Companies pull back on buybacks while issuing more shares

The rally in stocks during the spring combined with a thirst for liquidity drove many companies to issue new shares to the public, where they had a ready audience. At the same time, they pulled back on some unnecessary expenses, like buying back their own shares.

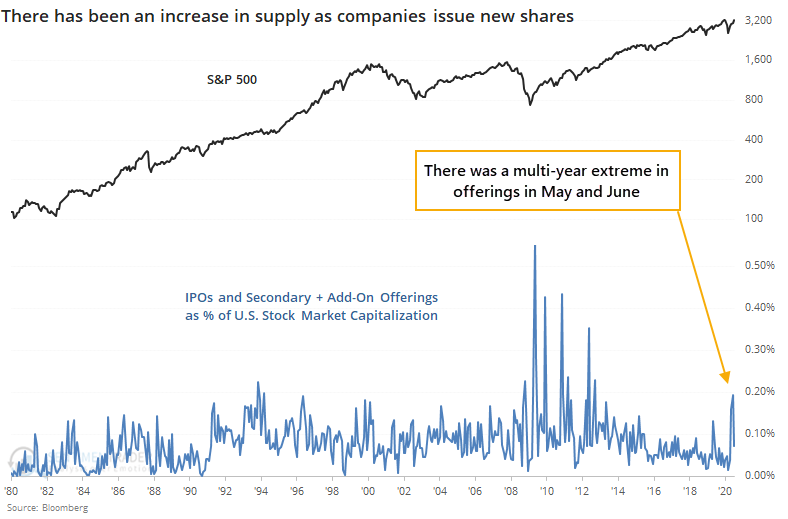

As Marketwatch notes, this has created a situation where the market is forced to choke down a lot of supply. New shares are being created through IPOs and secondary or add-on offerings, and fewer shares are being retired through buybacks.

While Bloomberg data differs somewhat from other sources, we can clearly see the jump in offerings. From May through July, there was $140 billion in IPOs and other offerings. As a percentage of the U.S. stock market, it was the most in 8 years.

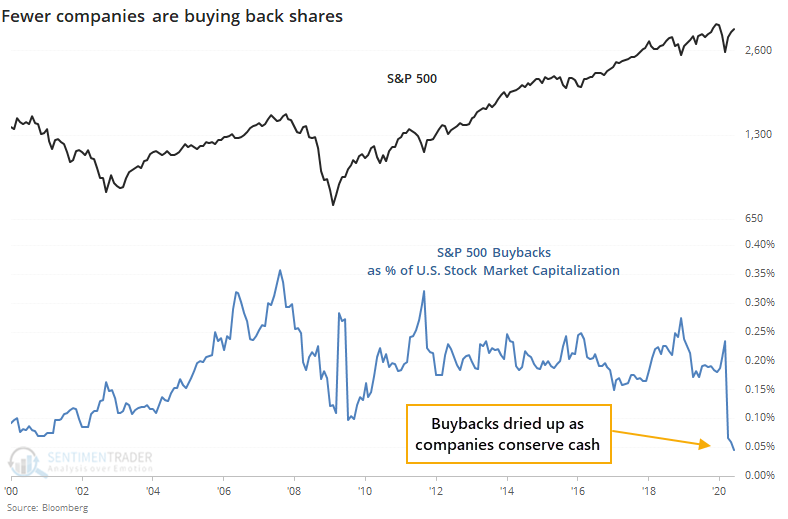

At the same time, buybacks have dried up as companies try to conserve cash without firing employees, cutting their dividends, or hamstringing their research and development budgets.

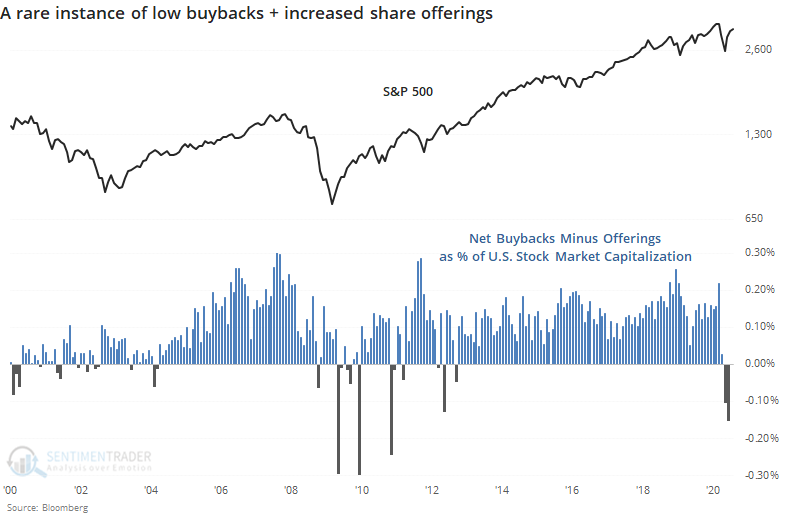

Theoretically, a combination of heavy buybacks and low offerings should be positive for stocks, since it would reduce supply. And few buybacks combined with heavy offerings should be negative.

But theory doesn't often play out in auction markets, and this is no different. Companies often increase their buybacks at precisely the wrong times, after shares have already rallied, and they pull back during times of crisis when their shares are cheap.

The chart above takes the total amount of buybacks as a percentage of market value and subtracts the total amount of share offerings via IPOs and add-ons. The higher the number, the more positive it should be for stocks. That wasn't the case - we saw high numbers right before market declines in 2007, 2012, and earlier this year.

The opposite scenario, where we are now, wasn't as clear-cut. Generally, these occurred after declines and before rallies, but it was not consistent.

The biggest takeaway is just a caveat about reading too much into the buyback vs offering theory of share supply. It sounds like this should be negative for stocks here, but the evidence doesn't give that a lot of support. If anything, we might say that companies got too pessimistic with their buybacks and that might actually be a positive. We already saw in May that a surge in offerings has not been an effective negative for stocks. Overall, it doesn't appear to be much of a reason for worry.