Headlines

|

|

Bond sentiment is starting to recover:

Over the past few months, pessimism toward the bond market reached extreme levels. That has started to ease as the selling pressure let up in recent weeks. Similar behavior typically led to multi-month gains in Treasuries, but with the biggest caveat being limited data under what may be the most comparable market environments.

|

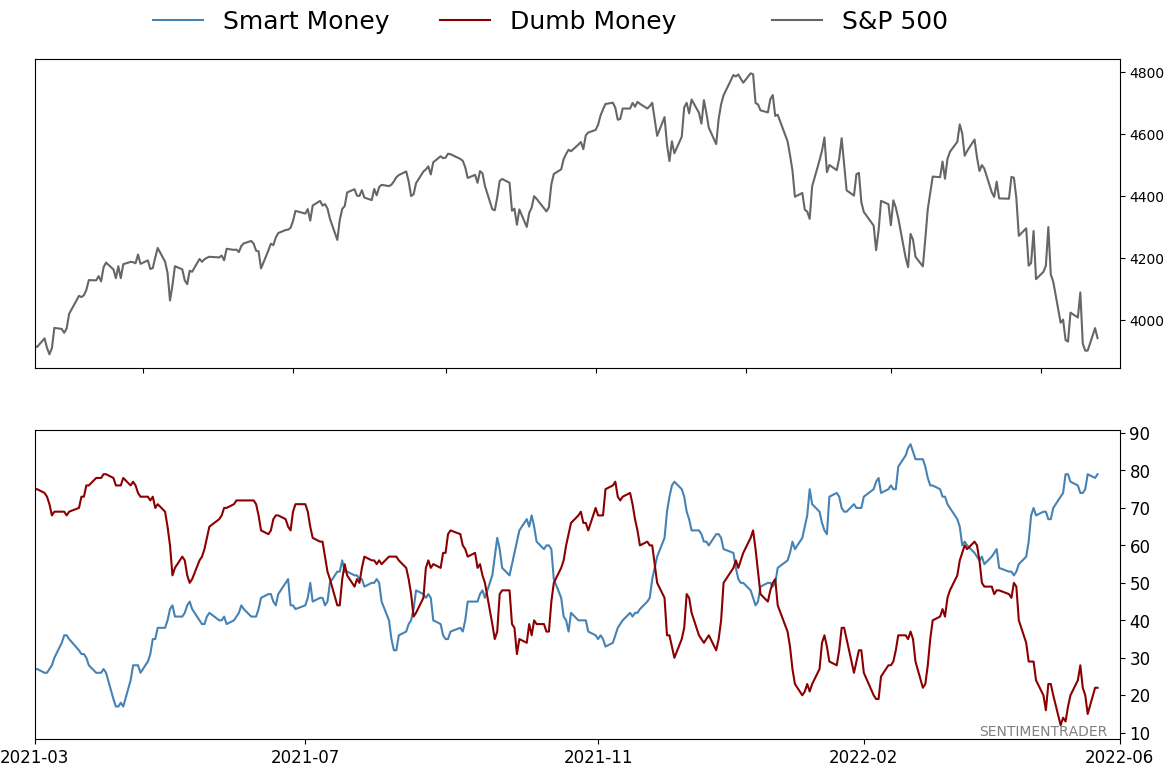

Smart / Dumb Money Confidence

|

Smart Money Confidence: 79%

Dumb Money Confidence: 22%

|

|

Risk Levels

Stocks Short-Term

|

Stocks Medium-Term

|

|

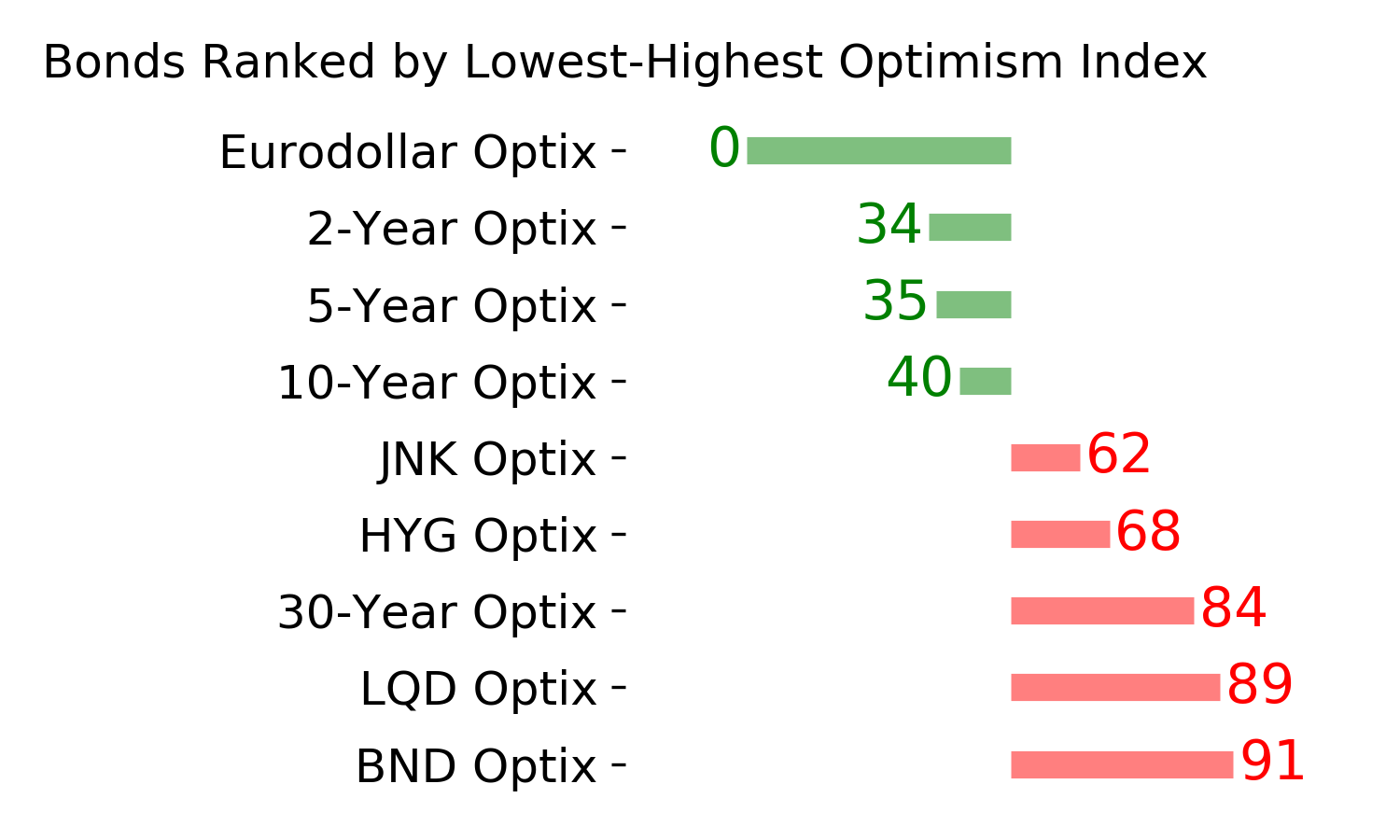

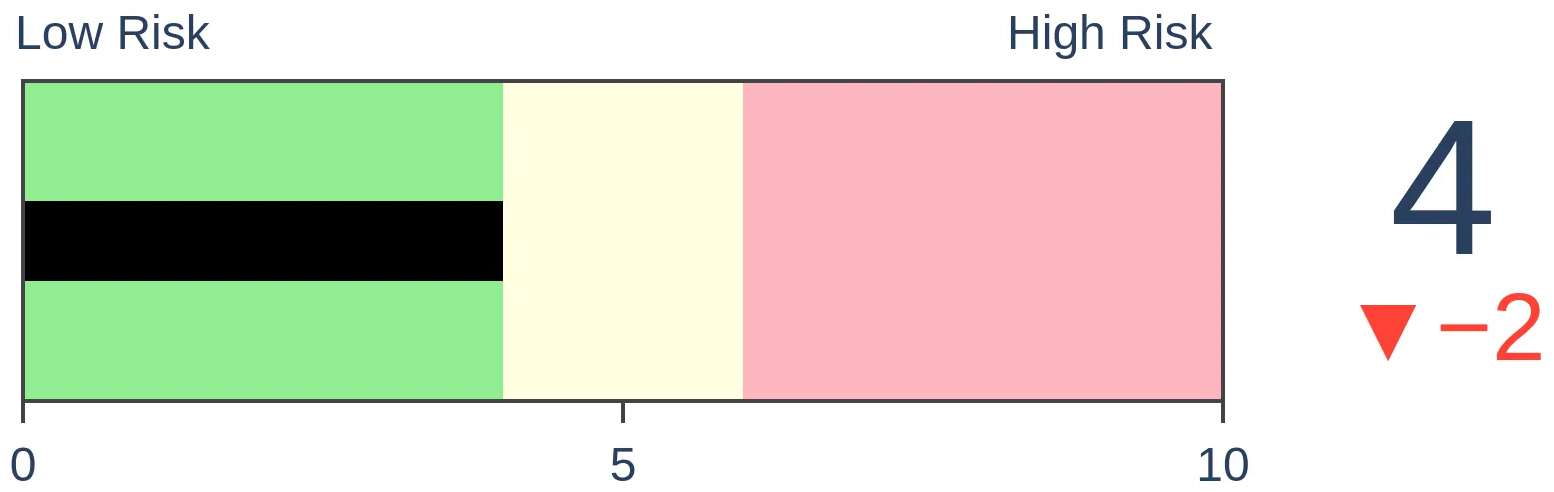

Bonds

|

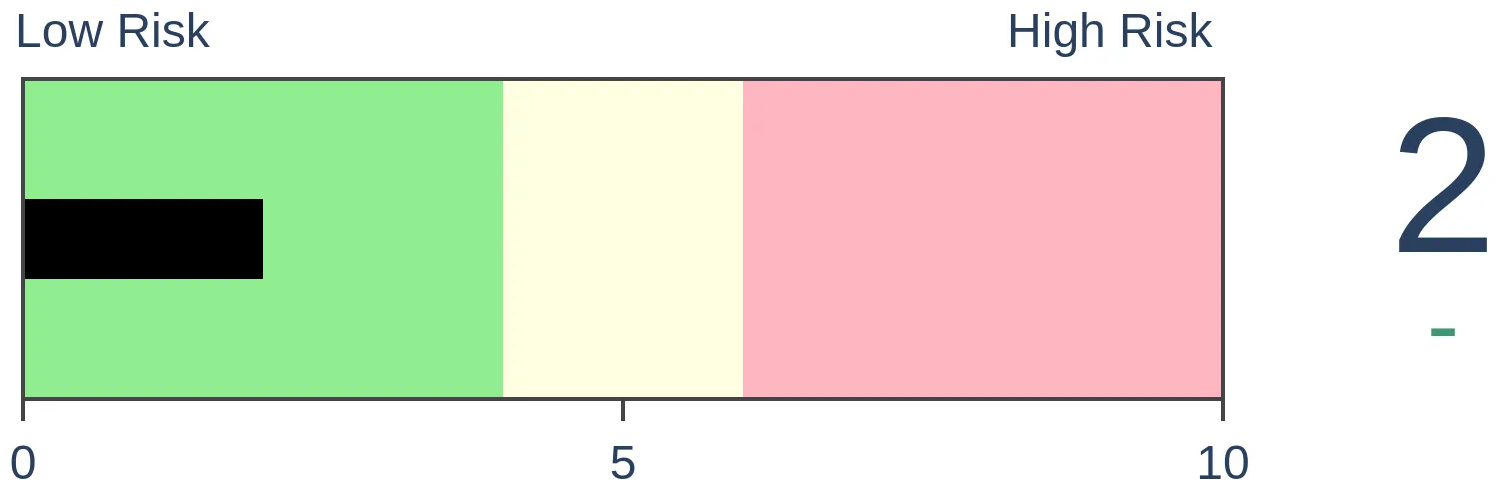

Crude Oil

|

|

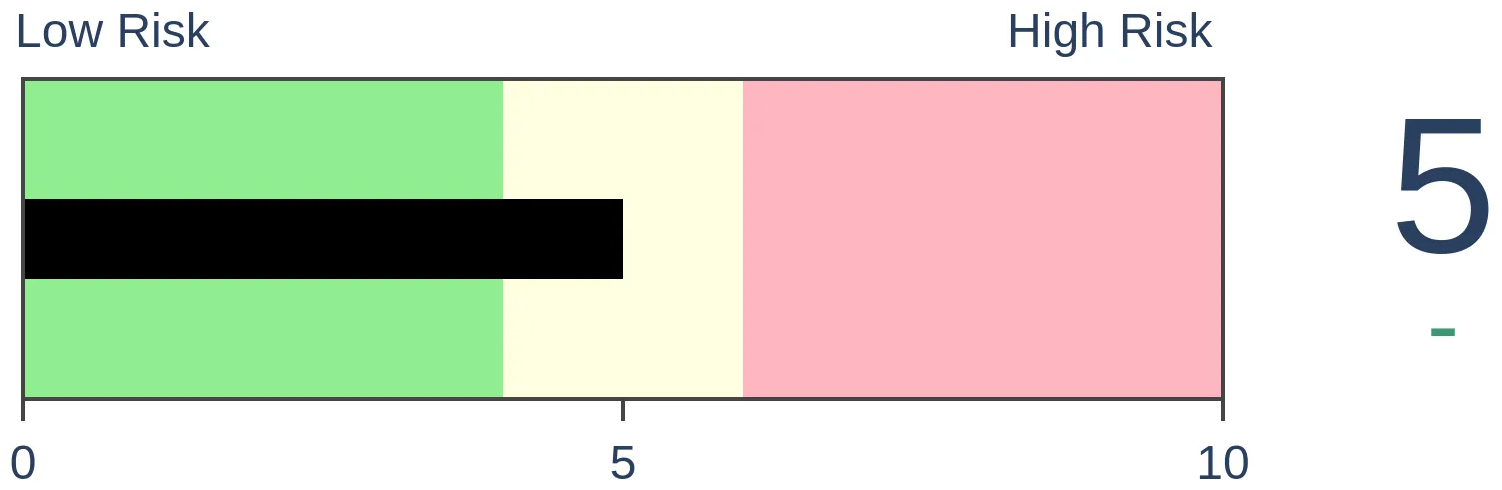

Gold

|

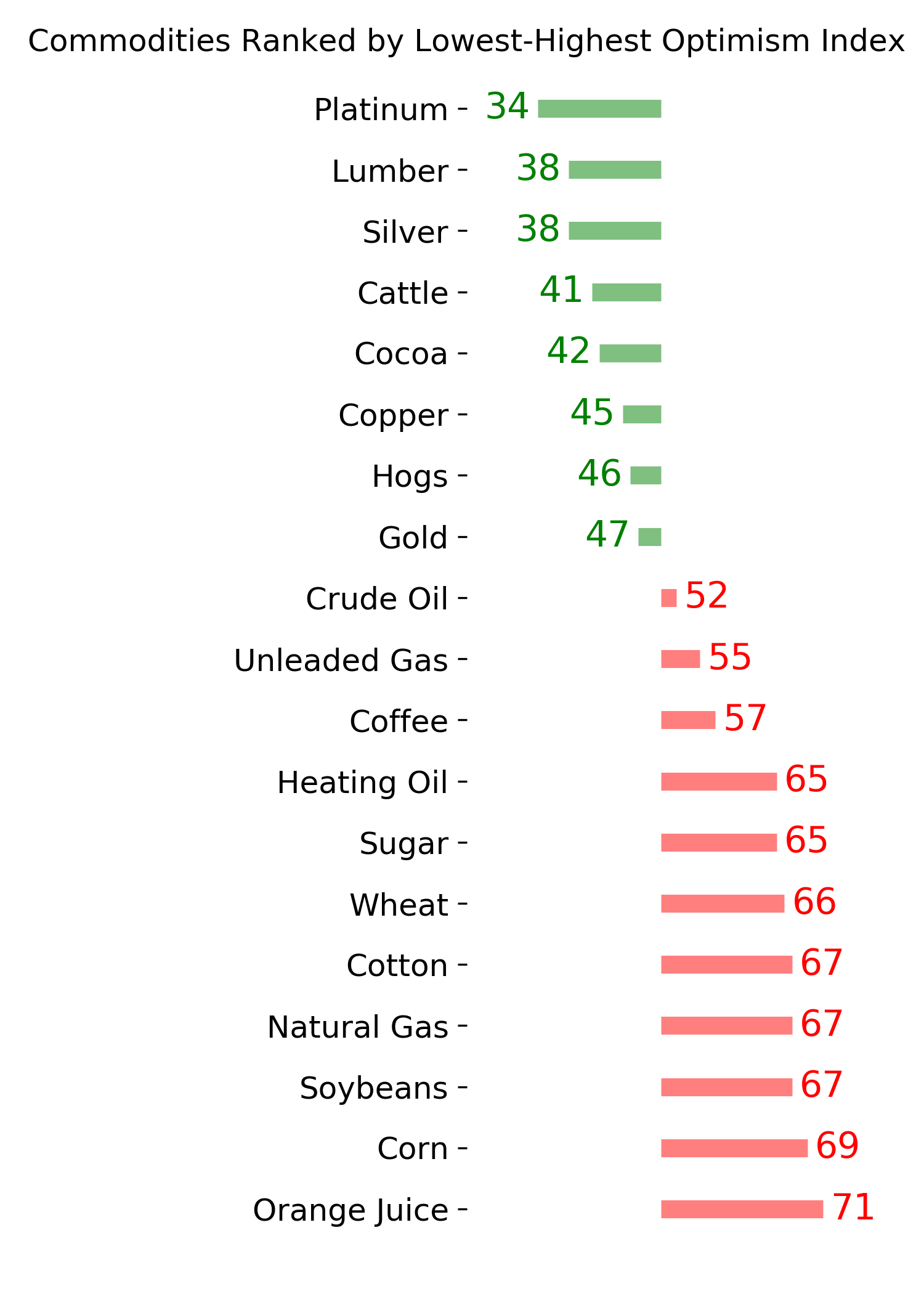

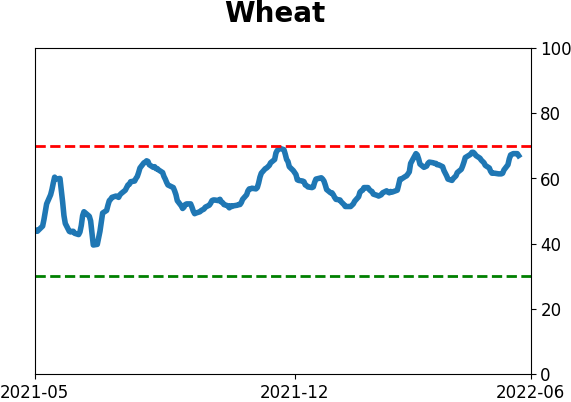

Agriculture

|

|

Research

By Jason Goepfert

BOTTOM LINE

Over the past few months, pessimism toward the bond market reached extreme levels. That has started to ease as the selling pressure let up in recent weeks. Similar behavior typically led to multi-month gains in Treasuries, but with the biggest caveat being limited data under what may be the most comparable market environments.

FORECAST / TIMEFRAME

None

|

Key points:

- Most indicators on the bond market are showing that extreme pessimism is starting to reverse

- Similar behavior tended to lead to multi-month gains

- The biggest caveat is limited data under what may be a vastly changed market environment

Embedded pessimism is finally starting to thaw

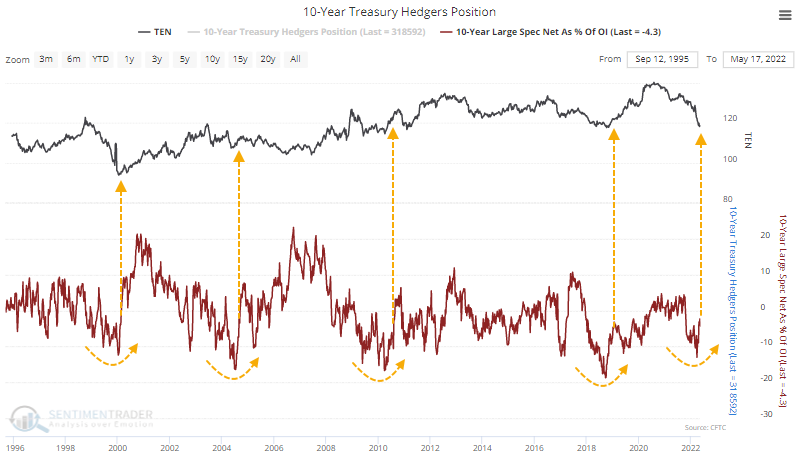

While the S&P 500 is the most important equity index in the world, the most important market is U.S. Treasuries. And sentiment there is finally starting to turn a bit more optimistic.

For the first time this year, large speculators are starting to cover their shorts in earnest and are on the cusp of going net long. While this is somewhat subjective, when they'd been heavily short and then started to cover in earnest, it was mostly a good sign for 10-year Treasury prices (meaning lower yields).

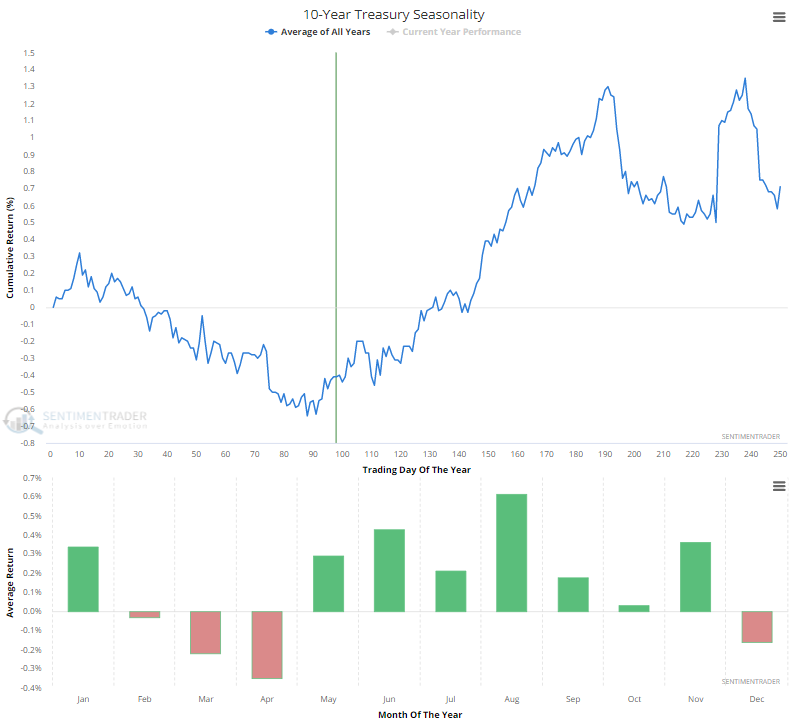

It's right on time as the seasonal window has turned positive. When we looked at this in April, we saw that the market had a bit more to go before the window turned positive, and while it's almost certainly just a coincidence, the selling started to stop right on time.

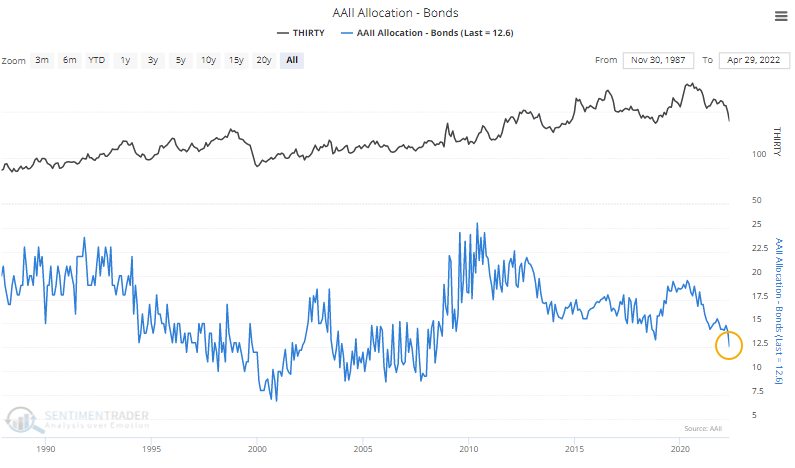

Individual investors remain wary as their allocation to bonds ticked lower again in the latest survey. They now have the lowest percentage of their assets in bonds since June 2008.

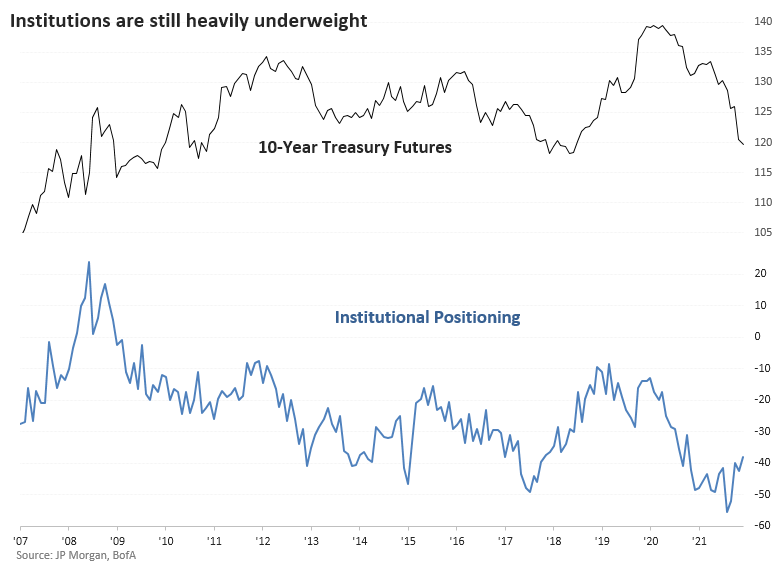

Professional investors seem to be even less inclined to be exposed to bonds, but that's starting to change. According to client positioning surveys from JP Morgan and BofA, client allocations to bonds are just picking up from at least 15-year lows.

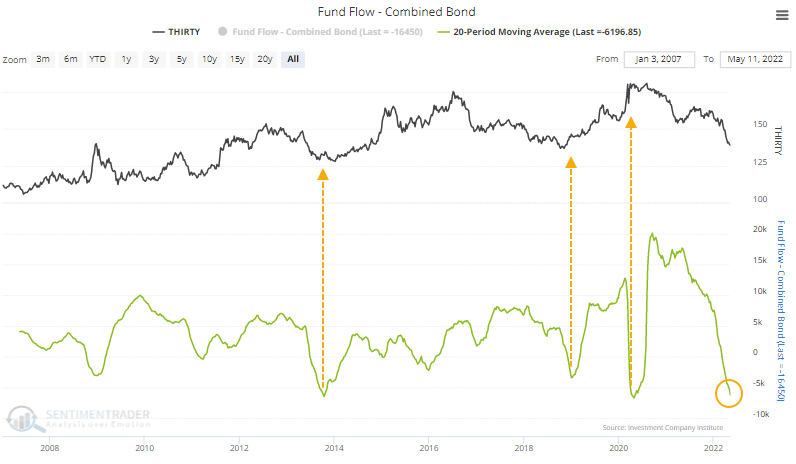

The persistently poor sentiment has resulted in persistent outflows from bond funds over the past 20 weeks, closing in on the records from October 2013 and April 2020.

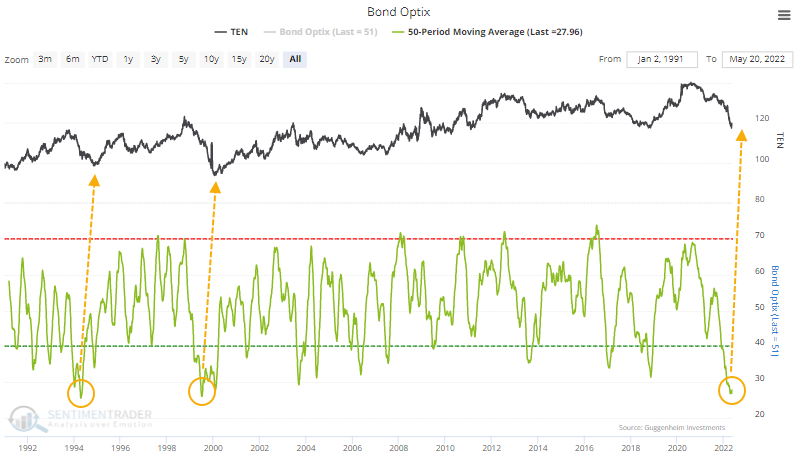

Taken altogether, the Bond Optix is finally starting to trough from near-record pessimism. As noted in April, this has tended to curl up ahead of the ultimate price low, at least from what we can see from a sample size of two and during what could be a completely new environment.

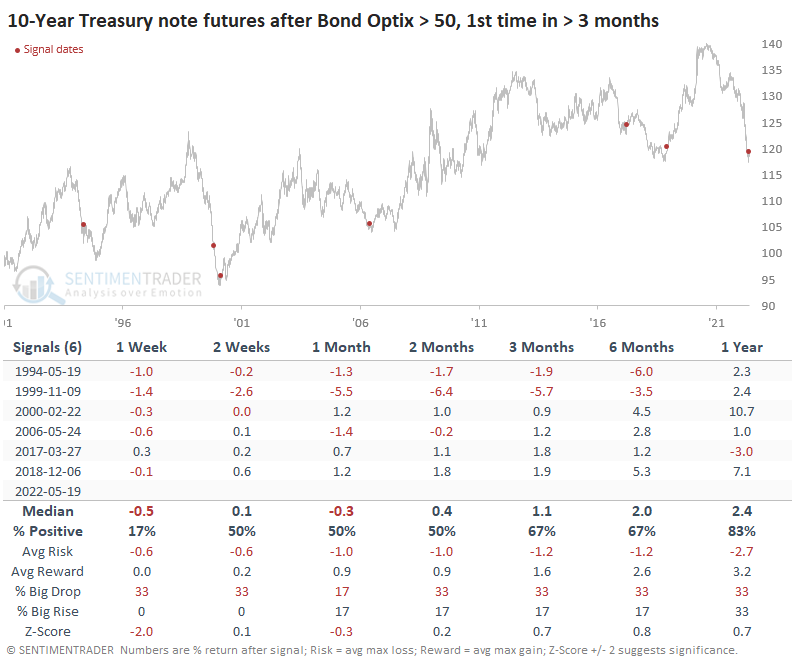

Over the past 30 years, when the Bond Optix finally exceeded 50% for the first time in months, it has mostly been a good sign, but the 1994 and 1999 signals were too early to capitalize on medium-term rallies.

What the research tells us...

The tricky part with gauging extremes in the bond market is the high likelihood that we've entered an environment that we haven't seen since before most of the data we have now was available. That makes trying to rely on extremes more fraught with "this time is different" danger than usual. From the data that we have over the past 30 years, the extreme pessimism that had built up over the past few months, and is now being relieved a bit, should indicate that further losses should be limited and temporary over a medium-term time frame.

Indicators at Extremes

Phase Table

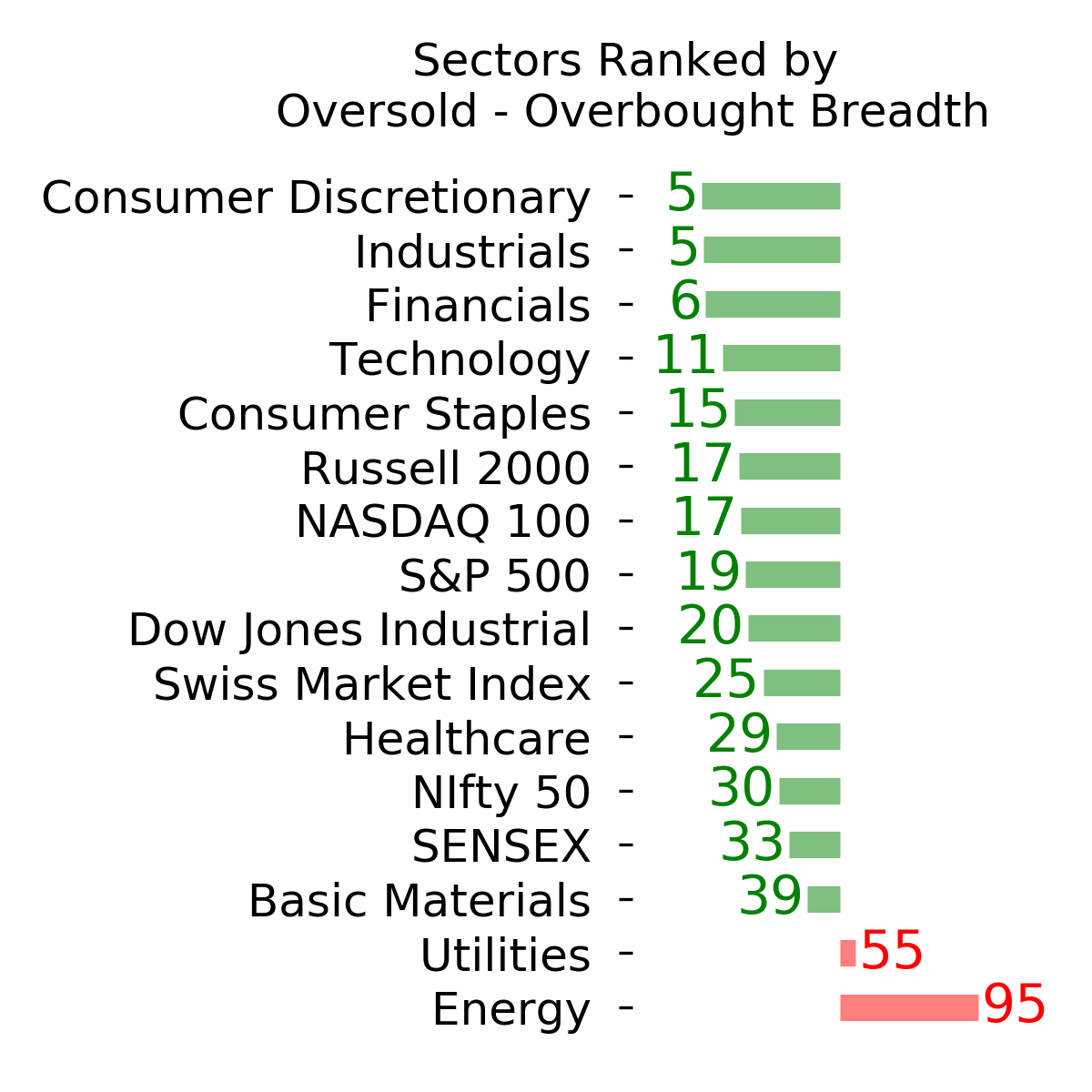

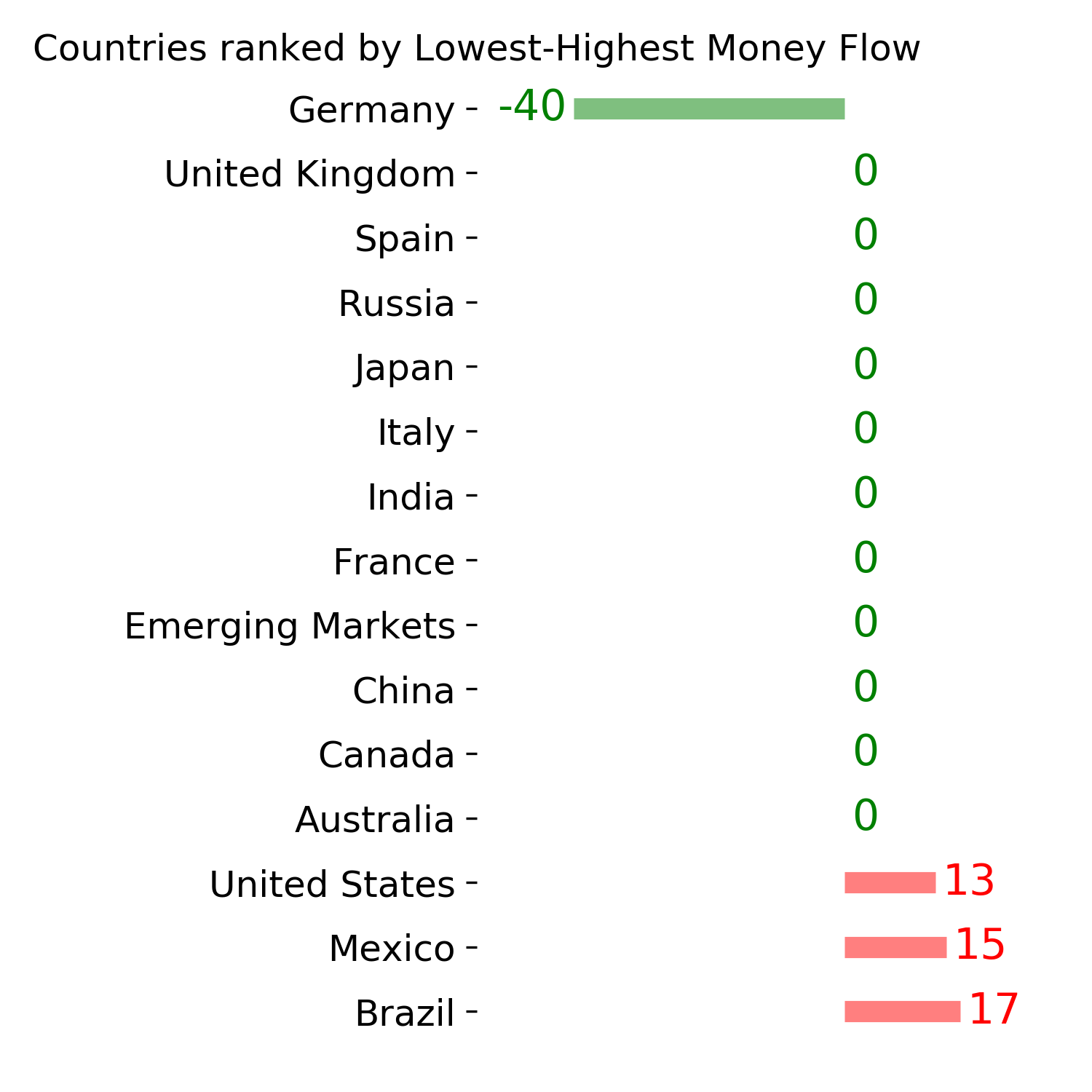

Ranks

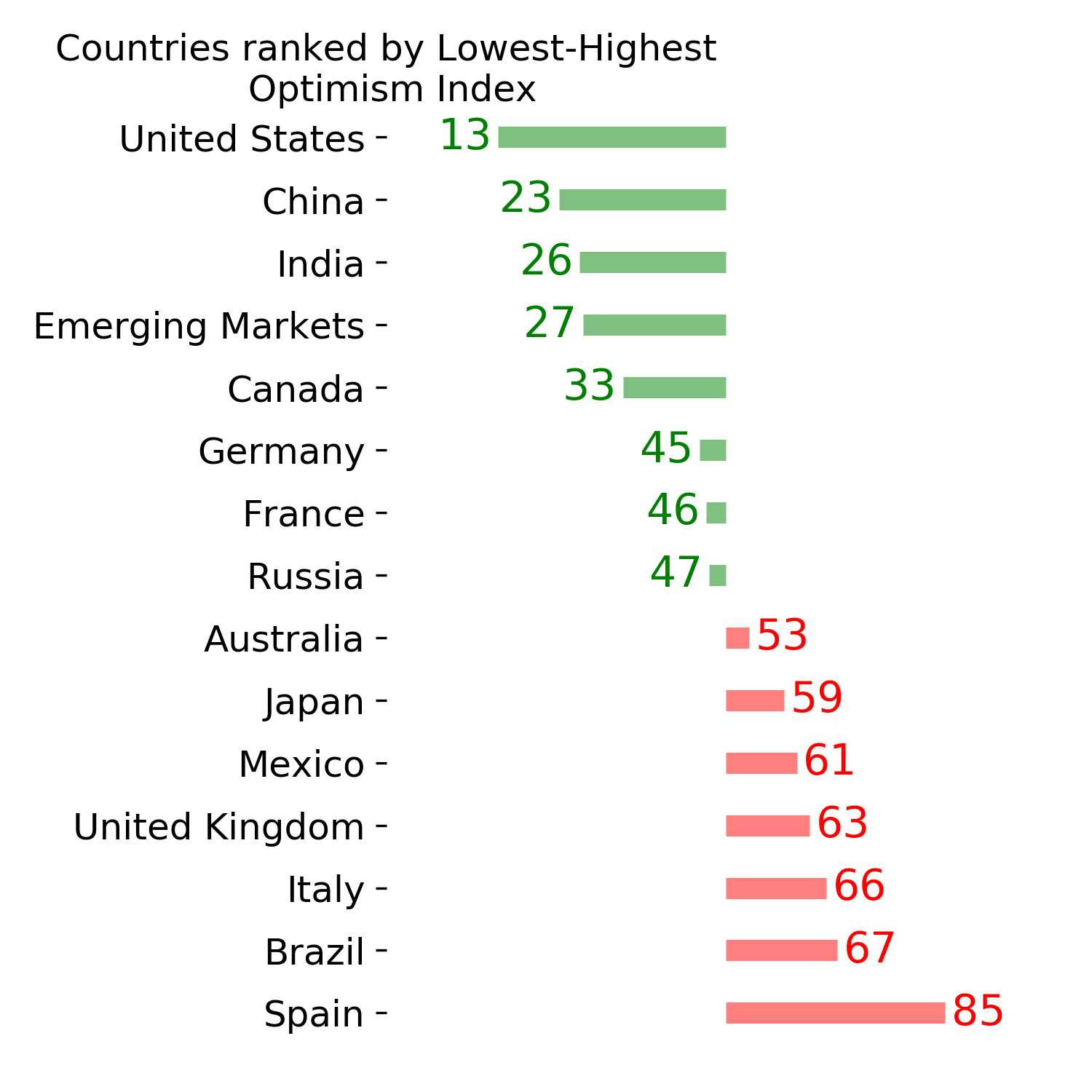

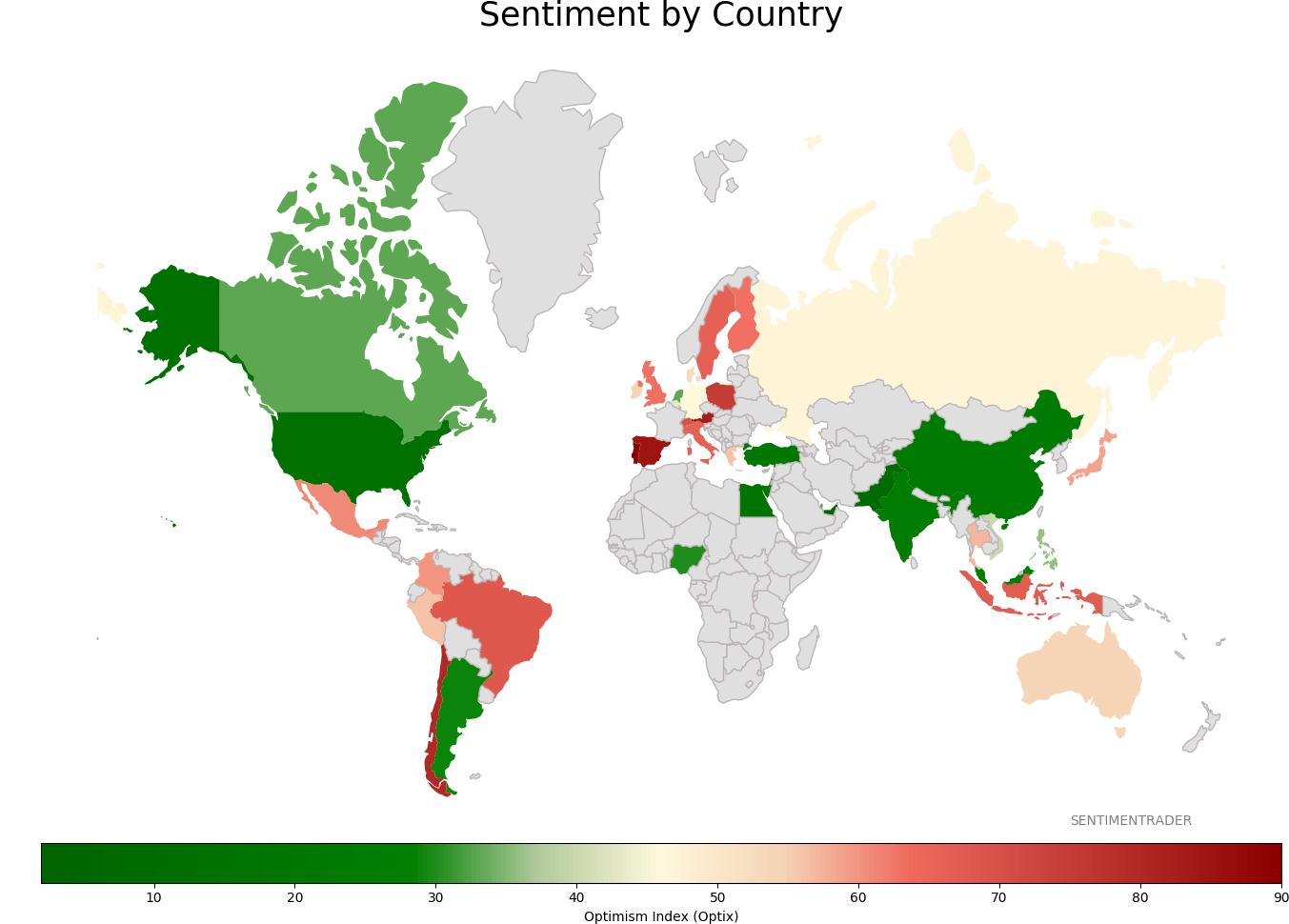

Sentiment Around The World

Optimism Index Thumbnails

|

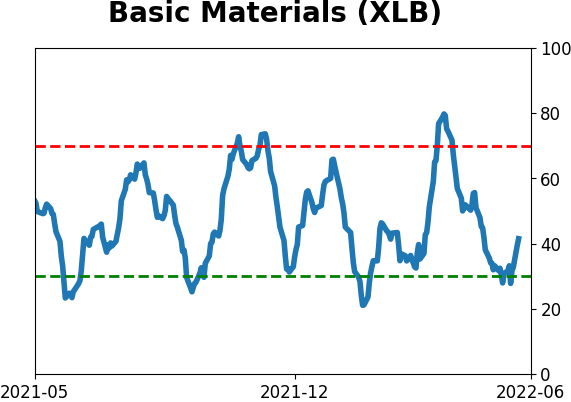

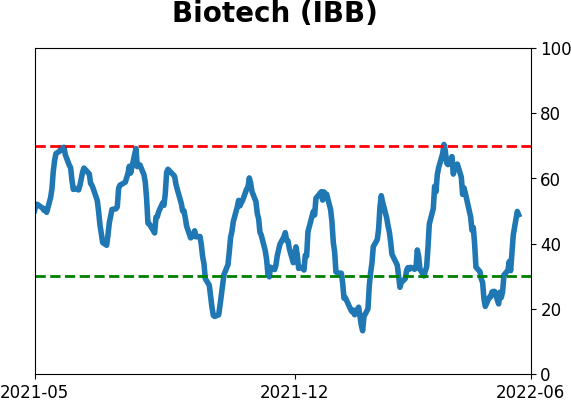

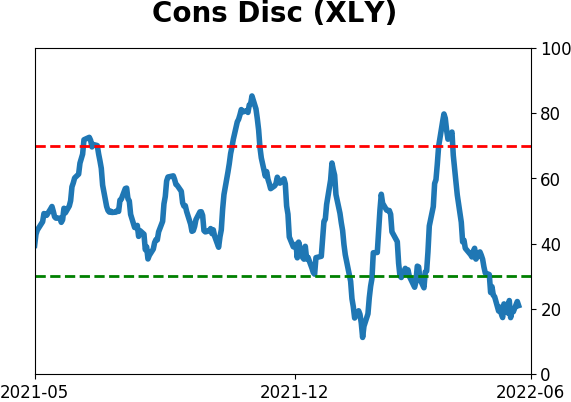

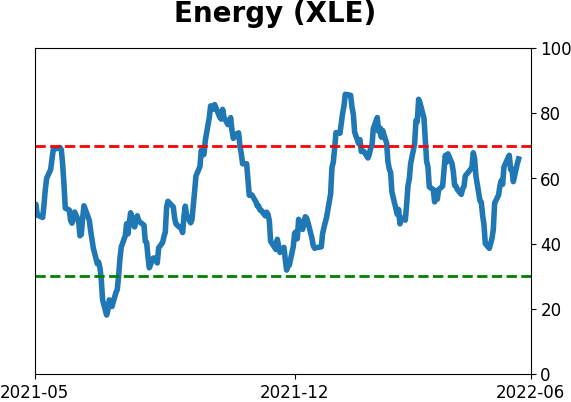

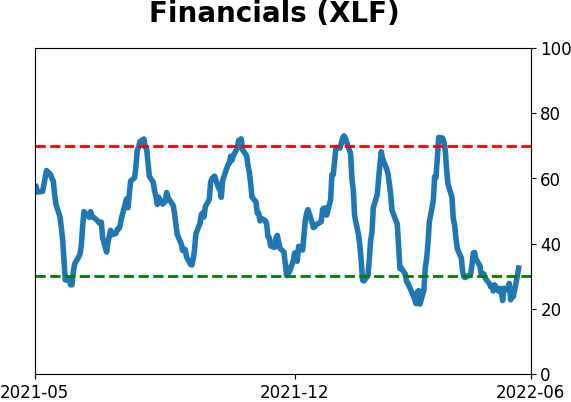

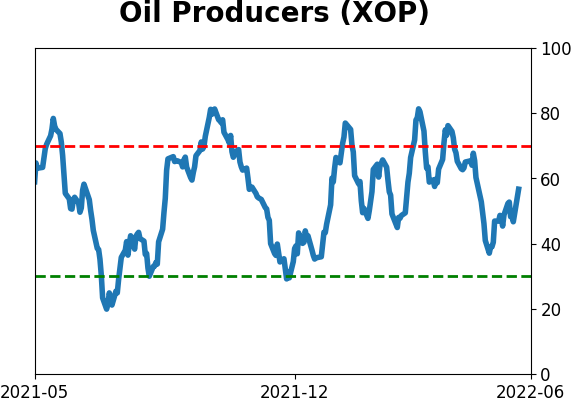

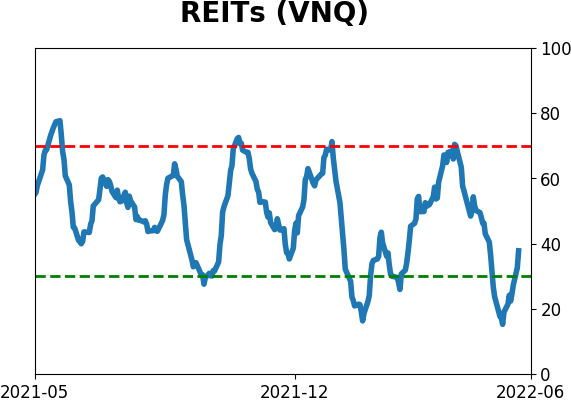

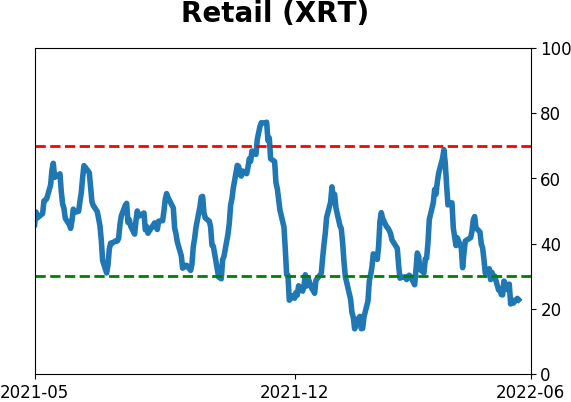

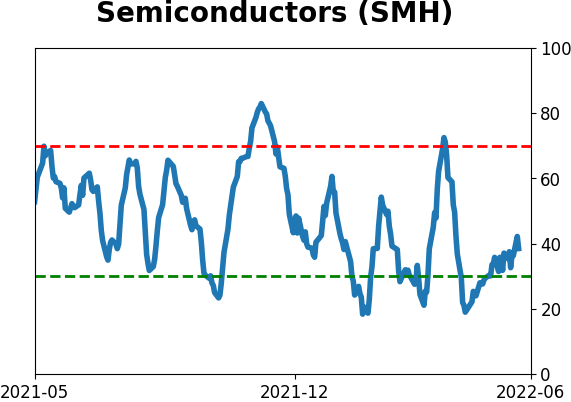

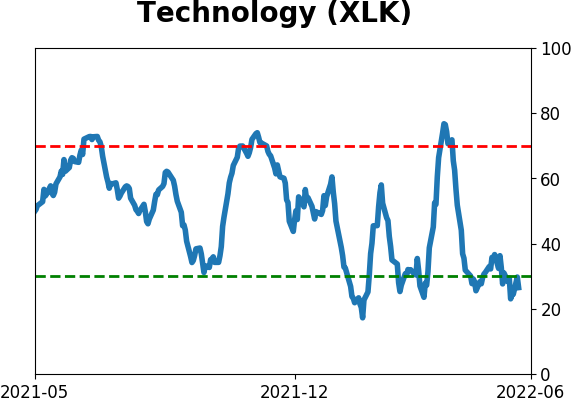

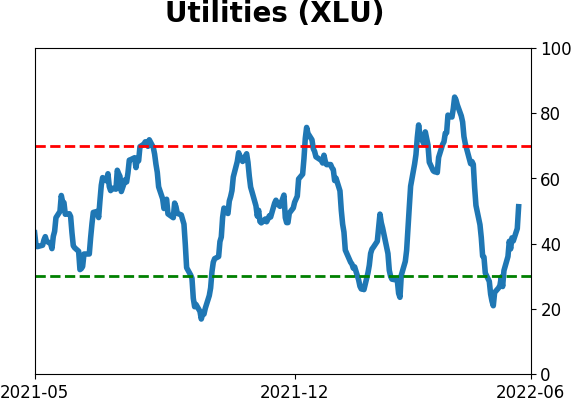

Sector ETF's - 10-Day Moving Average

|

|

|

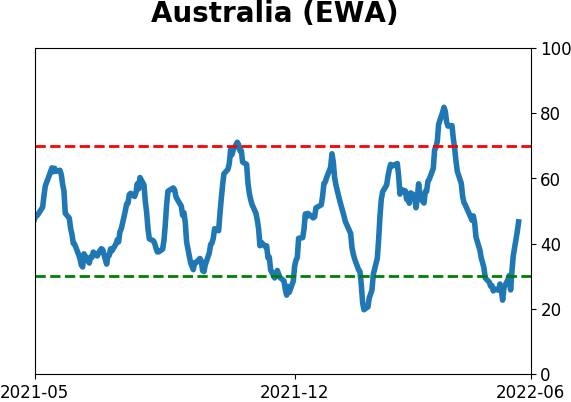

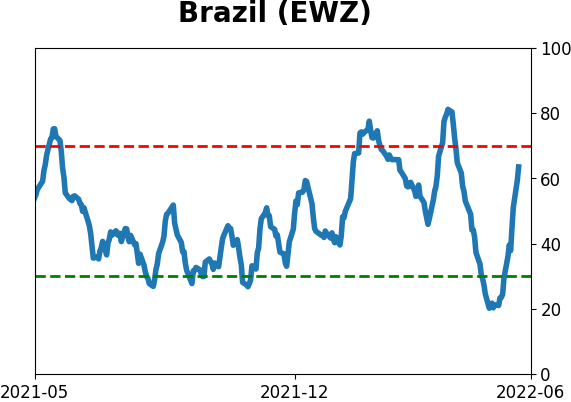

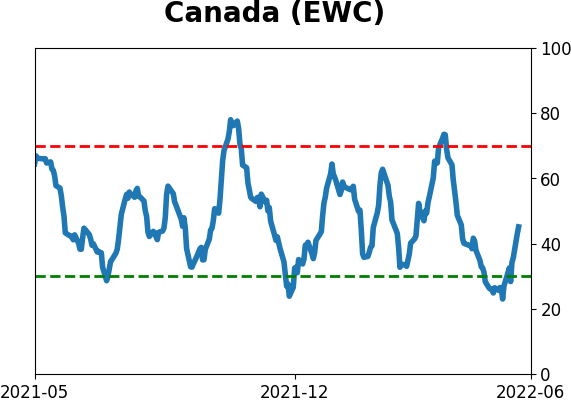

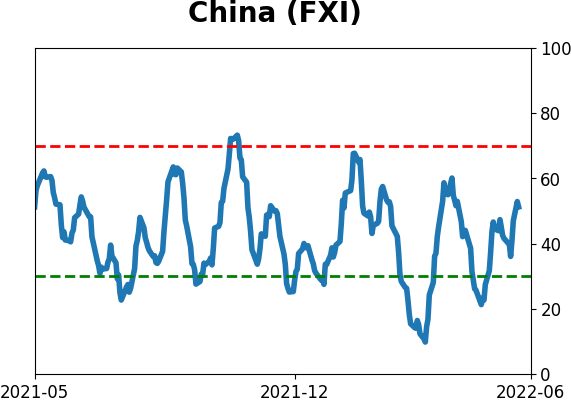

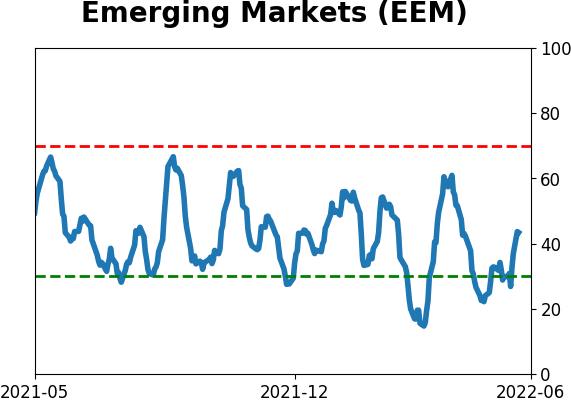

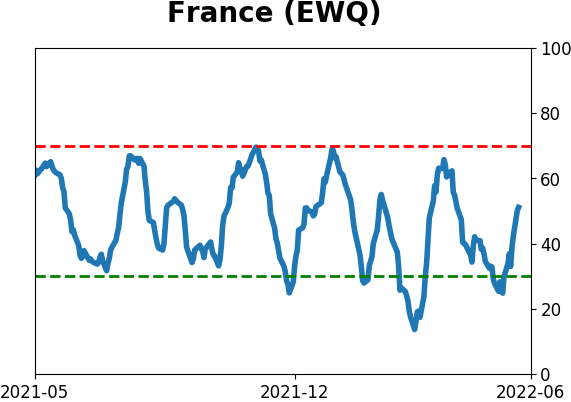

Country ETF's - 10-Day Moving Average

|

|

|

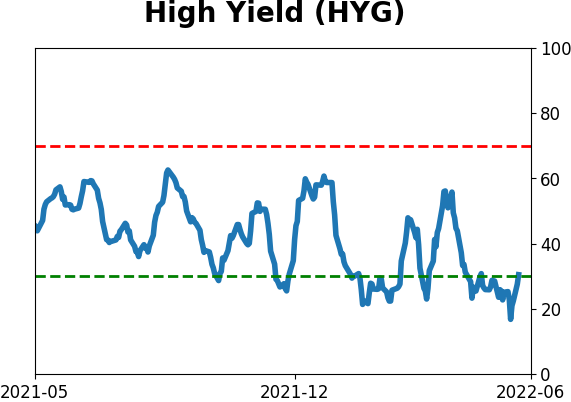

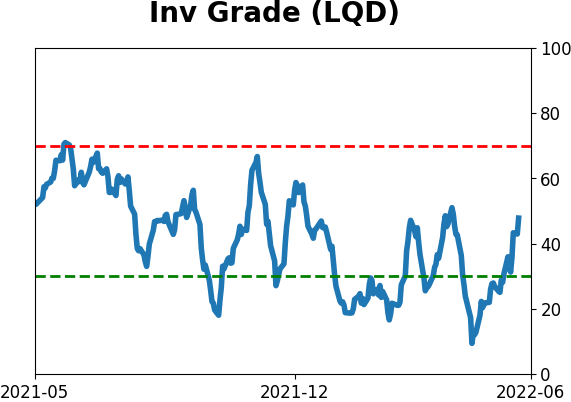

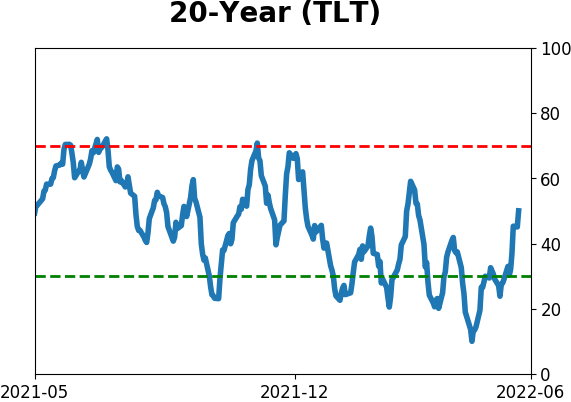

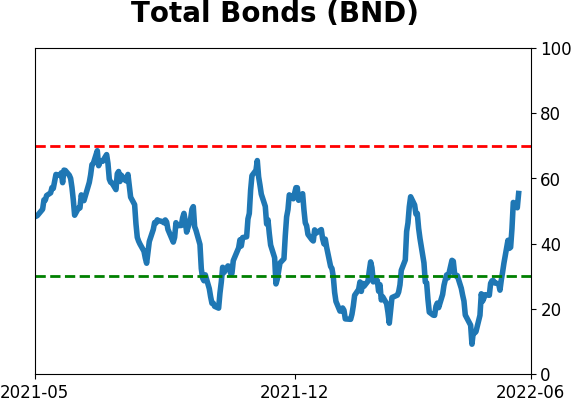

Bond ETF's - 10-Day Moving Average

|

|

|

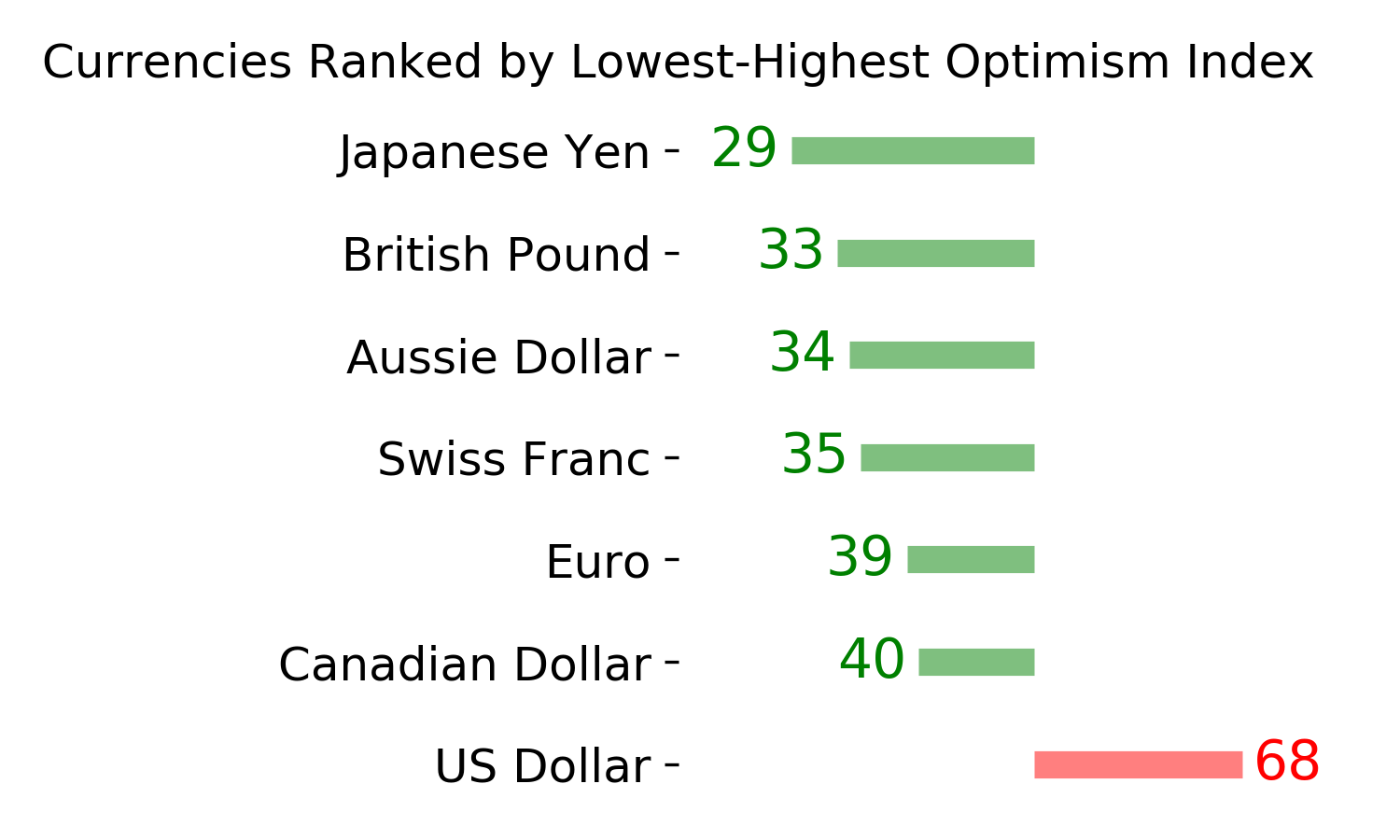

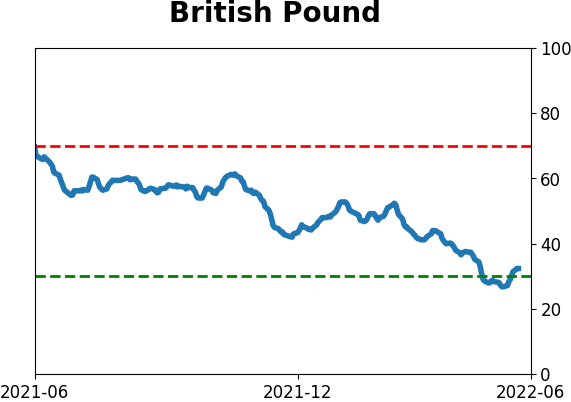

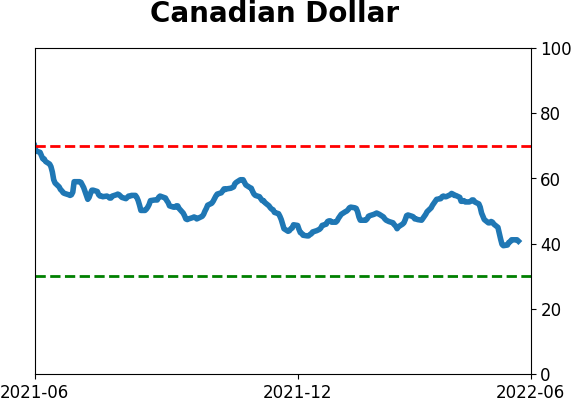

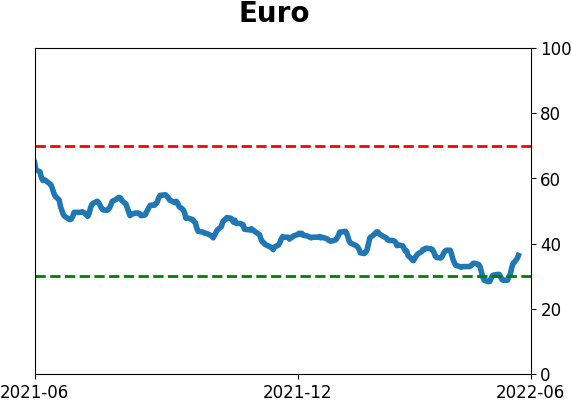

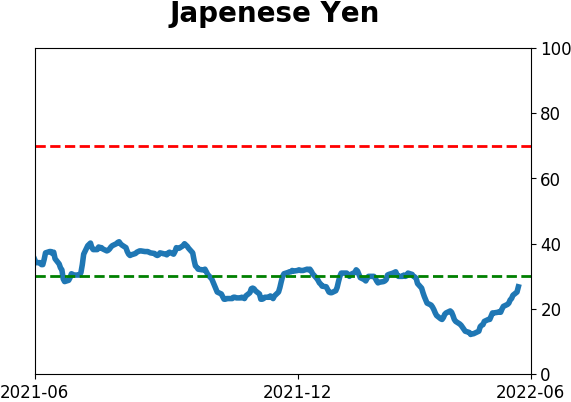

Currency ETF's - 5-Day Moving Average

|

|

|

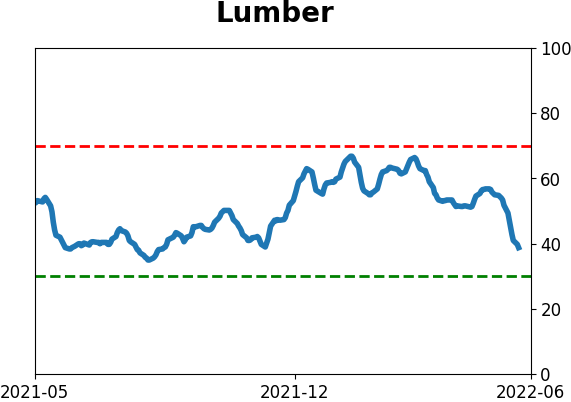

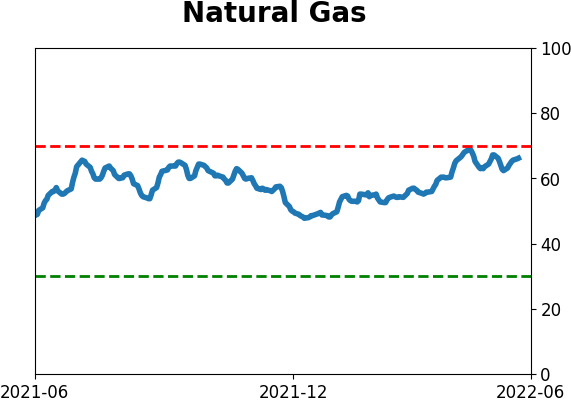

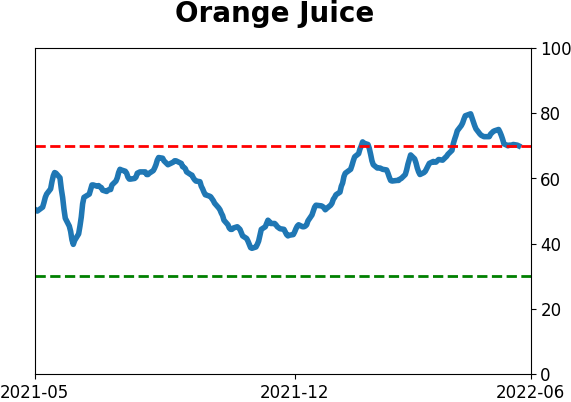

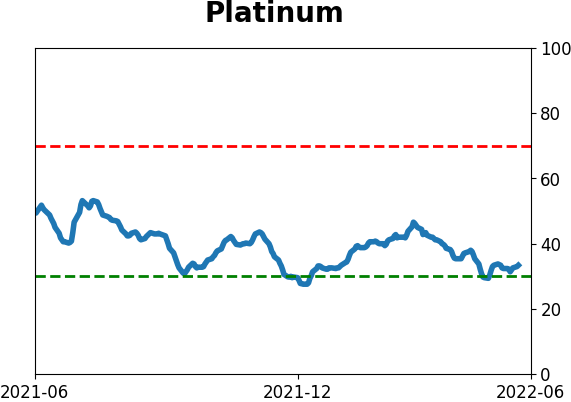

Commodity ETF's - 5-Day Moving Average

|

|