Surge in Chinese & HK stocks

As you've no doubt heard by now, Chinese equities have surged higher. This has pushed several breadth stats to historic extremes. Whether this will lead to another bubble like the one China experienced in 2015 is yet to be seen, but these breadth extremes are at least short term bearish for Chinese stocks.

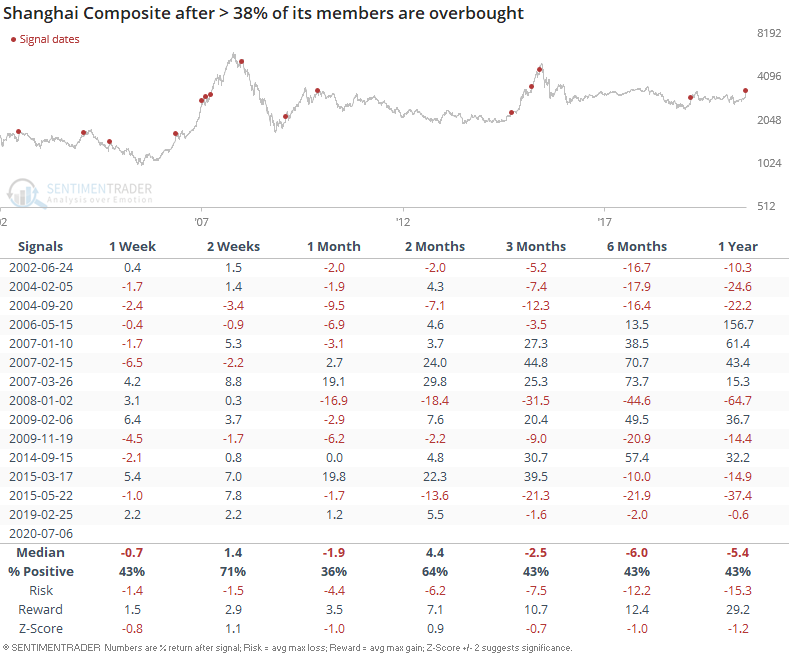

The rally has been decently broad-based, with almost 40% of Shanghai Composite members being overbought:

Similar historical cases led to weaker than average returns over the next month and 3+ months:

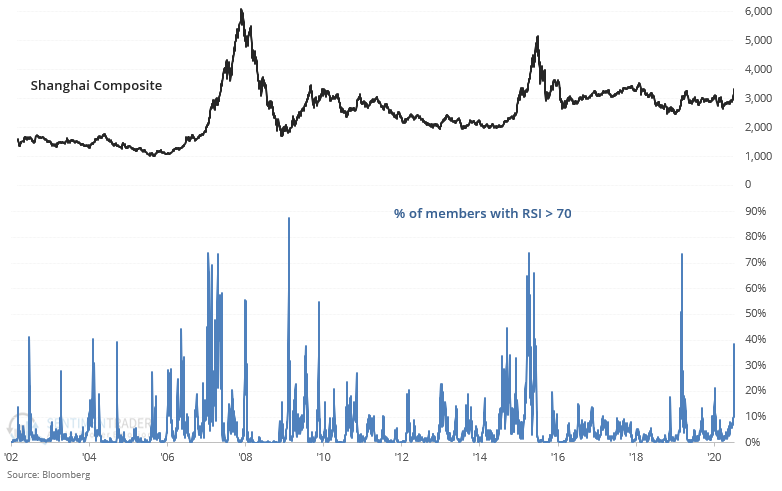

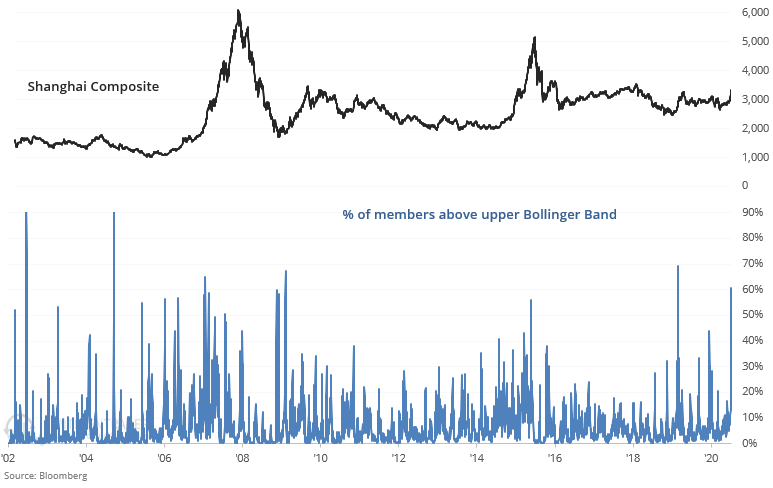

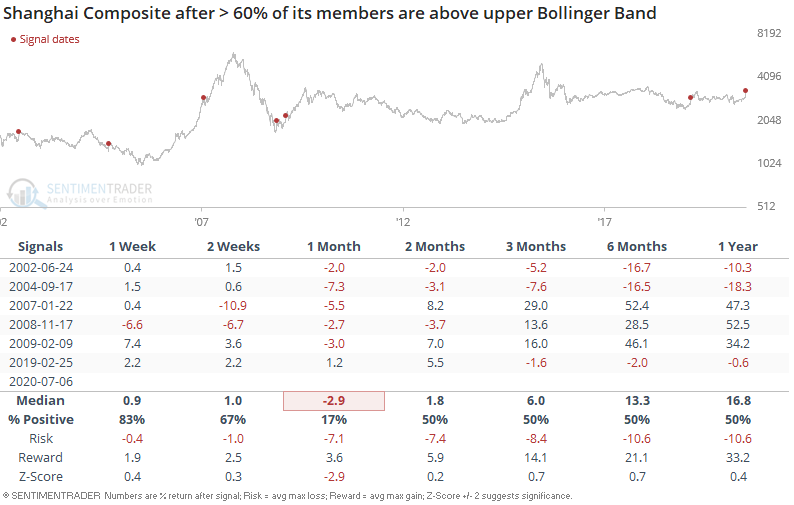

On a similar note, a solid 60% of Shanghai Composite members are above their upper Bollinger Band:

Such an across-the-board jump in Chinese stocks usually led to losses over the next month:

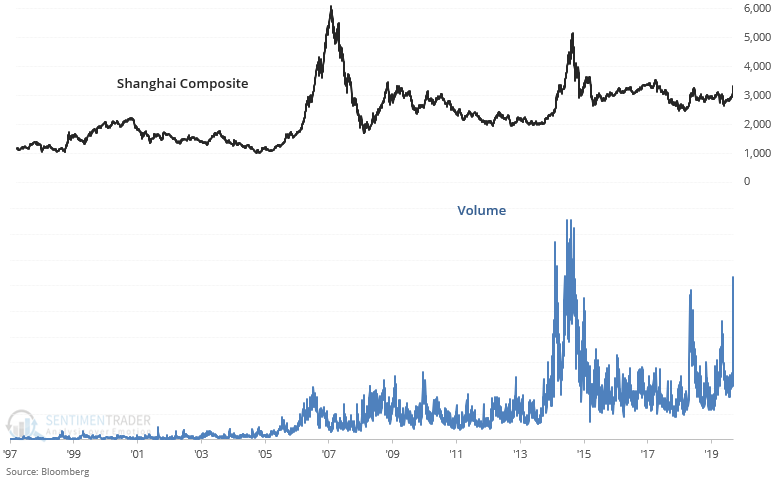

The jump in Chinese stock prices has been accompanied by a jump in volume:

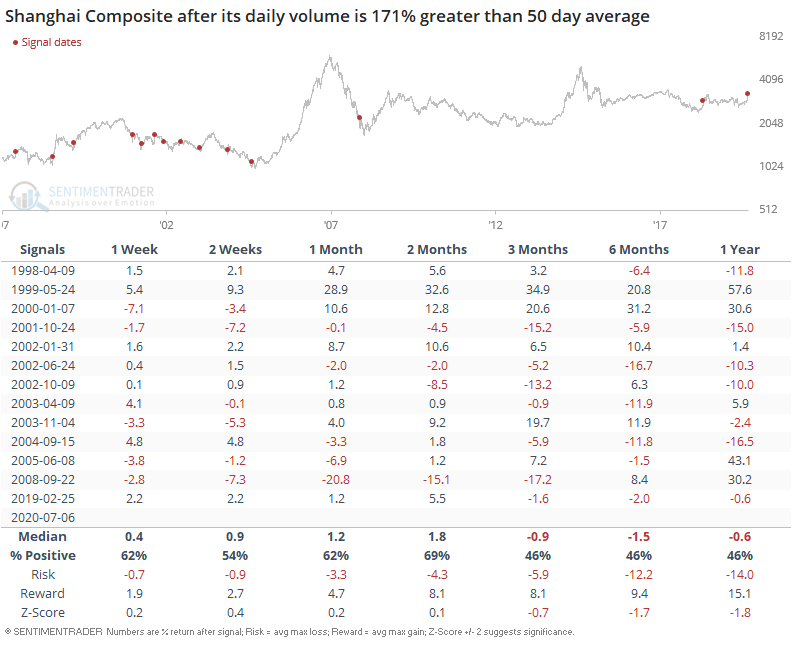

The last time we saw such high volume occurred during the 2014-2015 China bubble. Instead of looking at volume as a nominal #, we can compare it against its 50 day average. Historical cases of volume spikes led to worse-than-average returns for Chinese stocks over the next 6-12 months:

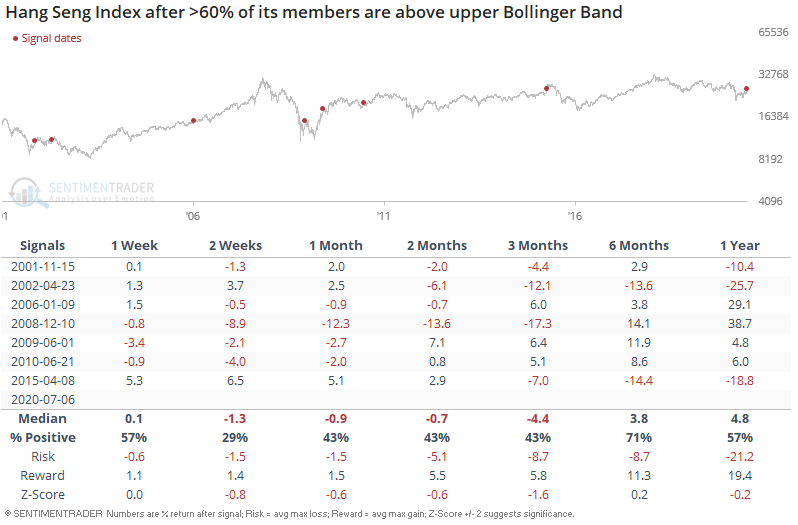

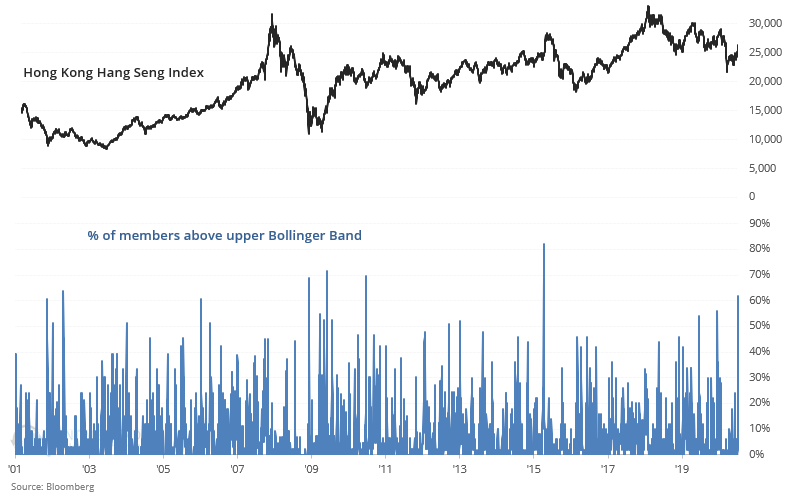

In Hong Kong, 62% of Hang Seng members are above their upper Bollinger Band:

As was the case in China, this usually led to losses for Hong Kong stocks over the next 2 weeks: