The yield curve says, "Don't worry"

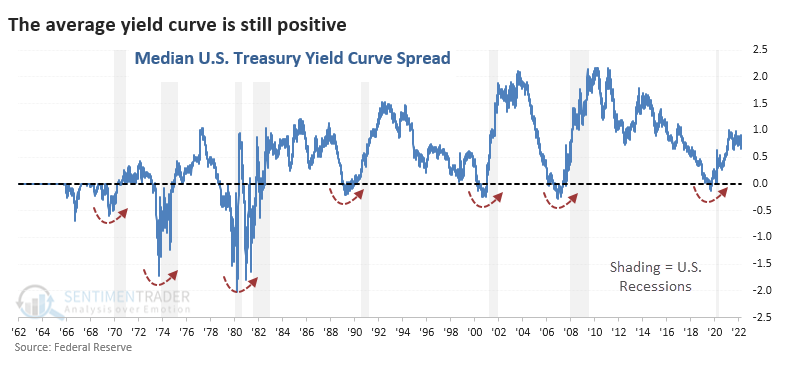

The average yield curve is far from inversion

In early 2019, investors were becoming increasingly concerned about yield curve inversions. As we saw at the time, inversions across the curve were spiking, with several short-term maturities yielding more than longer-term maturities. Using 55 different combinations of Treasury yields from 11 different maturities, more than half of the curves were inverted.

Headlines are stuffed once again with concerns about yield curves. But fewer than 10% of the combinations are currently inverted.

The chart below shows the median spread between the different combinations. This dipped below zero before every recession in the past 60 years. It's still well above that point now; as of Wednesday, the median spread was in the top 29% of all readings since 1962. Since 1982, it's still well above the top half of all days.

Based on where we are now relative to all other days, there's a very low probability that the U.S. would be in a recession across any time frame.

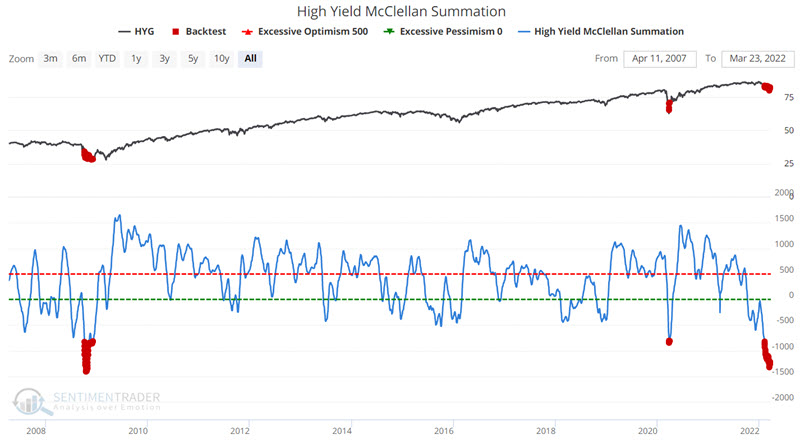

Junk bonds have been acting just like their name

High yield bonds are debt securities issued by companies with lower-quality credit. To attract buyers, these companies pay a higher interest rate on these bonds. As long as the company does not default on the principal or interest payments, these bonds' above-average returns are typically attractive to income-oriented investors.

Because the financial fortunes of the underlying company are so important, the performance of high-yield debt is typically more highly correlated to the stock market than to straight bonds. The overall state of the economy generally has more influence over the action of the high-yield bond sector than fluctuations in interest rates - although large swings in interest rates can still have significant influence.

With the decline in the stock market during the first quarter of 2022, combined with weakness in the overall bond market, the high yield bond sector took it on the chin.

The chart below highlights with a red dot those days when the High-yield McClellan Summation Index was below -800. Note that this is an infrequent occurrence, and as such, we are dealing with an admittedly small sample size.

Other indicators are showing similar long-term washouts in these bonds.