The Dollar Index is no longer in an uptrend

Key points:

- The Dollar Index (DXY) shifted from an uptrend to a downtrend

- After similar trend changes, the DXY tends to fall in value over the next six months

- Stocks and commodities like a lower dollar, with solid results 6-12 months later

- Long-term bond yields could tick up over the next few months

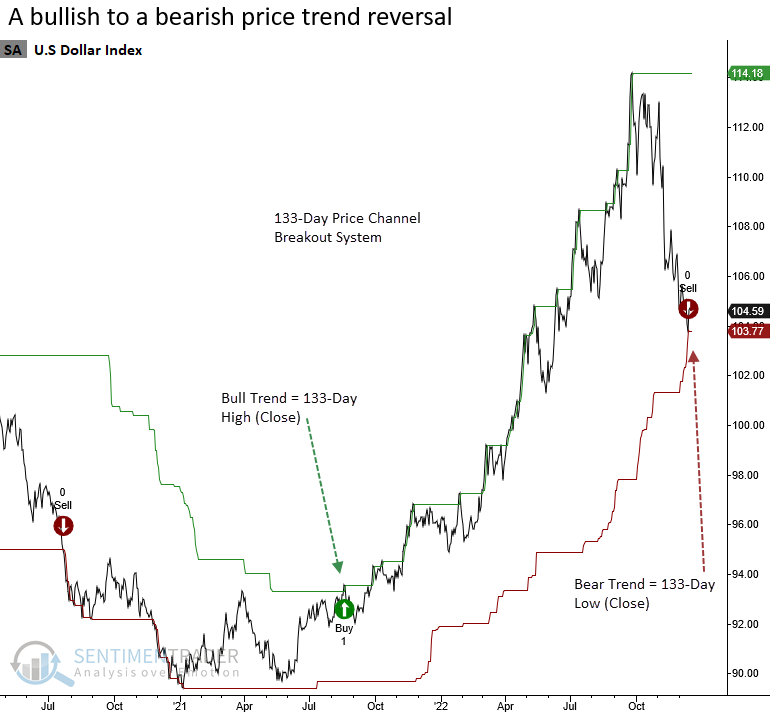

According to one trend-following model, the Dollar Index (DXY) is no longer in an uptrend

In August 2021, the trend-following model I use for currencies turned bullish on the Dollar Index (DXY). The system uses a price channel breakout methodology made famous by Richard Donchian.

After a year-long uptrend and trough-to-peak gain of 16%, the system has now flipped to a bearish trend condition. The trend change is not surprising, as the DXY has shown signs of a potential reversal over the last month.

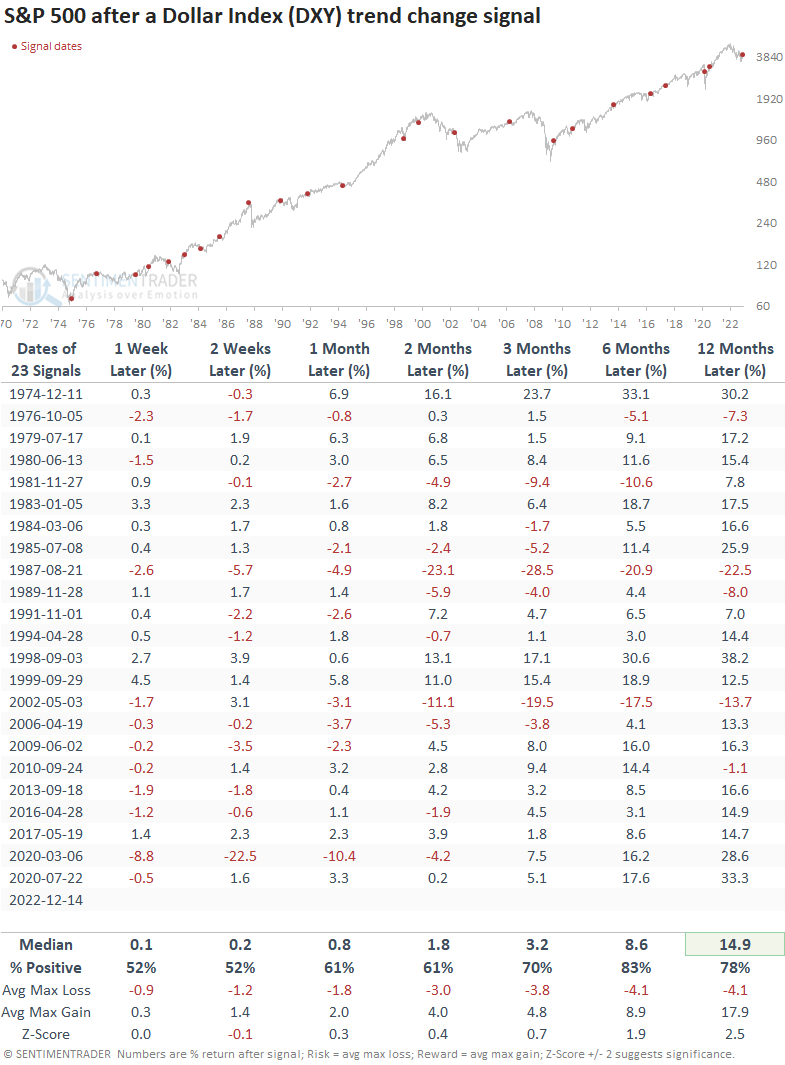

A bullish to a bearish trend reversal in the Dollar Index could provide a tailwind for stocks, which was not the case for most of the last year. When the DXY trend-following model is negative, the S&P 500 shows an annualized return of 10.1%.

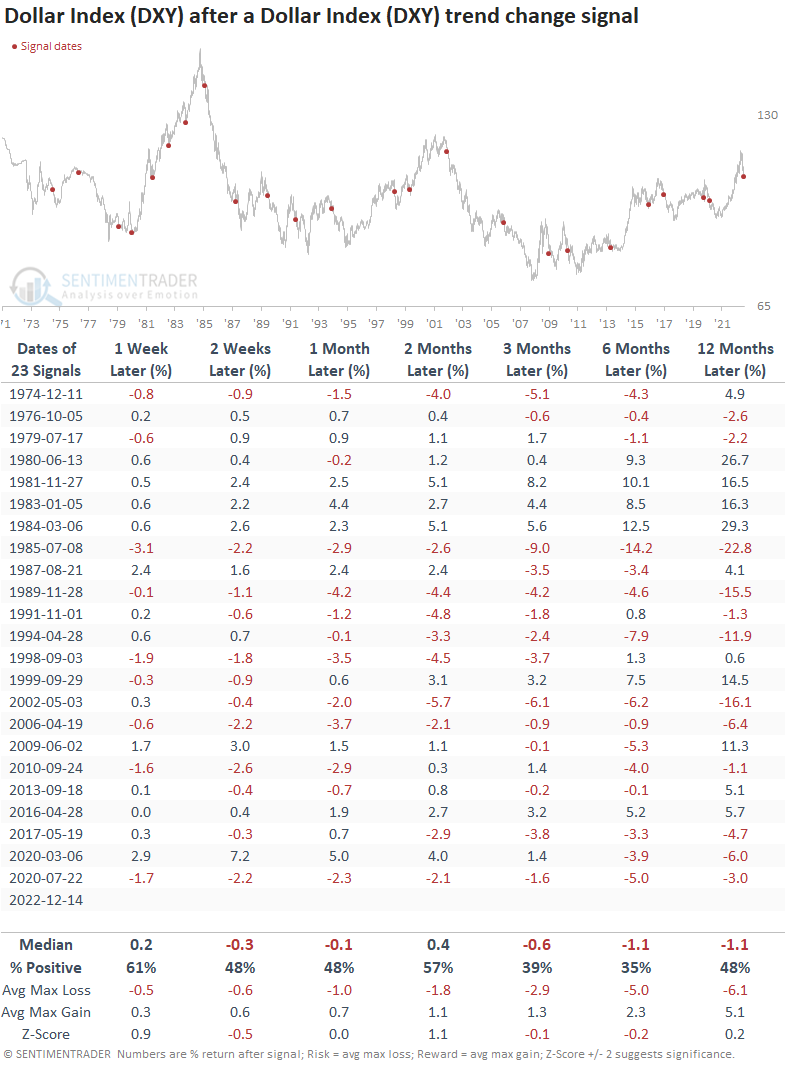

Similar trend changes preceded negative returns for the Dollar Index

The Dollar Index tends to decline across most time frames when the trend shifts from positive to negative. Trend change signals hit a rough patch between 1981 and 1984, resulting in painful whipsaws during a historic bull run. Since then, the DXY has shown a loss at some point in the first six months in 15 out of 16 cases.

Stocks tend to benefit from a weaker dollar over the long-term

A bearish dollar trend backdrop tends to help large-cap stocks, especially six- and 12 months later. Similar to interest rates, the impact operates with a lag. Besides the signals in 1987 and 2002, drawdowns were relatively benign a year later.

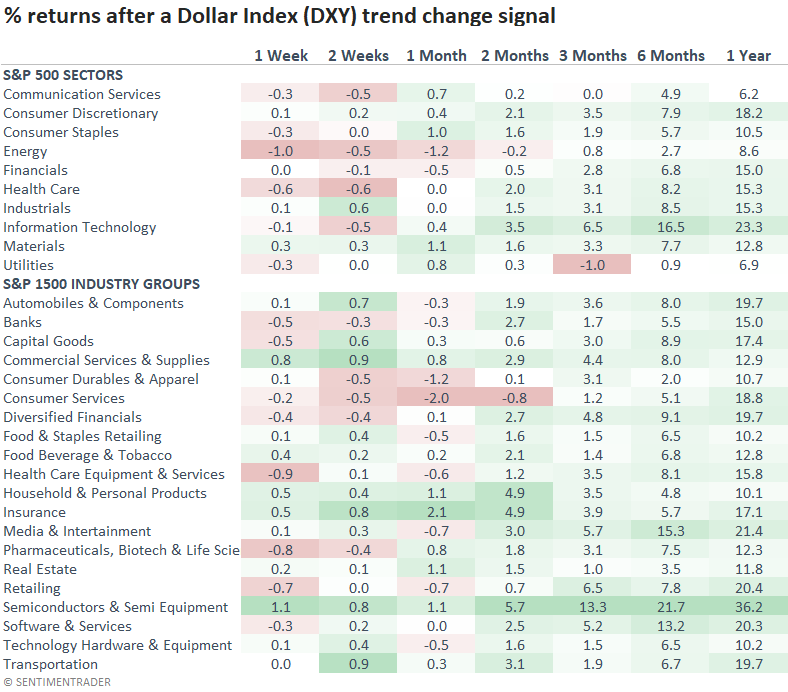

Most sectors and industries decline in the first four weeks after a dollar trend change. Still, they tended to recover and post solid returns in the six- and 12-month periods, especially Technology. Remember, a large percentage of Technology revenues come from outside the United States.

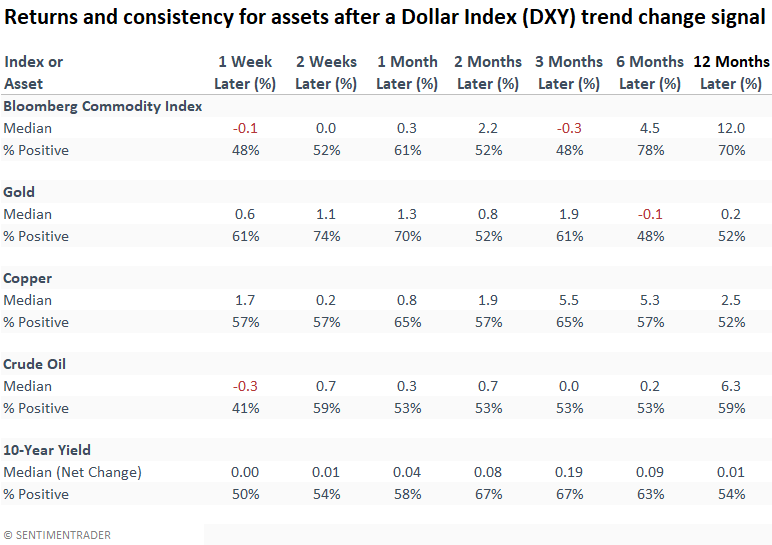

Commodities tend to benefit, and long-term yields could tick up a little

Commodities were mixed up to three months later. However, the long-term results look solid. On the other hand, Gold's performance was front-loaded, with a bullish outlook in the first month.

Interestingly, the 10-year yield shows a slight uptick across most time frames, which conflicts with a recent note suggesting rates could fall in the coming months.

What the research tells us...

The relentless rise in the dollar, crude oil, and interest rates resulted in tightening financial conditions, which wreaked havoc on equity markets around the globe. The toxic combination is reversing, which is typically a good thing for stocks. However, we must be mindful that the u-turn could signal a more significant economic slowdown is on the way. If that is the message, risk assets, like stocks, will suffer, and the Dollar Index (DXY) will likely turn higher from here.