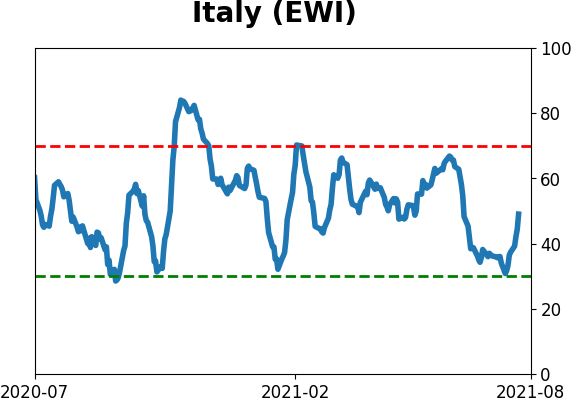

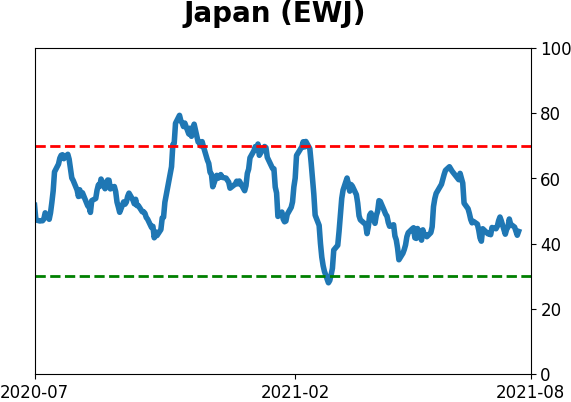

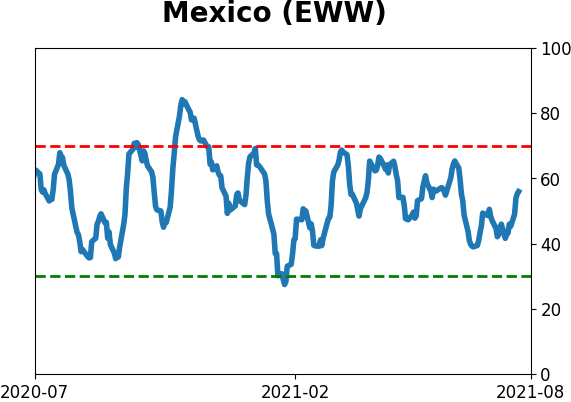

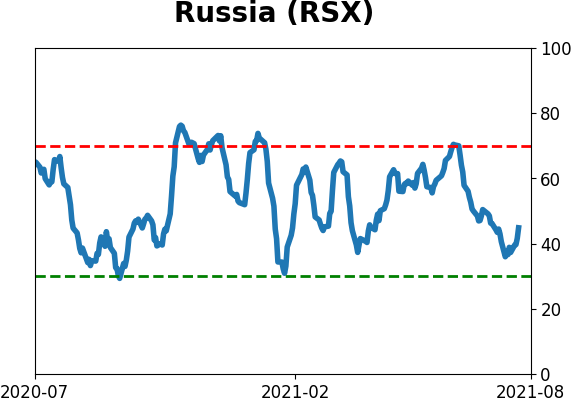

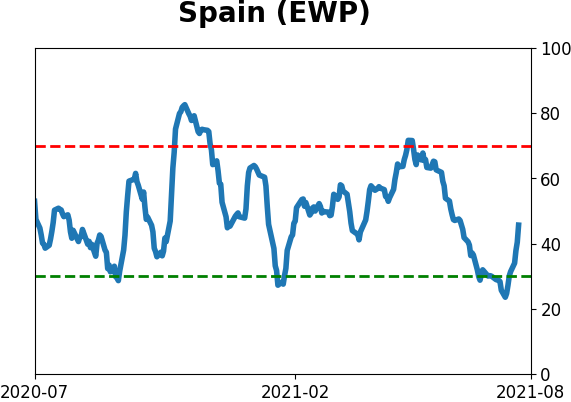

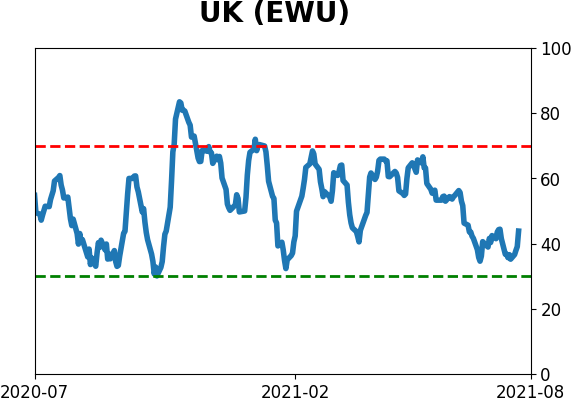

Country ETF's - 10-Day Moving Average

|

|

|

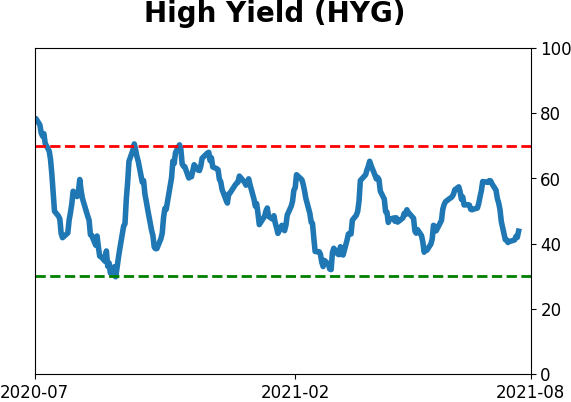

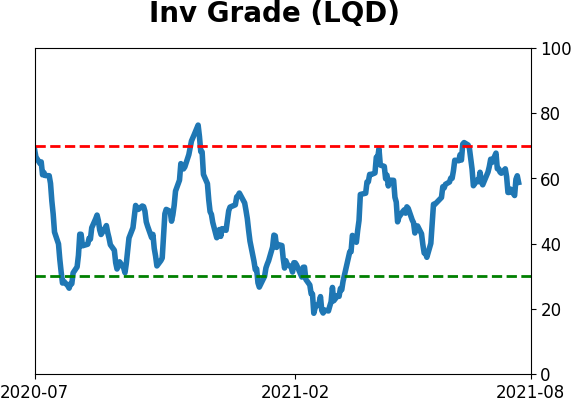

Bond ETF's - 10-Day Moving Average

|

|

|

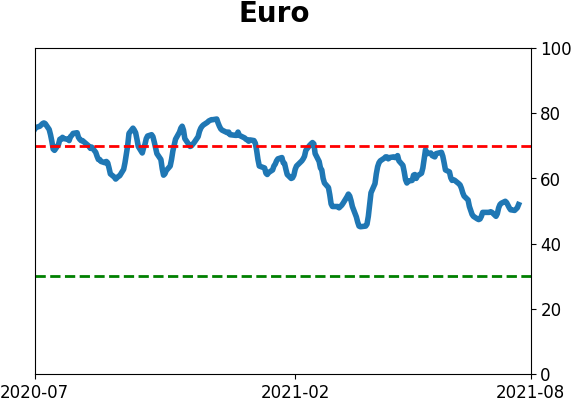

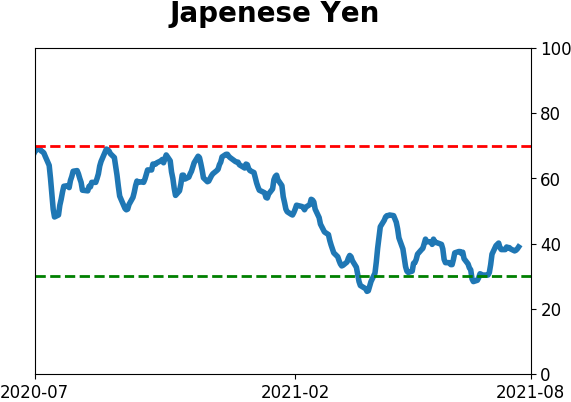

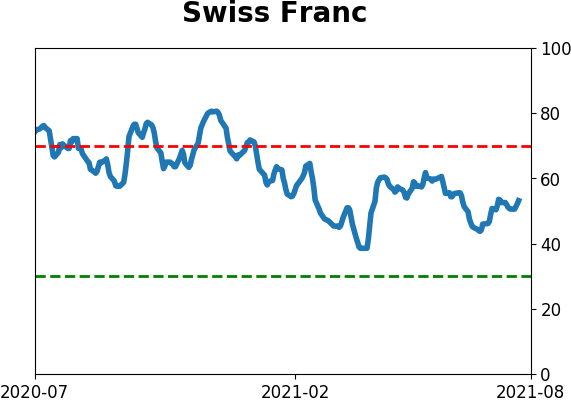

Currency ETF's - 5-Day Moving Average

|

|

|

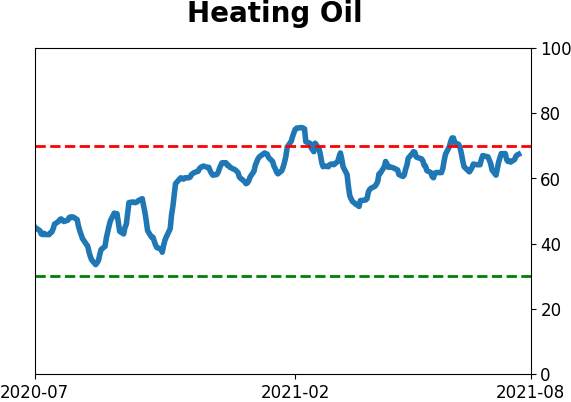

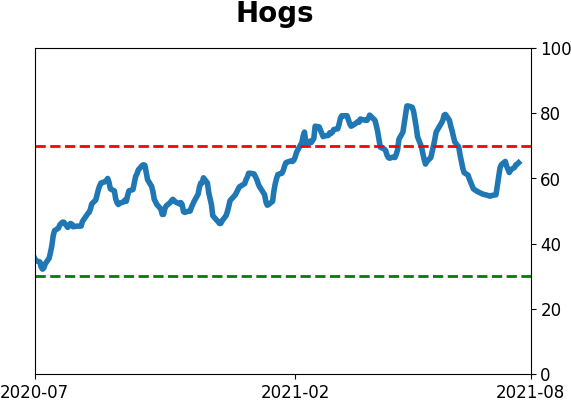

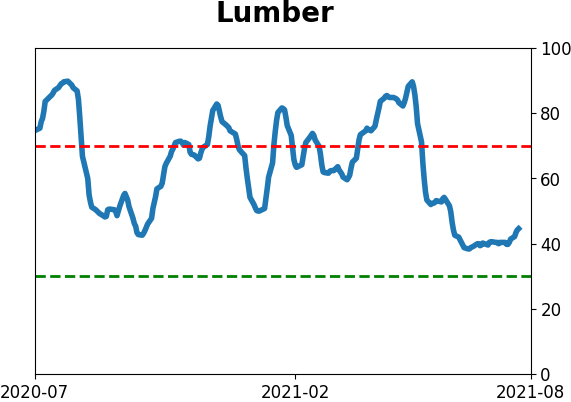

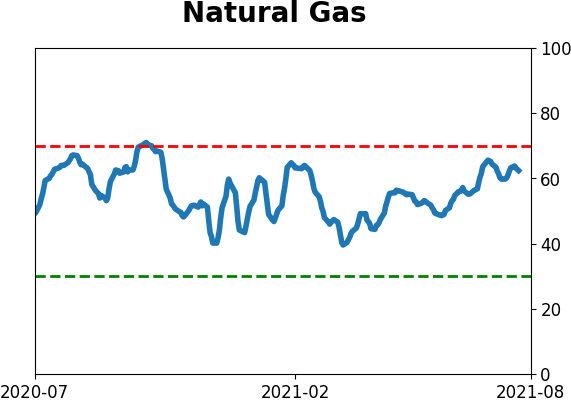

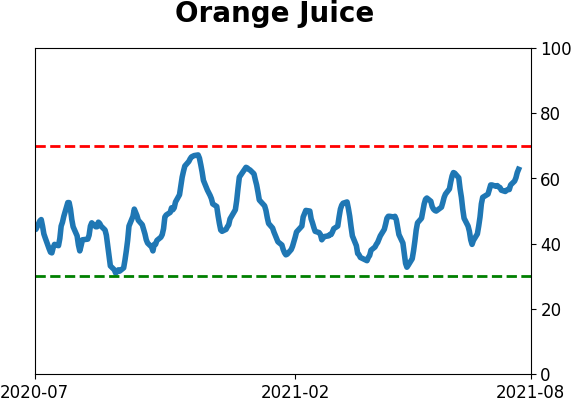

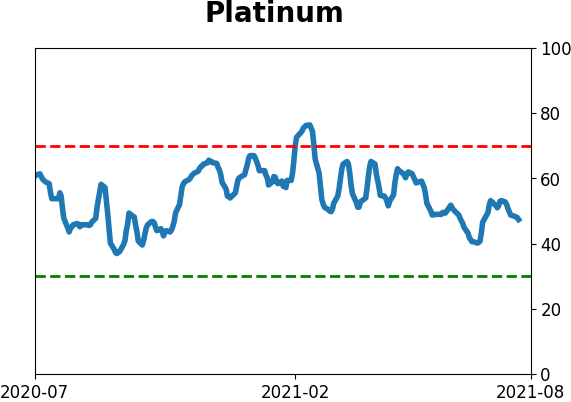

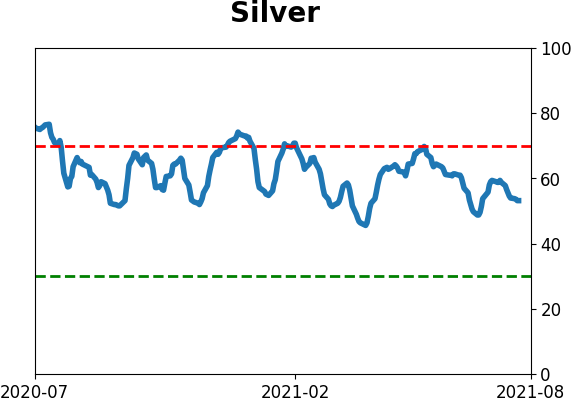

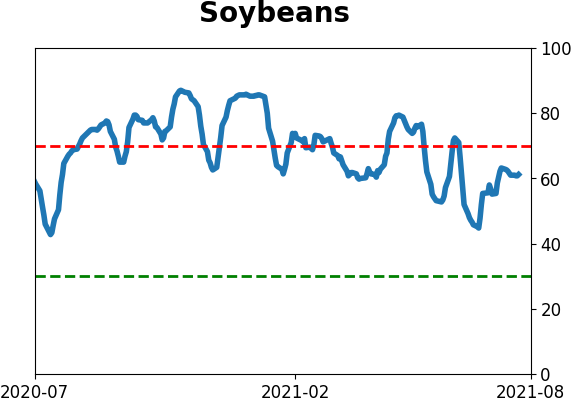

Commodity ETF's - 5-Day Moving Average

|

|