Corn seasonality and sentiment flash a warning

Key Points

- Corn enjoyed a terrific run from 2020 into 2022, rallying from $3 to $8 a bushel

- A recent -11% decline has traders wondering what will come next

- Seasonality and sentiment are presently arguing that more weakness is in store in the months directly ahead

- Traders should remain aware that a high inflation environment can cause an exception to the rule

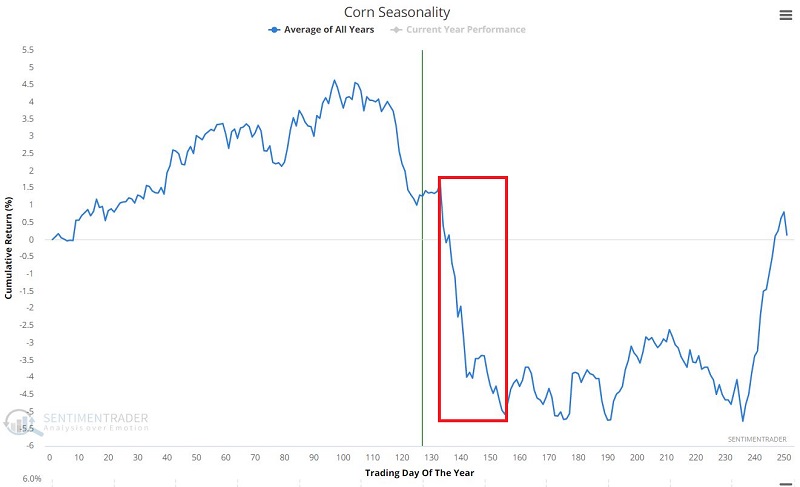

Seasonality

The chart below displays the annual seasonal trend for corn futures. The implication of the red box is pretty apparent.

The unfavorable seasonal period for corn extends from the close on Trading Day of the Year (TDY) #133 and through TDY #155. For 2022 this period extends from the close on 7/15/2022 through the close on 8/16/2022.

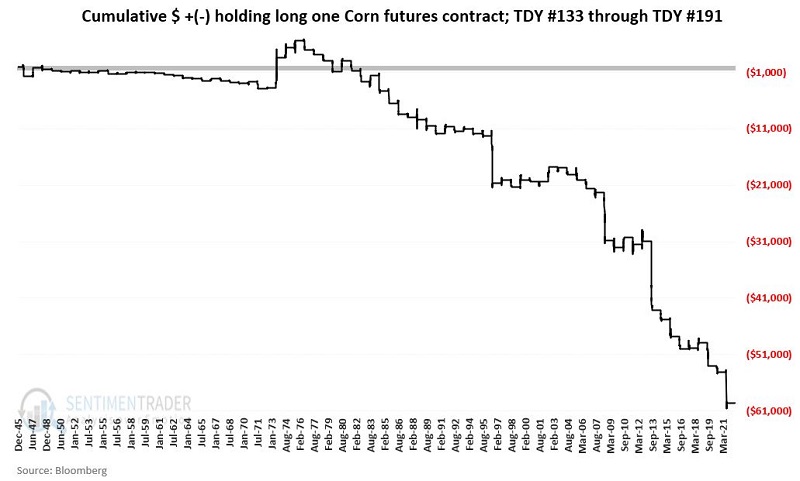

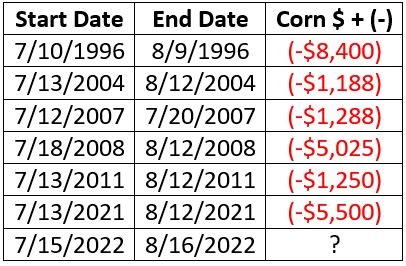

Does this mean that corn is sure to decline between these two dates? Not at all. But let's look at some history to understand better what to expect. The chart below displays the hypothetical cumulative gain/loss achieved by holding long one corn futures contract from TDY #133 through TDY #155 every year since.

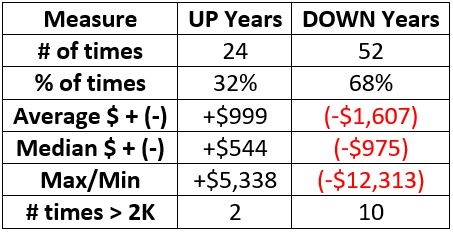

Once again, the long-term implication is pretty obvious. To put some numbers to it, the table below displays a summary of annual results.

Roughly two out of every three years has seen corn decline during this seasonally unfavorable period.

Sentiment

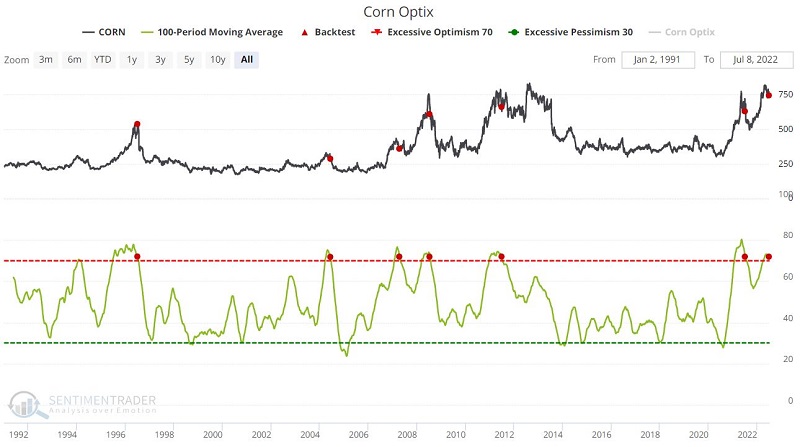

It is not surprising to learn that trader sentiment towards corn turned very bullish during the run-up in early to mid-2022. But what does this strong bullish sentiment suggest for corn going forward?

The chart below displays those times when the 100-day moving average for Corn Optix dropped below 72. In other words, this test looks for a period when corn Optix is high for an extended time, and then "the bloom comes off the rose" (or the crop, in this case).

The latest signal occurred on 7/6/2022. The table below displays a summary of corn futures performance following previous signals.

The table above shows that the "Not So Sweet Spot" is three months after a signal. This dovetails closely with the seasonally unfavorable period discussed earlier. Now let's put seasonality and sentiment together.

Seasonality and Sentiment Combined

Let's first create a simple Corn Seasonality and Sentiment (CSS) Model.

A = If today is between TDY #134 and #155 then -1

B = If the 100-day average of Corn Optix dropped below 72 anytime in the last 63 trading days, then -1

C = A + B

CSS Model = C

The bottom line:

- If neither indicator is bearish, the CSS Model will equal 0

- If either indicator is bearish, the CSS Model will equal -1

- If both indicators are bearish, the CSS Model will equal -2

Our Corn Optix data starts in 1996, so our test runs from 12/31/1995 through 7/6/2022.

CSS Model = 0

The table below displays the cumulative hypothetical gain from holding long one corn futures contract when the CSS Model = 0. The cumulative gain is +$77,825.

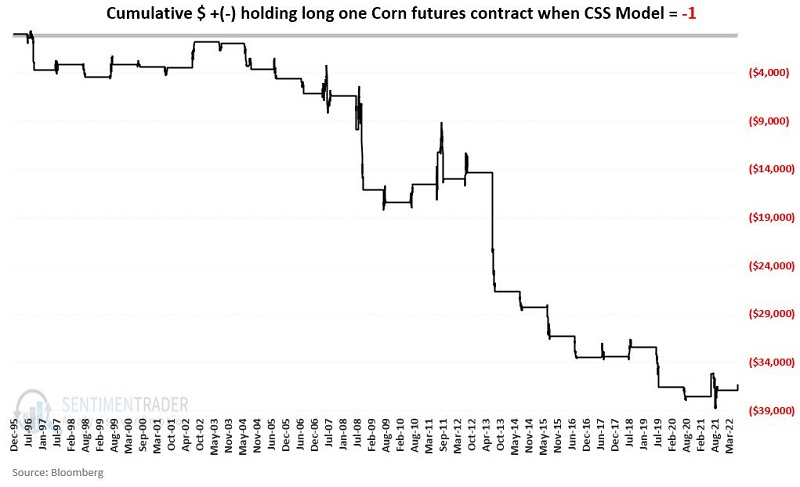

CSS Model = -1

The table below displays the cumulative hypothetical gain from holding long one corn futures contract when the CSS Model = -1. The cumulative loss is -$36,288.

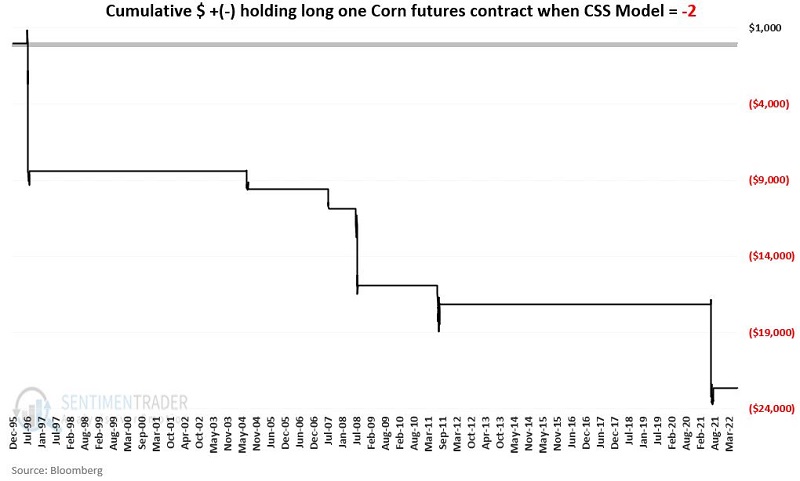

CSS Model = -2

The table below displays the cumulative hypothetical gain from holding long one corn futures contract when the CSS Model = -2. The cumulative loss is -$22,650.

The table below displays those times when the CSS Model was equal to -2.

NOTE: The CSS Model is presently at -1 and will be at -2 from the close on 7/15/2022 through the close on 8/16/2022.

What the research tells us…

Corn has demonstrated a tendency to perform poorly from mid-July into mid-August. In addition, when Corn Optix has reversed lower from a high level, future performance over the ensuing two to six months has tended to show weakness. Corn performance has been particularly unfavorable when both factors are unfavorable.

Will this year's negative period show more of the same, or will it be the exception to the rule as in 2007? There is no way to know in advance. But the bottom line is that aggressive traders might look to pay the short side of corn, and bullish traders had best make sure they have a solid reason to risk money on the long side of corn in the months ahead.