Stocks can rebound, but a recession looks more likely

Key points:

- More than 20% of sub-industry groups have declined > 40% from a 252-day high

- The consumer discretionary sector shows more than 50% of groups down > 40%

- After similar conditions, stocks tend to rebound, but a recession looks more likely

A rebound in stocks with a potential recession on the table

In a recent note, I shared a study that suggested the market could rally as selling pressure in sub-industry groups reached an extreme level within the context of a bear market. The S&P 500 rallied over 5% in two days. However, it subsequently rolled over and registered a lower low.

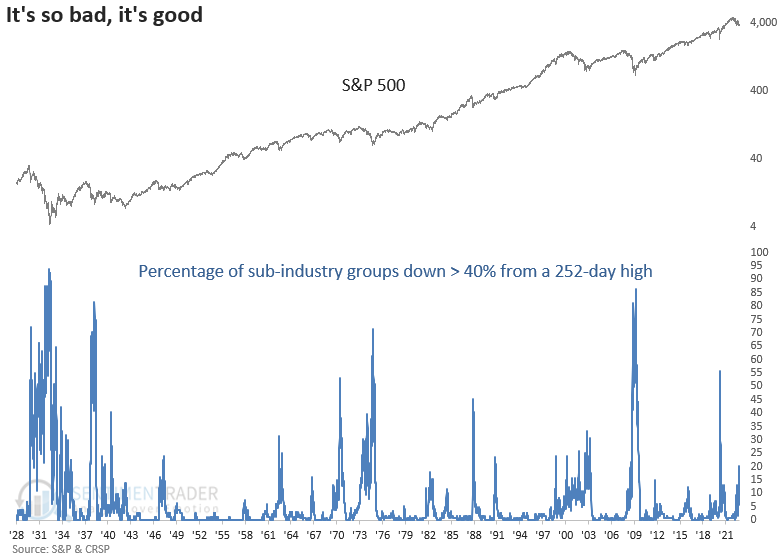

This week, the big-picture backdrop continued to deteriorate as more and more sub-industry groups declined by a significant amount relative to their annual highs. For only the 20th time since 1929, the percentage of sub-industry groups down 40% or more from a 252-day high exceeded 20%.

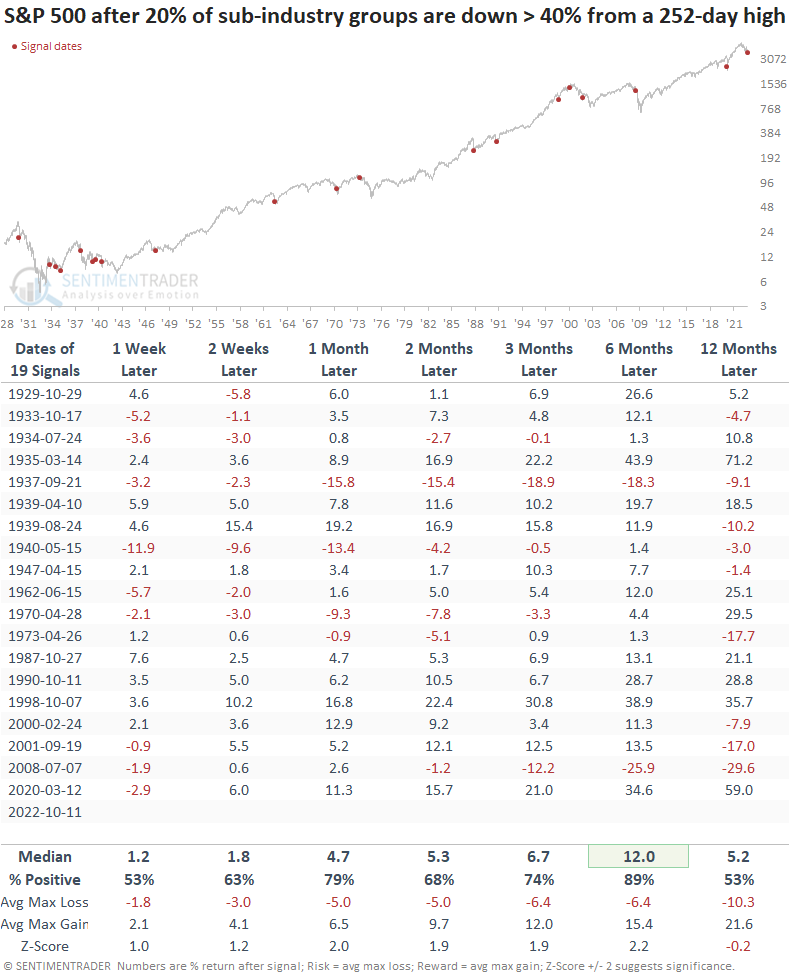

Similar readings preceded positive returns across medium-term time frames

When the percentage of sub-industry groups down > 40% from a 252-day high exceeds 20%, the S&P 500 typically rebounds on a medium-term basis. i.e., It's so bad, it's good. The signals in 1937 and 2008 were the exception, with pretty sizable drawdowns in the six-month window.

Returns and win rates deteriorate in the 12-month period, which should act as a reminder to keep an open mind concerning all outcomes.

High inflation and rising rates impact the consumer

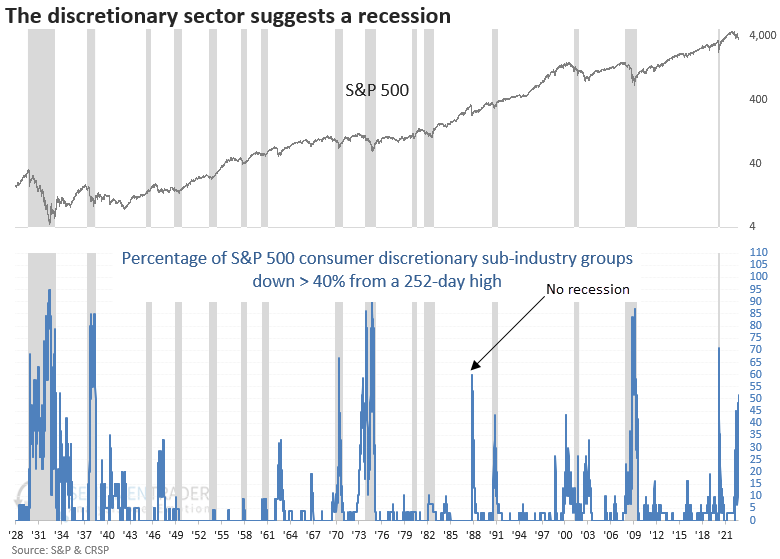

Sub-industry groups within the consumer discretionary sector dominate the number of groups down > 40% as the toxic mix of high inflation and rising rates impact the consumer.

On the brighter side, groups within the financial sector are almost nonexistent on the list. That's a good thing, as it lessens the likelihood of a banking crisis in the near term.

When I measure the percentage of sub-industry groups within the consumer discretionary sector that are down > 40% from a 252-day high, the indicator surpassed 50% on Tuesday. Except for 1987, all other readings of 40% or more occurred within the context of a recession. In the case of the 2001 recession, the signal occurred about a year prior.

I would keep an eye on the discretionary consumer sector as personal consumption drives a high level of economic output in the U.S.

What the research tells us...

The environment for stocks remains challenging as the toxic mix of high inflation, and rising rates continue to weigh on the outlook. While the market is once again oversold and looks poised for another countertrend rally, one must keep an open mind as recession risks look more likely. I would keep a close eye on the consumer discretionary sector, given its propensity to signal a potential upturn in the business cycle and the stock market around bear market bottoms.