Why the failed breadth thrust is not necessarily bad

Key points:

- Three weeks after a massive breadth thrust, the S&P 500 has suffered large losses

- The reaction to the latest thrust was the worst in history

- After other failed thrusts, the S&P showed a strong tendency to rebound

Three weeks after a breadth thrust, nothing but losses

Three weeks ago, buyers were so interested in owning stocks that they bought pretty much all of them.

Within the S&P 500, more than 90% of stocks traded above their 50-day moving averages, after fewer than 5% of them did in June. When a similar thrust occurred in the spring of 2020, buyers continued to push the index higher over the next few weeks. This time, it has been an almost immediate failure.

The thrust was triggered on August 12 when more than 90% of S&P 500 stocks traded above their 50-day moving average. In the three weeks since then, the S&P index rallied only +0.6% above the August 12 close and fell as much as -8.3%.

This is the worst three-week reaction in the history of breadth thrusts. Ouch.

Classic technical analysis would suggest that this is an ominous sign. But we don't have much use for "classic technical analysis" because much of it is grounded in superstitions, anecdotes, and arbitrary rules. If we instead look at the evidence, we can see that it hasn't been as ominous as we might assume.

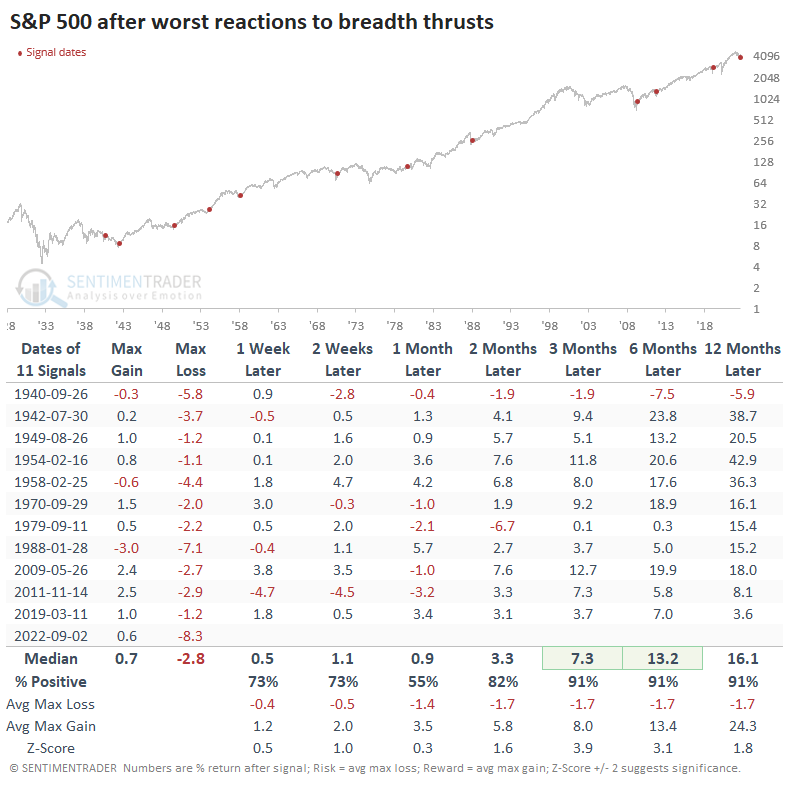

Failed breadth thrusts have not been a dire signal

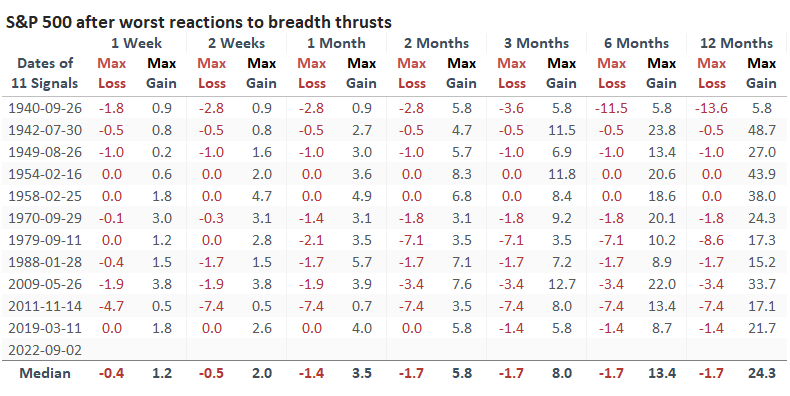

The table below shows the worst three-week reactions to similar breadth thrusts since 1928. These are times when fewer than 5% of S&P stocks were trading above their 50-day average, then more than 90% of them did. In the following three weeks, the index showed the worst reactions, with the smallest gains and largest drawdowns.

Curiously, only one signal, in 1940, showed persistent losses in the months ahead. After the others, the S&P 500 rebounded, and its gains were usually significant.

The Risk/Reward Table shows that within the next three months, only two signals suffered a drawdown of more than -5%. All but one of them enjoyed a gain of more than +5% within that time frame.

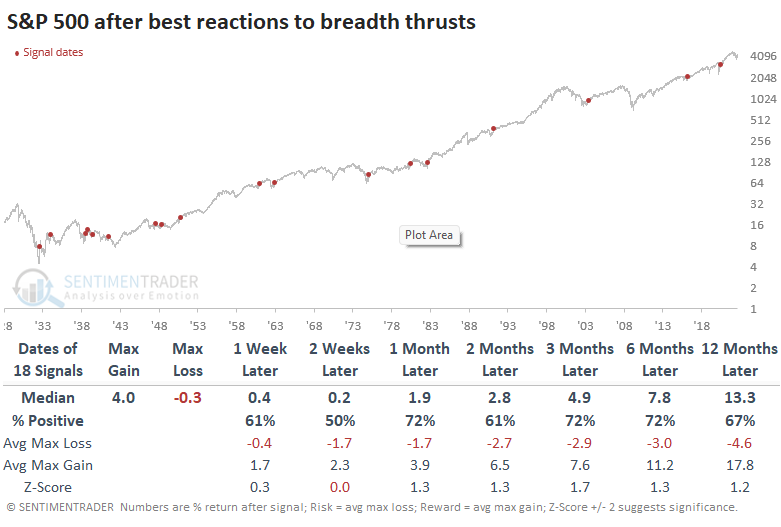

Contrast this performance to those signals that showed the best reaction. These are times when the index rose the most and suffered the smallest drawdown in the three weeks following a thrust.

After most time frames, the S&P showed less consistent gains, smallest gains, larger drawdowns, and smaller maximum gains.

What the research tells us...

The ridicule being heaped on the multiple breadth thrusts since June has reached a fever pitch. Because stocks have declined, it seems like everyone is discounting the signals and marking them down in the "failure" column. They certainly have failed so far; that is objectively true. But it also missed the point because they are not consistent short-term signals. Instead, they are guides that longer-term sentiment has shifted, and investors are now willing to buy stocks eagerly. That sentiment tends to persist for months.