TradingEdge Weekly for May 20 - Historic selling pressure, spike in pessimism, skyrocketing crops

Key points:

- During the last two weeks, there has been a historic cluster of selling pressure

- The number of indicators showing pessimism has spiked

- New lows have been overwhelming new highs, especially in tech stocks

- Small traders are betting against the market, as dealers take the other side

- Foreigners are selling U.S. stocks to a historic degree

- Wall Street analysts are downgrading S&P 500 company price targets, and have been consistently

- A big worry - the long-term trend has changed for the first time in years

- Energy stocks are facing some cross-currents

- Corn and wheat have spiked but now enter a weak seasonal window

- The momentum of agricultural contracts has been historic

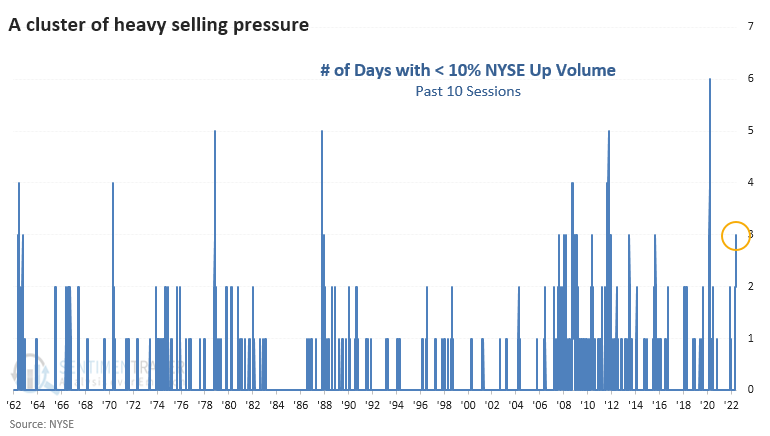

A severe selling cluster

The sheer overwhelming selling pressure over the past two weeks has been remarkable. When stocks drop, almost everything drops. And volume has been almost entirely one-sided. Wednesday marked the third session in ten days when less than 10% of NYSE volume flowed into advancing securities, among the most clustered bouts of severe selling in 60 years.

Such severe selling clusters tended to coincide with exhaustive climaxes and positive future returns, with the glaring exception of the financial crisis when it was a regular feature.

What's depressing about Wednesday's session is that it occurred so soon after investors had been so aggressive the other way. On Friday, more than 90% of volume flowed into advancing stocks. An old market cliche is that we only see severe reversals like this during bear markets. Well, maybe, but if that's the case, it was an excellent time to be a buyer because the S&P sported double-digit gains over the next year.

This has been a remarkable stretch of volatility in breadth data. The figures have become more volatile over the past 20 years but this still ranks as one of the most significant clusters of extreme volume flows since 1962. Similar clusters tended to precede positive medium- to long-term returns, but they also triggered relatively early in bear markets in 1973 and 2007.

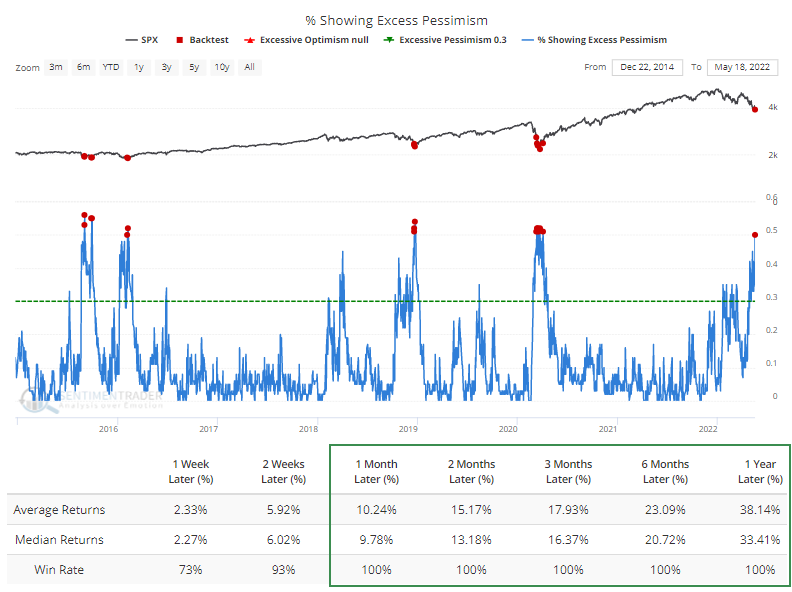

We already know that sentiment is washed out, but pessimism became even more widespread during Wednesday's session. For one of the few times since the financial crisis, half of our indicators were showing extreme pessimism. After the others, returns were excellent.

Going back to when we started calculating this, it's not as pretty of a picture for bulls. It mainly occurred during short-term bottoms, but with the notable exceptions of the waterfall declines during July 2002 and October 2008. The biggest caveat is that we had fewer indicators then, so seeing more than 50% of them at extremes was easier.

Maybe the selling was so bad it's good

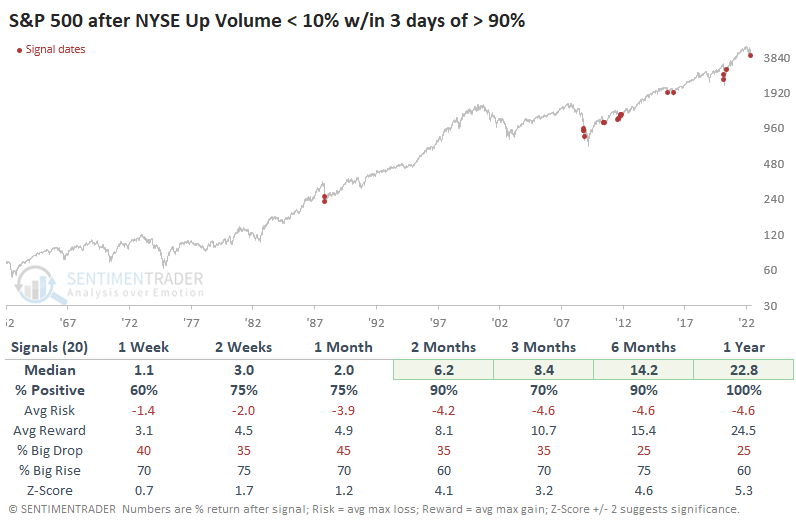

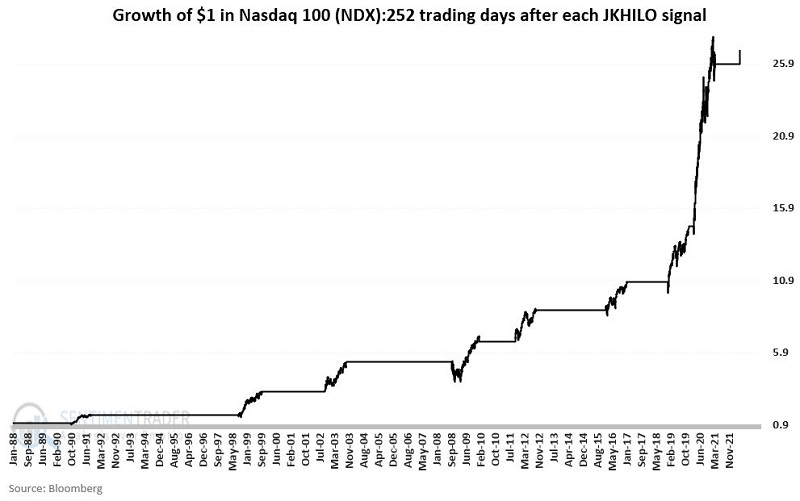

When 52-week lows overwhelm new highs, it is typically a sign of a "washout" and often marks the ending portion of a bear market. An indicator that Jay developed many years ago gave a bullish signal on May 12.

Decades ago, Norman Fosback developed an indicator called The Hi/Lo Logic Index. Gerald Appel developed another indicator using daily high and low data. Jay combines the two into a compelling and robust indicator of its own, "JKHiLo."

There are various ways to interpret JKHiLo readings, but the most important thing to note is when the daily reading drops to an excessively low level, which it now has.

Jay looks for a drop below 10.0 in JKHiLo to signal a potential turning area for the stock market. The table below displays when JKHiLo dropped below 10 for the first time in six months and future returns in the Nasdaq 100 (NDX).

The main thing to jump out is the performance of the NDX 6, 9, and 12 months after a signal. Each of these periods is marked by a 100% Win Rate and very robust returns. However, the first three months after a signal can be a different matter, as we will discuss in more detail momentarily.

The chart below displays the growth of $1 invested in NDX (this can be emulated by trading ticker QQQ which tracks the Nasdaq 100 index) held for 252 trading days after each signal (including overlap signals on 10/8/1998 and 1/23/2009).

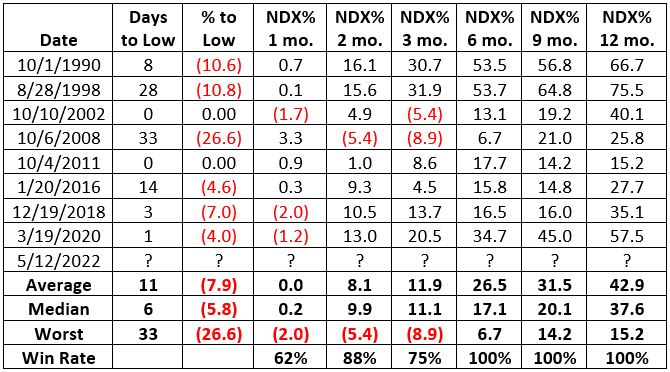

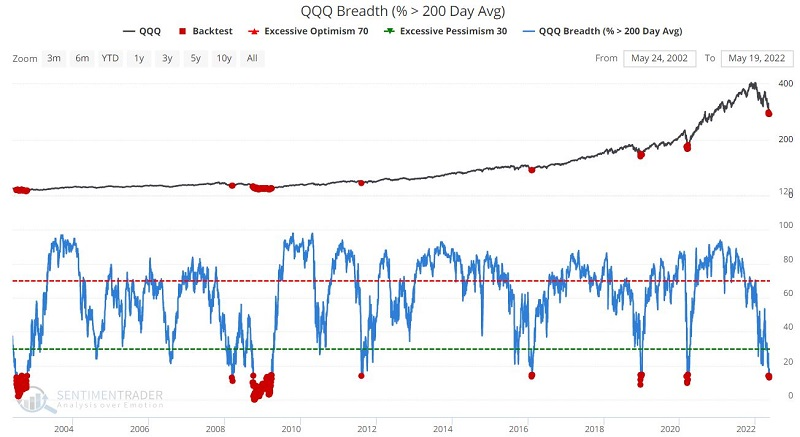

Jay also noted that long-term trends among stocks in the NDX are deteriorating quickly. By late this week, fewer than 15% of stocks were still holding above their 200-day moving averages.

The numbers are aided somewhat by the fact that there were many days below 15% leading up to the 2002 and 2009 lows. Signals in 2002 and 2008 were followed by extreme drawdowns between the initial signal and the actual low. If we only look at the first cross below 15%, then overall returns decline, but there was only one loss over the next year, from 2008.

Another positive - extremely negative sentiment

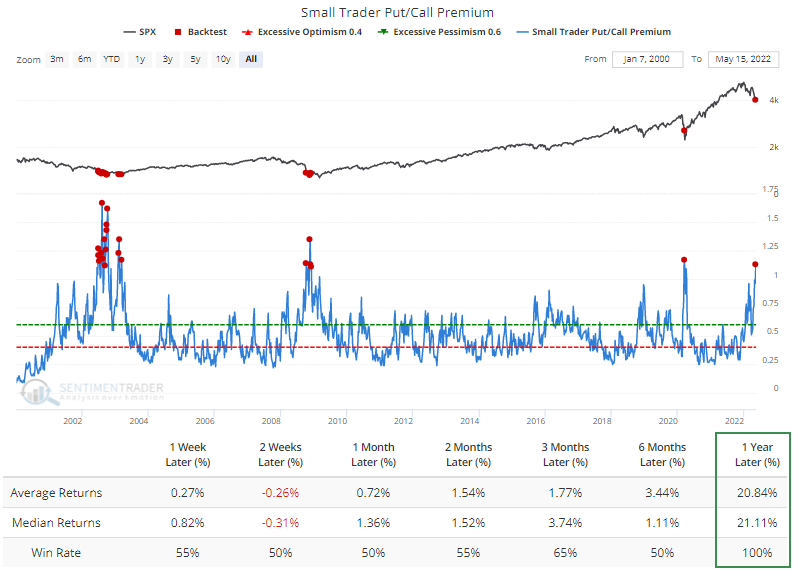

Small traders are getting awfully nervous. And now they're willing to pay up for the right to protect against a crash.

For only the 7th time in 22 years, last week, the smallest options traders spent 30% or more of their volume buying put options to open. The premiums that small traders paid for protection were more than 10% higher than the premiums they paid for call options.

It's extremely rare for retail traders to pay more in premiums for put protection than for speculating on rallies. The S&P 500 rallied over the next year after every time they did so, averaging a healthy return of 21%. The only precedents are all-out market crashes, so there was a lot of volatility in the short term.

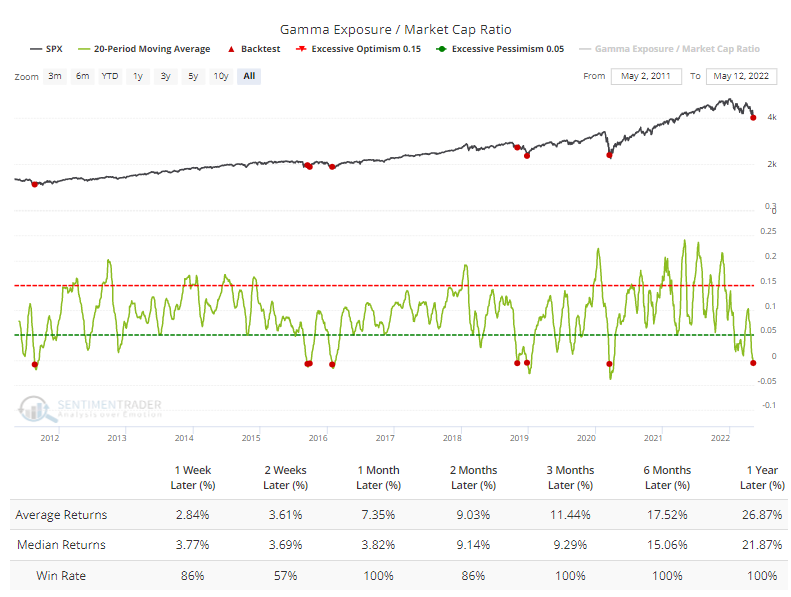

Their bearish bets have been building for weeks, and somebody has to take the other side of those trades. That often means dealers on Wall Street, who then have to hedge their exposure by buying or selling underlying stocks.

Because of that effect, the 20-day average of Gamma Exposure has dropped below -1% of the market value of U.S. stocks. Every time this happened before, the S&P rallied in the months ahead. We only have data from 2011, so there is no telling what this might have meant in 2002 or 2008.

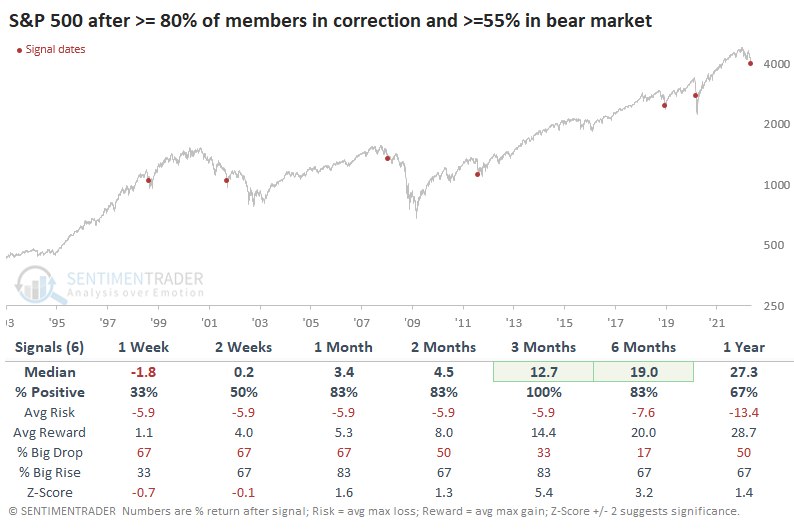

All of this betting against stocks by retail investors comes as more than 80% of stocks in the S&P 500 fell into correction territory (more than 10% off their 52-week high). For stocks that are losing, more and more are losing badly. As of late last week, more than 55% into bear markets (off more than 20% from their highs).

The table below shows S&P 500 returns whenever more than 80% of S&P 500 stocks were in a correction, and more than 55% were in a bear market. While this occurred about midway through the 2000-02 bear market and early on in the 2008 bear, the S&P 500's returns during the next three months were positive every time due to relief rallies.

The S&P 500's (almost) bear market

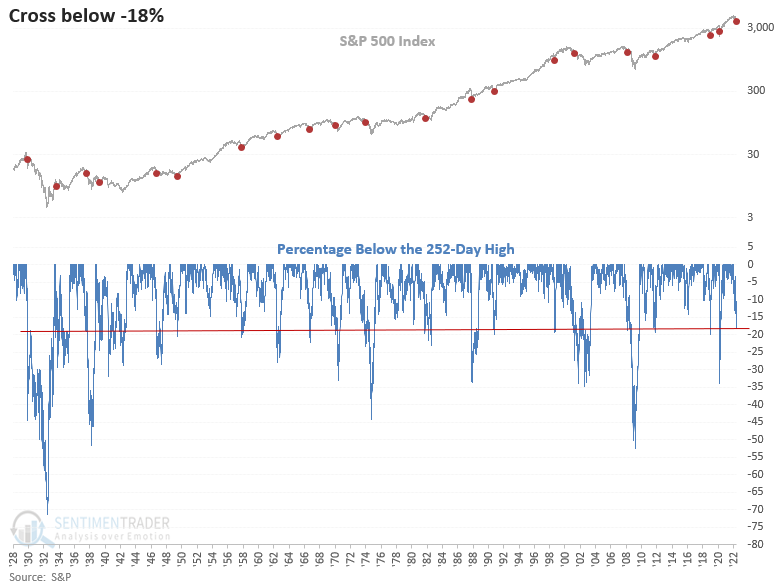

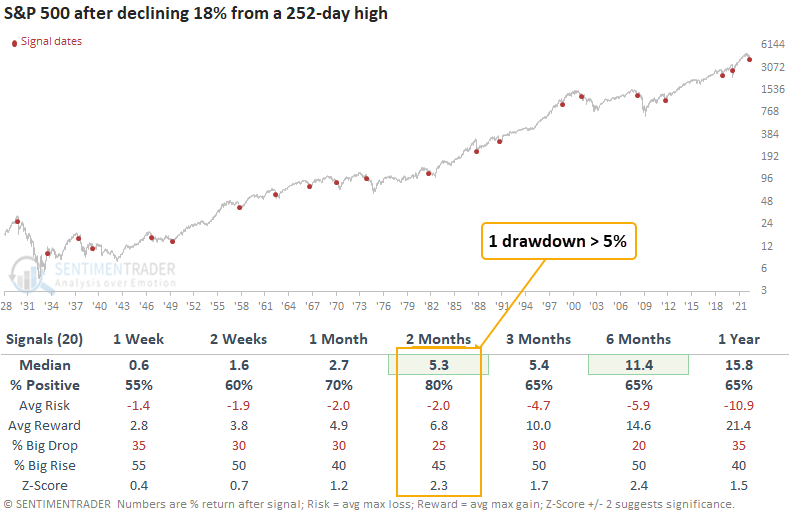

The S&P 500 closed down 18% from its 252-day high last week. Dean showed that after similar signals, the index closed higher 80% of the time 2 months later.

This study generated a signal 20 other times over the past 93 years. After the others, S&P 500 future returns, win rates, and risk/reward profiles look solid across almost all time frames.

The key is that if we're in a positive long-term market environment (increasingly dubious) then these have been good buy signals. When returns continue to slide in the weeks and months ahead, it has indicated persistent bear market conditions.

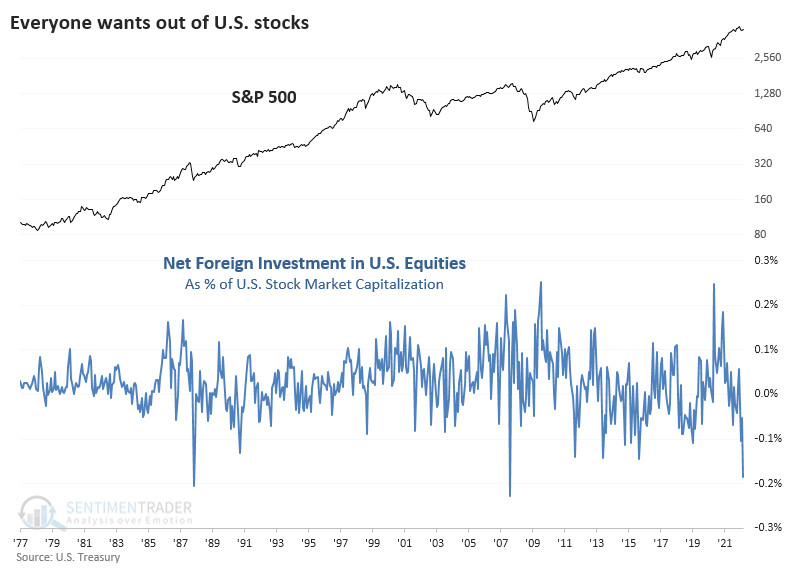

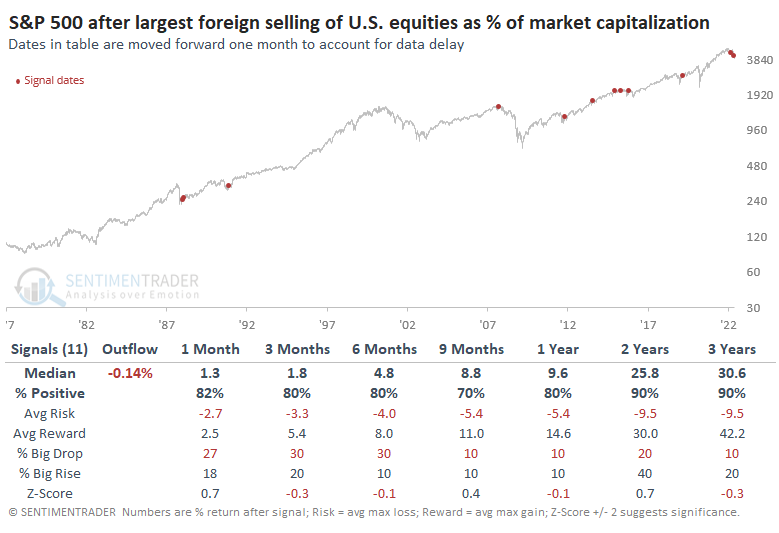

Concerns about a bear market cause foreigners to flee

Everyone wants out of the U.S. Despite claims that the U.S. is the only relatively safe place to be, and despite a rising dollar, sentiment toward U.S. stocks is horrid. That's true among people that live here and people that don't.

According to the U.S. Treasury in a just-released report, foreign investors pulled a stunning $90 billion from U.S. equities in March. That's more than double the previous record outflow...and that was just in January of this year. It's likely gotten worse since then.

The gigantic outflow was a record in absolute terms, but even when expressed relative to the total market capitalization of U.S. stocks, the recent outflow still ranks as the 3rd-largest since 1977.

After the most significant outflows, the S&P 500 tended to rebound. The dates in the table are moved forward one month to account for the delay in reporting from the Treasury.

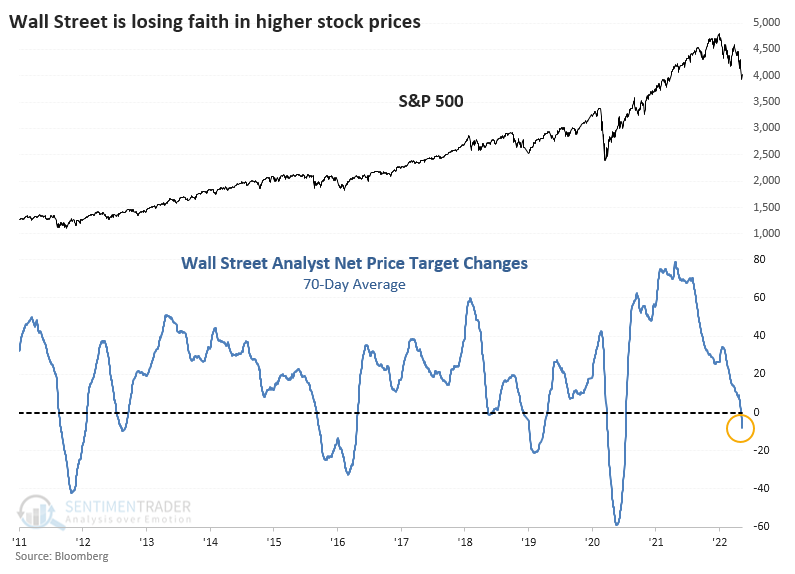

Even Wall Street is bailing

Stocks are losing some of their biggest supporters. When you lose Wall Street, then you know things are bad.

While they haven't yet gotten to the point of panic, analysts on Wall Street have been busy downgrading the price targets on stocks they follow within the S&P 500. Over the past 70 sessions, the net number of their price target upgrades versus downgrades has fallen to an average of -8.

By the time a 70-day average of net price target changes fell to the current level, it's been at about the peak of selling pressure during past corrections. Even though data is limited, it's worth noting that while analysts have been consistently knocking down the price targets of companies they follow, they haven't been as busy reducing earnings estimates. In other words, analysts hate the technicals of stocks they're following but seem to be okay with the fundamentals.

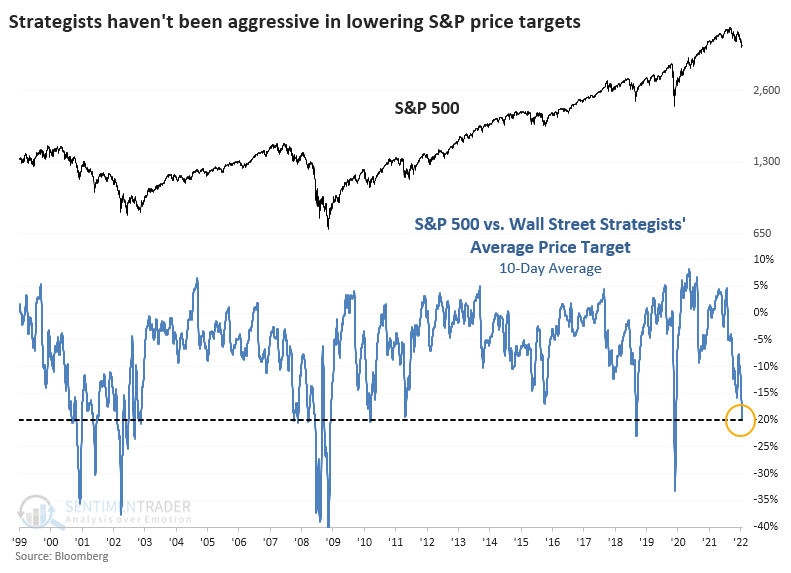

Wall Street analysts tend to work from the bottom up, monitoring and estimating earnings trends for individual companies and sectors. Strategists tend to work from the top down, looking at wide-ranging macro factors and potential impacts on earnings for entire countries or indexes.

Similar to when we looked at this after the late 2018 sell-off, analysts are downgrading price targets heavily on individual stocks, while strategists haven't been as aggressive in lowering their price targets for the S&P 500 index. Over the past ten days, the S&P's price has traded at a 20% discount to the average year-end strategist target.

In the past, we've highlighted the historical importance of the S&P falling to a 20% discount from the average strategist price target. Stocks have tended to rebound from such severe discounts.

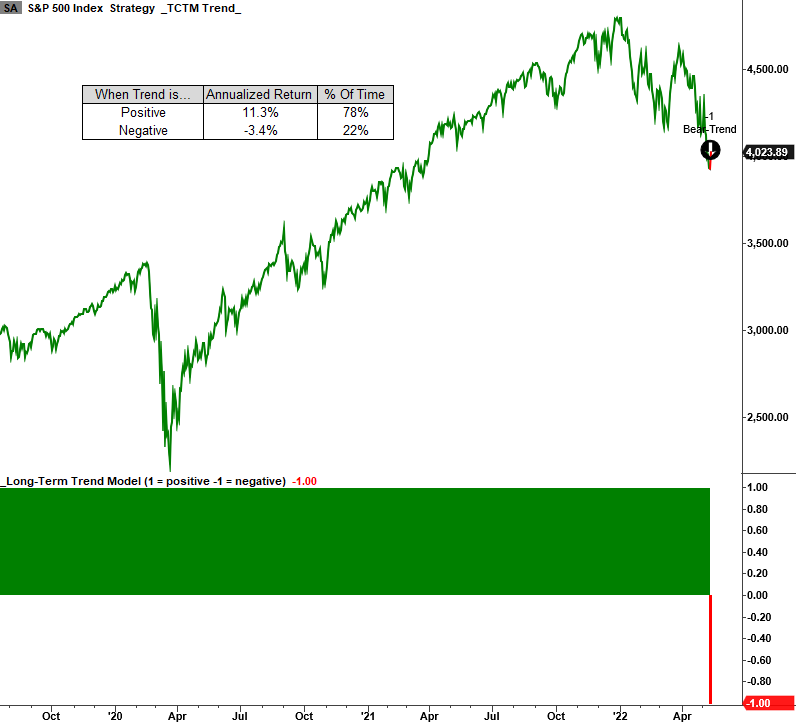

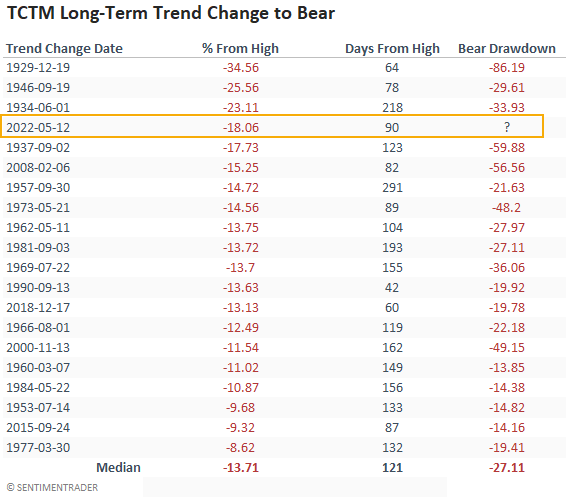

One big worry - the long-term trend has change

Dean's TCTM long-term trend model flipped from bullish to bearish on May 12. The trend change moves the overall TCTM status from cautious bull to negative. It's now imperative to monitor the recession composite model, which recently triggered a new alert. Recessionary bear markets typically see more significant drawdowns.

The TCTM is not a pure black-box model that says we should be all in or out. And it should act as a complementary tool to your research process. Annualized returns are unfavorable when the model is negative, -3.4% versus +11.3% when it's positive.

The long-term trend model change occurred when the S&P 500 was down 18.06% from the index peak. Comparing the current trend change to other signals shows one of the most significant drawdowns in history. After similar trend change drawdowns, the overall bear market decline looks troubling.

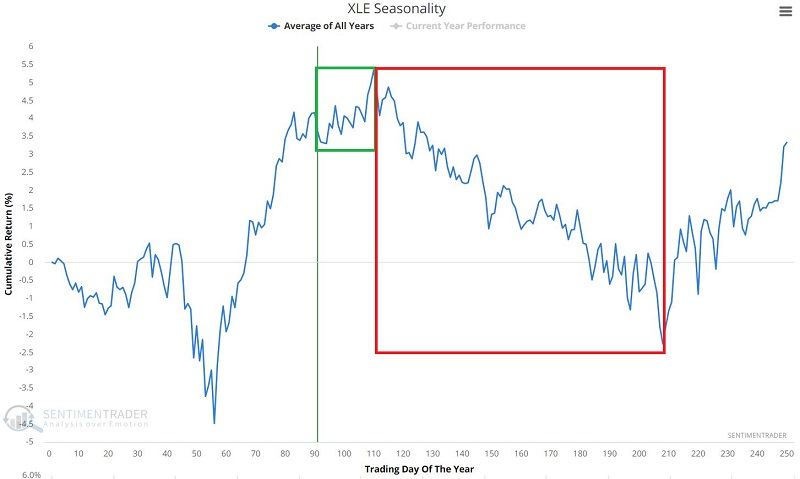

Cross-currents in Energy stocks

Jay looked at some cross-currents in the Energy sector. While there is a high level of correlation among stocks in the sector (usually a positive for future returns), there are some headwinds.

Historically, the energy sector has been one of the more reliably cyclical sectors - showing strength in the 2nd quarter and weakness - often significant - in the second half of the year. The chart below displays the annual seasonal trend for XLE.

The seasonally favorable period runs through June 11th and the unfavorable period runs into mid-October. However, one must remember that seasonality is "climate, not weather" and that the chart above is NOT a roadmap but merely a visual representation of the average of years in the past.

Corporate insiders of the companies held by ticker XLE have been doing a lot of selling in recent months. The chart below displays those weeks when our more than 90 insiders in Energy companies were selling shares in the open market over the past six months. The sector struggled after other high readings.

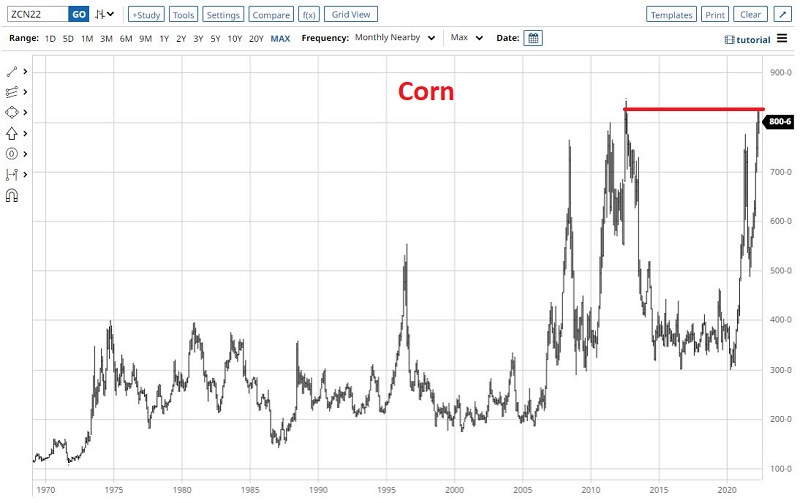

Decision time in some agricultural commodities

Coffee, Corn, U.S. Dollar, and Wheat have all recently established an obvious line of price resistance. Jay noted that each of these markets is soon to enter a seasonally unfavorable period. Traders in these markets should be very alert to the potential for a sharp downside reversal in the weeks and months ahead.

The chart below displays a long-term chart for corn futures and a relevant price resistance line.

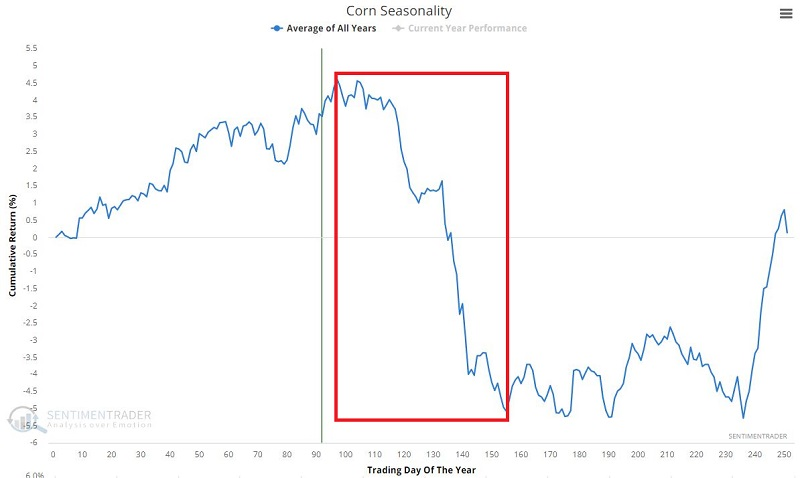

The chart below displays the annual seasonal trend for corn futures. Note the impending period of seasonal weakness. For 2022 this period extends from the close on May 20 through the close on August 12.

This period showed a positive return during 27 years and a negative one during 54 years. The average, median, and maximum losses were all larger than their positive counterparts.

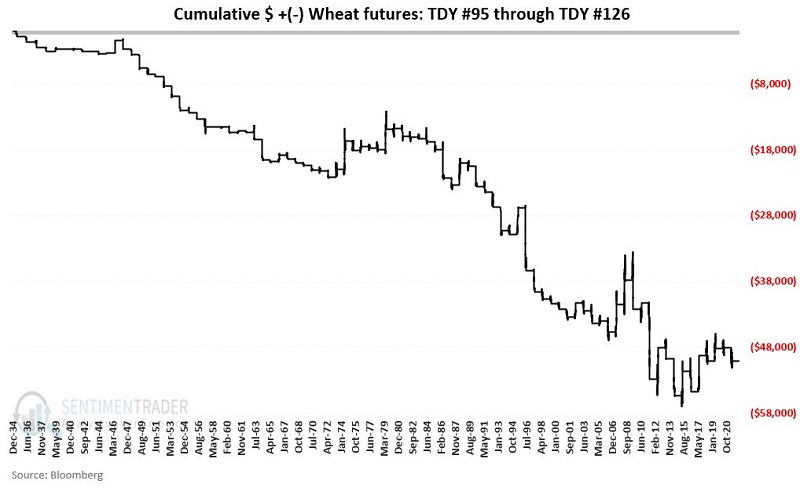

The chart below displays a long-term chart for wheat futures and a relevant price resistance line.

Like corn, wheat is facing a weak seasonal window. For 2022 this period extends from the close on May 18 through the close on July 1.

The chart below displays the hypothetical return achieved by holding a long position in wheat futures only during this period every year since 1935.

The "obvious" play for each of the markets highlighted above is to look to play the short side during the seasonally unfavorable period as long as the price remains below the indicated resistance level. The most important keys are to a) make sure the dollar risk between any short entry price and a stop-loss price above resistance is within a trader's tolerance for risk and b) resolve to exit the trade if resistance is pierced and not wait around "hoping" for a reversal.

A concern for shorts is the monster momentum that ag has shown

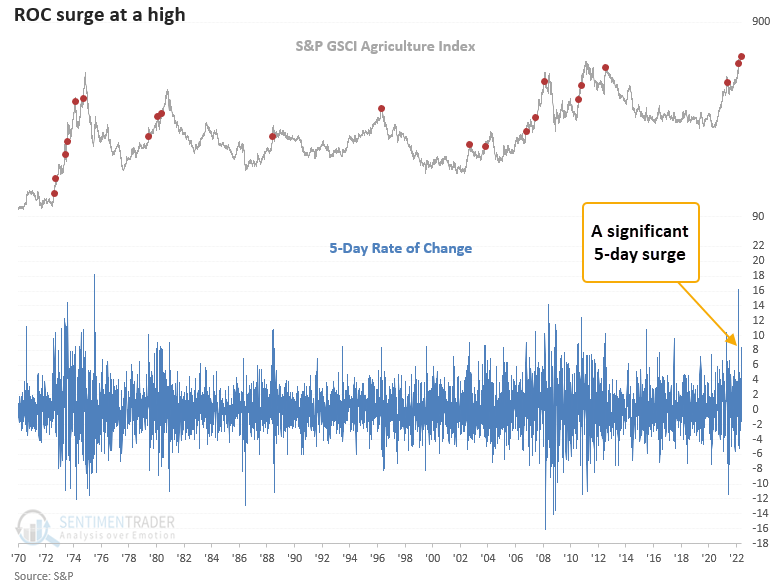

An index of agricultural commodities surged 8% over a 5-day period while closing at a 252-day high. Dean showed that similar conditions preceded rising food prices, especially over the next three to six months.

The Dollar Index is surging as the Federal Reserve has increased the benchmark fed funds rate twice and intends to raise rates even further to tame inflation. Usually, that would be an unfriendly environment for commodities. However, they continue to defy the odds, and it looks like food prices could go higher despite the record run. On Tuesday, a basket of agricultural commodities surged 8% to a new all-time high.

Agricultural commodities tend to see a cluster of short-term surges during bullish trend environments.

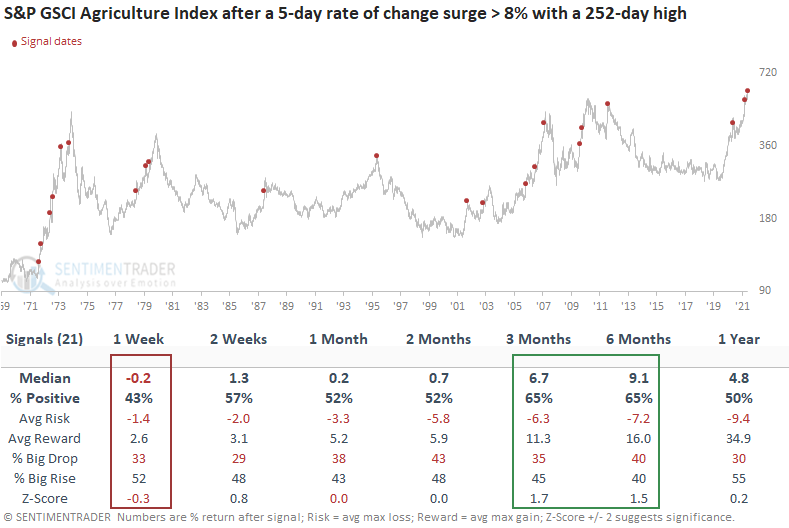

This study generated a signal 21 other times over the past 50 years. After the others, agricultural commodity returns were positive across all time frames except for the 1-week window. The 3 & 6-month time frames show solid returns, win rates, and z-scores, which means we may not get relief anytime soon for our grocery bill. 1996, 2002, and 2012 are the only instances where we saw an almost immediate price peak.

Because of the imminent weak seasonal windows in corn and wheat (and several other contracts), if this momentum is going to relax, now is the time for it to do so.

About TradingEdge Weekly...

The goal of TradingEdge Weekly is to summarize the research published to SentimenTrader over the past week. Sometimes there is a lot to digest and this summary is meant to highlight the highest conviction or most compelling ideas we discussed. This is NOT the full research that's published, rather it pulls out some of the most relevant parts. It includes links to the published research for convenience; if you don't subscribe to those products it will present the options for access.