Two potential headwinds for gold

Key points

- Gold has stalled once again at a 3-year-old resistance level

- Gold is entering a slightly unfavorable seasonal period

- Unless gold can punch through resistance, the combination above may act as a weight that can pull gold down in the near-term

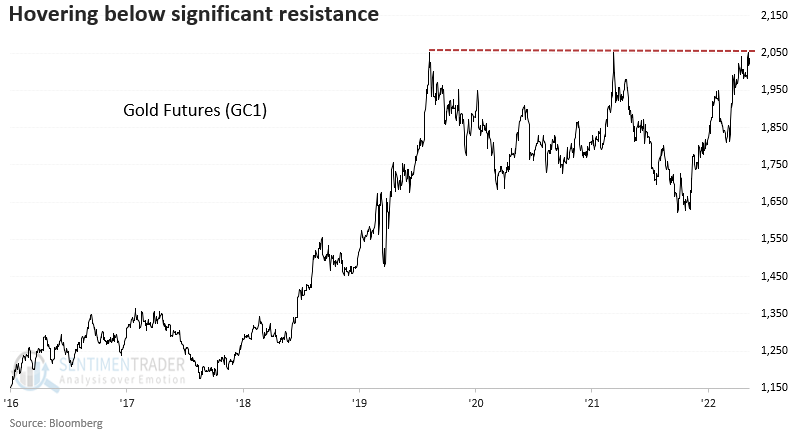

The current state of affairs

Gold bullion has rallied over 22% since early November 2023. In the process, gold has threatened several times to breakout to new all-time highs. It may still get there. However, there are two reasons for mild concern. As you can see in the chart below, gold has repeatedly "bumped its head" against resistance in the $2,050-$2,070 range.

On a somewhat subjective basis, historically, when a market tries repeatedly to break through a relatively strong line of resistance and fails, it often suffers a setback before gathering itself for another run. There is no way to know (except in hindsight) if that is what is presently happening with gold. But it certainly fits the pattern at the moment.

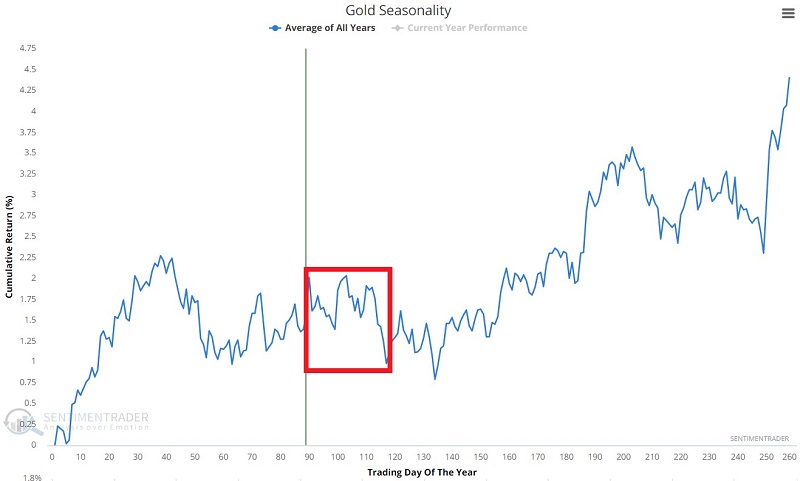

The second concern is that gold is entering a period of seasonal weakness.

Gold seasonality as a possible headwind

The chart below displays the annual seasonal trend for gold futures.

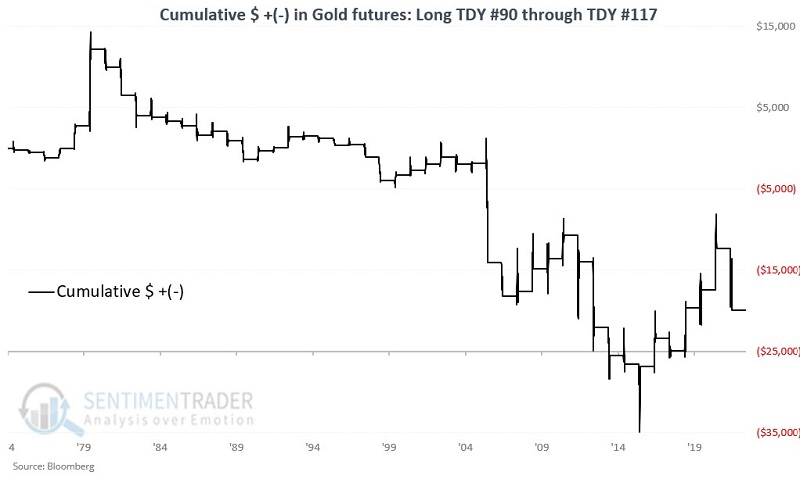

Note the period of weakness that extends from Trading Day of Year (TDY) #90 through TDY #117. For 2023, this period extends from the close on 2023-05-09 through the close on 2023-06-15. The chart below displays the hypothetical $ +/- achieved by holding a long position in gold futures only during the TDY #90 through TDY #117 period each year since 1975.

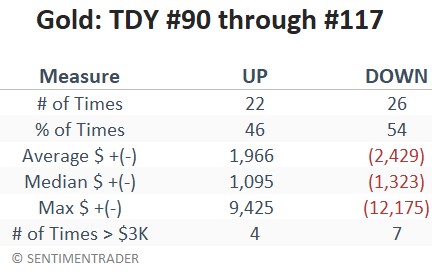

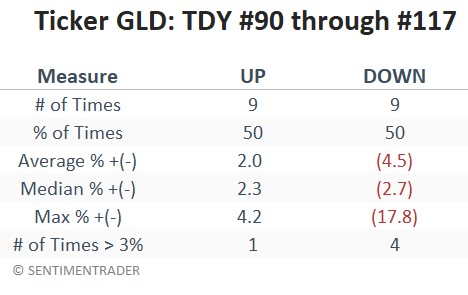

The table below summarizes gold futures' performance.

On a year-to-year basis, the results are essentially a coin flip (46% up, 54% down). But the down years tend to be noticeably weaker than the up years.

Similar results with ETF ticker GLD

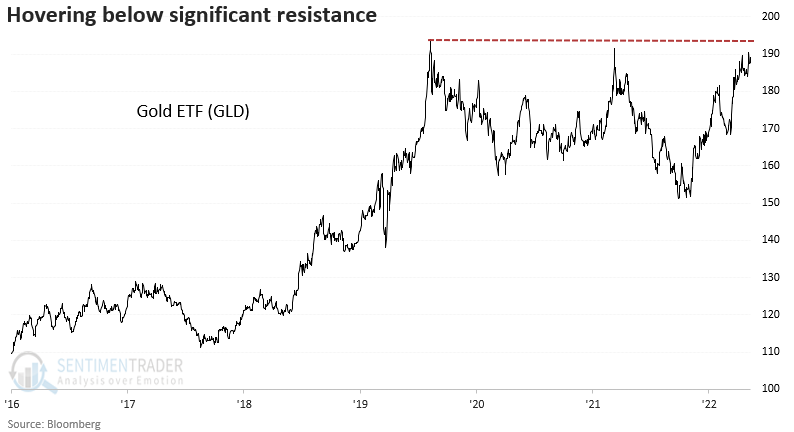

The SPDR Gold Trust is an ETF intended to track the price movements of gold bullion. It started trading in November 2004. As you can see in the chart below, GLD also stalled recently below a significant level of resistance.

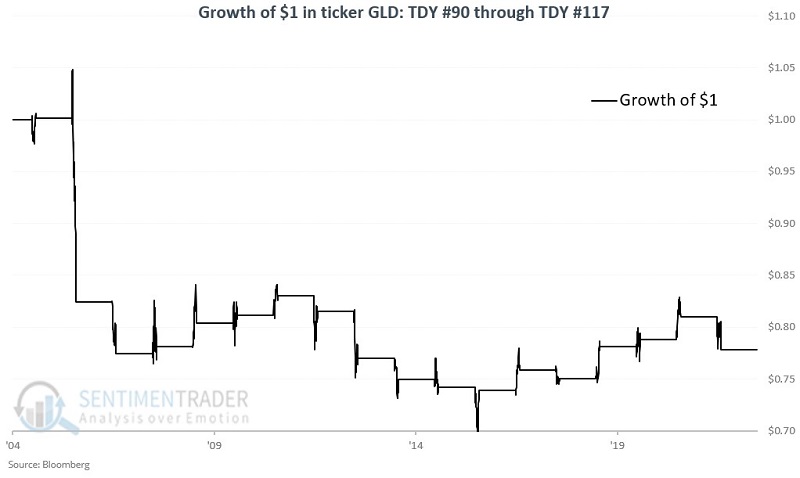

The chart below displays the growth of $1 invested in GLD only during the TDY #90 through TDY #117 period for gold futures each year since 2005. The table below summarizes GLD performance.

What the research tells us…

Labeling the TDY #90 through TDY #117 period as "bearish" for gold would be a misnomer. But it would be an even bigger misnomer to label it "bullish." Both gold bullion and ticker GLD have lost ground during this period over many years. At the very least, this raises the question of whether it is worthwhile to allocate capital to gold-related investments at the moment. Given the inability (so far) of gold to punch through a three-year-old level of resistance, the potential for a pullback seems elevated. All of that said, one of the most apparent statements regarding any tradable asset is that the most bullish thing it can do is rise in price. If gold can break through to the upside (and hold above the previous resistance), seasonal concerns are best ignored.