The yield curve is crashing

Key points:

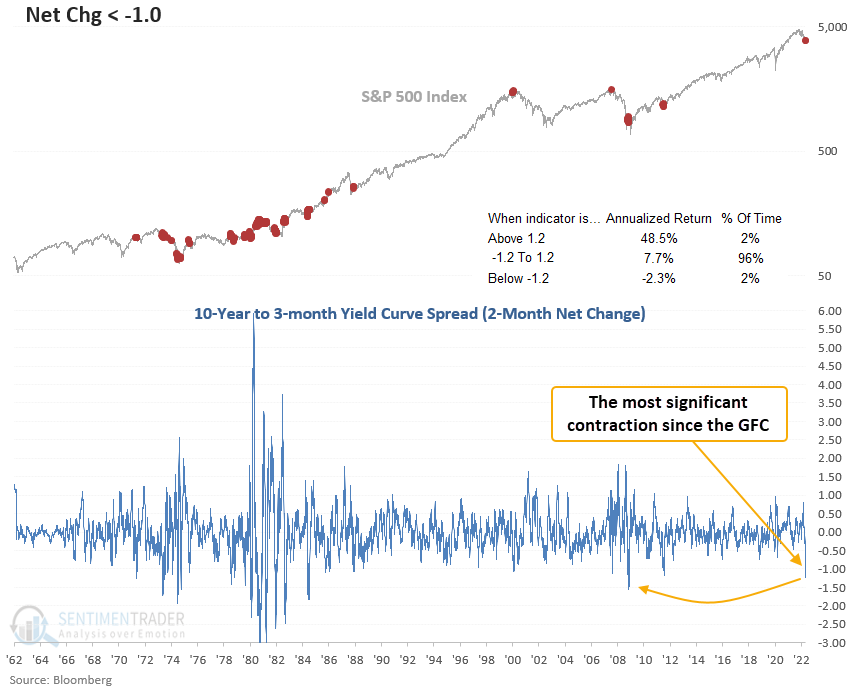

- The 10-year to 3-month treasury yield curve spread has contracted by a significant amount

- When I measure the net change over the trailing 2 months, it shows a decline of 123 basis points

- After similar signals, stocks show flat to slightly negative returns in the 1-2 month time frame

- Commodities and the yield curve tend to decline in the weeks/months following a signal

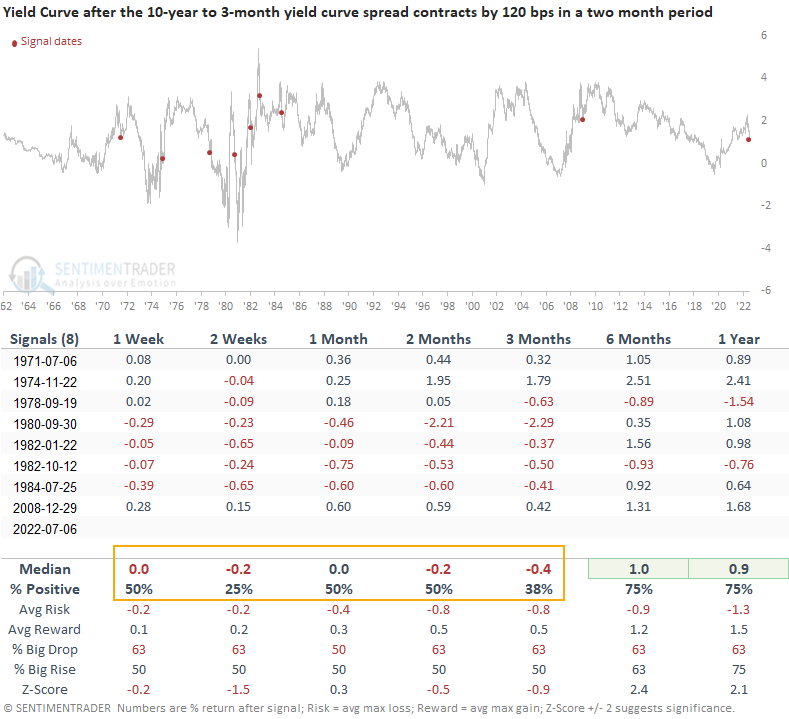

What happens when the 10-year to 3-Month yield curve contracts by a significant amount

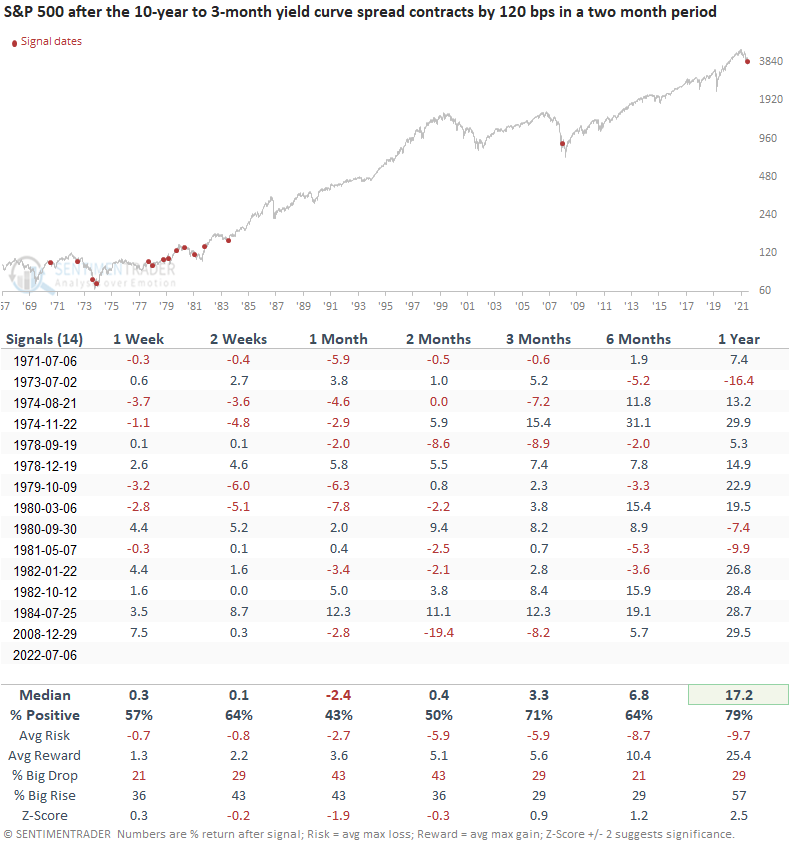

Let's conduct a study to assess the outlook for stocks, commodities, and the yield curve when the 2-month net change for the yield curve spread declines by 120 basis points. I will use a reset that requires the net change to cross above 0% to screen out repeats.

For the first time since the GFC and the 15th time since 1971, the 2-month net change for the yield curve spread has fallen by over 120 bps. Significant contractions of this magnitude have been rare in the last 3 decades. However, they were more prevalent during the inflationary 1970-80 period.

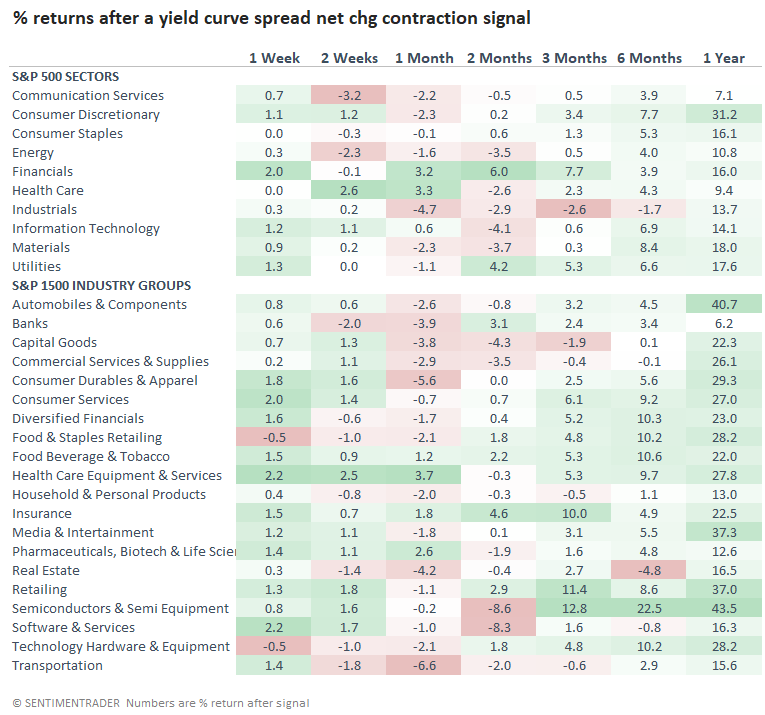

Similar signals preceded flat to negative returns for stocks

This study generated a signal 14 other times over the past 51 years. After the others, the S&P 500 tends to struggle in the 1 & 2-month time frames. The 3-12 month windows look better, especially the 1-year stats.

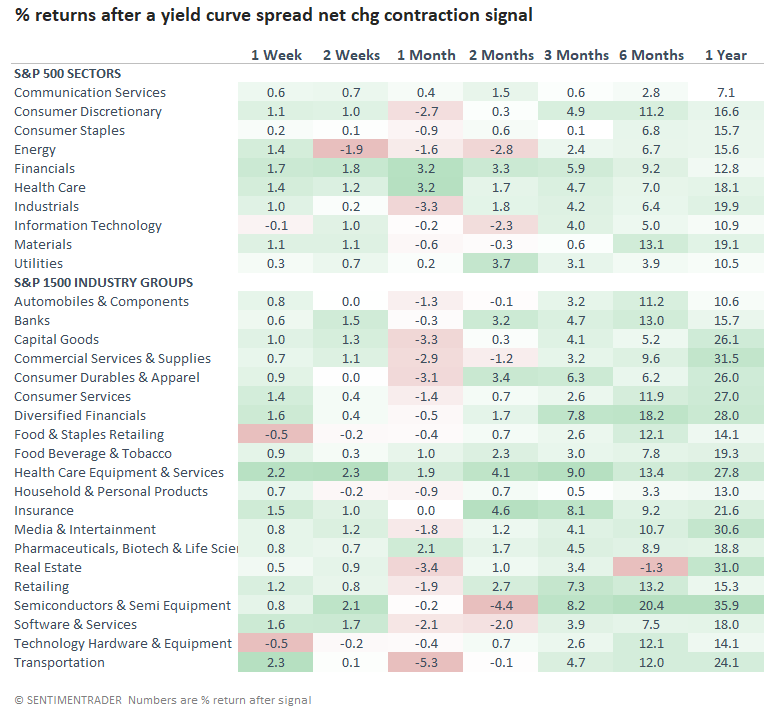

Not surprisingly, a collapse in the yield curve impacts cyclical sectors and industry groups the most. From a defensive standpoint, health care looks the best.

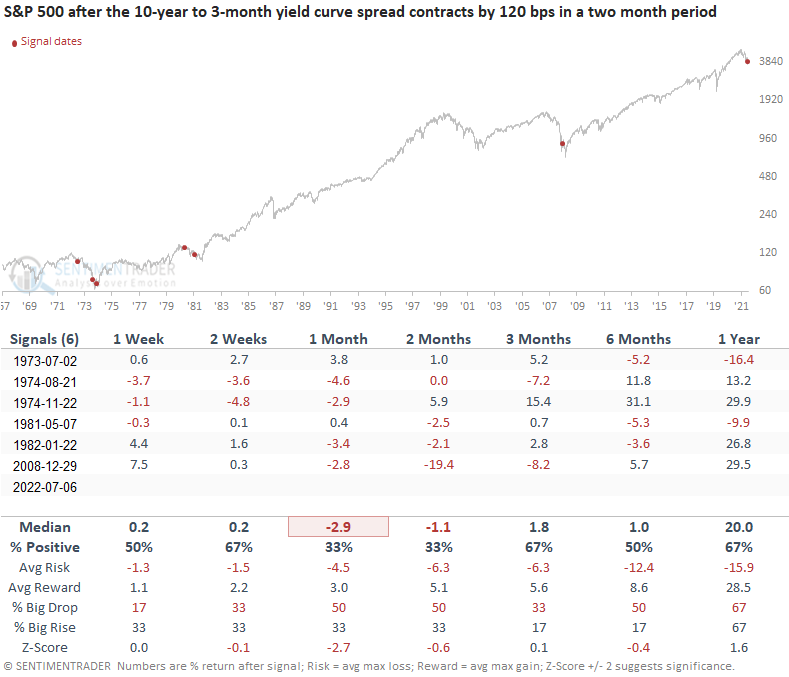

If I isolate signals that occurred in an equity bear market, which is the case now, the stats look a little worse, with negative returns in the 1 & 2-month time frames.

Once again, the bear market signals look unfavorable in the 1 & 2-month time frames across most sectors and industries. Interestingly, financials are one of the betters groups.

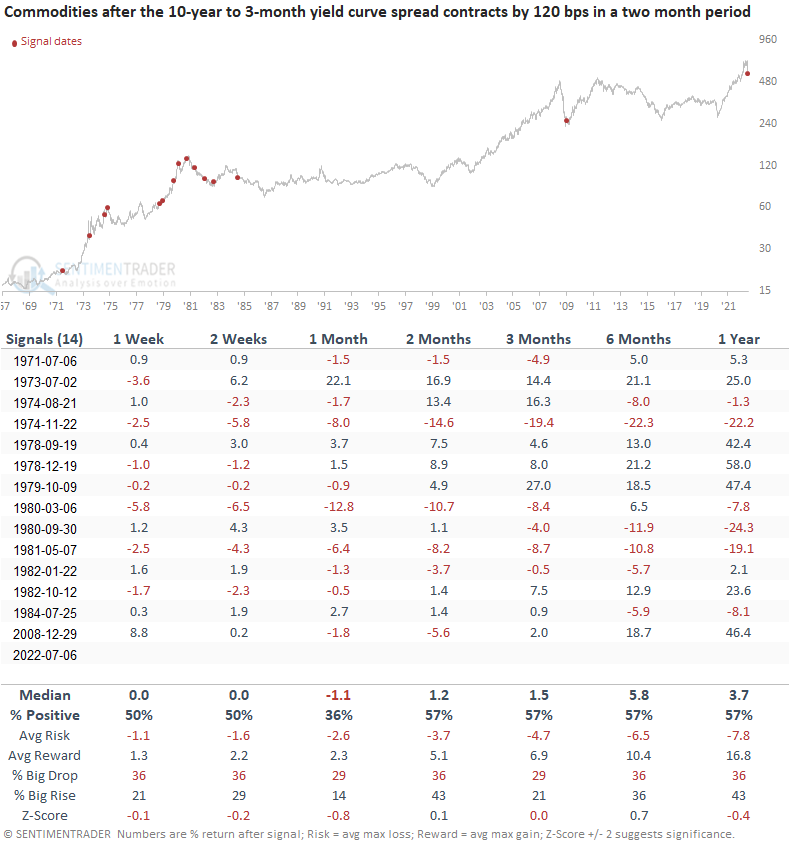

What happens to commodities after yield curve signals

Commodity performance is flat to slightly negative in the first month. A yield curve crash signal shows a loss in 11 out of 14 cases at some point in the first three months.

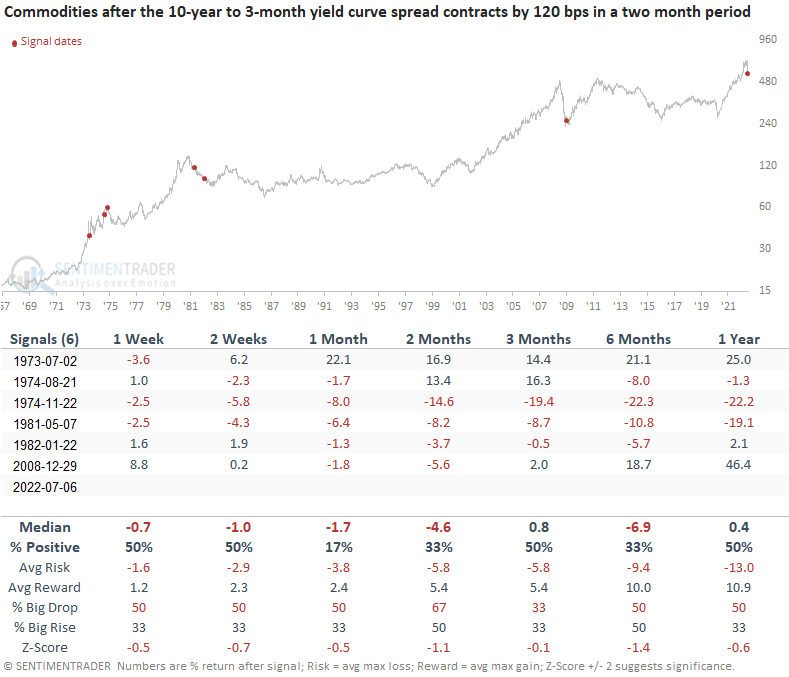

Commodity performance looks significantly worse when the stock market is in a bear market.

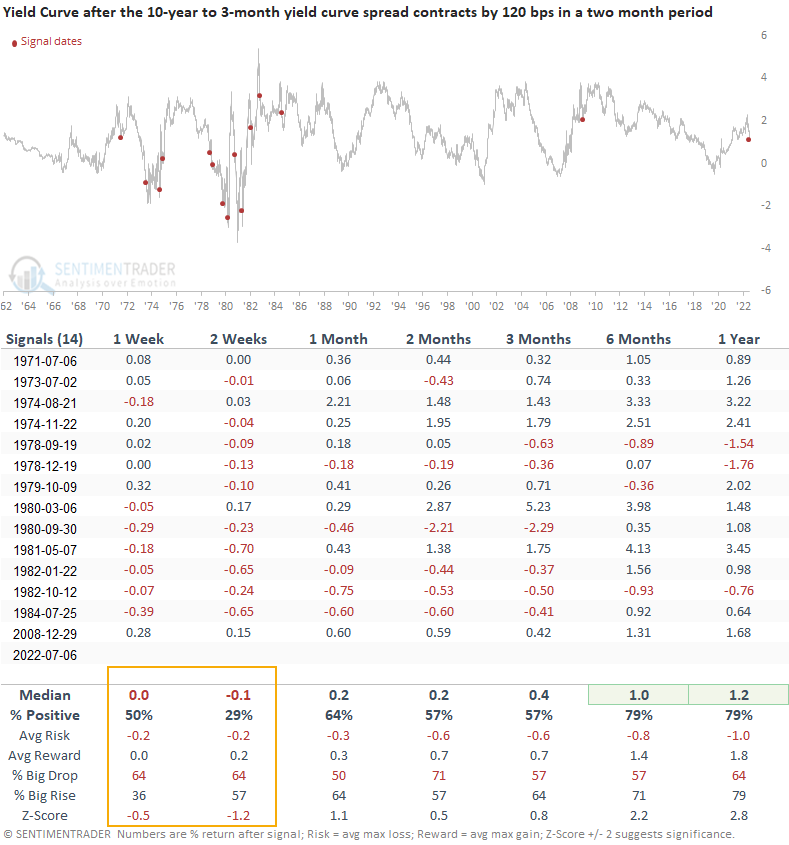

What happens to the yield curve after signals

The yield curve shows a tendency to decline further in the near term. However, the 6 and 12-month time frames suggest the curve could steepen.

Let's add some context to the yield curve table. I will now isolate signals that occurred when the 10-year to 3-month spread was positive. When a 2-month net change signal occurs, and the spread is positive, the yield curve tends to collapse further over the next 3 months.

What the research tells us...

When the 2-month net change for the yield curve spread declines by 120 basis points or more, the downward shift in the curve typically signals a potential softening in economic activity. Similar setups to what we're seeing now have preceded flat to negative returns for stocks and commodities in the 1 & 2-month time frames. Bear market instances look worse for both groups, especially commodities. Applying the signals to the yield curve suggests the curve could contract further, especially in cases with a positive slope, like now.