Thursday Color - Russell vs S&P Volatility, Summation Extremes, IWM Inflow, AAII Bulls

Here's what's piquing my interest so far today. Indexes are nearing new highs, but the number of securities also hitting highs is lagging pretty badly. Troy mentioned this the other day and it may be even more of a shorter-term worry for the next couple of weeks if it continues.

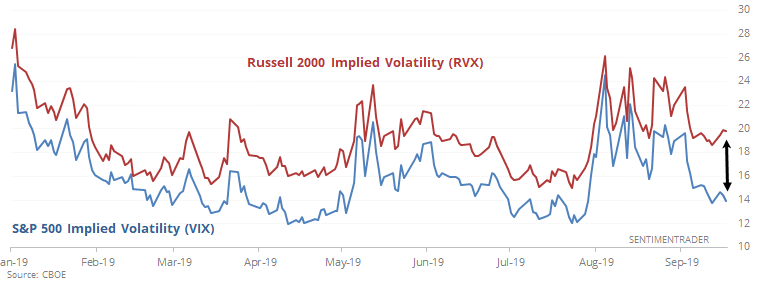

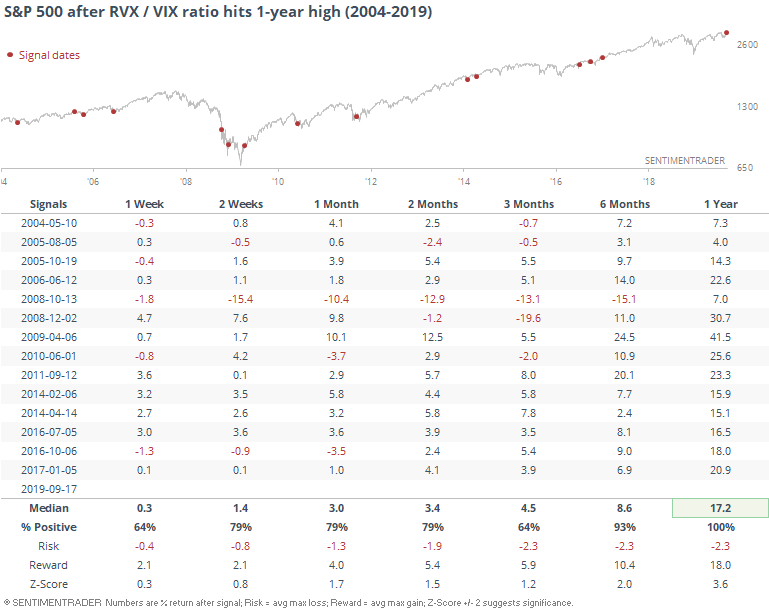

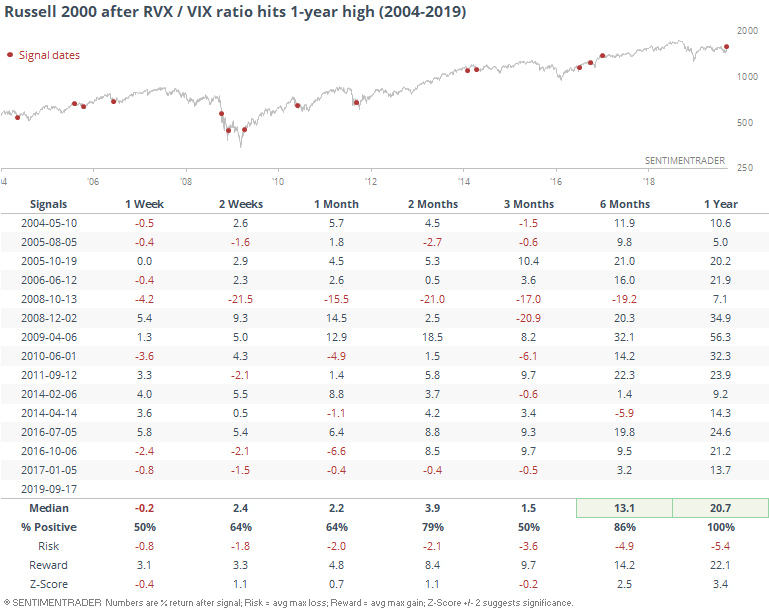

Volatility Divergence

The WSJ notes that traders are pricing in higher (and rising) volatility for small-cap shares, while lower expectations for larger-cap ones. That has caused the "VIX" for the Russell 2000 to diverge from the one on the S&P 500.

If traders are right and small-caps get hit by still-higher volatility, that could weigh on the market. But other times the difference between the two got so wide that it hit the widest level in at least a year, it didn't show any drag on the S&P 500's returns.

Or the Russell 2000's.

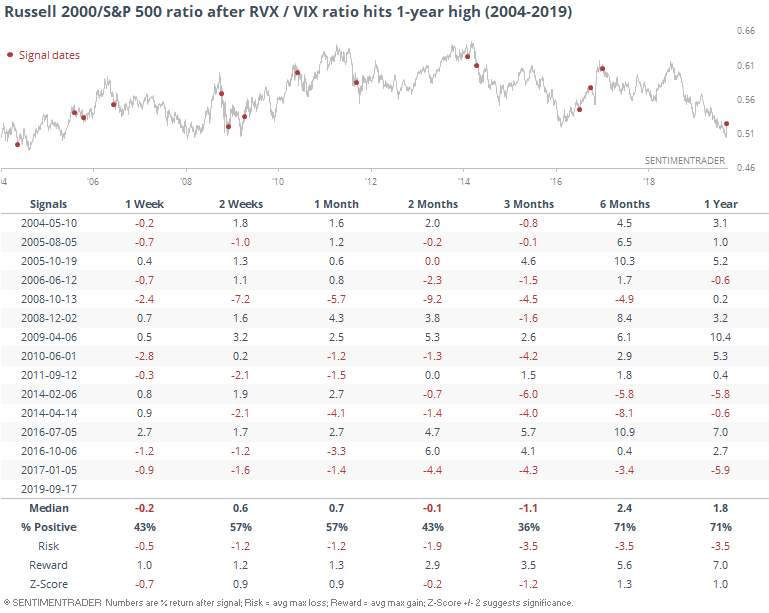

The ratio between the two indexes showed mixed results. Over the next 2-3 months, the Russell lagged behind the S&P, but longer-term, the Russell out-performed.

Super Summations

We've looked at long-term breadth momentum in several indexes over the past few sessions, via the McClellan Summation Index. A couple more are making notable moves.

The German DAX Summation Index has moved above +1,000 for the first time in years. That should be a good long-term sign that buying interest in that market has moved to a new threshold. And, generally, its longer-term returns after other instances were good. If we use the Backtest Engine to look at other times the indicator crossed above that level, ignoring any clusters within months of each other, then the DAX rose 79% of the time over the next three months.

To run this same study, just click here then press the Run Backtest button and click the Multi-Timeframe Results tab.

An interesting wrinkle is that all 3 times the DAX showed a negative return over the next three months were times when sellers stepped in immediately after breadth momentum hit this high of a level. The suggestion is that if buyers show enough gumption to keep buying in the coming week, then it bodes well longer-term, too.

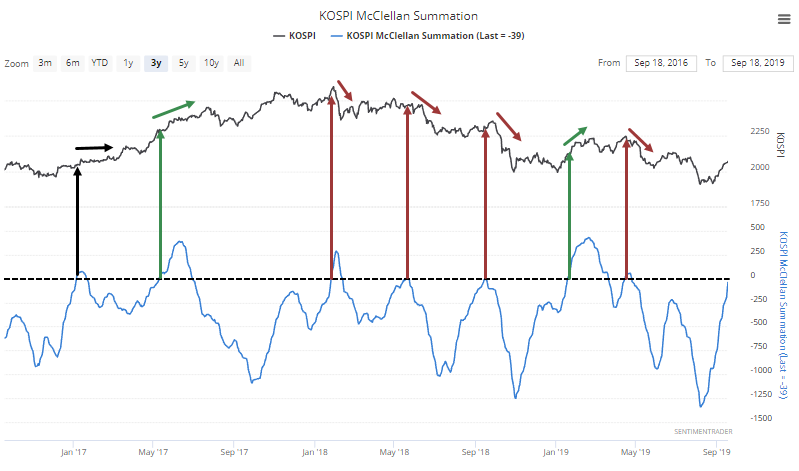

The South Korean Kospi index is another overseas index seeing its Summation Index hit the highest level in months. It's trying to turn positive, which has led to a struggle in that market in recent years. Bulls would definitely want to see this become positive and the market hold up, otherwise it's just more of the same.

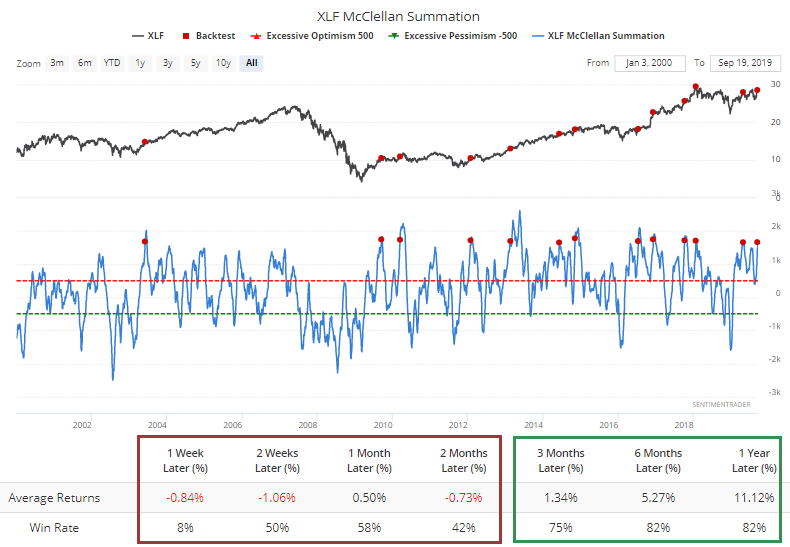

Among U.S. sectors, the Summation Index for financials is the highest relative to its recent past. That has preceded a further gain for XLF over the next week only once out of 12 times, and weaker-than-average returns even up to a couple of months later, but decent gains longer-term.

Small-Cap Revival

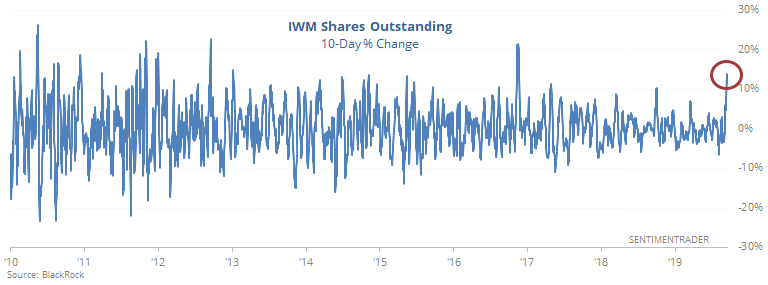

ETF traders seem to have found affection for small-cap shares again. The IWM fund has seen steady inflows over the past couple of weeks and its shares outstanding have hit their highest level of the year.

Its shares have expanded by more than 14% in only 10 days, one of its largest, fastest expansions since the financial crisis.

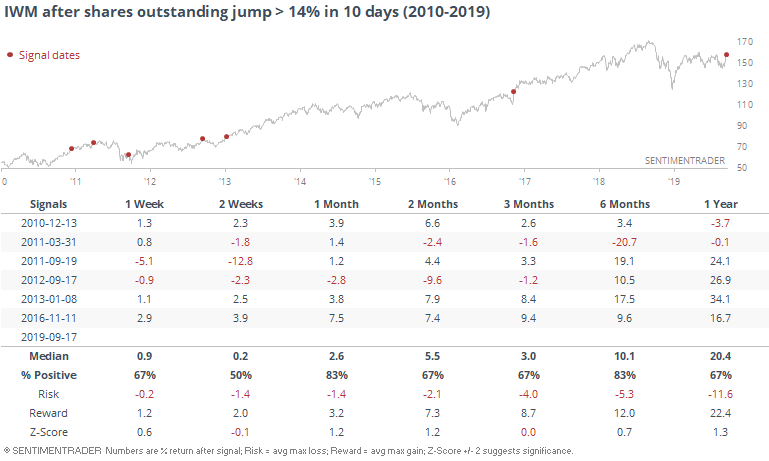

Knee-jerk contrarianism would suggest this is a bad sign of "dumb money" ETF traders rushing in after a rally. Empirically, it's hard to prove that. Other large jumps in shares outstanding have not been a consistent contrary indicator.

It was a very bad sign in 2011 both times (eventually), and again in 2012, but the others led to gains. Very roughly, when we see this kind of activity after a long period of decline or consolidation, it tends to be more of a positive than negative.

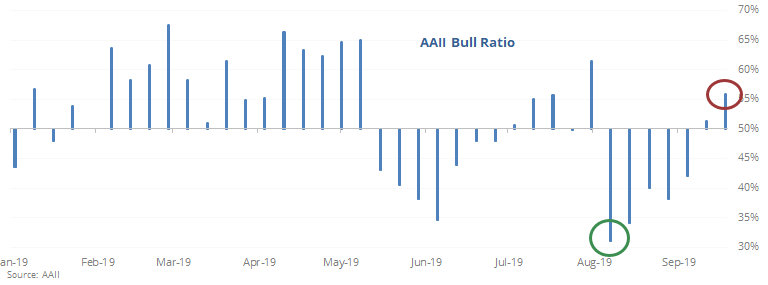

Bulls Coming Back

The latest AAII survey shows another sense of renewed optimism after a suspiciously deep period of pessimism in August. The Bull Ratio has gone from barely above 30% to above 55%, the highest since July.

Typically, rising optimism is a good thing until it reaches an extreme, which it's not yet at. That's especially the case when the rise comes from a very low level.

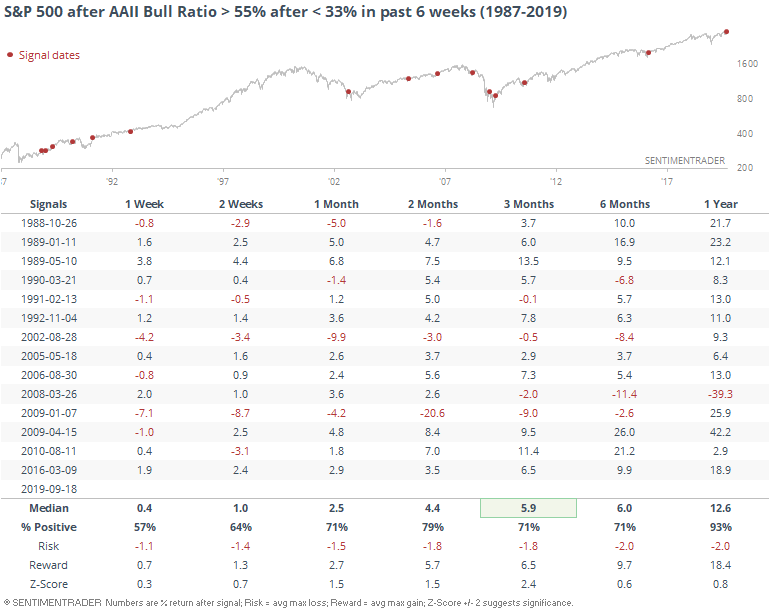

Below, we can see each time that the Bull Ratio cycled from below 33% to above 55% within 6 weeks.

Returns for the S&P 500 going forward weren't spectacular, but they were above random, with the best being over the next three months. A year later, there was only a single loss, but it was extremely large thanks to the fakeout rally in early 2008.

As Troy notes, individual investors aren't the only ones who've been deeply pessimistic. Even corporate CFOs are showing a large degree of apprehension, usually without merit (in terms of stock prices, anyway).