The Historical Implications of a NASDAQ Breadth Thrust

Key points:

- A "Breadth Thrust" detects market momentum, and typically involves a large number of stocks advancing over a given period relative to the number of stocks declining over the same period

- Two well-known breadth thrust indicators are the Zweig Breadth Thrust and Deemer Breakaway Momentum

- Another such measure that fewer investors are aware of is something I refer to as NASDAQ Breadth Thrust; It recently fired a new signal

A NASDAQ Breadth Thrust Defined

I define a NASDAQ Breadth Thrust (heretofore NBT) as follows:

A = Daily NASDAQ Advances

B = Daily NASDAQ Declines

C = 10-day total of A

D = 10-day total of B

E = ((C/ (C + D)) * 100)

Variable E is simply the percentage of total advances in the last 10 trading days divided by the total of advances and declines.

A new NBT occurs when Variable E closes a day at 62% or higher. A new NBT occurred on April 14th, 2026. Does it matter?

To address the potential significance, let's consider only the first NBT in any 12 months.

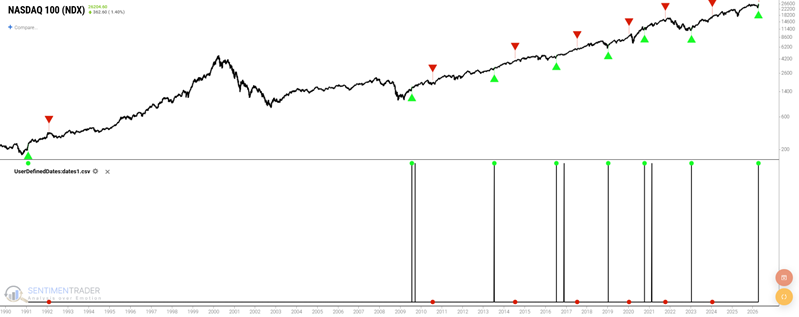

Market Action following the first NASDAQ Breadth Thrust in a year

Let's take a closer look at Backtest Edge. The chart below displays all NBT (1st in 12-month) signals. The green up arrow highlights the date