The S&P 500 reclaims its most important level

Key points:

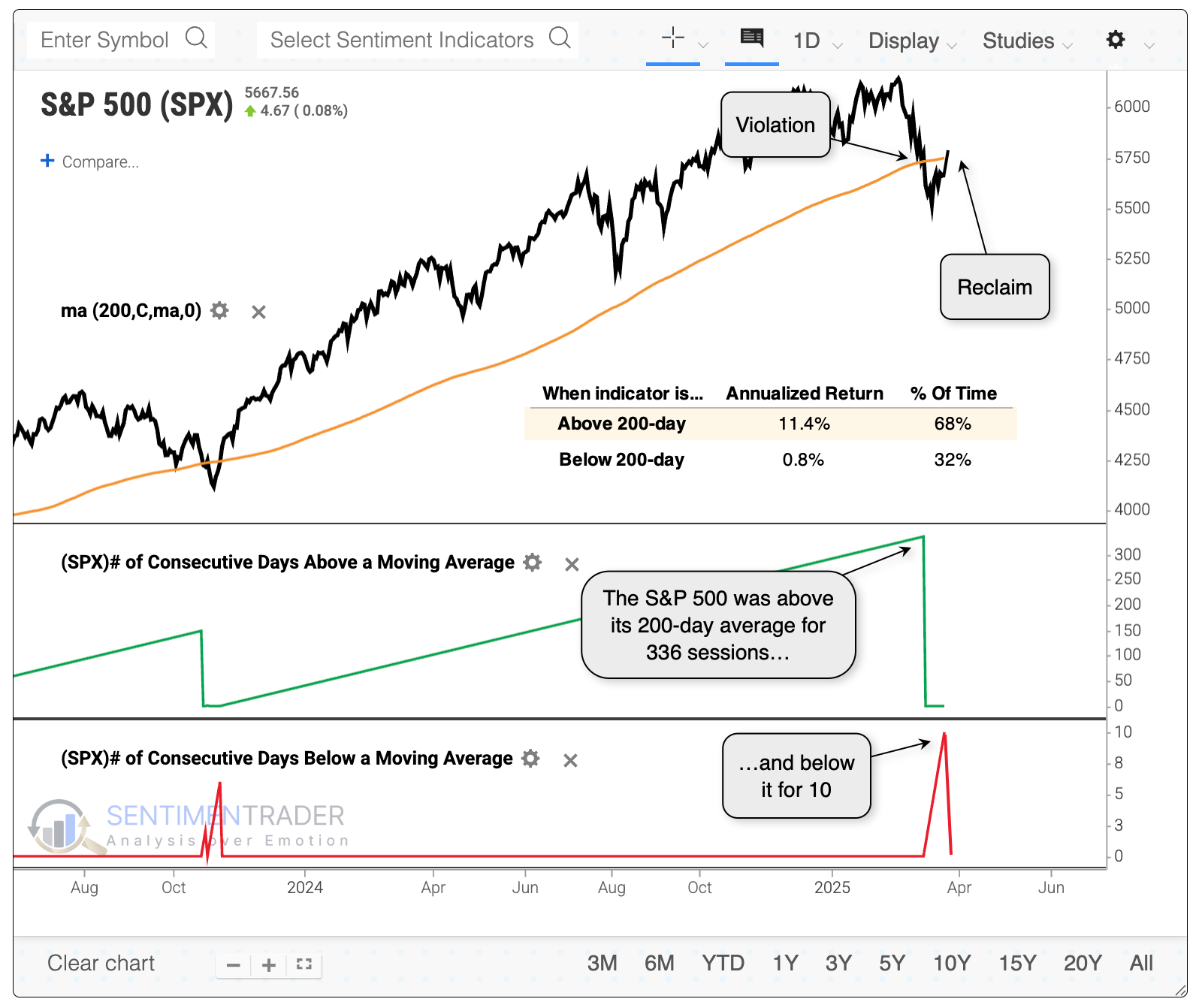

- The S&P 500 went more than a year above its 200-day average and just reclaimed it after two weeks below

- The index shows much better performance when above average than below, so this should be a good thing

- Ironically, brief stints below average after long bull markets have shown vulnerabilities that often morphed into deeper trouble

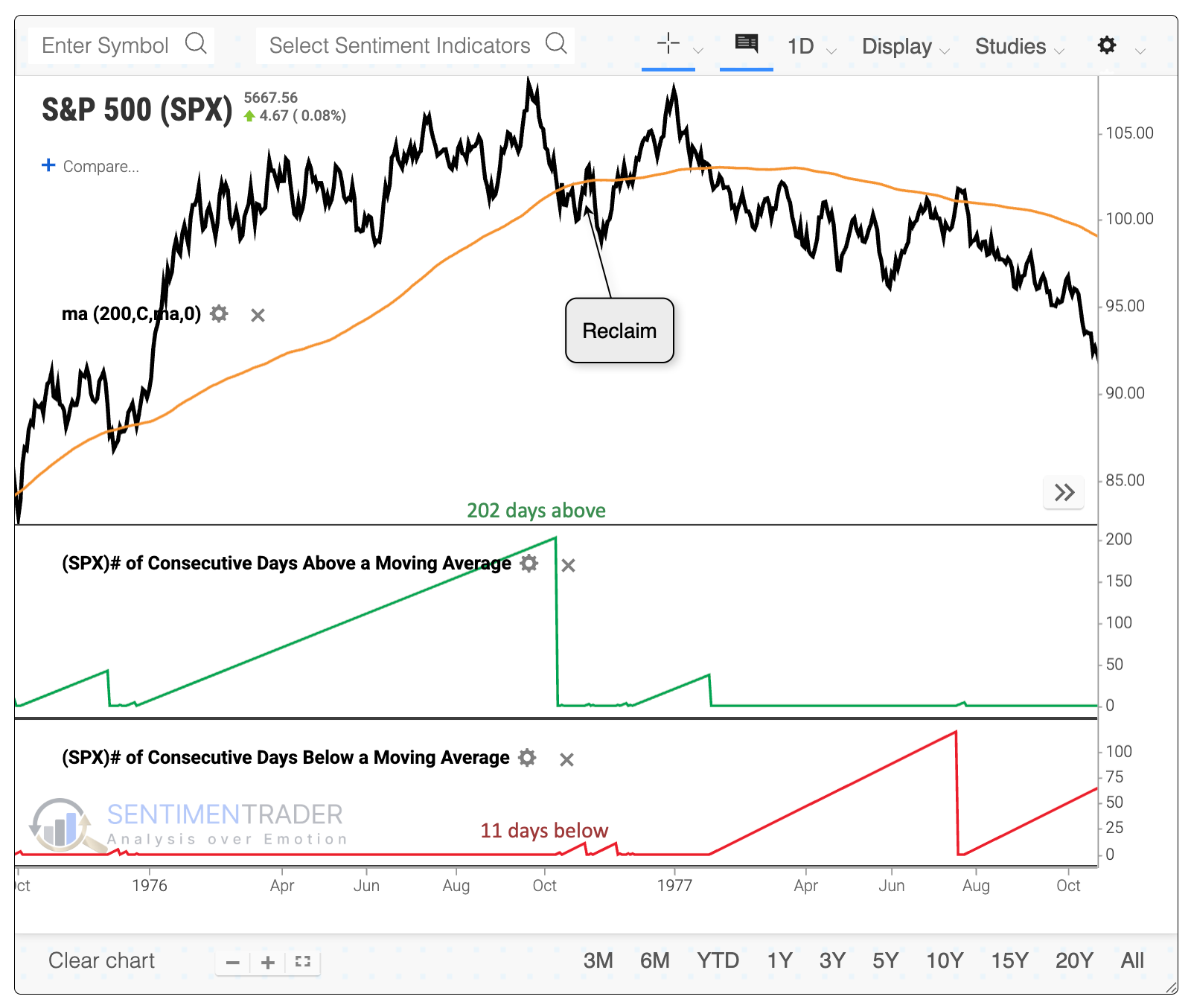

Just a short stint below average

Since the S&P 500 fell into a correction, its path has mostly followed the "good" precedents that didn't fall into bear markets. It's also good that there was evidence of deep pessimism and a rush back into stocks with overwhelming force.

The rally early this week allowed the S&P to reclaim its widely watched 200-day moving average, as well. Nothing but good things there, as the index's annualized return is astronomically better when above its average than when below.

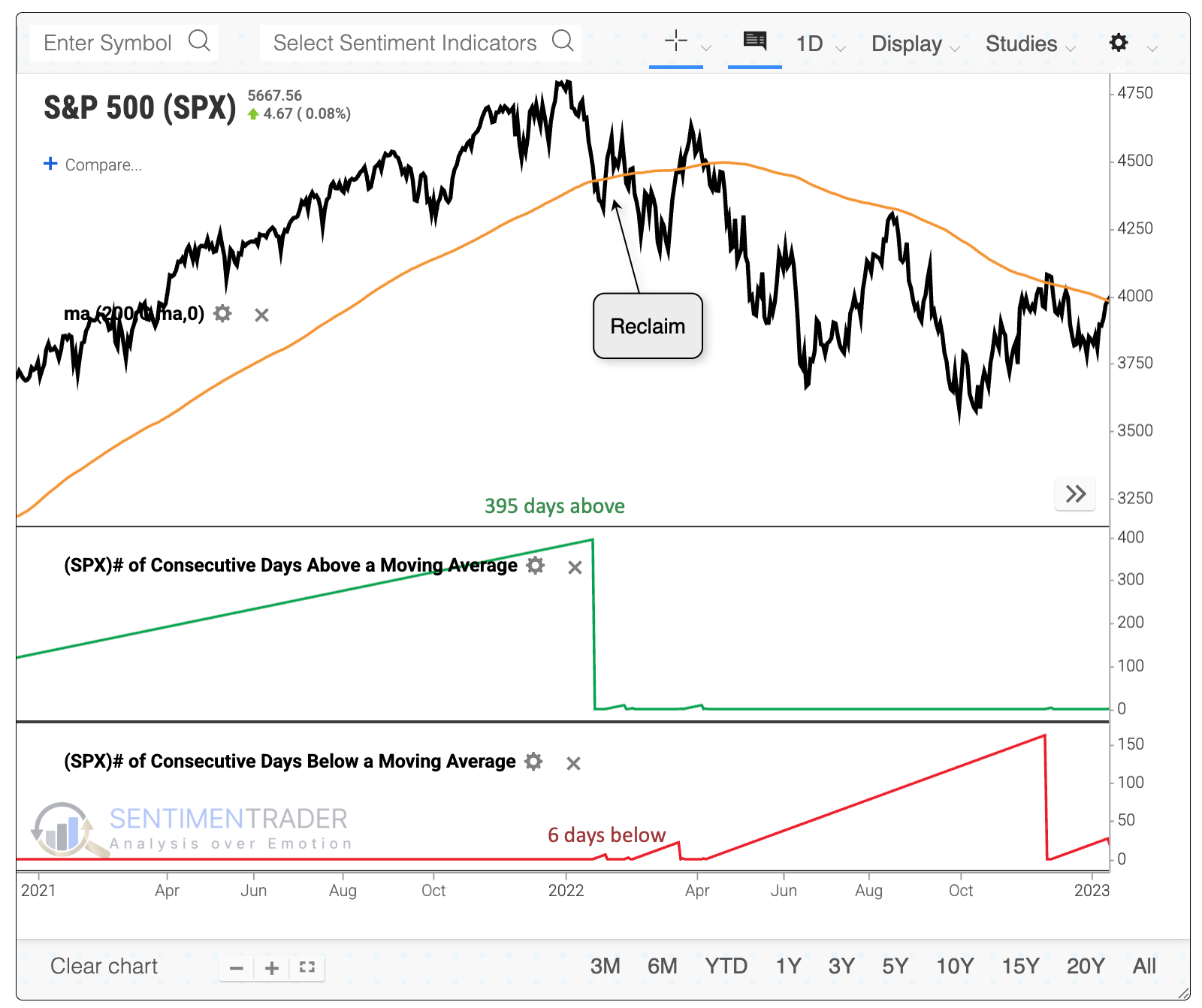

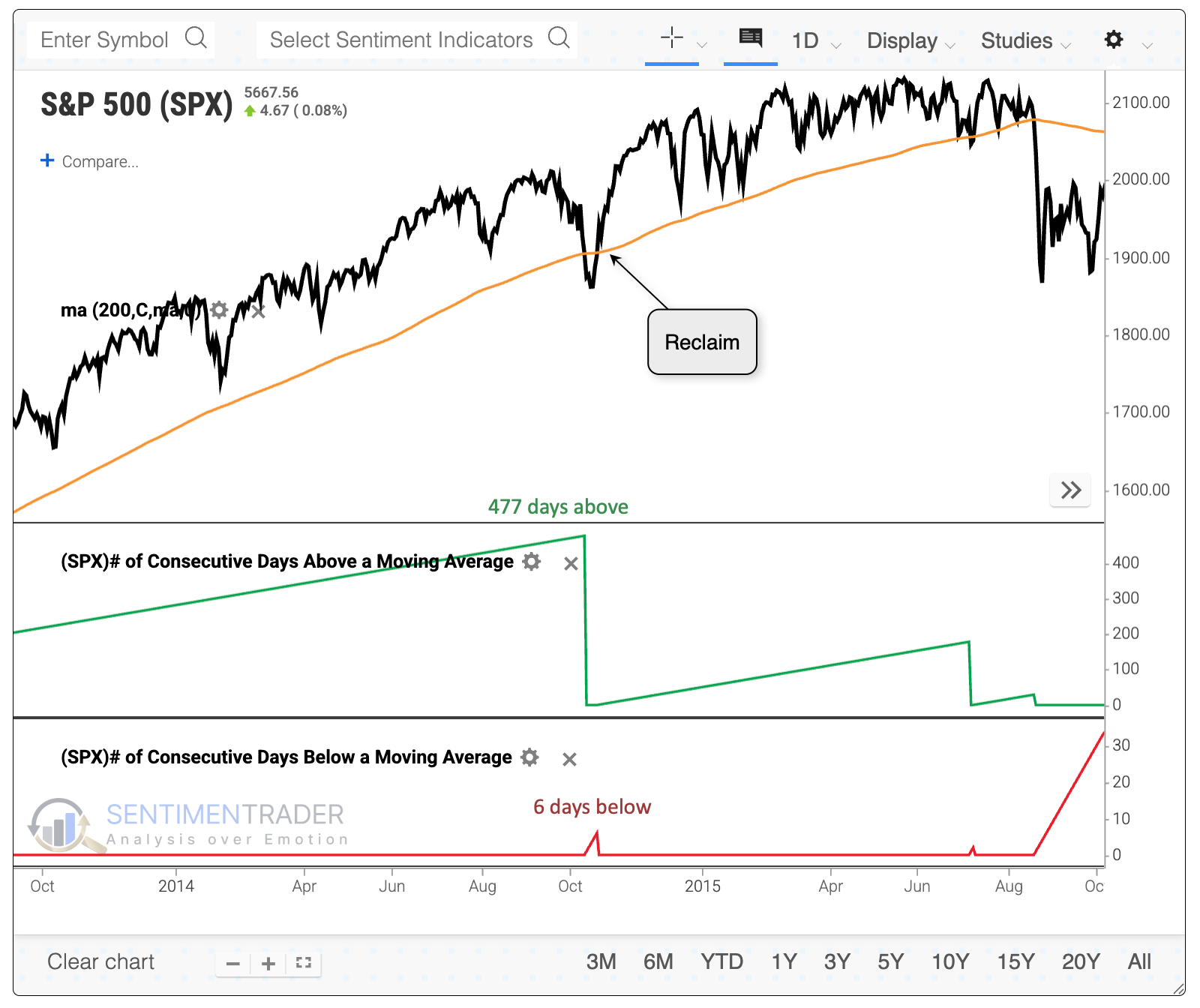

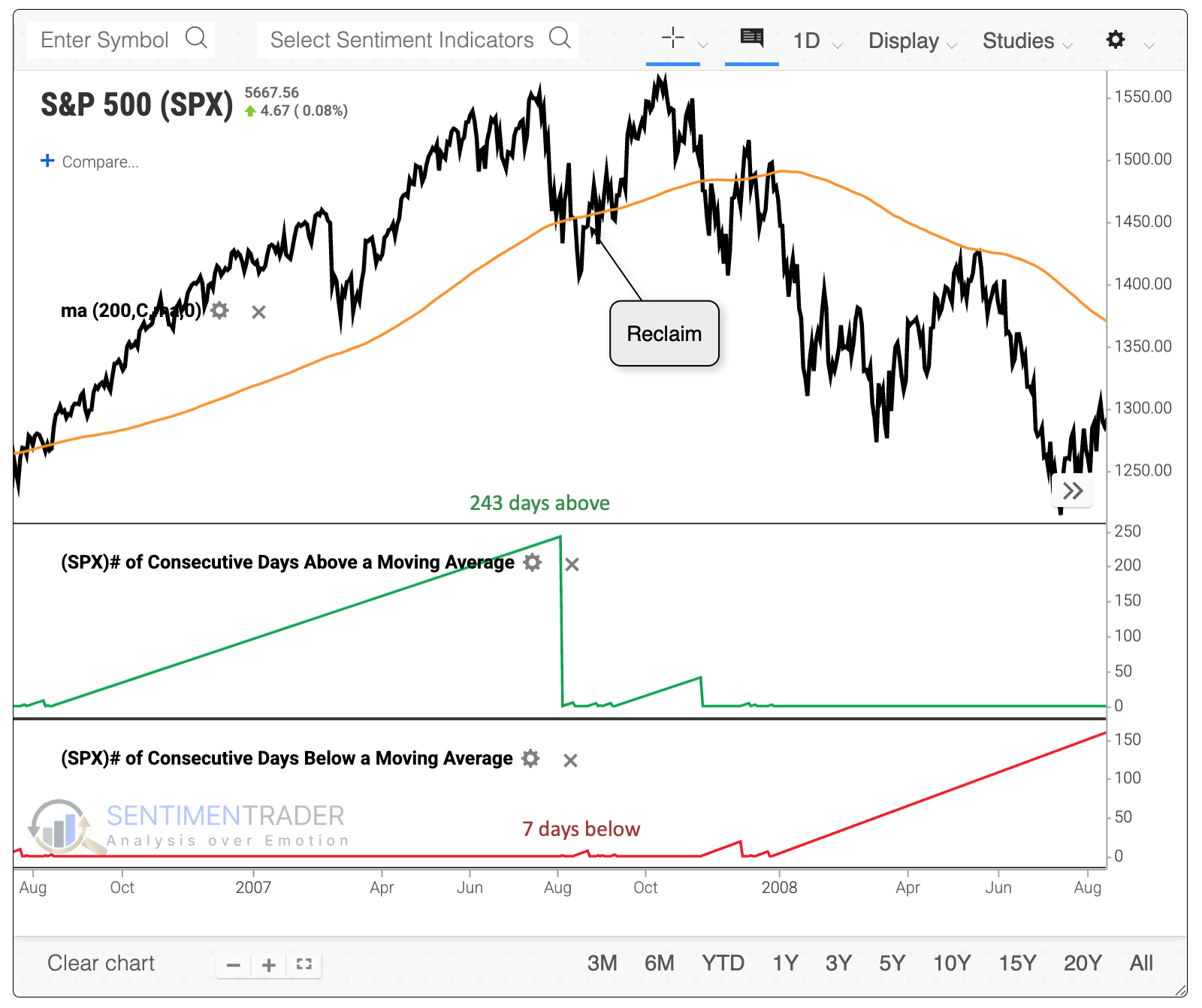

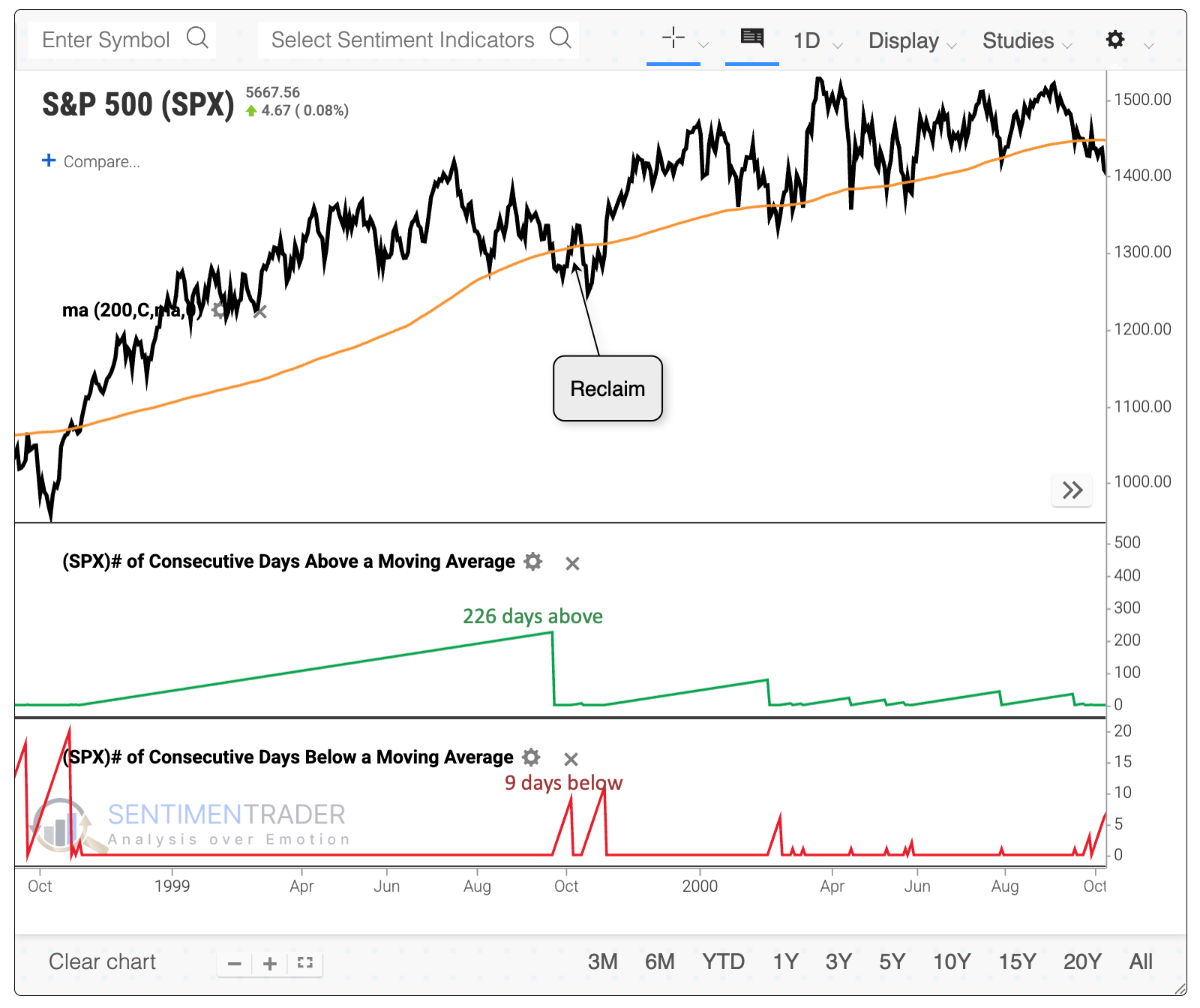

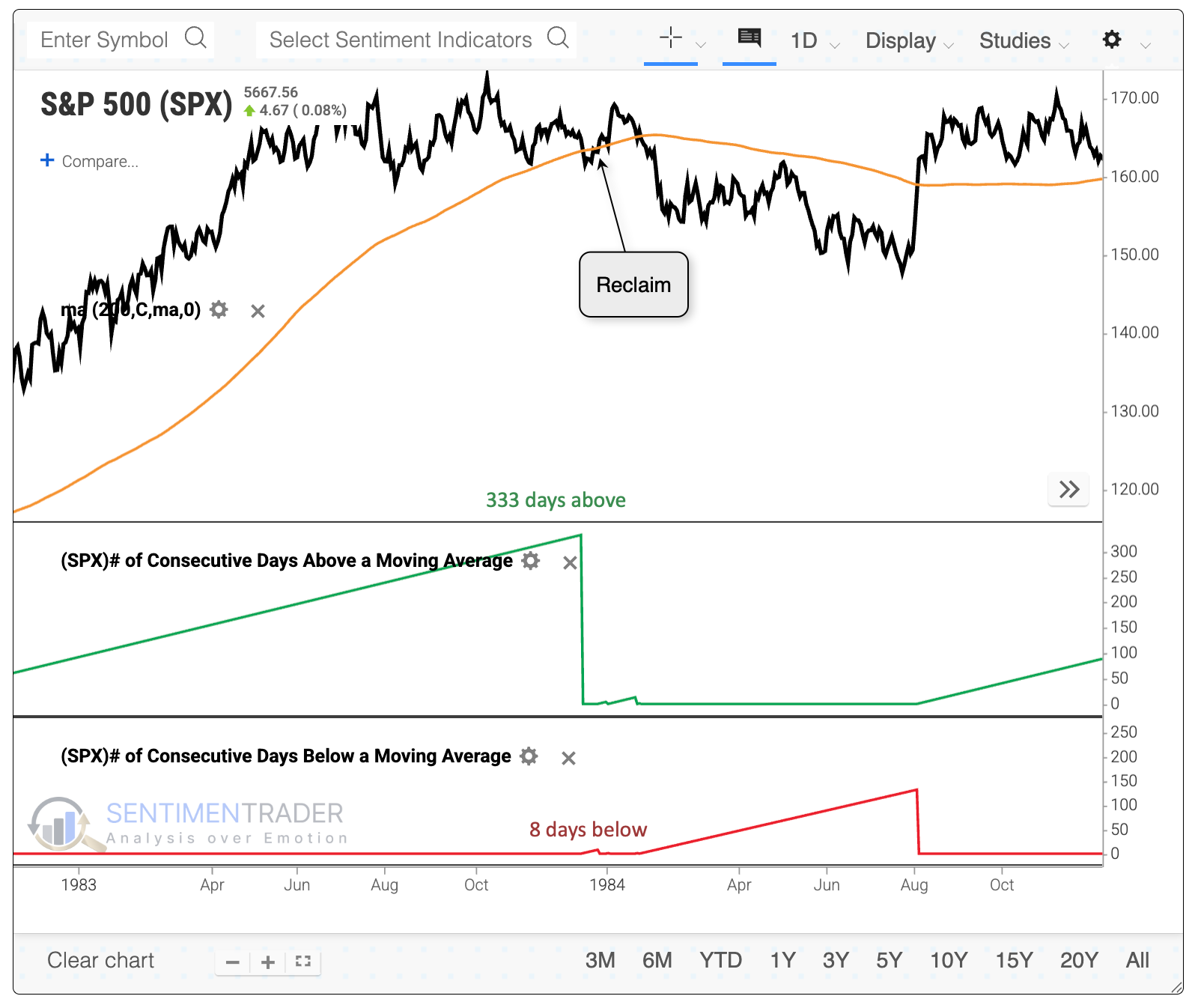

The Backtest Engine 2.0 allows users to plot (and test) how many days a stock or index has been above or below a moving average of any length. The above chart shows that the S&P 500 had been above its 200-day moving average for more than 300 sessions, then below it for only 10 before rising above it once again.

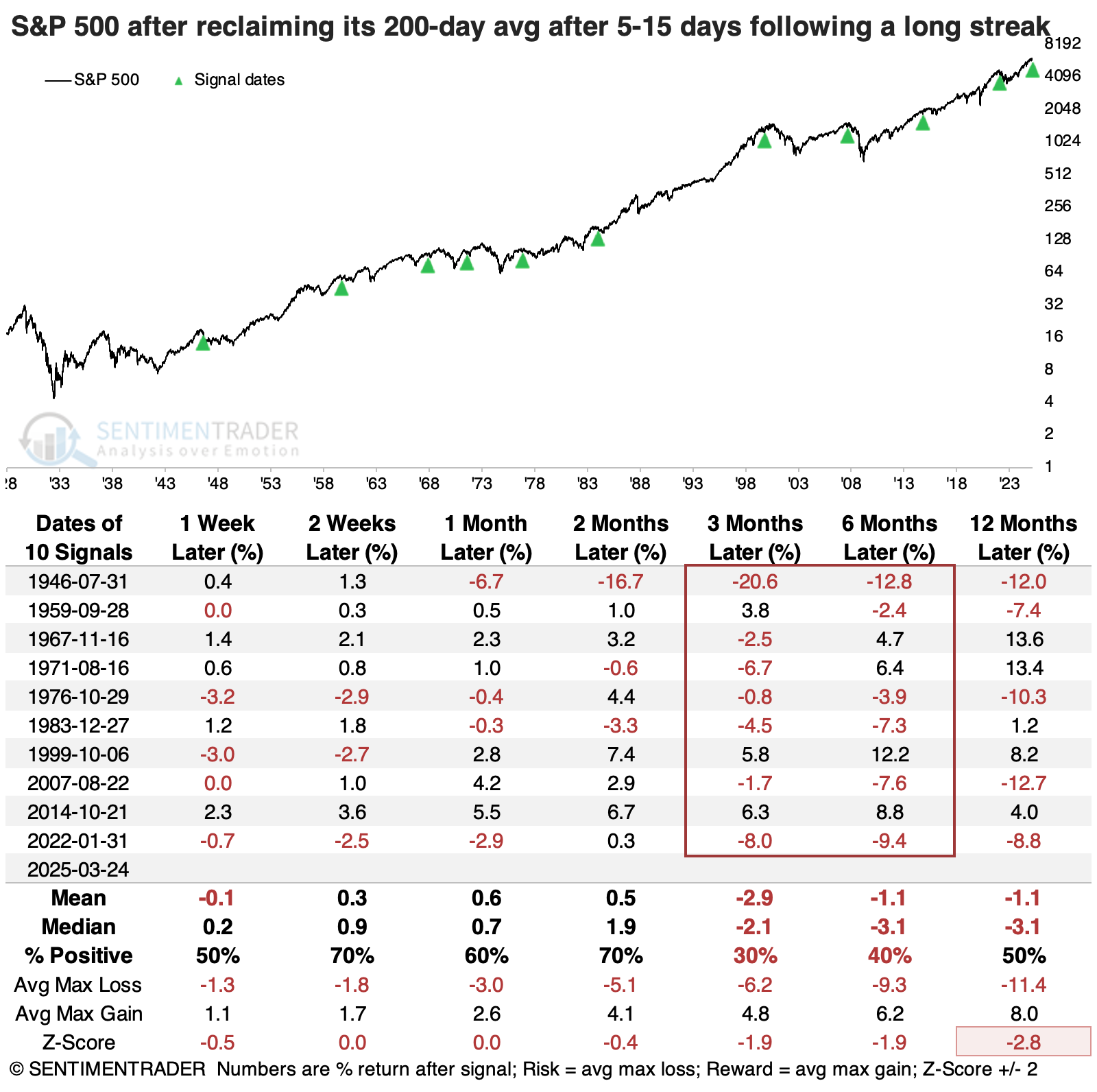

This seems like bull market behavior - a long, uninterrupted uptrend, then a drop that immediately attracted dip-buyers. When looking at historical precedents, though, something stuck out - the last four times this occurred were ahead of limited and unsustainable upside in 1999, 2007, 2014, and 2022. The S&P suffered a negative return either three or six months following 8 of the 10 signals.

We're looking at any time the S&P went more than 200 sessions above its 200-day average and then dropped below it for between 5 and 15 sessions before reclaiming it.

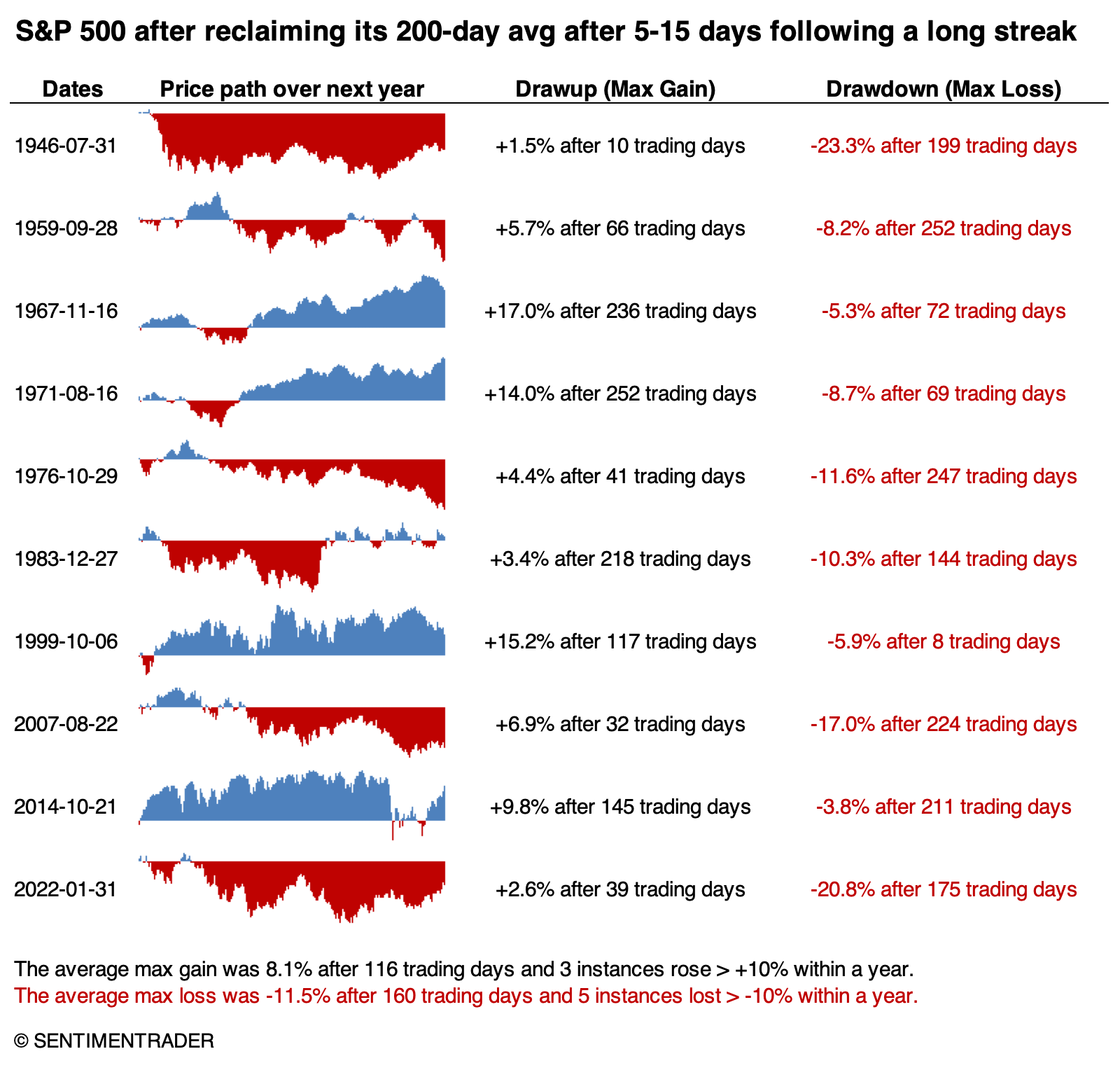

A drawdown analysis shows a negative skew, with more -10% drawdowns than +10% drawups. Only four of the ten signals showed more reward than risk over the following year.

The charts below show each instance, a year before and a year after the S&P reclaimed its 200-day average after a long stretch above and a 5-to-15-day dip below.

The instances that held up the best tended to see follow-through buying in the days ahead, pushing further ahead of its 200-day average. Those that didn't manage much of a bounce and quickly fell back below the 200-day average tended to see more of a struggle in the months ahead.

What the research tells us...

Even if we loosen the parameters in the study above, the S&P's returns in the months ahead tended to be weaker than average. This may be surprising since popping back above the 200-day average is supposed to be a positive development. It is, but we should be on the lookout for a relatively quick failure. If we see that in the days ahead, it will raise questions about the sustainability of some of the prior studies. We'd still give those bullish implications the benefit of the doubt - it's only if the S&P cannot sustain interest above its average that confidence in a bullish outcome will suffer.