The first Fed rate cut

Key points:

- The Federal Reserve is on track to change its interest rate trajectory after a long hiking cycle

- Stocks showed mixed returns after nine other "first cuts"

- Defensive sectors like staples and utilities tended to perform relatively well, as did value stocks

A new regime

After the longest hiking cycle in a decade and a half, the Federal Open Market Committee is expected to reduce its Fed Funds target rate this week. It would mark the end of the 2nd-longest tightening cycle in 35 years.

Much ink has been spilled on the implications, and we won't wade into potential macroeconomic repercussions. We're also not going to participate in the delusion that we can know whether this cut will precede an economic recession, which can dramatically impact forward returns.

All we can know is what we know right now; the rest is conjecture. There is a place for that, and this ain't that place.

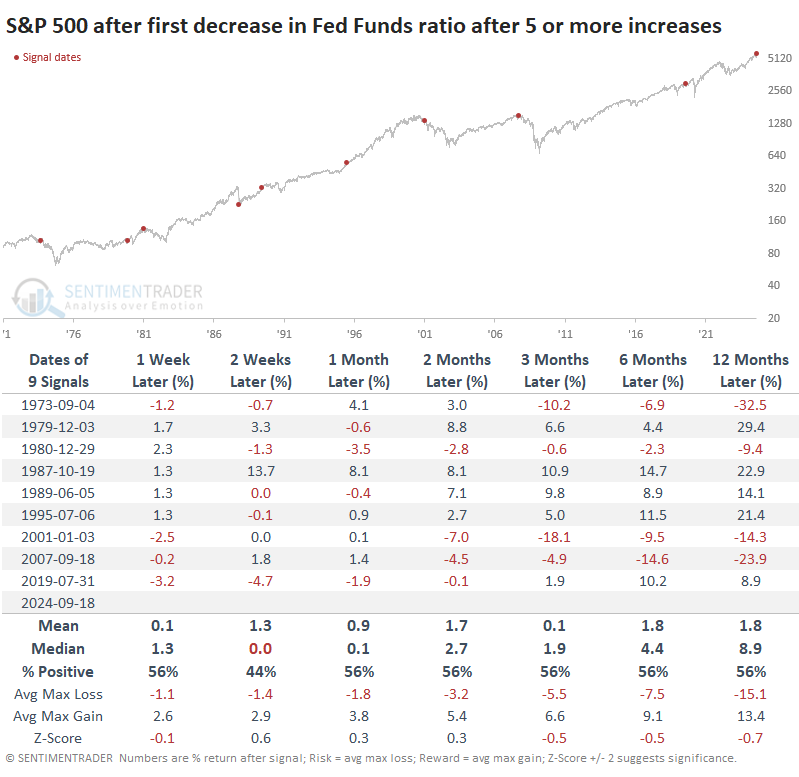

Assuming the Fed follows through on its promise, the implications for stocks are mixed. The last three cuts after a hiking cycle all preceded devastating bear markets. Before that, there was no real pattern. There was no discernable difference in returns based on how far the S&P 500 was from a multi-year high at the time of the first cut.

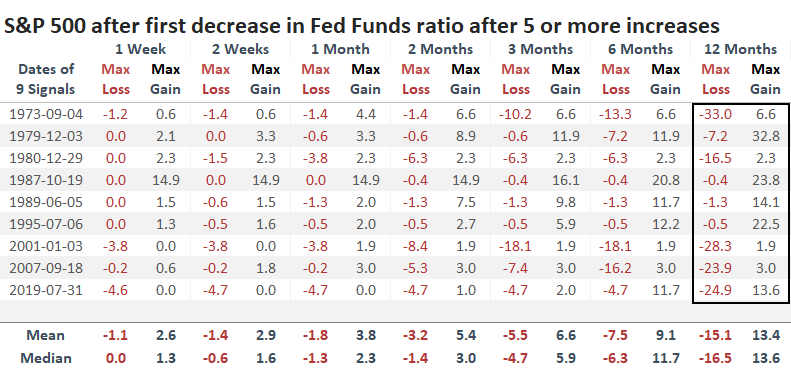

The table of maximum risk and reward across time frames shows a pretty binary result. Over the next year, stocks either enjoyed decent gains with low risk or limited gains with high risk. There wasn't any middle ground. A decent heuristic was watching the next two weeks - if risk exceeded reward, then it was a strong suggestion that the following year would be tough.

Bad for the dollar, good for value

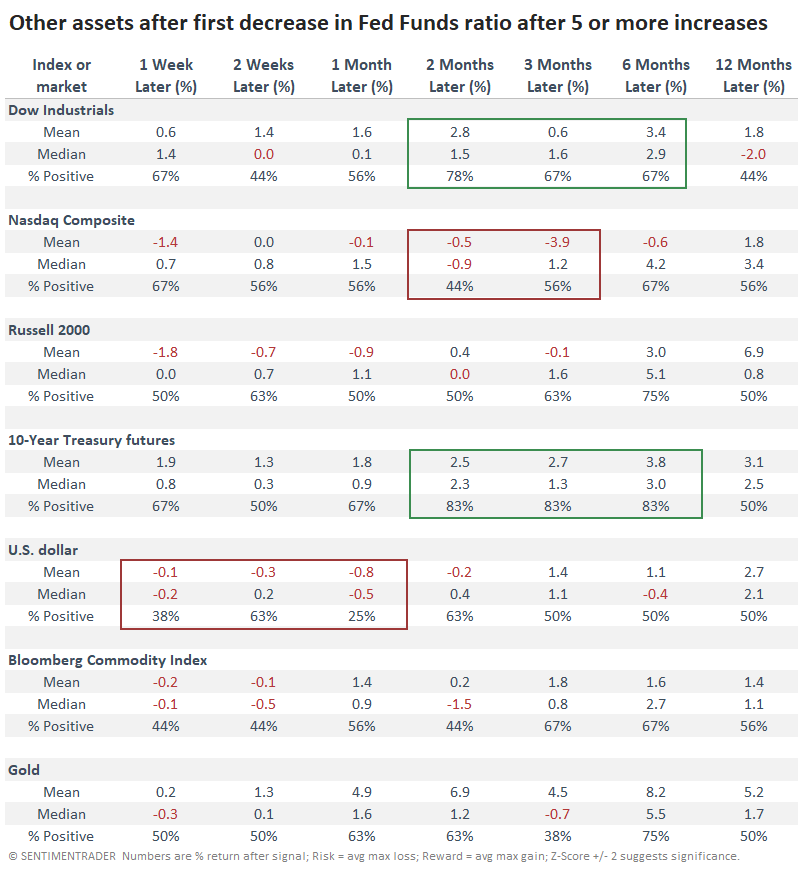

It was a mixed picture among other indices and assets, even among time frames. Generally, the Dow Industrials held up better than the S&P or, especially, the Nasdaq Composite and Russell 2000. The dollar tended to suffer in the immediate aftermath of the cut, but that didn't help gold or commodities too much. 10-year Treasury futures did well over the medium-term (suggesting yields declined).

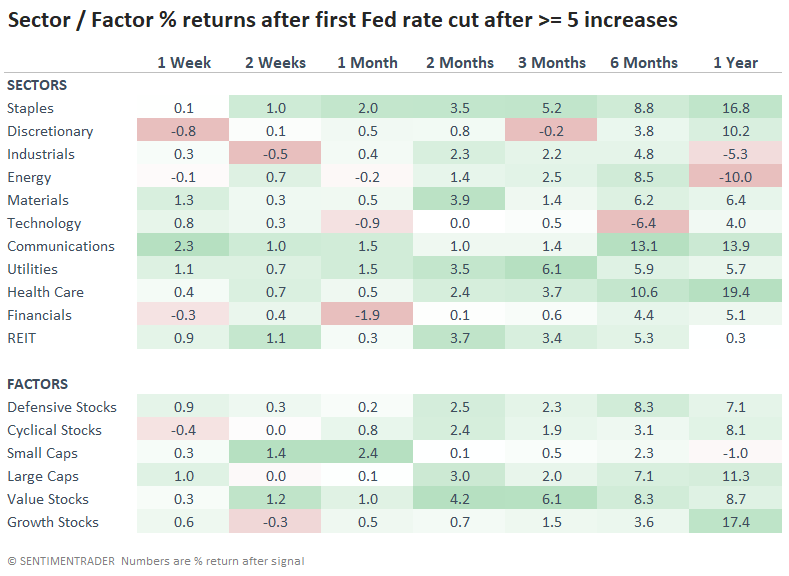

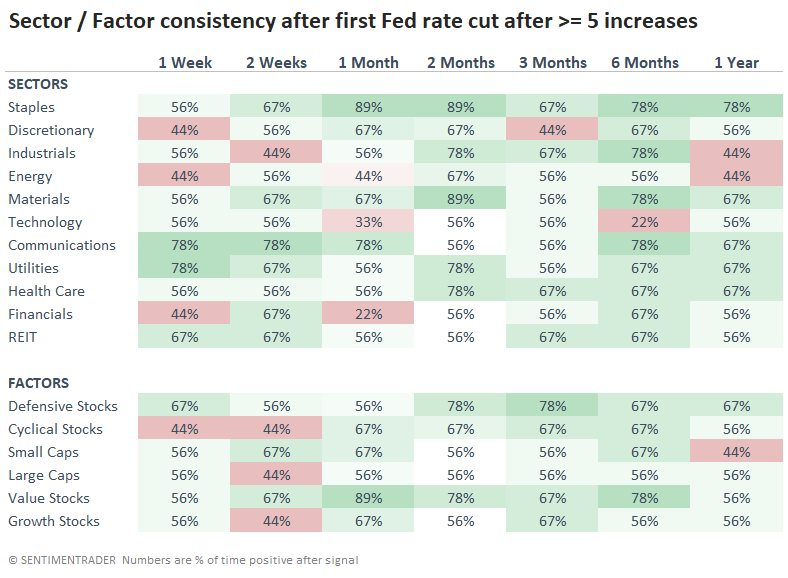

Among sectors and factors, the next three months showed a dramatic difference in the median return between staples (+5.2%) and discretionary stocks (-0.2%). Utilities and health care also enjoyed robust returns, with a definite tilt toward value (+6.1%) over growth (+1.5%). However, much of that edge either eased or reversed over longer time frames.

The win rates among sectors and factors showed a tilt toward defensive and value factors and sectors. Over the following three months, staples rose 67% of the time versus a 44% win rate for discretionary.

What the research tells us...

Opinions aside, the imminent cut in the Fed Funds rate has been a crap shoot for investors. There was no consistent pattern in forward returns after significant hiking cycles. The last few have been major warning signs, while most of the others were not at all. They were more consistently negative for the dollar (for a while), tech stocks (ironically enough), while being good for Treasury notes and bonds, value stocks, and defensive sectors.