The Monday Smackdown in the Volatility Index (VIX)

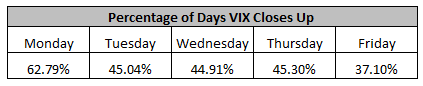

The Volatility Index (VIX) smackdown on Monday was highly unusual as it closed down 9.88%. Monday's represent the day of the week with the highest percentage of up closes for the VIX. According to my calculation, the VIX increases 62.79% of the time. As the table below shows, this is significantly more than any other day of the week. The stark difference between Monday's and Friday's is known as the weekend effect as options are sold on Friday to take advantage of time decay.

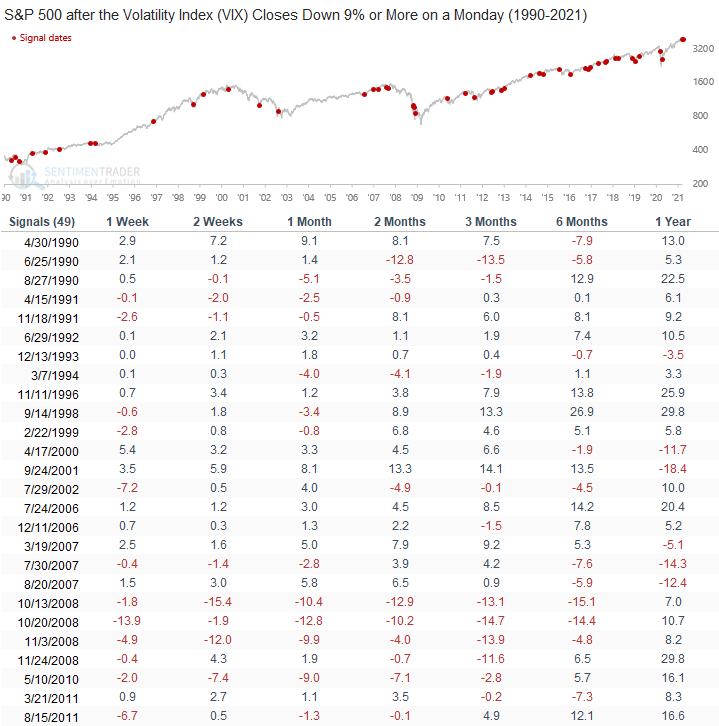

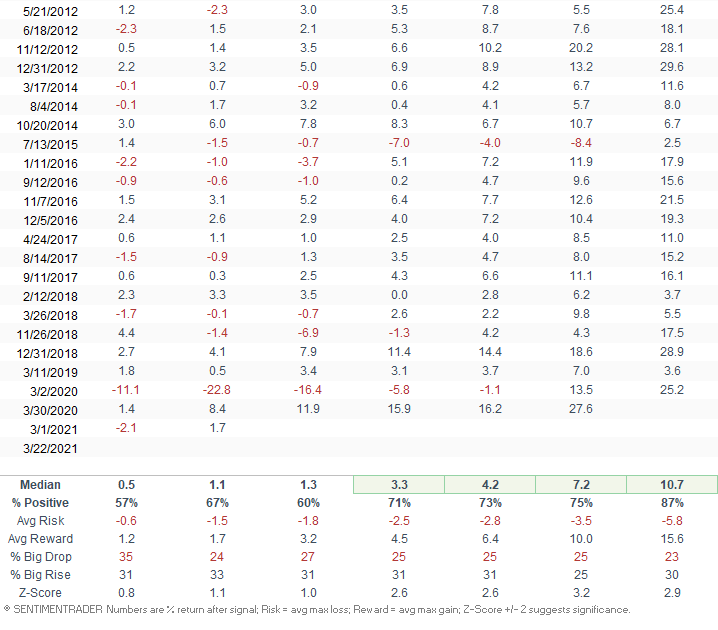

Let's take a look at forward returns for the S&P 500 when the VIX closes down more than 9% on a Monday.

S&P 500 Signal Performance

As the table below shows, a VIX collapse of 9% or more on a Monday has only occurred 49 times since 1990. The results look robust in the 8 to 52-week timeframe.