The big picture for the bond market

Key Points

- Interest rates tend to move in long-term waves

- The long-term trend in interest rates has arguably reversed from a downtrend to an uptrend

- Treasury bonds are a pure play on interest rates and will continue to decline as long as interest rates continue to rise

- Investors may need to adjust their thinking towards bonds as a safe haven

- After a nearly 40-year decline in interest rates, many investors will struggle to "unlearn" everything they thought they'd learned about bonds in the past four decades

- In the near term, the recent decline in bond prices is likely to moderate (which will be detailed in Part II)

The big picture

Interest rates had been down-trending for almost 39 years - from October 1981 into March 2020. The chart below (courtesy of AIQ TradingExpert) displays ticker TYX (which tracks the yield on the 30-year treasury bond x 10) and its 120-month exponential moving average from 1970 to the present. Interpretation is fairly simple:

- TYX < 120-month EMA = declining interest rate trend

- TYX > 120-month EMA = rising interest rate trend

The treasury yield topped at 15.2% in October 1981 and then declined for almost 39 years before bottoming at just 0.84% in March 2020. Since that time, the yield has risen to roughly 3%.

By this measure, a rising rate trend began in 1973, and a declining rate trend was established in 1985 (when TYX dropped below its 120-month EMA). After 37 years in a confirmed downtrend, TYX finally moved decisively back above its 120-month EMA during April 2022. This suggests the beginning of a new long-term rising trend in interest rates (although a "whipsaw" - whereby TYX reverses and drops back below its 120-month EMA - is always possible with any moving average-based trend following method).

Where to from here?

Now that TYX has moved above its 120-month EMA, the character of the bond market has changed, and we may be in the very early stages of a long-term rise in interest rates. How long? The chart below (courtesy of McClellan Financial Publications) suggests that interest rates move in roughly a 60-year cycle - 30 years down and 30 years up.

According to the 60-year interest rate cycle suggested in the chart above, the low in rates in 2020 was essentially ten years "overdue." If rates follow this long-term cycle, we should expect to see interest rates generally trend higher into 2040 (a close look at that chart above reminds us that, a) this cycle is by no means exact, and rates do not rise or fall in a straight line).

This turn of events suggests that investors may need to forget most of what they learned about the bond market over the past four decades (i.e., bonds do not always go up, and bonds are not always a safe haven).

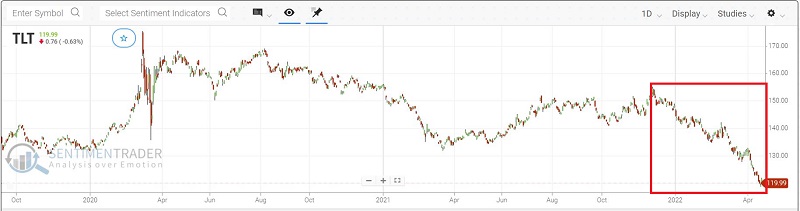

Long-term treasury bonds - the purest play on interest rate changes have, not surprisingly - been hit hard as rates spiked in recent months. The chart below displays the ticker TLT (iShares 20+ Year Treasury Bond ETF). Note that this ETF has lost roughly -33% since peaking in March 2020 - including a -22% plunge since December 2021.

As Jason has covered in-depth recently, the general good news is that most overbought/oversold and sentiment indicators for bonds have reached extreme levels. This situation cannot last forever. So, there is reason to expect bonds to "bounce." Unfortunately, the reality is that treasury bond prices react first and foremost to changes in interest rates. So as long as rates trend higher, bond prices will remain under pressure.

In Part II, I will detail a potentially positive development starting soon despite the overwhelming gloom and doom surrounding the bond market and the realities of the effect of rising rates on bonds.

What the research tells us...

The evidence suggests that we may be in the early stages of a long-term rising trend for interest rates. The danger is twofold:

- Rising interest rates make money more expensive and have a profound impact - much of it negative - on the overall economy

- Investors have been conditioned over the past 40 years to operate in a declining interest rate environment

Investors overwhelmingly have learned that bonds are a steady source of returns. In reality, they are only a steady source of returns when interest rates fall. When interest rates rise - particularly when the initial interest rate is very low - the reality changes dramatically. Likewise, many trading systems and strategies are designed to switch to long-term treasury bonds as a wealth-generating safe haven when the stock market goes south. This explains why so many investors are shocked by what has happened so far in 2022, with both stocks and bonds getting hit hard.

Unlearning 40 years of bond market lessons will not be easy for most investors. But it may be essential for success in the future.