The reversal in the Dollar Index continues

Key points:

- The Dollar Index (DXY) declined by more than 4.5% over one month

- After similar contractions, the DXY continued lower over the next six months

- Stocks and commodities tend to struggle in the near term but benefit 6-12 months later

- Long-term bond yields are likely to decline over the next year

The reversal in the Dollar Index continues

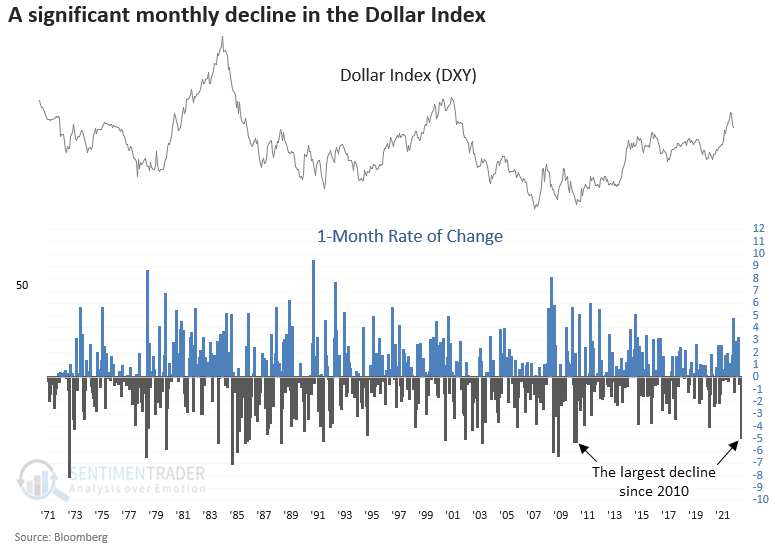

The Dollar Index (DXY) is down over 1% today, adding to the swift reversal from a 20-year high. Today's adverse price action comes after the DXY declined by almost 5% in November, representing the most significant monthly decline since 2010.

Could the plunge in the Dollar Index foreshadow a potential trend change or a recession? Unfortunately, we will only know in hindsight. However, we can use history as a guide to provide us with some potential outcomes for the DXY and other asset classes on a go-forward basis.

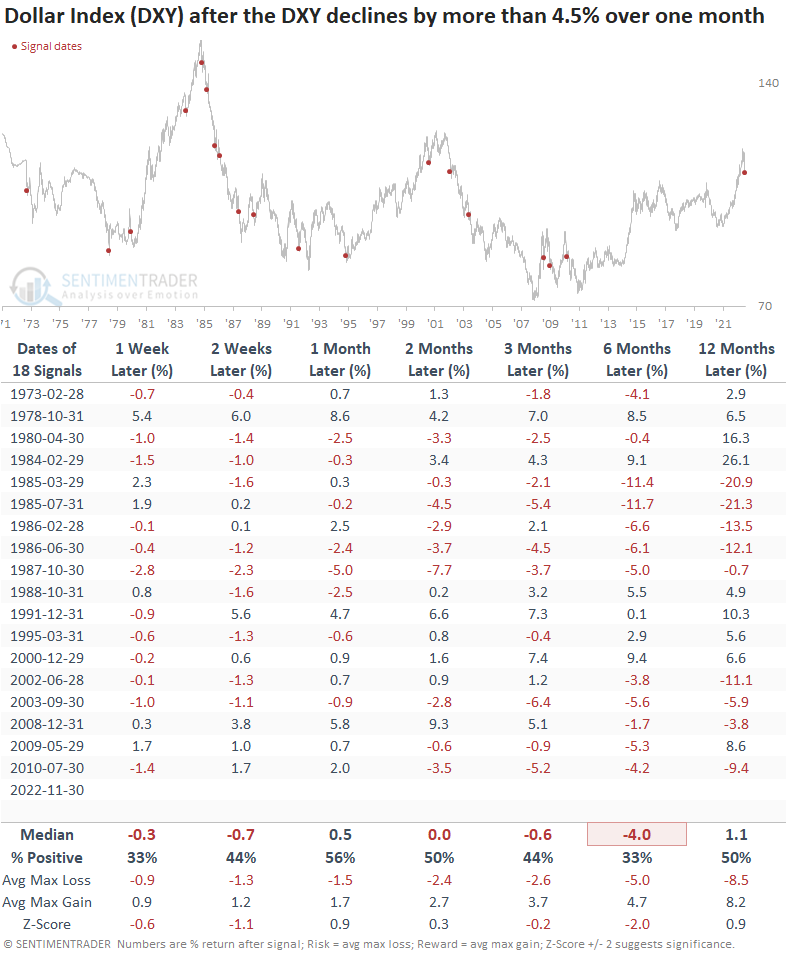

Similar monthly declines preceded negative returns for the Dollar Index

The Dollar Index tends to decline after it plunges by 4.5% in a month, especially six months later. The signal shows a negative return at some point in the first six months in 17 of 18 cases.

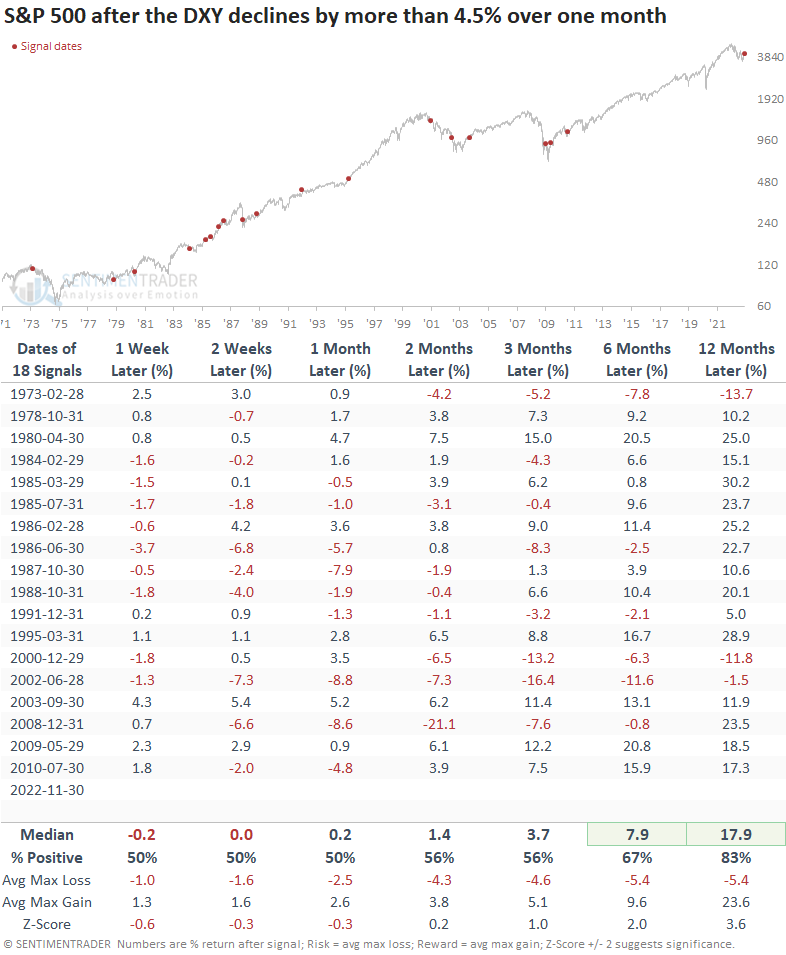

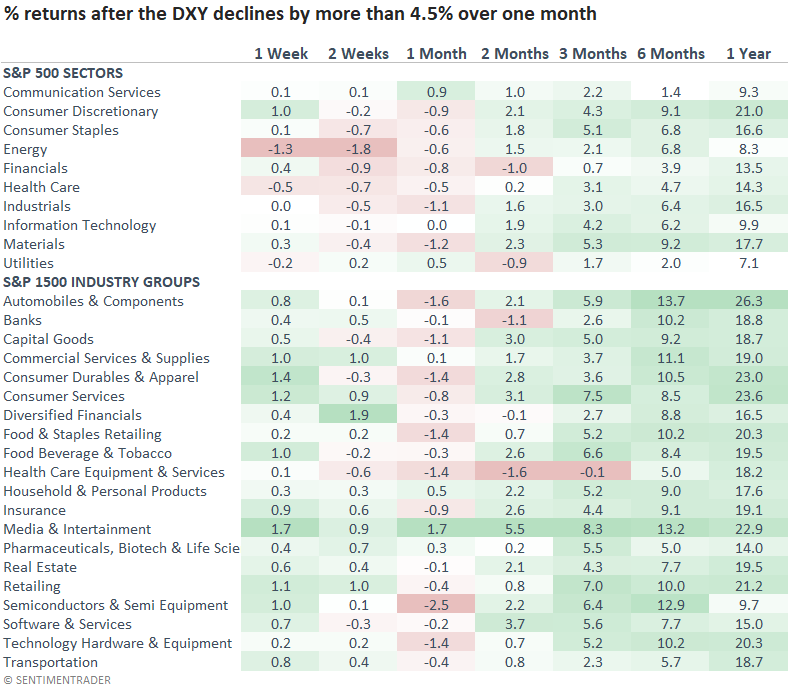

Stocks tend to benefit from a weaker dollar over the long-term

The S&P 500 was slightly negative to flat over the first month. Still, it showed a tendency to recover and post solid returns in six- and 12-month periods. The significant drawdowns a year later all occurred during long-duration bear markets.

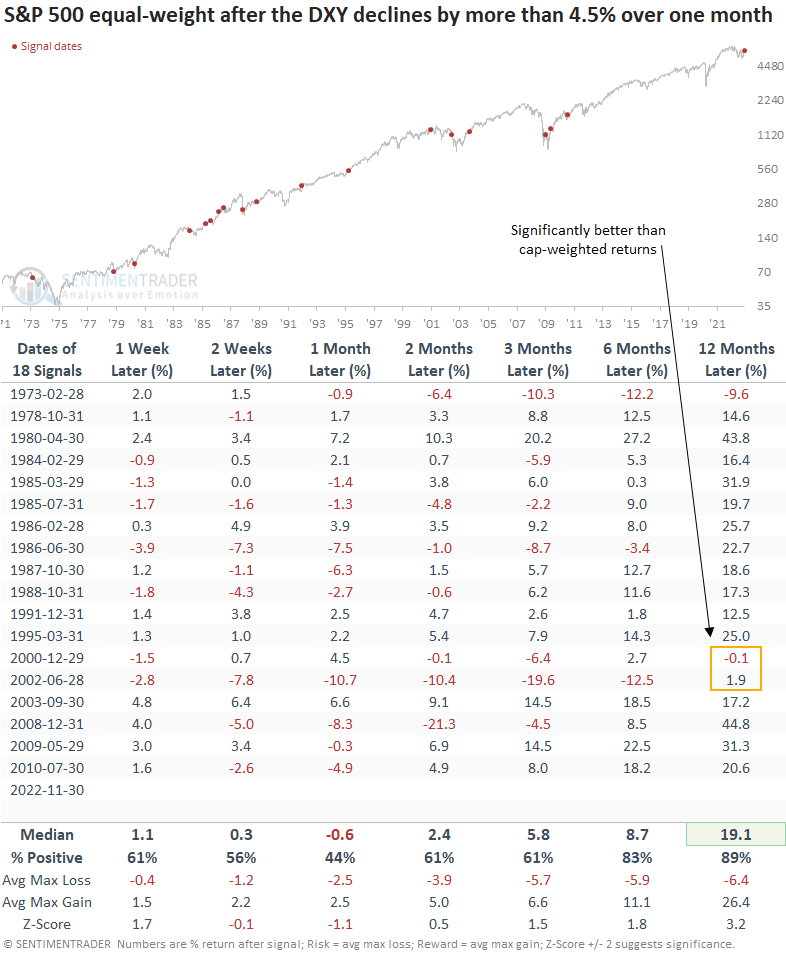

The S&P 500 equal-weighted index shows a similar return profile to the cap-weighted version. One notable difference is the performance in the 2000-02 bear market. The average stock performed much better as the cap-weighted index was impacted by Technology. Sound familiar.

Interestingly, large-cap sectors did not benefit as much from the weaker dollar as the all-cap industry groups. i.e., the lower dollar did not benefit large companies with more overseas exposure. I would also note that resourced-based sectors like energy underperformed in the near term.

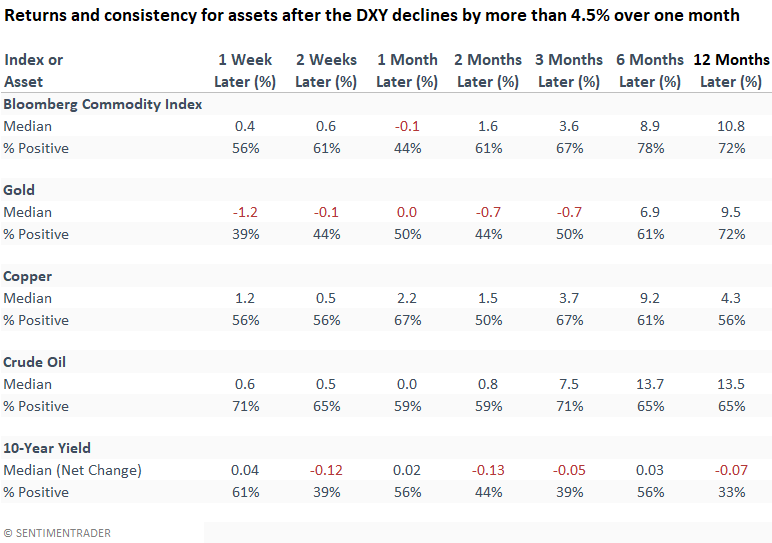

Commodities tend to benefit, and long-term yields could decline

Commodities tend to show an upward bias, with solid results in the six-to-12-month time frames. Interestingly, gold struggles in the first three months. With gold up 8% in November and 3% more today, that could be the case again.

The 10-year yield should decline. However, we must remember that most signals occurred during a secular decline in yields.

What the research tells us...

The Dollar Index remains under pressure after reversing from a 20-year high. More often than not, a falling dollar tends to be bullish for stocks and commodities over the long term. From a big-picture perspective, one has to wonder what, if any, message we should take away from the relentless decline in the DXY. Risk assets will struggle if it's signaling that the Fed made a policy mistake and a recession is coming.