The U.S. dollar suffers a dramatic decline

Key points:

- The Dollar Index (DXY) has experienced a sharp decline, falling 10% over five months

- Similar downturns led to further near-term losses in the DXY before it staged a rebound

- The S&P 500 rose 80% of the time over six months, aided by strength in multinational sectors

What are the possible effects of a sudden weakening in the dollar's value?

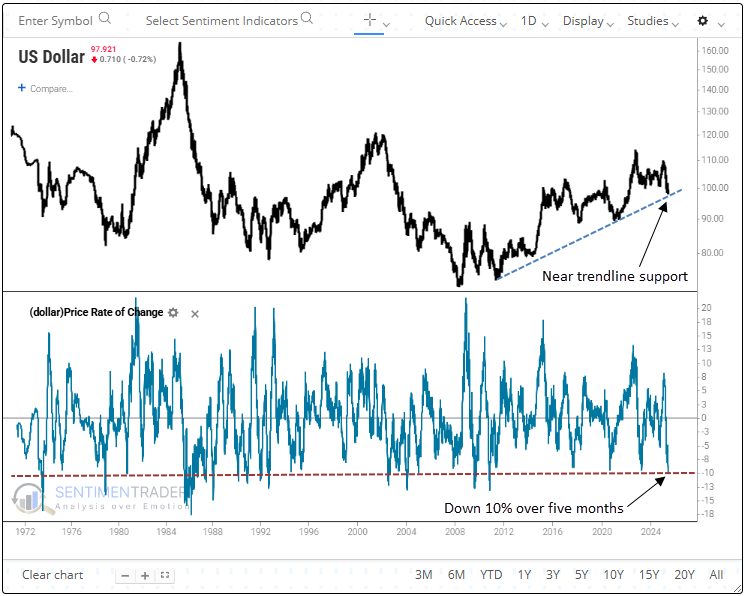

The U.S. Dollar Index (DXY) peaked in January and has since experienced a swift and pronounced decline, falling 10% over the past five months.

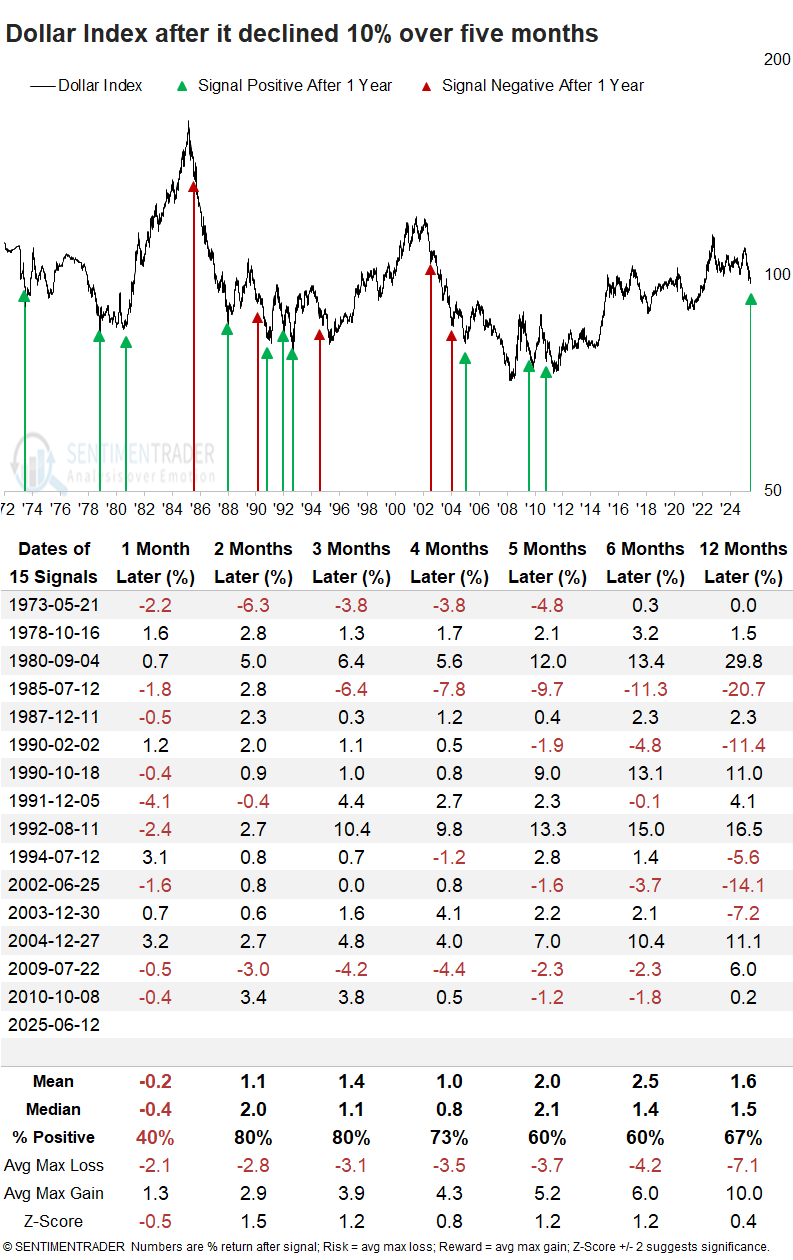

Since its inception in 1971, the dollar has suffered a drop of this magnitude only 15 other times, most recently 15 years ago in the aftermath of the global financial crisis.

Why does this matter? Because a depreciating U.S. dollar can contribute to higher inflation and altered capital flow dynamics, with downstream effects on commodities and equities, particularly among multinational firms and resource producers.

Comparable drops have often resulted in deeper losses before a rebound

A 10% decline in the Dollar Index (DXY) over five months has often led to further weakness in the following month. Yet, this downside momentum usually subsided, as the DXY rebounded in 80% of cases by the two- and three-month mark, with the majority of the gains occurring around the two-month mark.

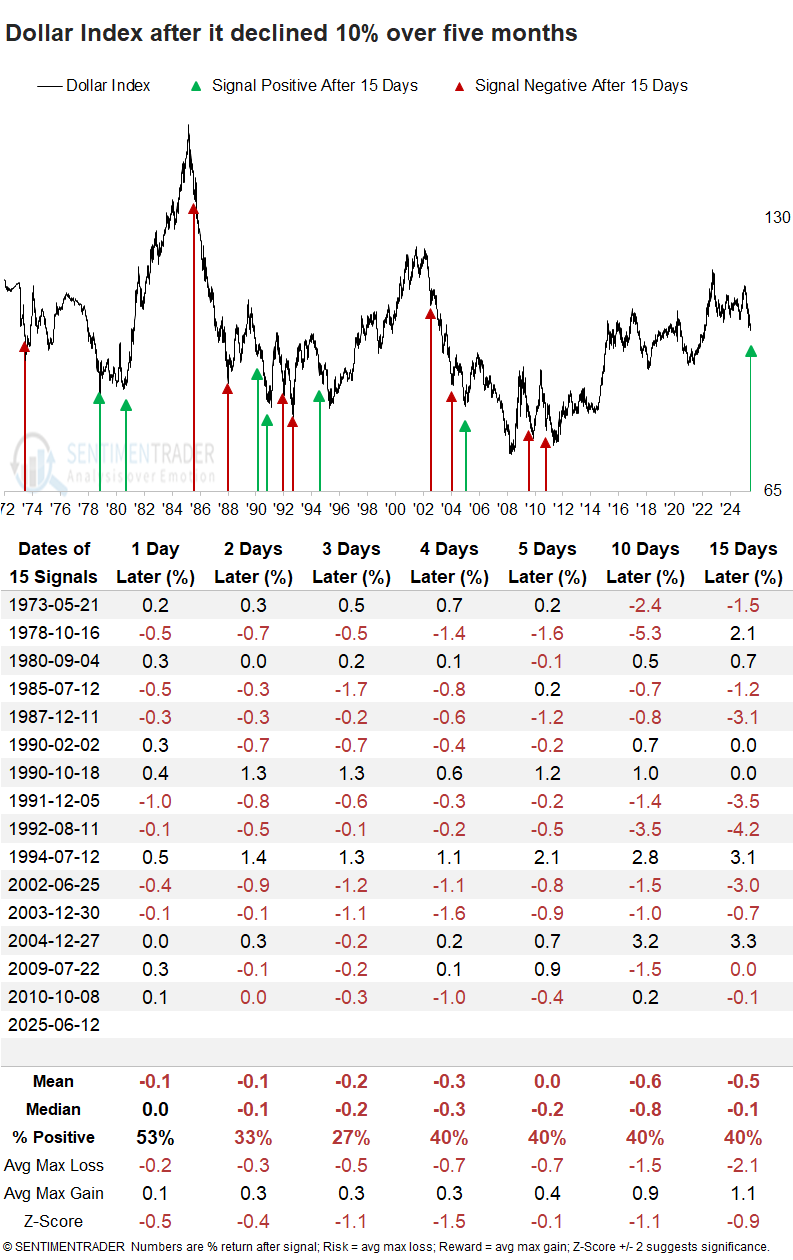

Although the short-term outlook, from one to fifteen days, for the dollar appears weak, the overnight conflict in the Middle East could alter that trajectory, potentially accelerating the rebound that typically emerges over the next two to three months.

Equities tend to benefit from a weaker dollar environment

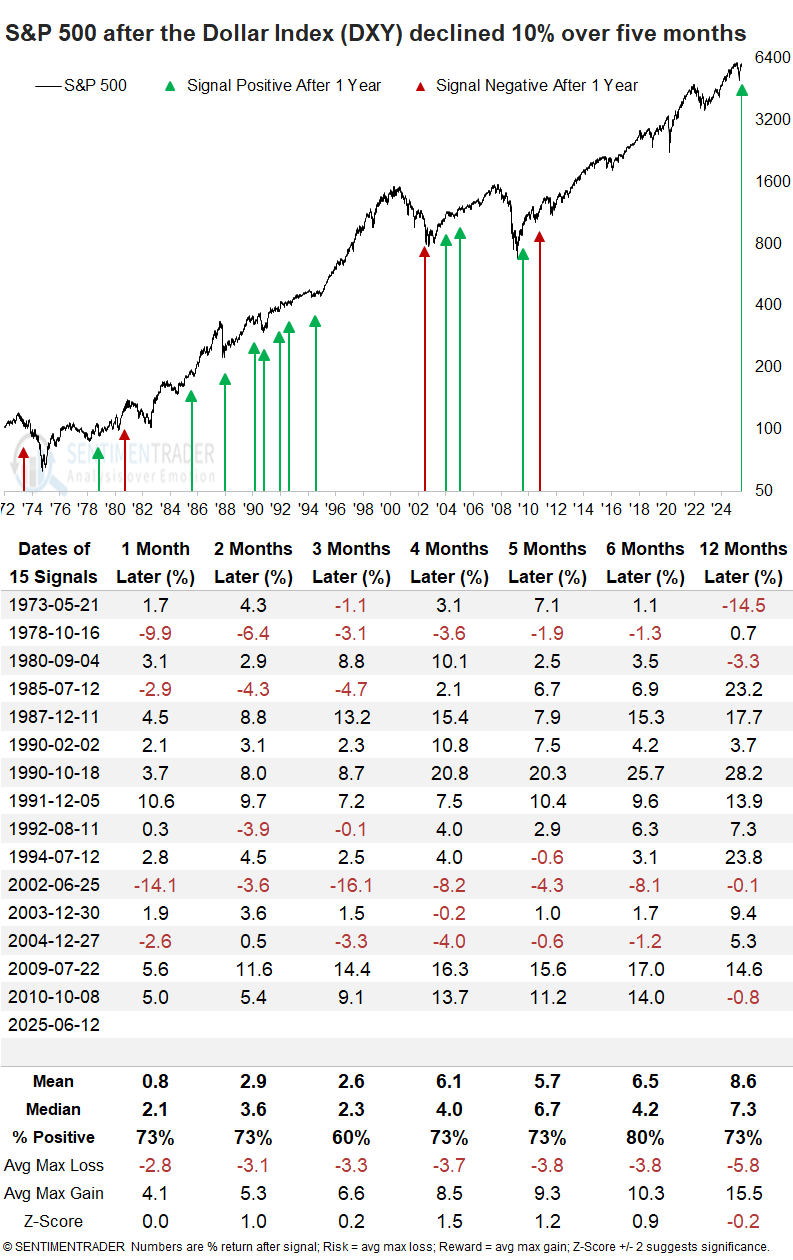

A drop in the dollar, similar to the current one, has typically been a positive for the S&P 500, which has rallied 80% of the time over the next six months.

When I examined instances where the S&P 500 was above its 200-day average, such as now, the index showed a 75% win rate five, six, and twelve months later.

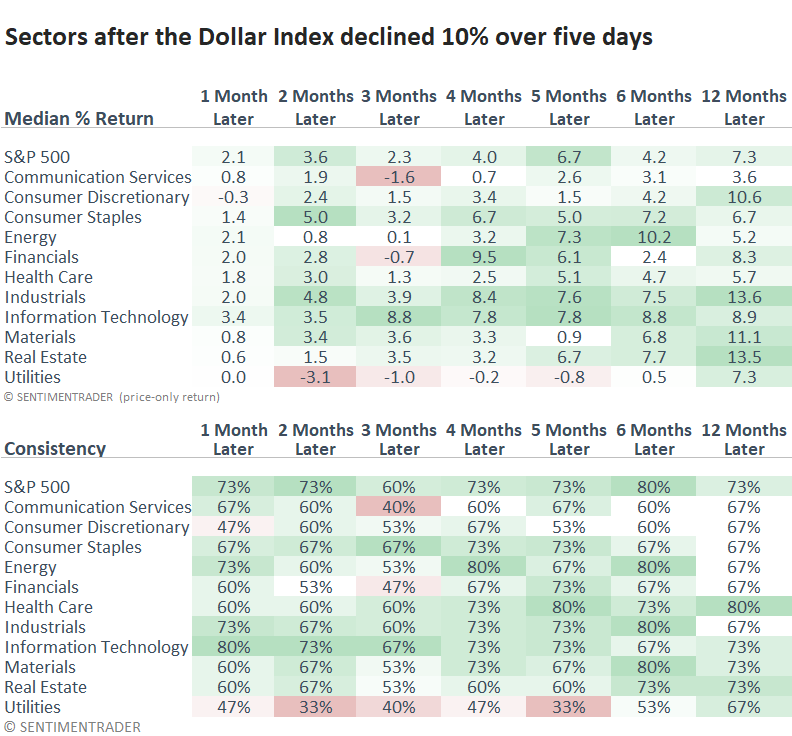

Among all sectors, Consumer Staples, Industrials, and Technology, each heavily comprised of multinational corporations, demonstrated the most persistent outperformance relative to the S&P 500 in the ensuing six months.

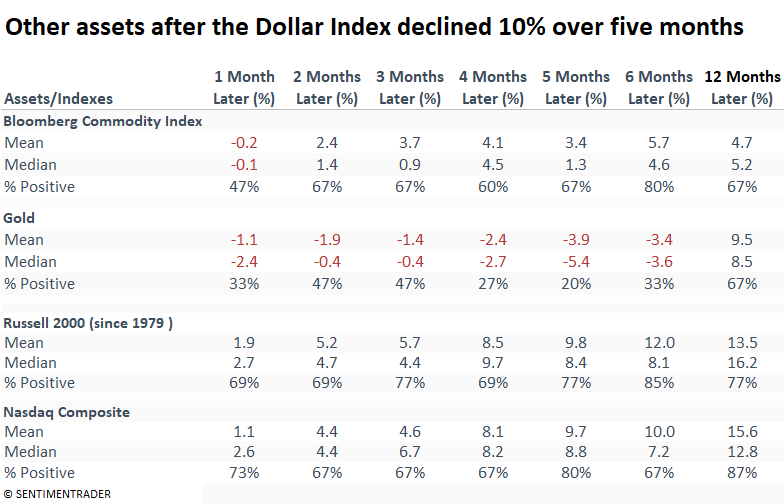

Commodities, denominated in dollars, showed a strong tendency to rally, with gains occurring 80% of the time over the next six months. Gold, on the other hand, often moved lower, likely weighed down by the dollar's rebound over the ensuing two to three months.

The Russell 2000 and Nasdaq Composite rallied after a sharp drop in the dollar, mirroring the response seen in the S&P 500 and its sectors.

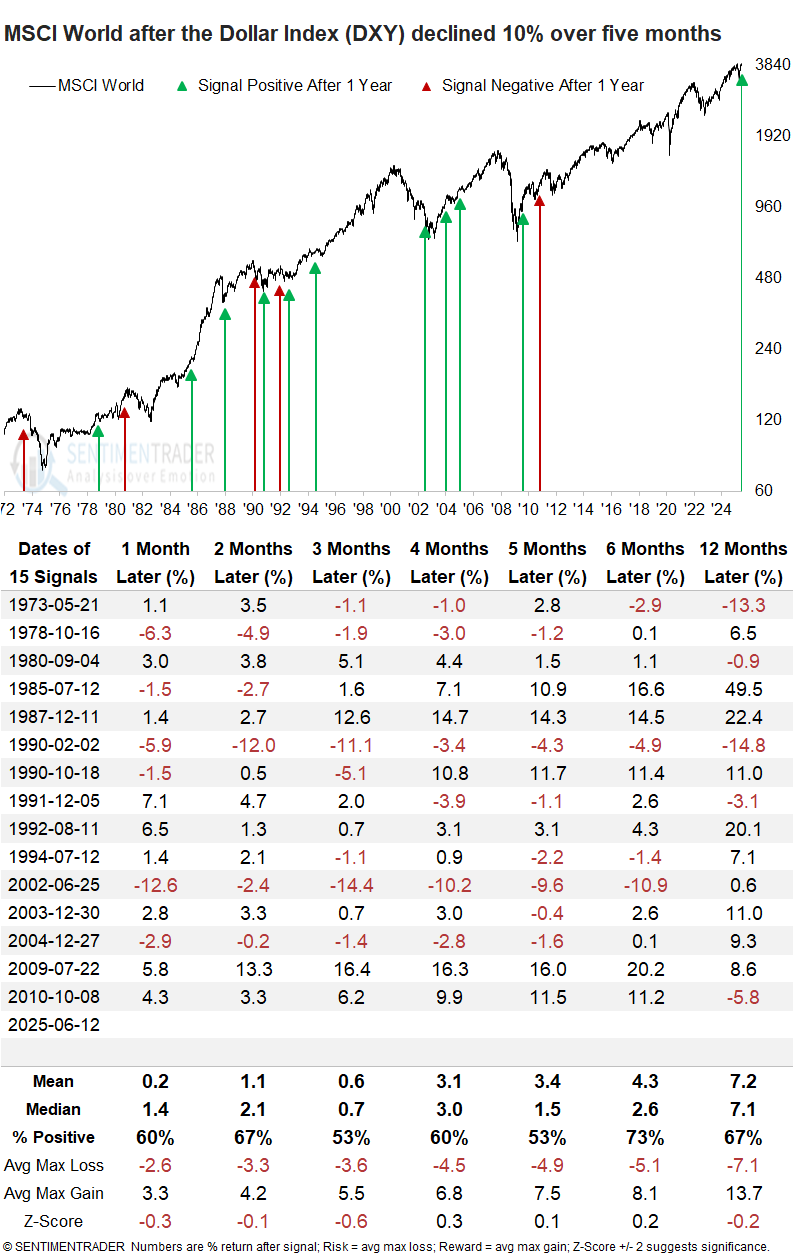

From a broad global perspective, the MSCI World Index rallied, but the results were uninspiring, especially in the three to five-month range.

What the research tells us...

The U.S. dollar has experienced significant weakness over the past five months, providing a supportive backdrop for risk assets. Such sharp downside momentum tends to persist in the short term before giving way to a multi-month rebound. A weaker dollar typically benefits stock indexes, such as the S&P 500, which includes many multinational companies, while also providing a tailwind for commodities. However, if the dollar begins to rebound over the coming months, as it has following similar setups, assets like gold, which tend to be inversely correlated, could come under pressure. That said, these historical tendencies may be disrupted in the near term due to heightened geopolitical tensions in the Middle East, which have the potential to drive volatility across currency, equity, and commodity markets.