Headlines

|

|

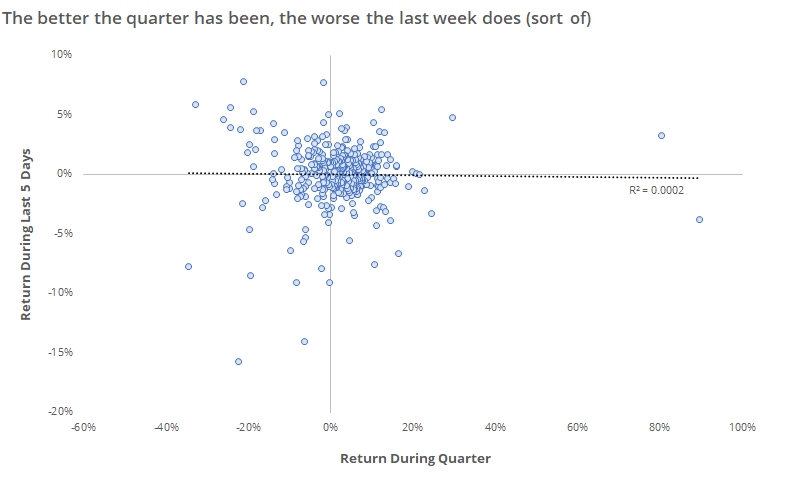

Looking at the last week of a big quarter:

This quarter has been among the very best in market history. Since 1928, this currently ranks in the top 10 of all quarters. When we look at how the S&P has fared up to the last week of each quarter, we can see a negative correlation with the return during the last week, potentially a result of rebalancing activity.

Indexes, and safe havens, rally without bringing members along:

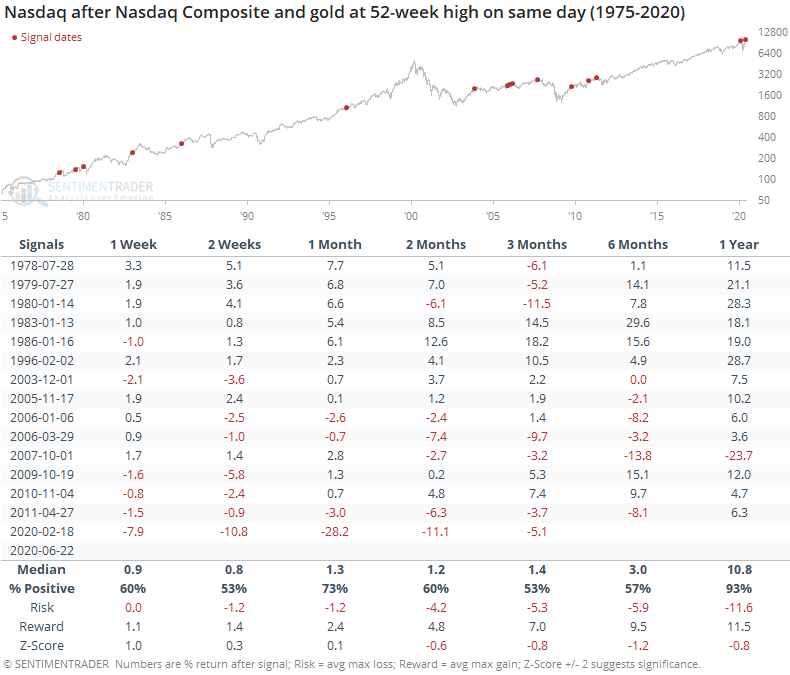

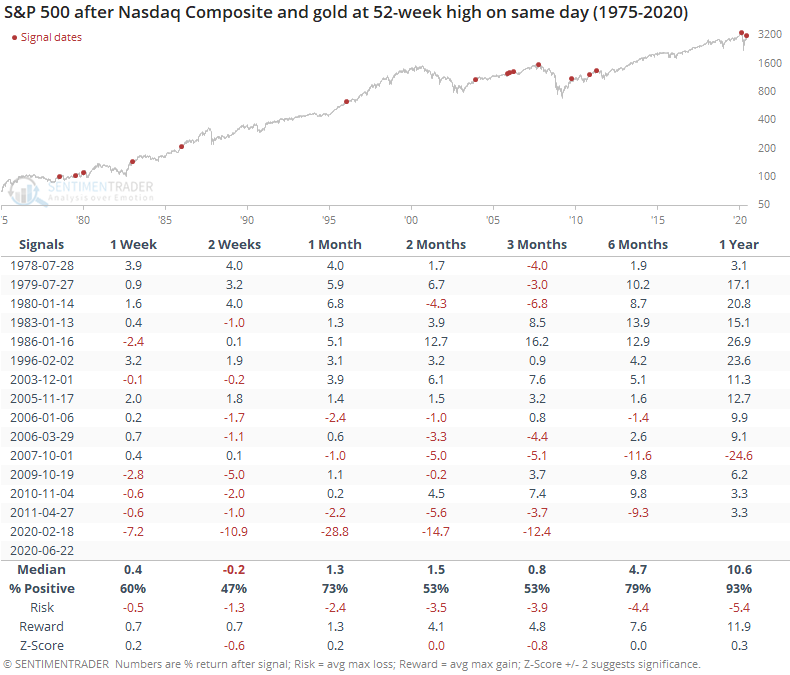

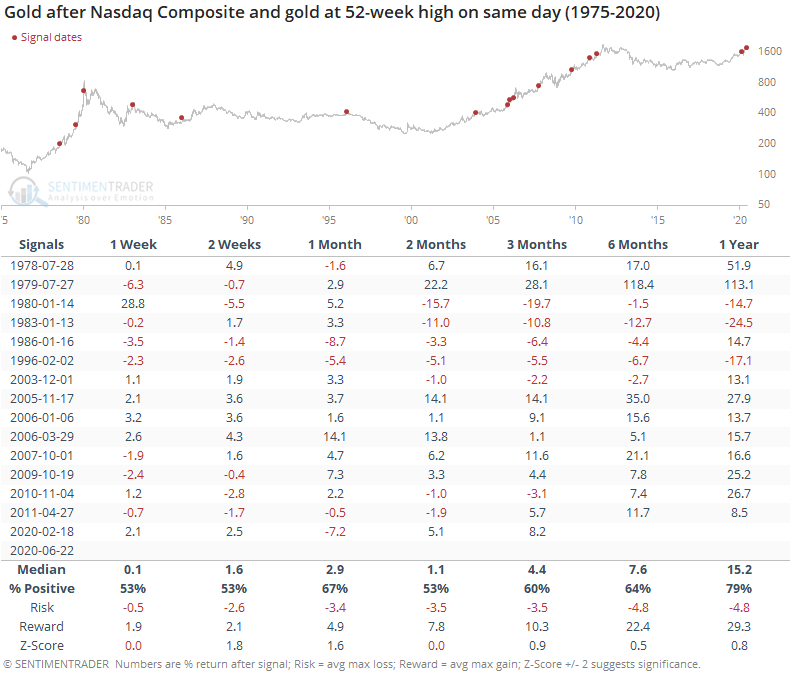

The S&P 500 is more than 3% above its 200-day average, with fewer than 45% of its stocks rising above their own averages. That hasn't happened since 2000. It's also odd that the Nasdaq hit a 52-week high on the same day as gold, a safe-haven asset. This adds to discomforting oddities triggering in the current market.

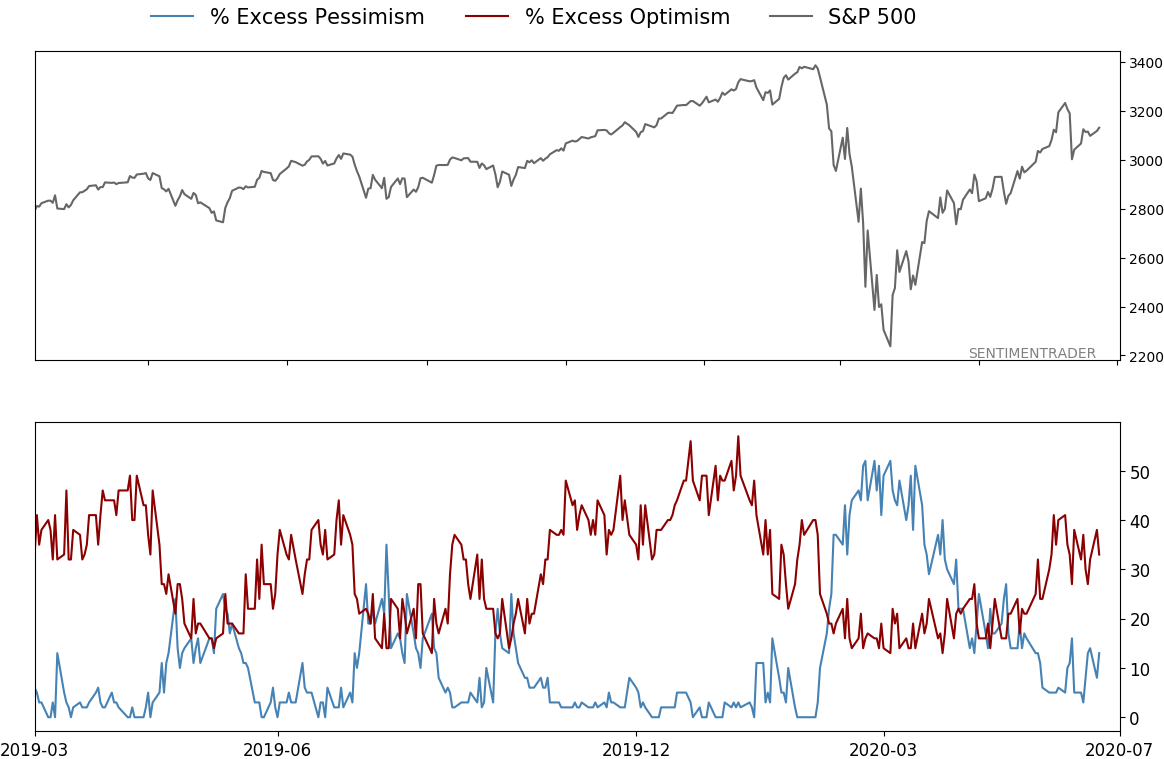

Bottom line: The suggestion is flat/lower prices short- to medium-term, and higher prices long-term. Indicators are currently showing excessive optimism, with Dumb Money Confidence was recently near 80% and has gyrated since then, during what appears to still be an unhealthy market environment. The Active Studies show that when we look at stocks from various perspectives, there is a heavy positive skew over the medium-term long-term. Recently, there have been troubling signs of reckless speculation, but the breadth thrusts and recoveries have an almost unblemished record at preceding higher prices over a 6-12 month time frame. Indicators and studies for other markets are mixed with no strong conclusion.

Wall Street wants in again: Wall Street analysts have been trying to keep up with their stocks, and failing. Over the past 10 days, they've upgraded the price targets on an average of more than 75 stocks per day. As Troy showed in a premium note, this tends to lead to a jump in volatility. According to the Backtest Engine, there have been 4 times when the 10-day average of upgrades reached this high of a level, and two months later the VIX was higher by at least 23%, and much higher in three of the cases. The dates were 2011-01-14, 2014-01-15, 2018-01-08, and 2020-01-10. They were all in January when analysts were updating their new-year forecasts.

|

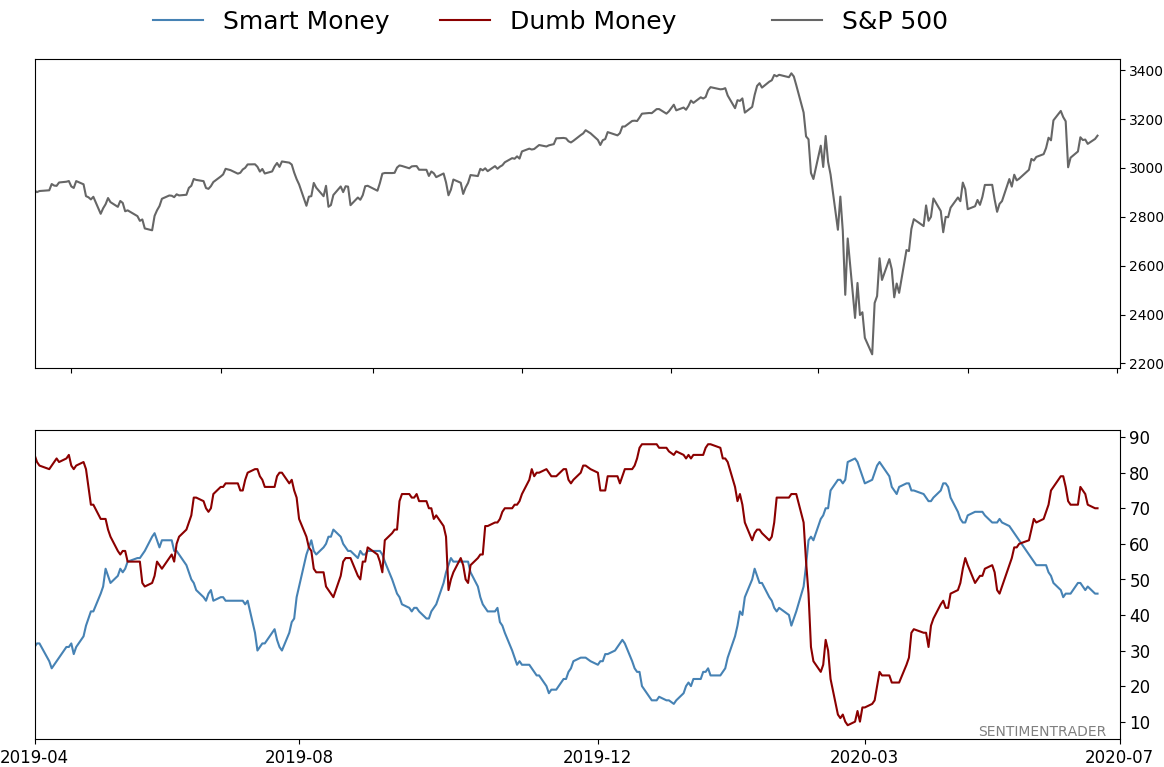

Smart / Dumb Money Confidence

|

Smart Money Confidence: 46%

Dumb Money Confidence: 70%

|

|

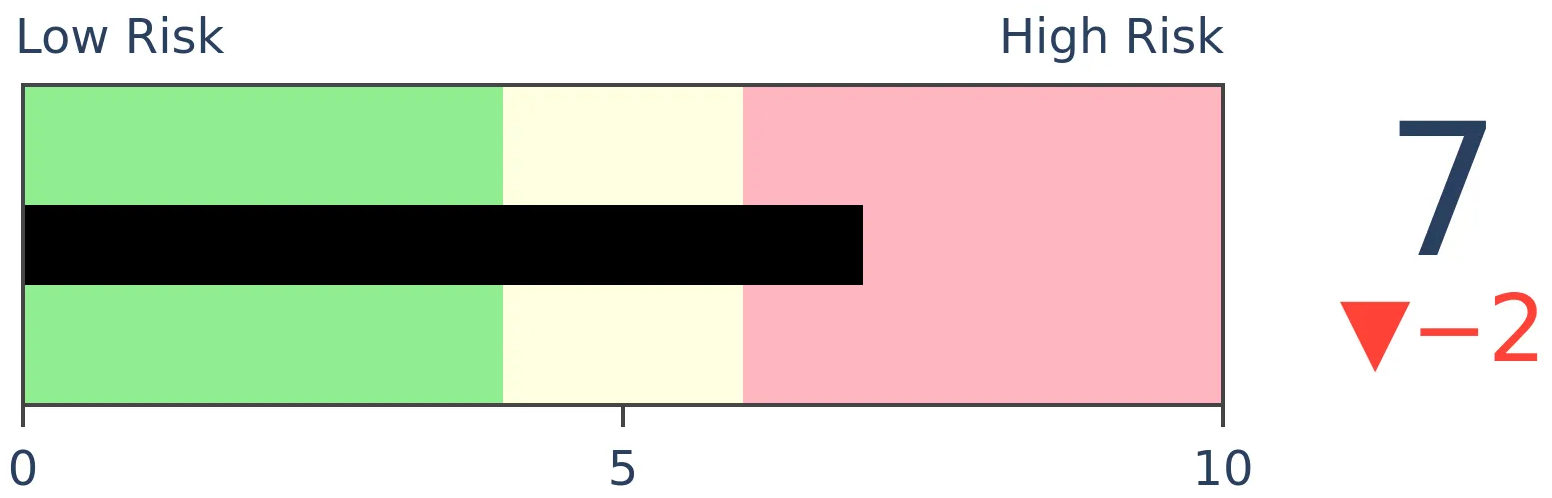

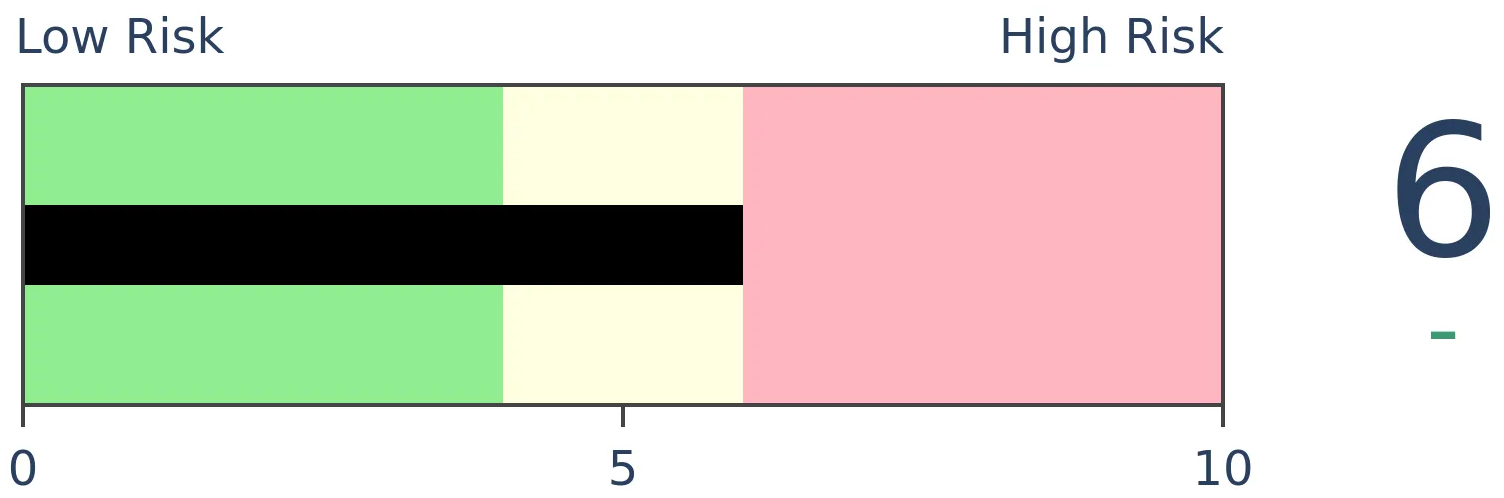

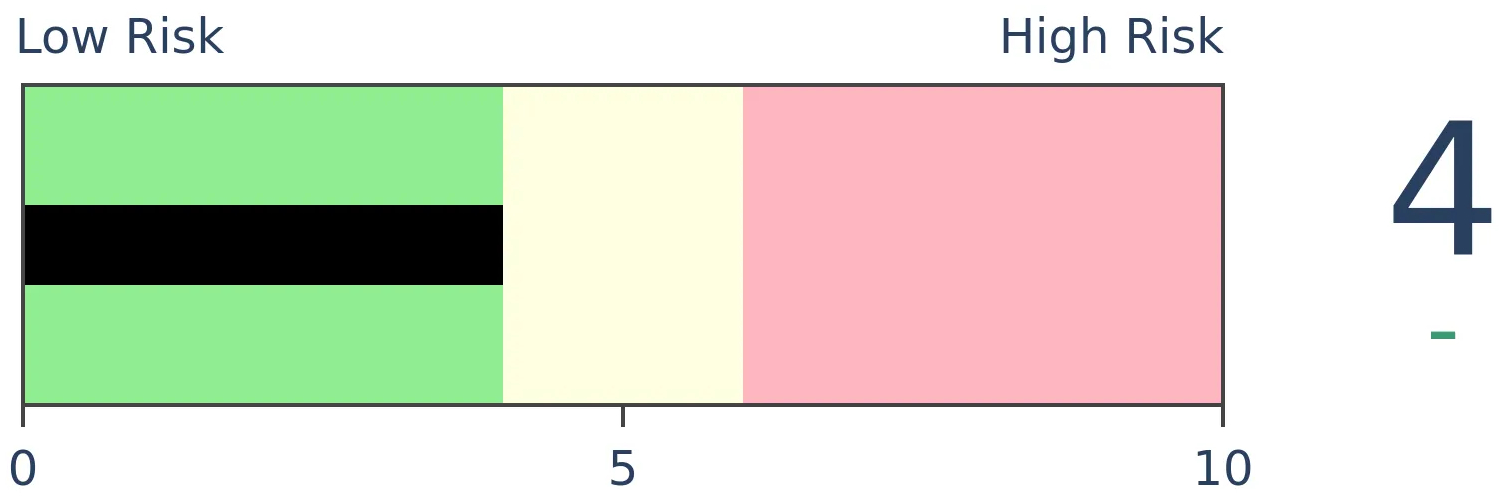

Risk Levels

Stocks Short-Term

|

Stocks Medium-Term

|

|

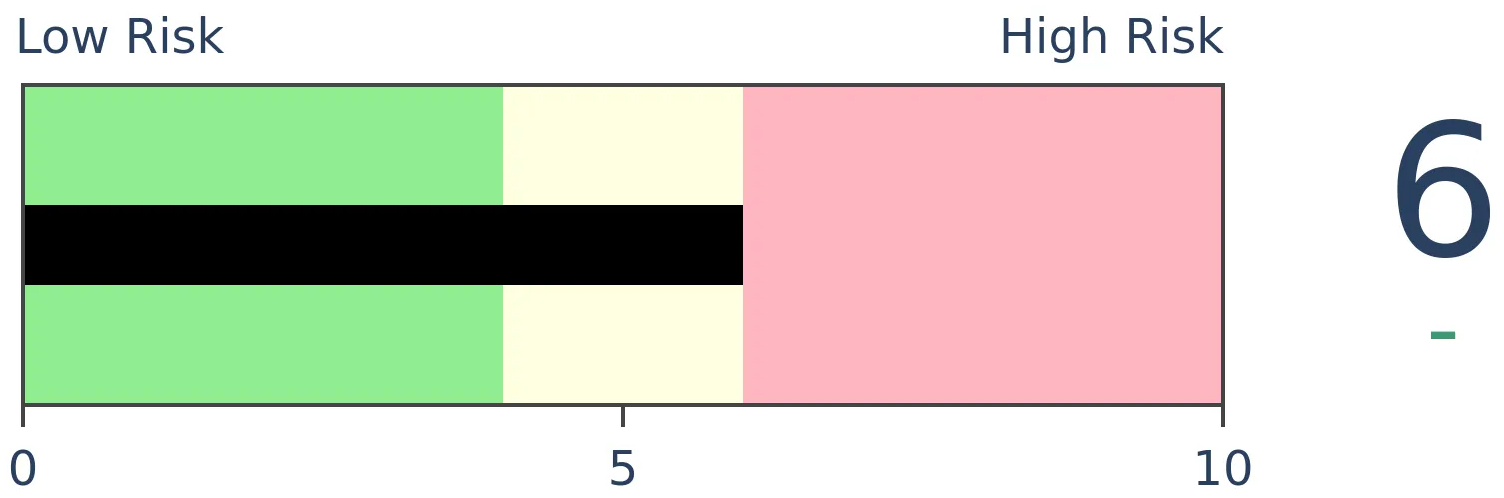

Bonds

|

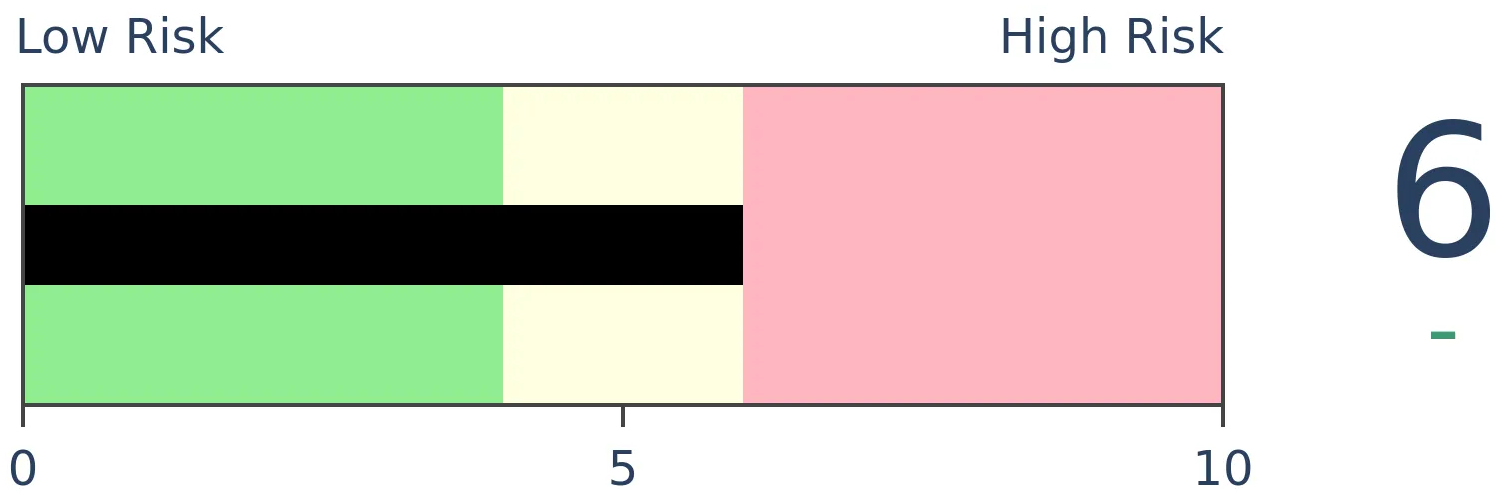

Crude Oil

|

|

Gold

|

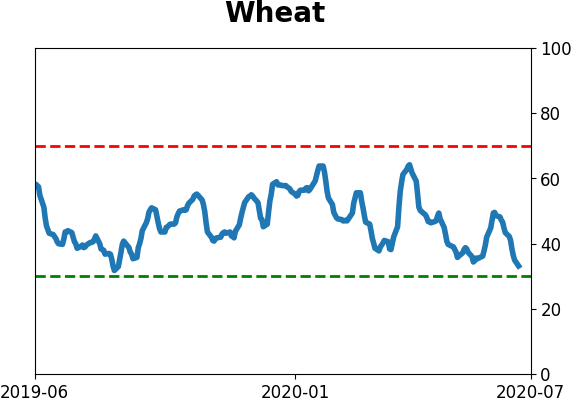

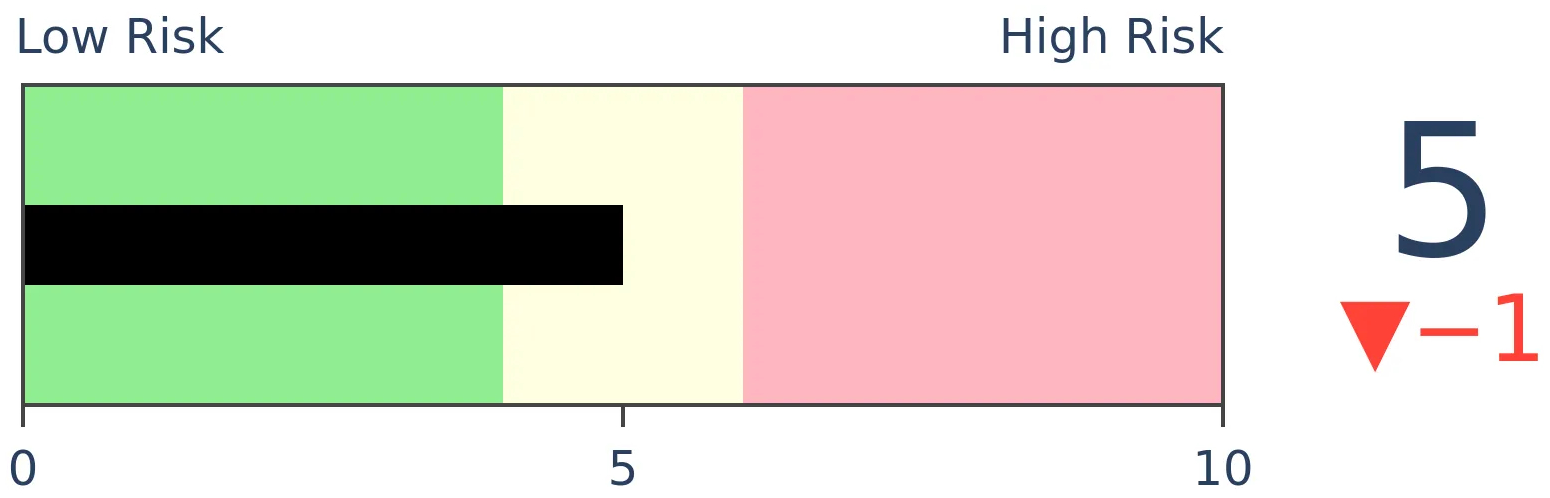

Agriculture

|

|

Research

BOTTOM LINE

This quarter has been among the very best in market history. Since 1928, this currently ranks in the top 10 of all quarters. When we look at how the S&P has fared up to the last week of each quarter, we can see a negative correlation with the return during the last week, potentially a result of rebalancing activity.

FORECAST / TIMEFRAME

None

|

We're nearing the last week of the quarter, and what a quarter it has been. The S&P 500 is on track for a nearly 20% gain, ranking in the top 10 out of 369 quarters since 1928.

We've looked at the concept of window dressing in the past, with inconclusive results. This is the theory that since stocks have done so well during the quarter, funds have an incentive to add to their stock positions before quarter-end, in order to show investors that they're invested.

Like most things market-related, it sounds good in theory, but empirical evidence is almost nonexistent. It might occur in some individual stocks, but for the market as a whole, it's mostly a non-factor.

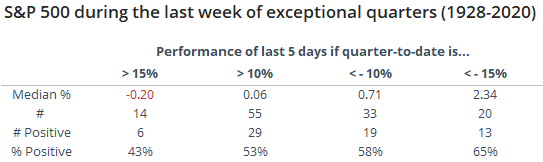

The chart below shows every quarter since 1928. The x-axis is the S&P's return for the quarter, up to the last week of the quarter. The y-axis is the return during that last week of the quarter.

The correlation between them is essentially zero. It's slightly negative but not enough to consider it any kind of edge.

That includes all quarters, even the meek ones. If we restrict our look to the most exceptional quarters - and this is surely one of them - then we can see a bit more of a pattern.

If the S&P had rallied 15% or more up to the last week of a quarter, then that last week returned a median -0.2% and was positive 43% of the time. That's fairly week given an overall positive bias during the study period. Theoretically, if investors are rotating out of stocks near the end of good quarters, then they should be rotating into bonds. And there was some evidence of that - the Bloomberg Barclays U.S. Aggregate Bond Index averaged a return of 0.4% during those weeks and was higher 81% of the time since 1989.

If the S&P had dropped 15% or more during a quarter, then there was a pretty strong bullish bias during the last week, returning a whopping 2.3% on average. That's an enormous return for only a week's worth of work. The Bloomberg bond index averaged a return of 0.2% during these weeks and was higher 64% of the time.

Given the strong rally this quarter, and the (small) inverse correlation between quarter-to-date and last-week returns, it would suggest a minor negative short-term bias for the coming week, potentially as large funds rebalance their asset allocation.

BOTTOM LINE

The S&P 500 is more than 3% above its 200-day average, with fewer than 45% of its stocks rising above their own averages. That hasn't happened since 2000. It's also odd that the Nasdaq hit a 52-week high on the same day as gold, a safe-haven asset. This adds to discomforting oddities triggering in the current market.

FORECAST / TIMEFRAME

None

|

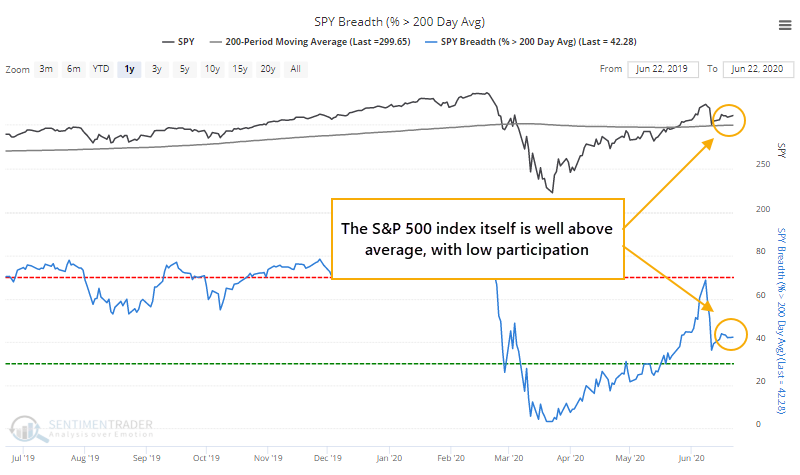

The Nasdaq keeps rallying, the S&P 500 has moved well above its 200-day moving average, and yet relatively few stocks seem to be coming along for the ride.

As Troy showed in a premium note, the Nasdaq Composite has rallied 7 days in a row, while fewer than 45% of stocks in the S&P 500 have moved above their 200-day moving averages. That hasn't happened since the year 2000.

The S&P itself moved to more than 3% above its 200-day average, and yet less than half of stocks within the index have managed to climb above their own averages. As we saw last week, this is a theme across industries, sectors, and world indexes.

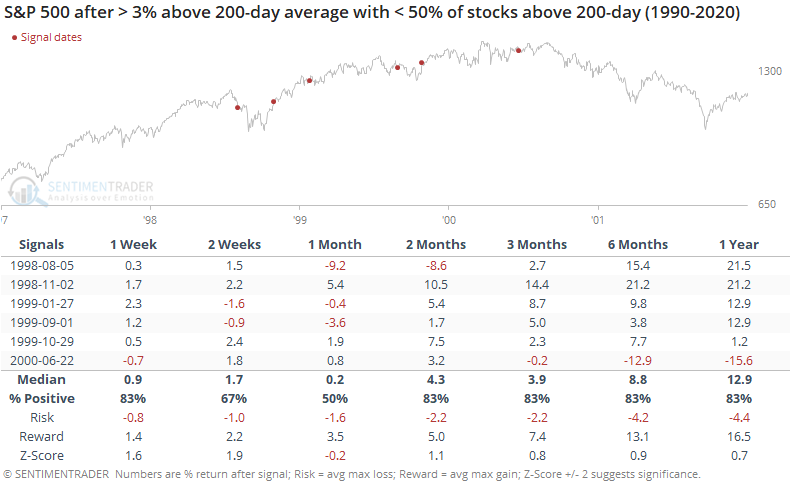

The last time that happened was also in the year 2000. Since 1990, the only signals were from 1998 through 2000.

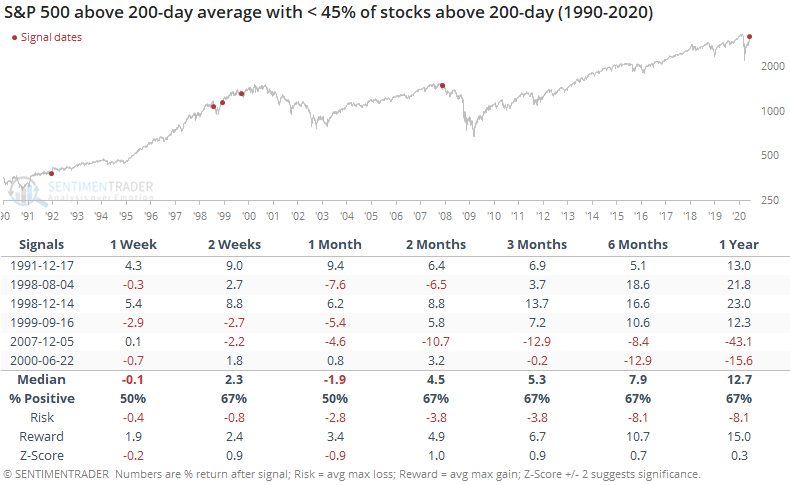

If the S&P was above its 200-day average by any amount, while fewer than 45% of its members were above their averages, then that only happened in 2007, and 1999 prior to that.

It's curious that this streak in the Nasdaq is occurring simultaneously with gold. Typically, the latter is considered a safe haven, more likely to rise when stocks are volatile.

Over the past 15 years, this led to consistently negative short- to medium-term returns in the Nasdaq, but not so much prior to that.

For the S&P, it also tended to be a short- to medium-term negative over the past 15 years. The risk/reward was unimpressive up to three months later.

For gold, it was a mixed sign, but kind of the opposite of that in the Nasdaq and S&P. Up to the last 15 years, it was mostly negative over the short-term medium-term, and mostly positive since then.

Oddities like this started building in late 2019, and it took months before any potential consequences. The above studies don't suggest an immediate worry, as the future returns were too inconsistent to suggest "sell." But periods of rising index prices and high optimism, during markets where relatively few stocks are in long-term uptrends, have a strong tendency to resolve lower in the weeks-to-months ahead. Seeing some safe-haven assets rally along with stocks adds to the discomfort.

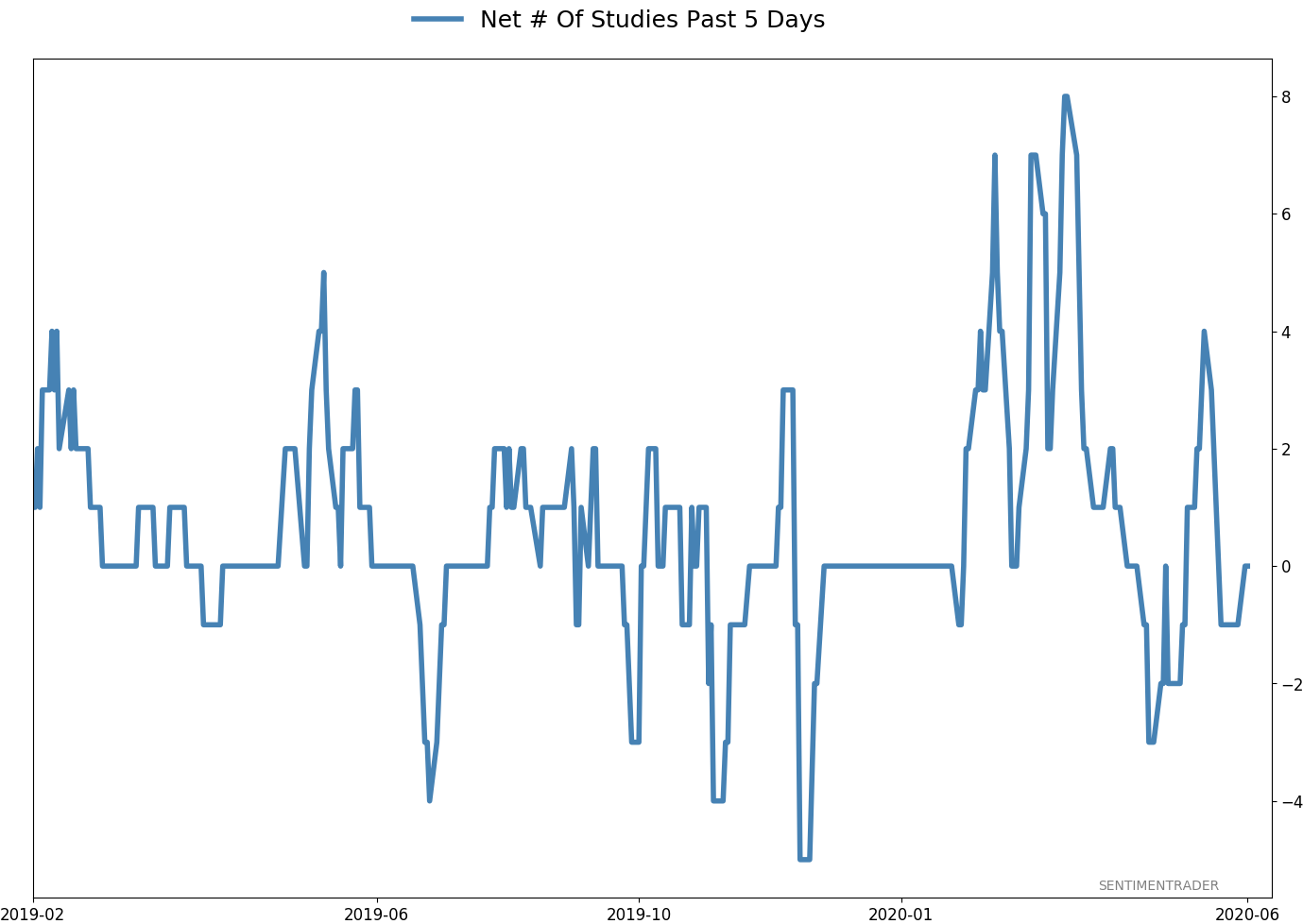

Active Studies

| Time Frame | Bullish | Bearish | | Short-Term | 0 | 1 | | Medium-Term | 8 | 6 | | Long-Term | 40 | 1 |

|

Indicators at Extremes

Portfolio

| Position | Weight % | Added / Reduced | Date | | Stocks | 29.8 | Reduced 9.1% | 2020-06-11 | | Bonds | 0.0 | Reduced 6.7% | 2020-02-28 | | Commodities | 5.2 | Added 2.4%

| 2020-02-28 | | Precious Metals | 0.0 | Reduced 3.6% | 2020-02-28 | | Special Situations | 0.0 | Reduced 31.9% | 2020-03-17 | | Cash | 65.0 | | |

|

Updates (Changes made today are underlined)

In the first months of the year, we saw manic trading activity. From big jumps in specific stocks to historic highs in retail trading activity to record highs in household confidence to almost unbelievable confidence among options traders. All of that came amid a market where the average stock couldn't keep up with their indexes. There were signs of waning momentum in stocks underlying the major averages, which started triggering technical warning signs in late January. After stocks bottomed on the 23rd, they enjoyed a historic buying thrust and retraced a larger amount of the decline than "just a bear market rally" tends to. Those thrusts are the most encouraging sign we've seen in years. Through early June, we were still seeing thrusts that have led to recoveries in longer-term breadth metrics. The longer-term prospects for stocks (6-12 months) still look decent given the above. On a short- to medium-term basis, it was getting harder to make that case. Dumb Money Confidence spiked and there were multiple signs of a historic level of speculation. Given that, I reduced my exposure a bit when stocks gapped down and failed to hold the lows of late last week. This is likely the lowest I will go given what I still consider to be compelling positives over a longer time frame. There is not a slam-dunk case to be made for either direction, so it will seem like a mistake whether stocks keep dropping (why didn't I sell more?) or if they turn and head higher (why did I let short-term concerns prevail?). After nearly three decades of trading, I've learned to let go of the idea of perfection.

RETURN YTD: -5.8% 2019: 12.6%, 2018: 0.6%, 2017: 3.8%, 2016: 17.1%, 2015: 9.2%, 2014: 14.5%, 2013: 2.2%, 2012: 10.8%, 2011: 16.5%, 2010: 15.3%, 2009: 23.9%, 2008: 16.2%, 2007: 7.8%

|

|

Phase Table

Ranks

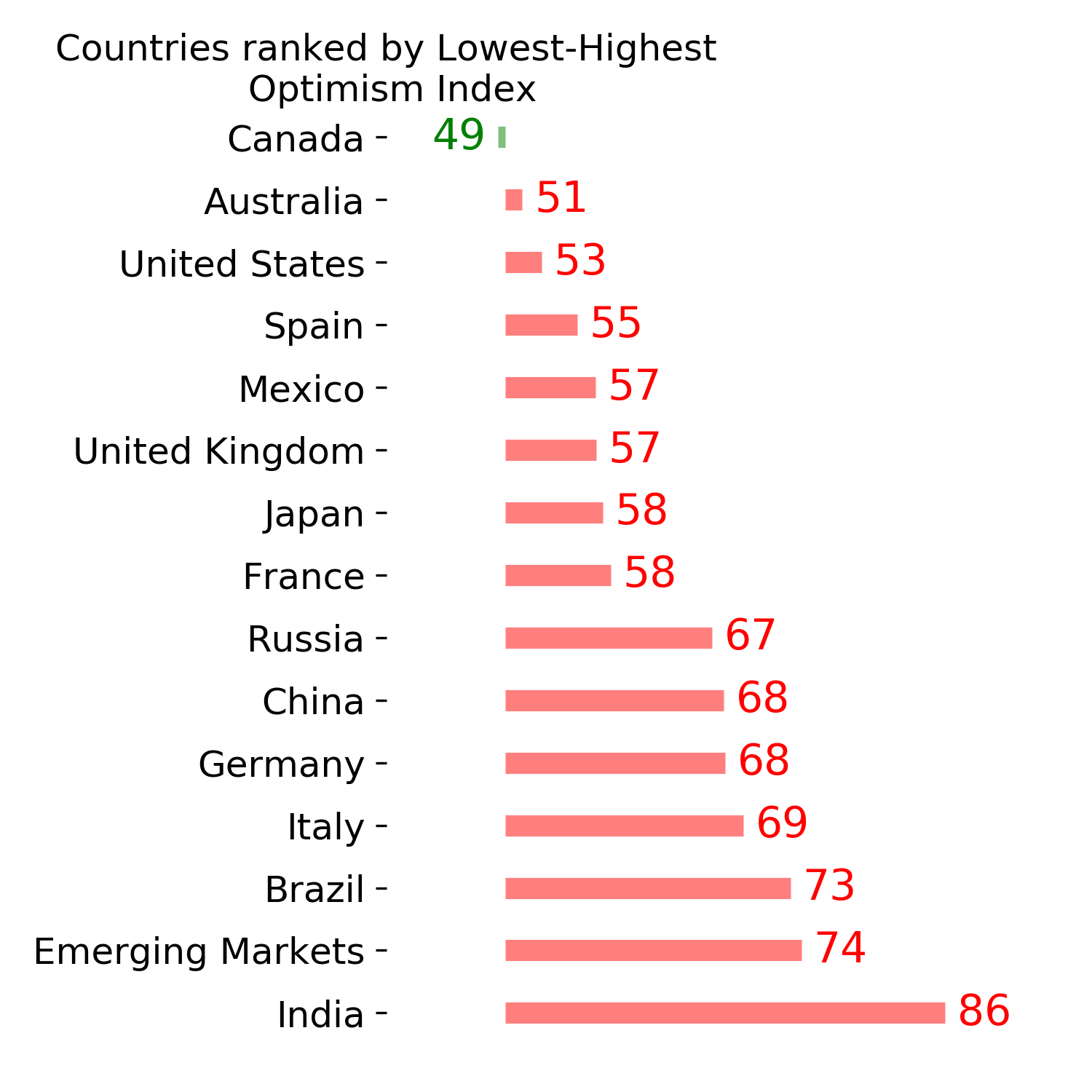

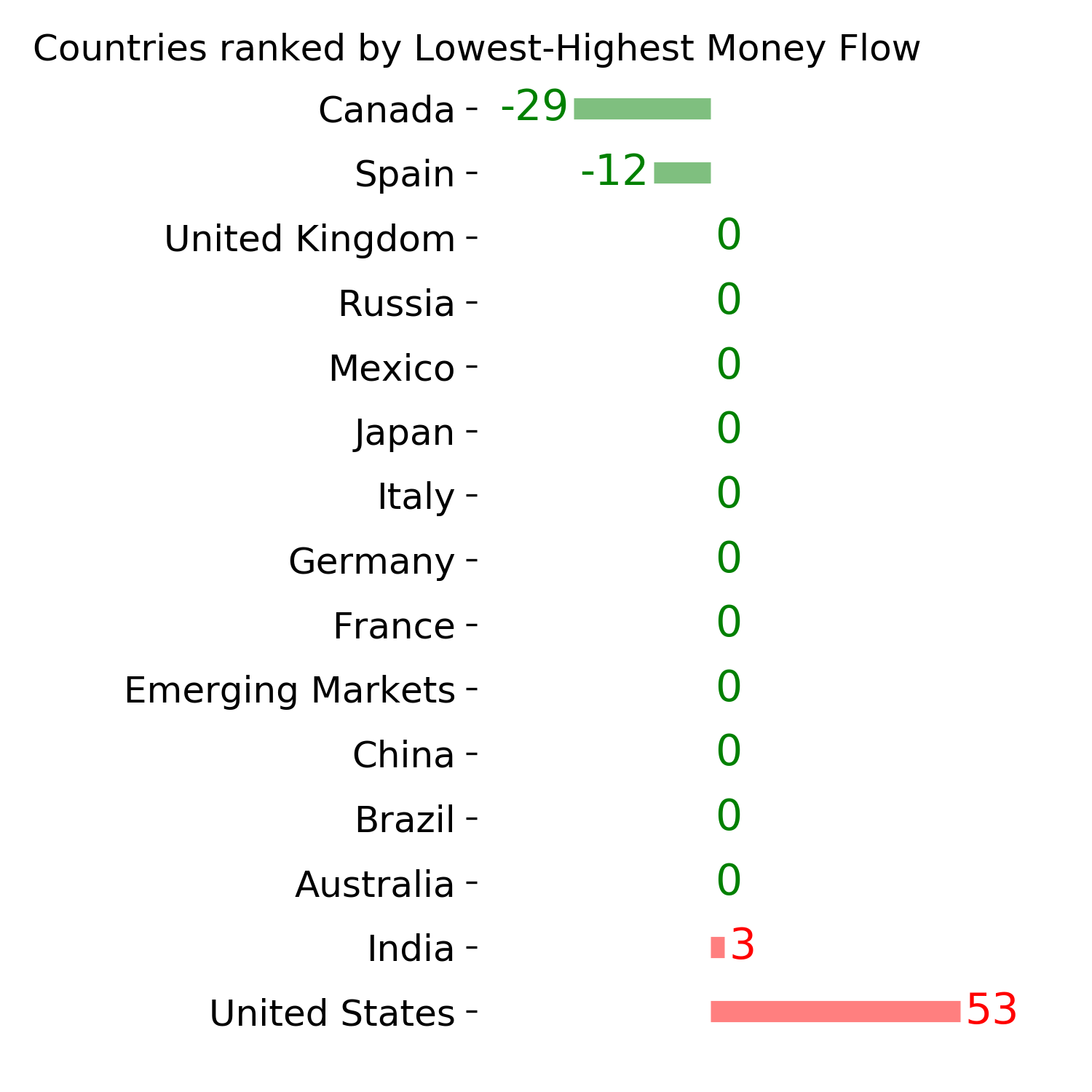

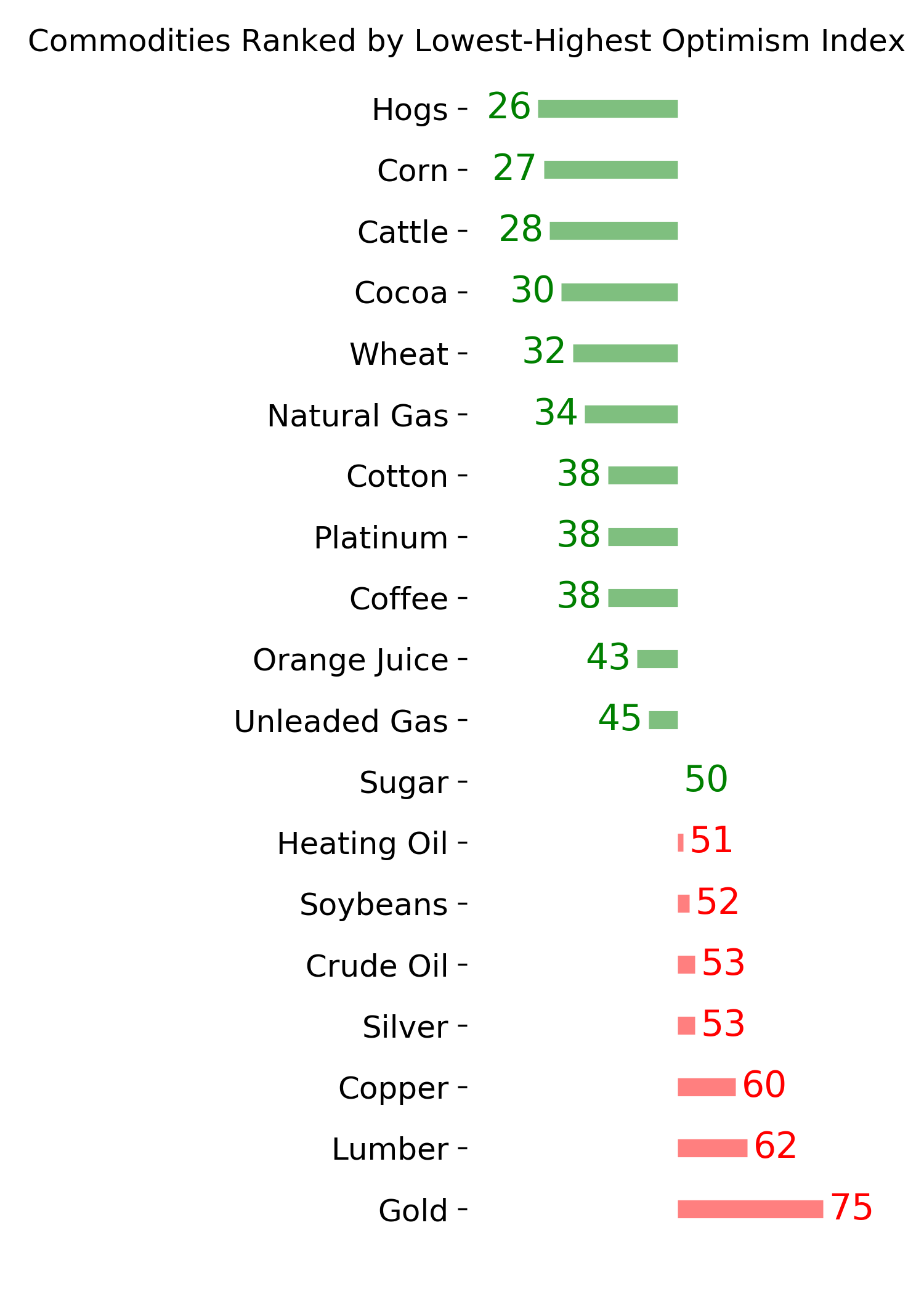

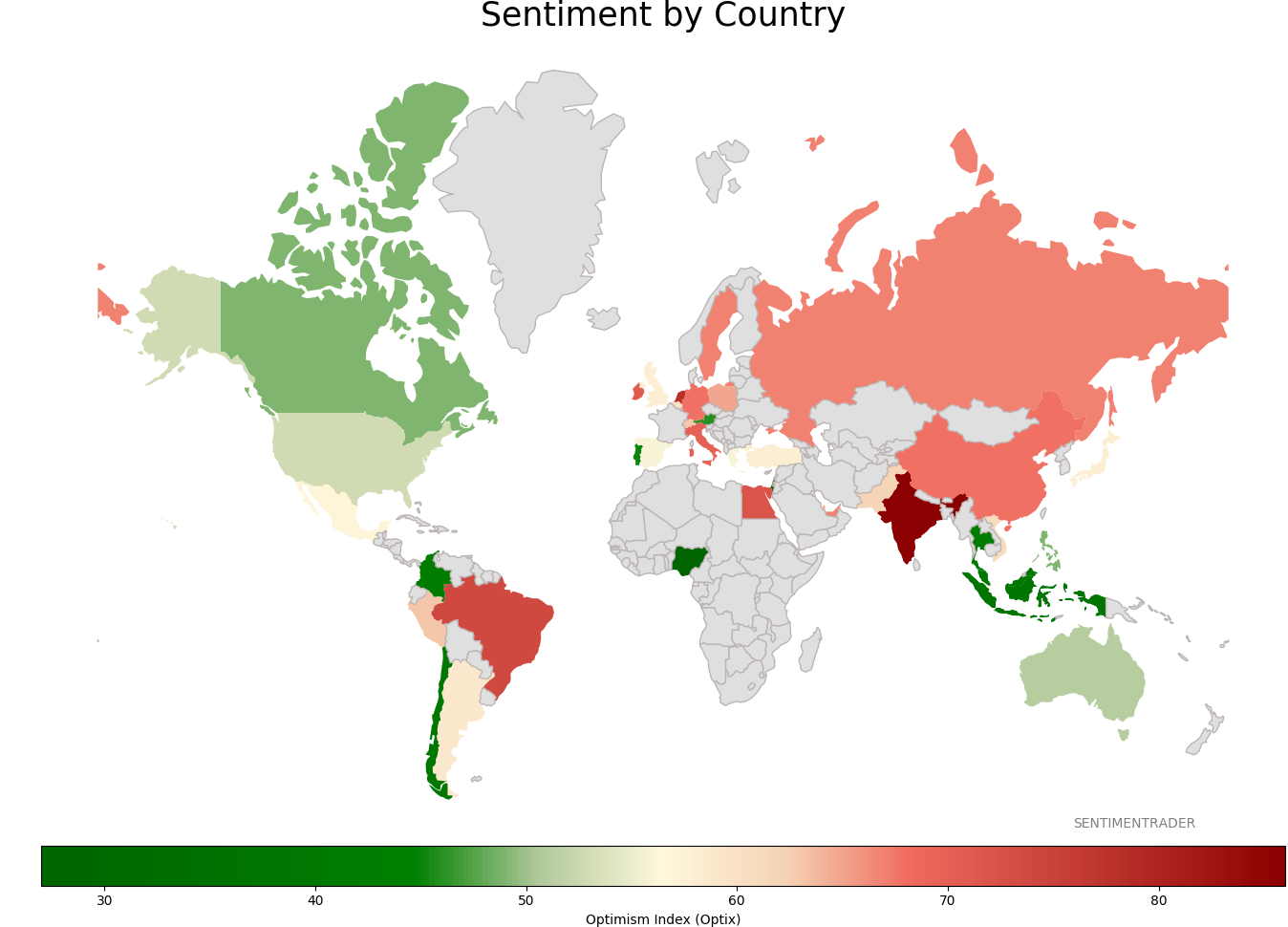

Sentiment Around The World

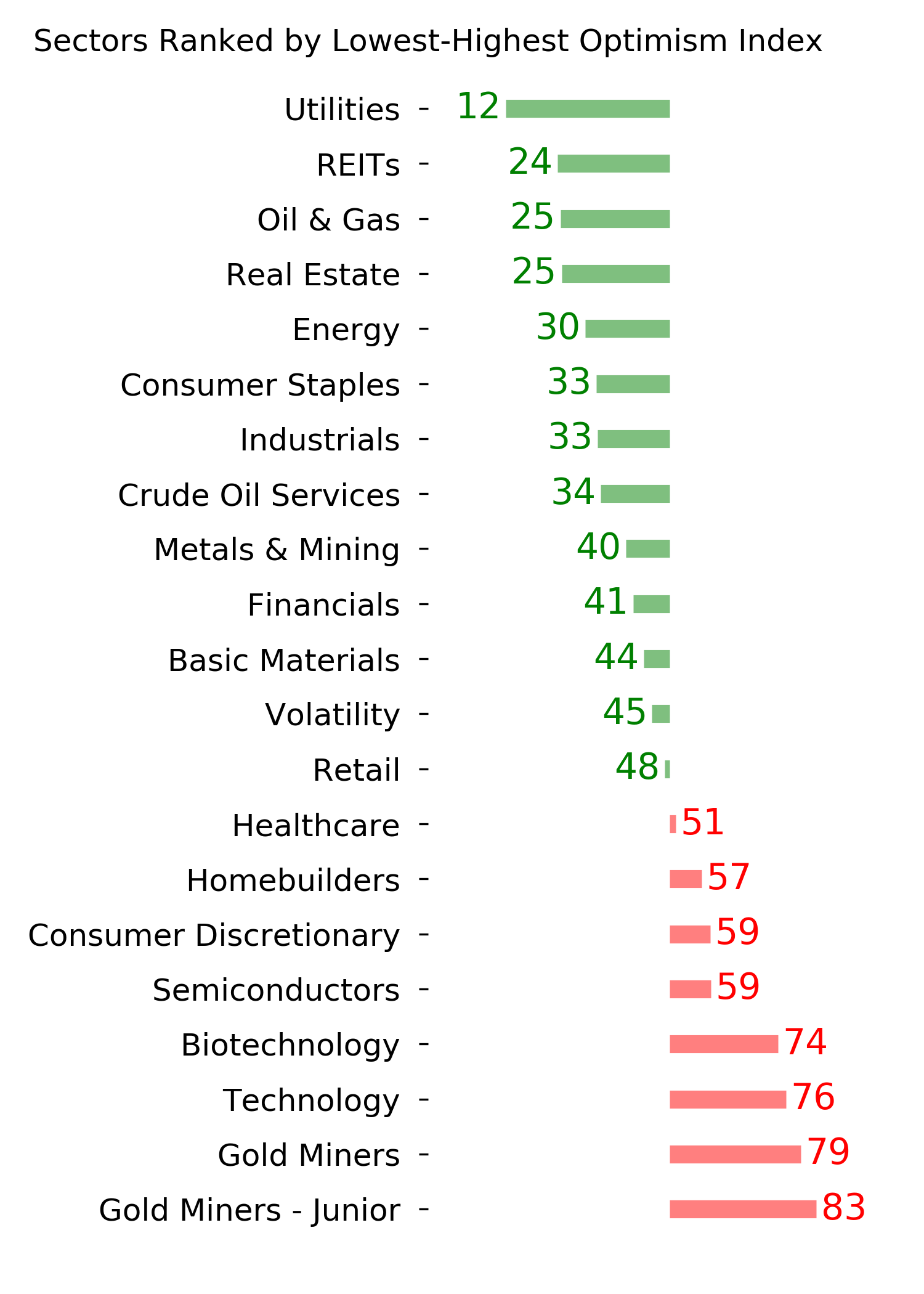

Optimism Index Thumbnails

|

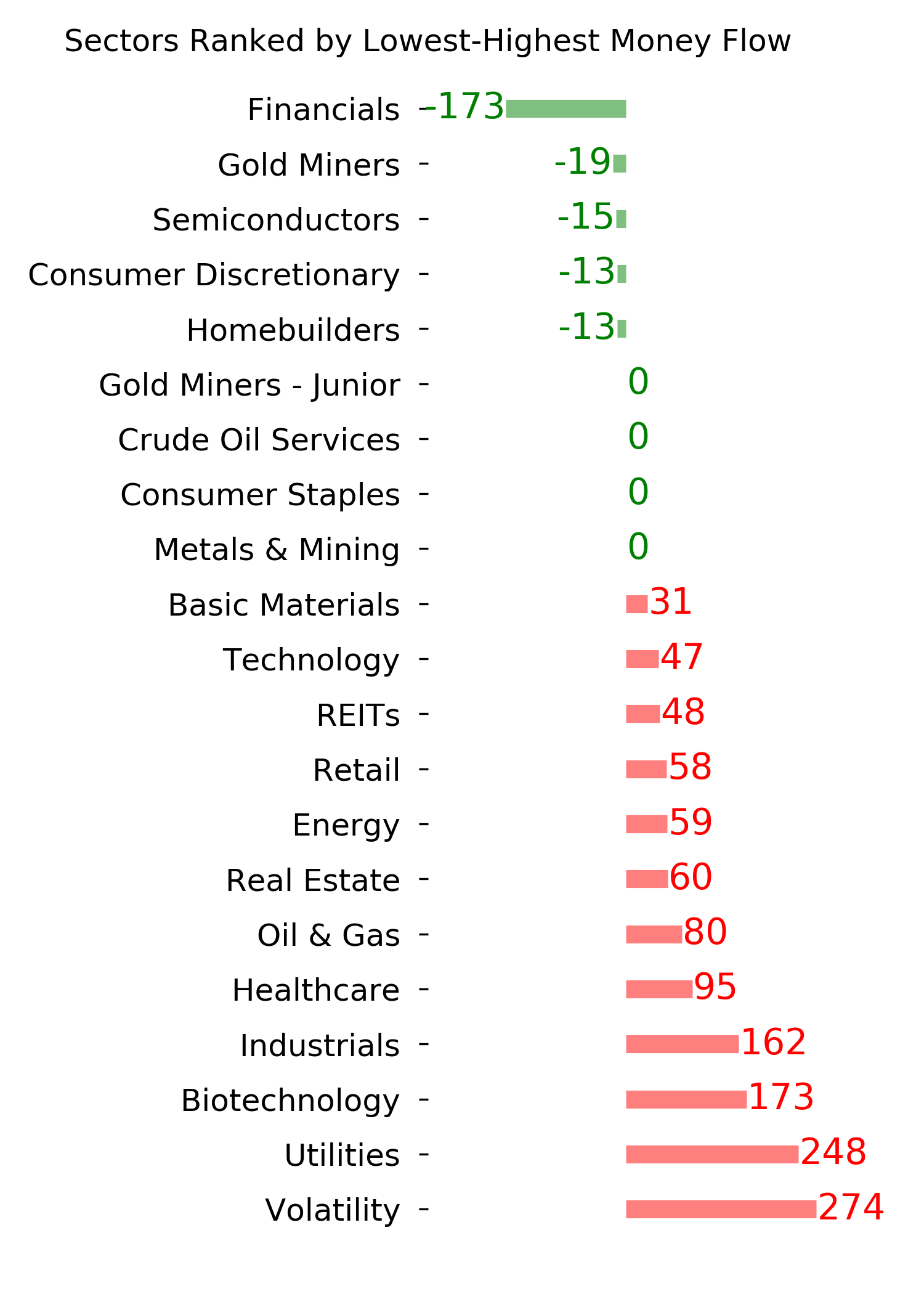

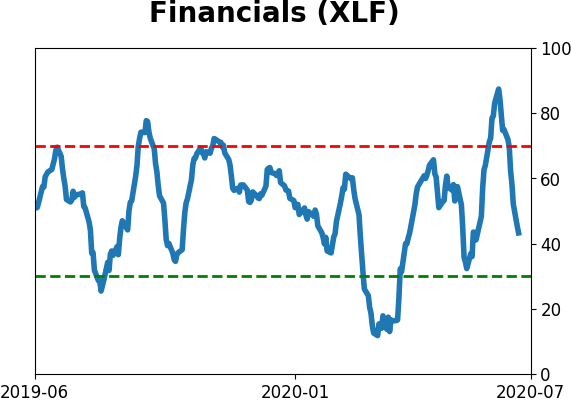

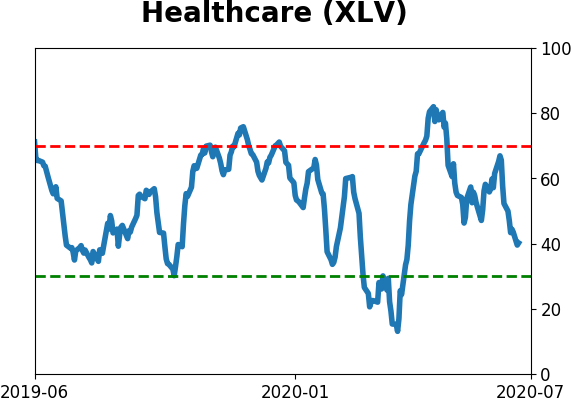

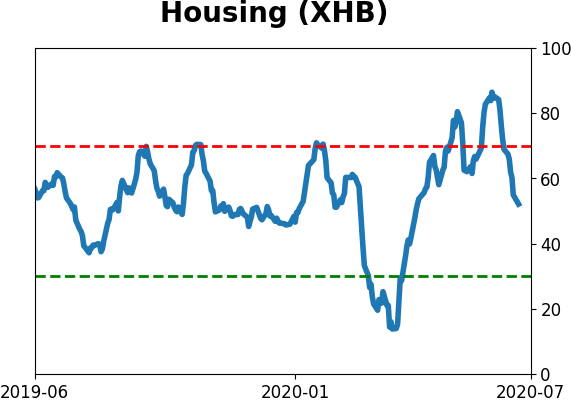

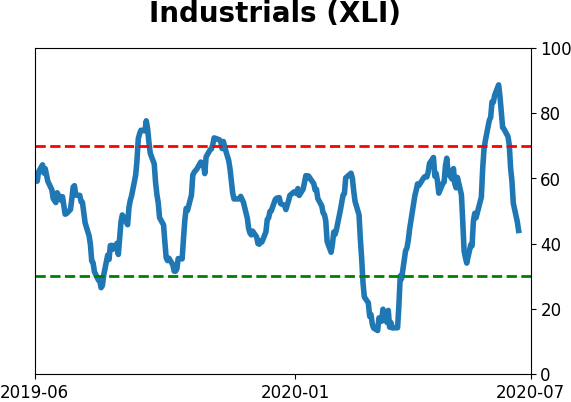

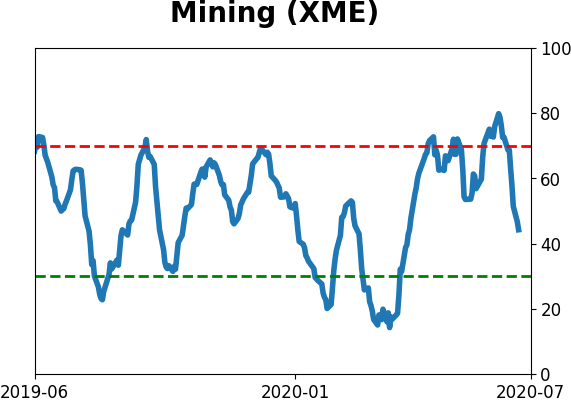

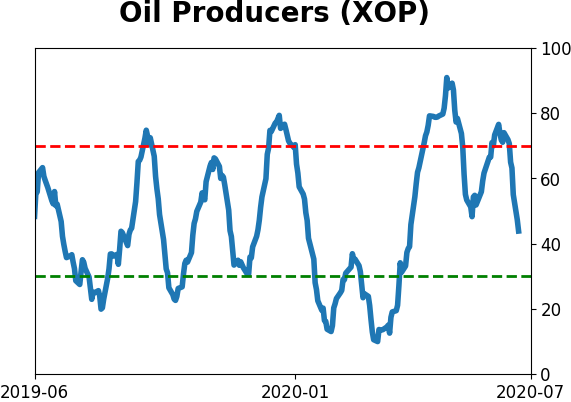

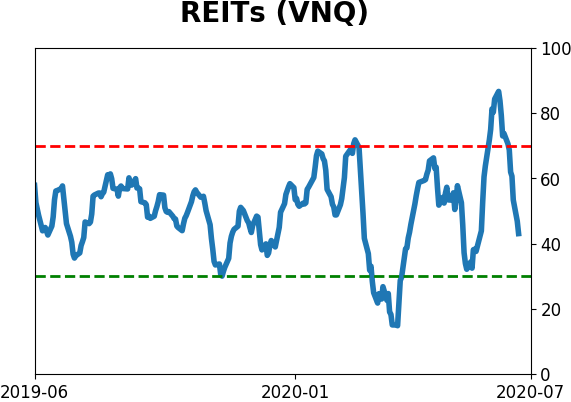

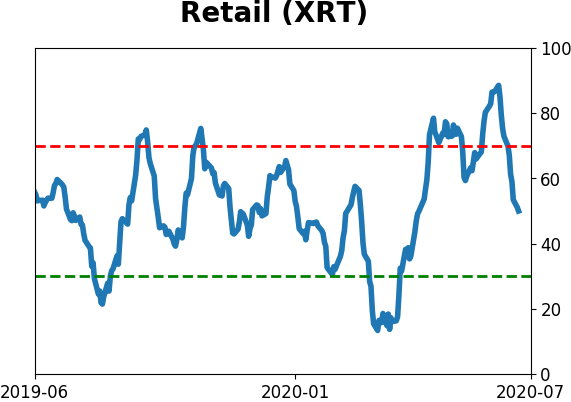

Sector ETF's - 10-Day Moving Average

|

|

|

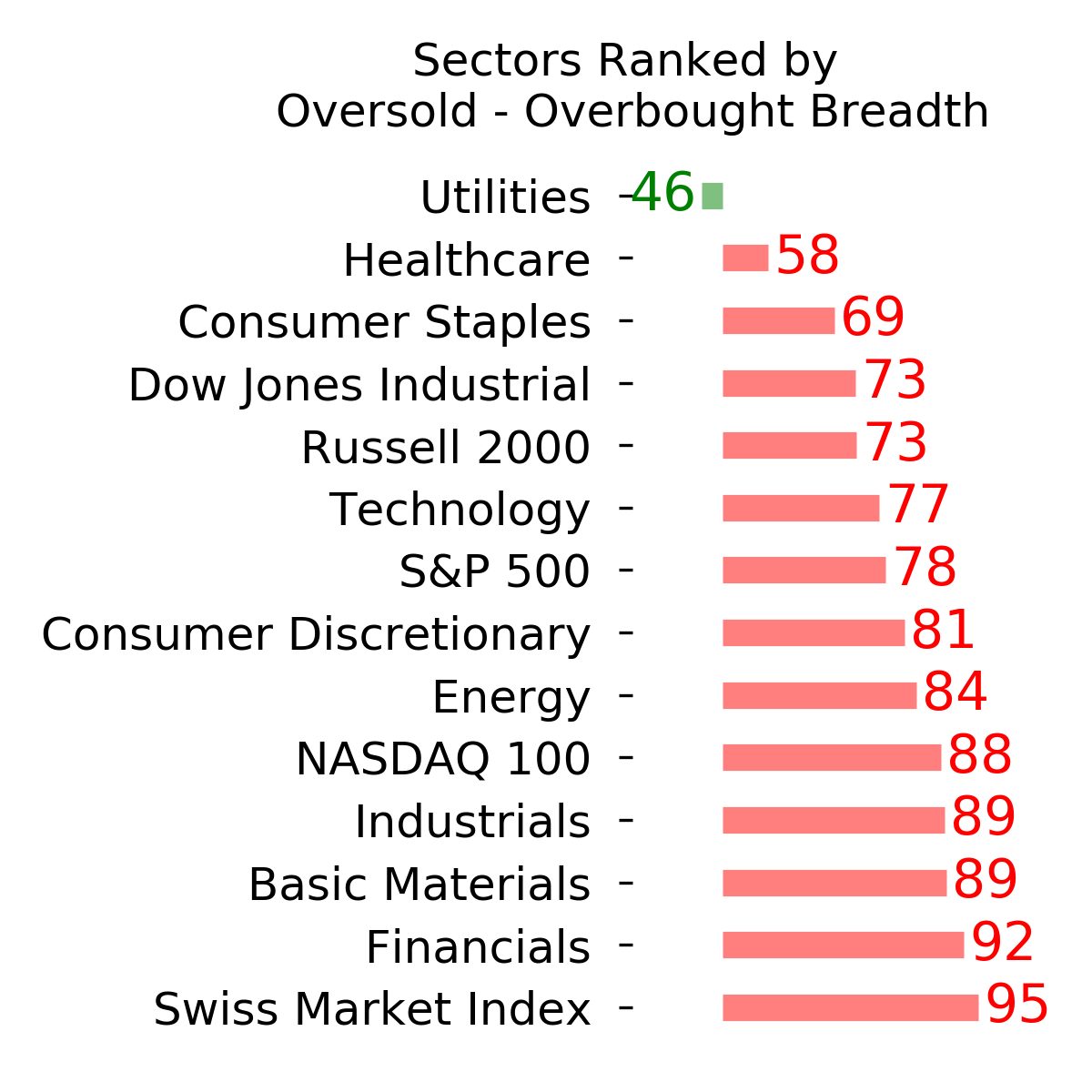

Country ETF's - 10-Day Moving Average

|

|

|

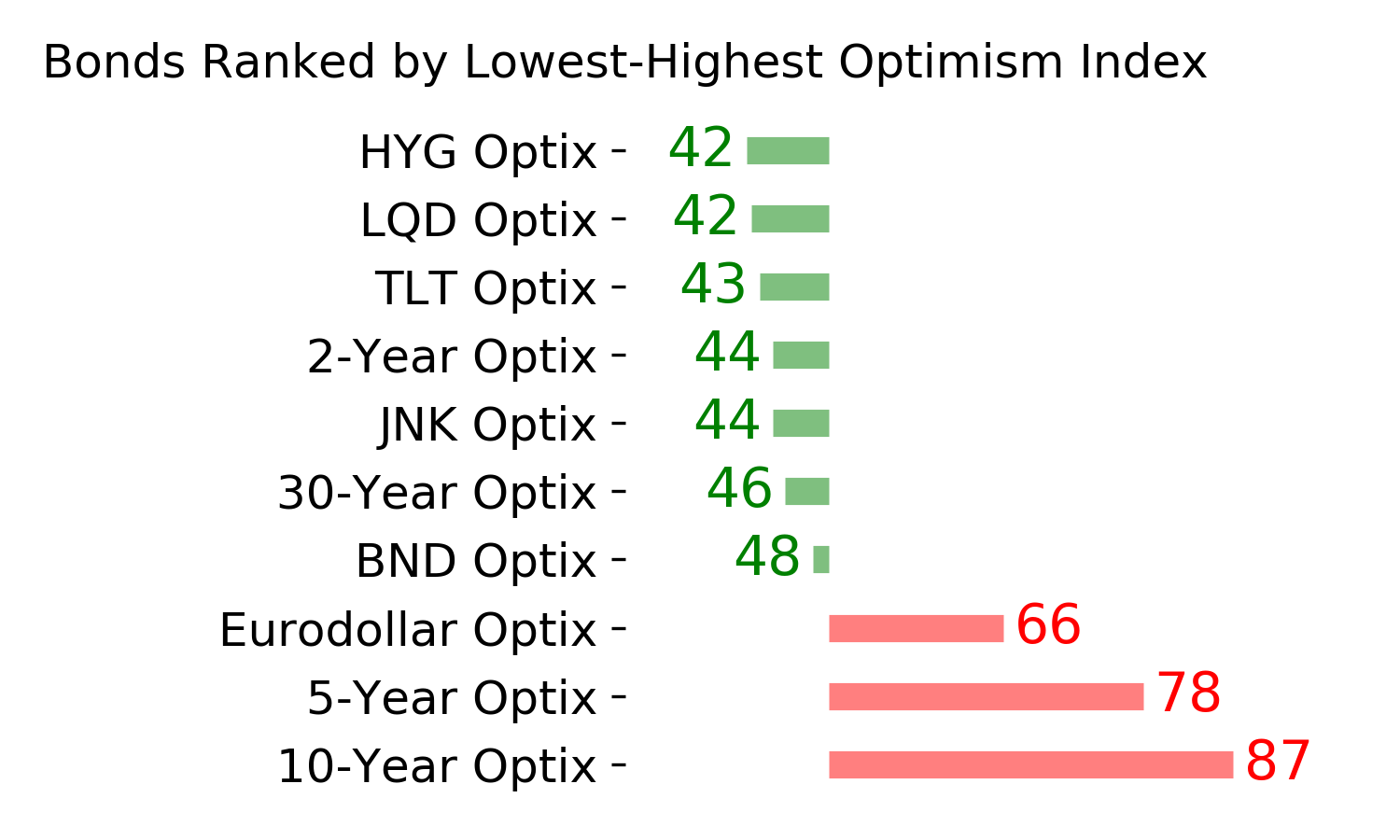

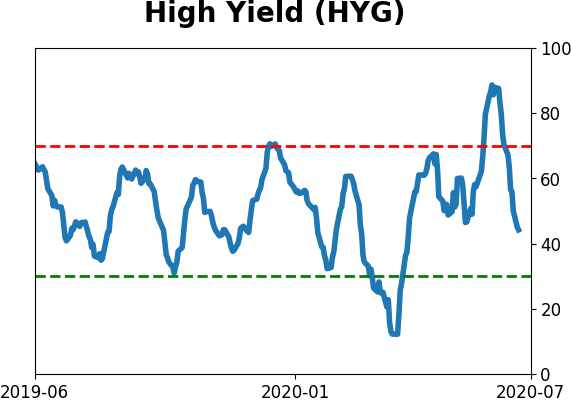

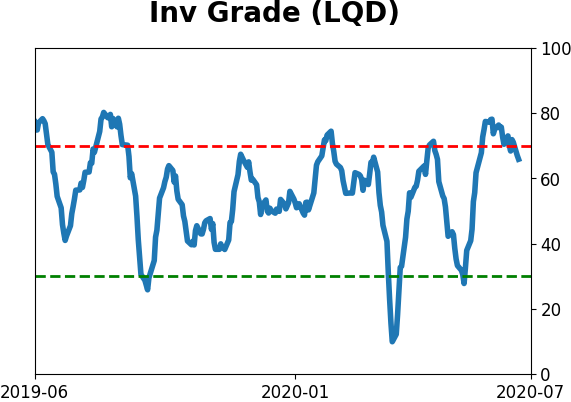

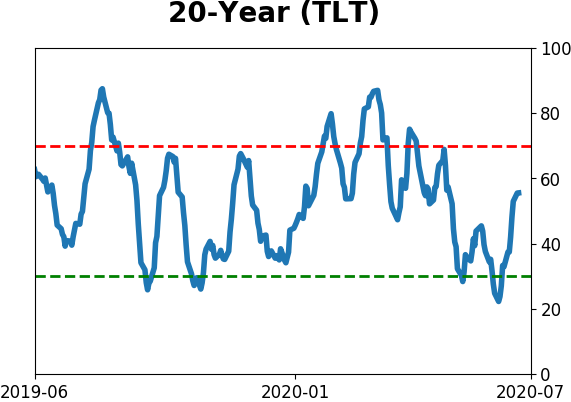

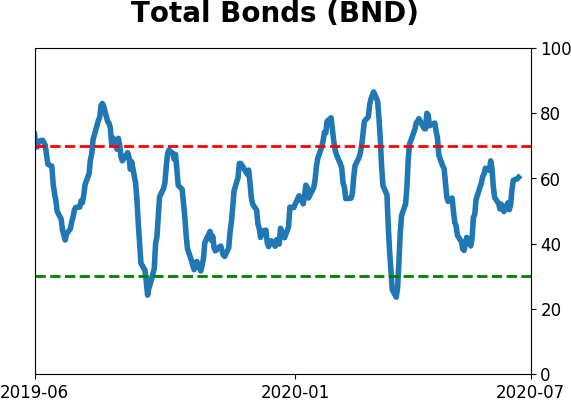

Bond ETF's - 10-Day Moving Average

|

|

|

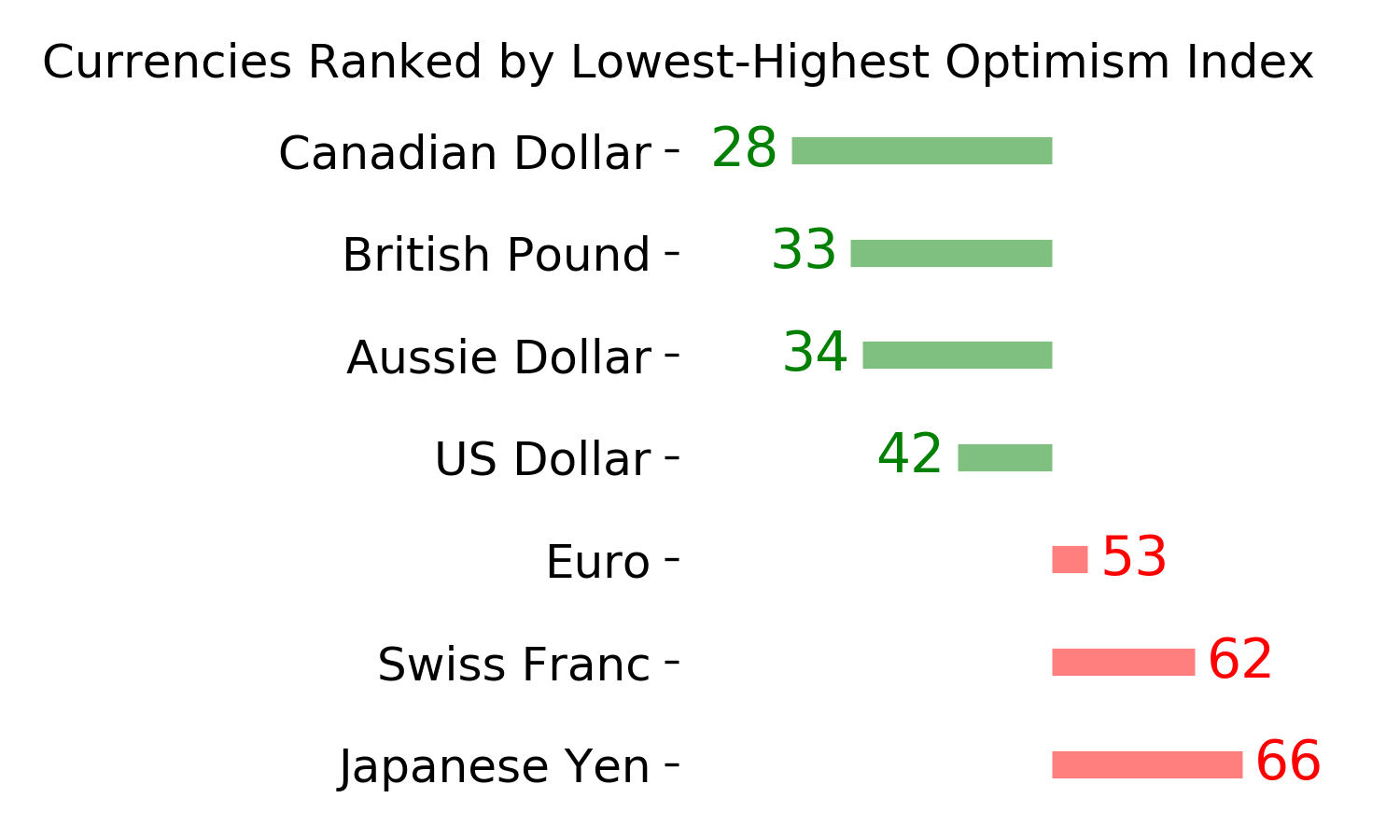

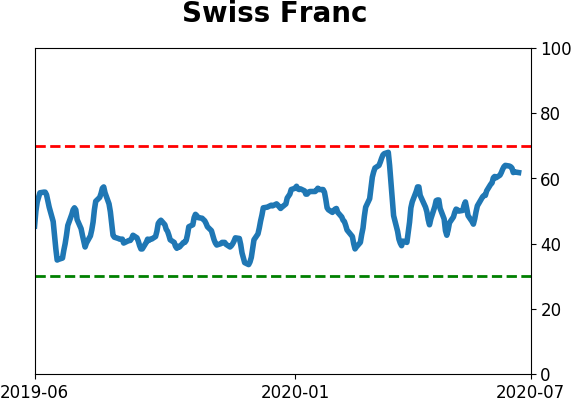

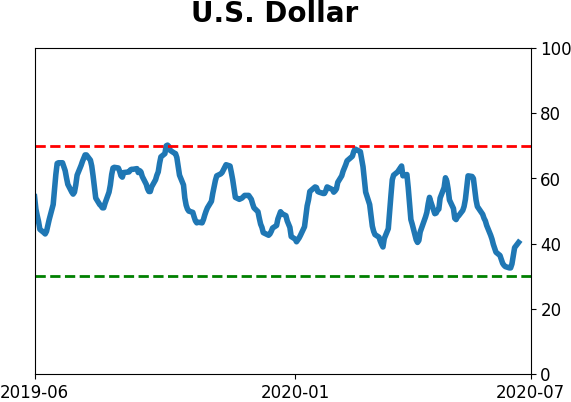

Currency ETF's - 5-Day Moving Average

|

|

|

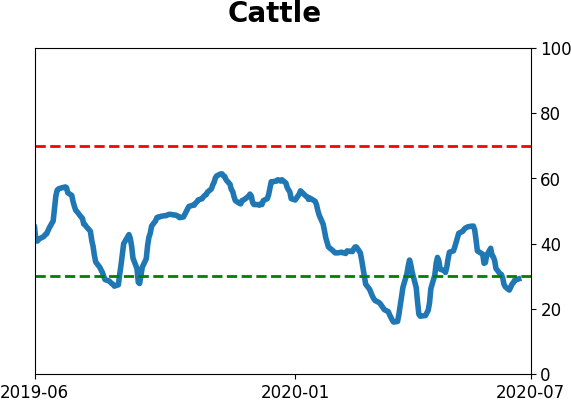

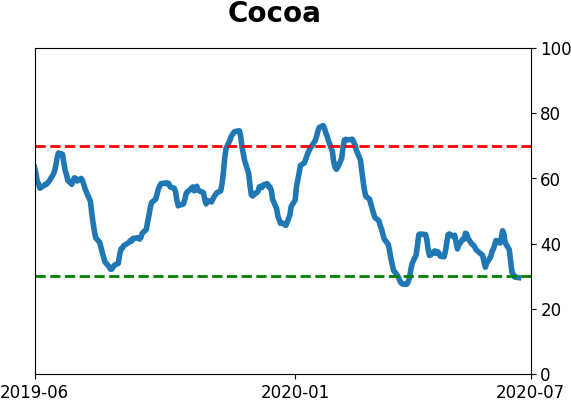

Commodity ETF's - 5-Day Moving Average

|

|