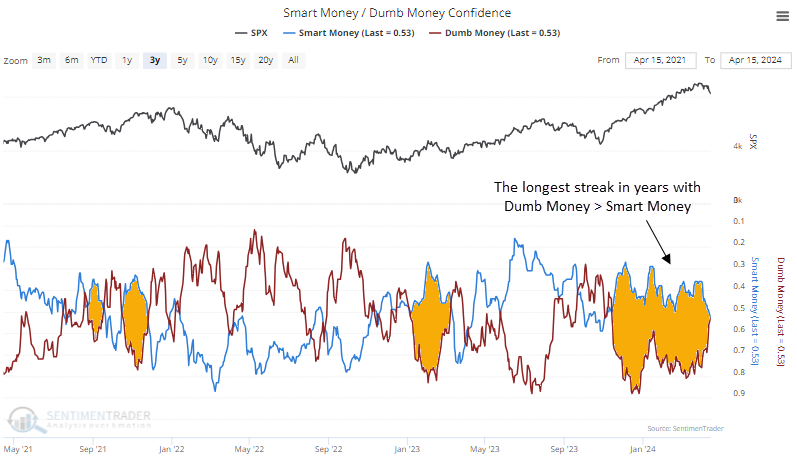

Smart and Dumb Money are on equal footing

Key points:

- For the first time in almost six months, Smart Money Confidence and Dumb Money Confidence are equal

- That ended a long streak of net optimism, which is typically only seen during ongoing bull markets

- After streaks of optimism ended, the S&P 500 showed a strong tendency to rebound in the months ahead

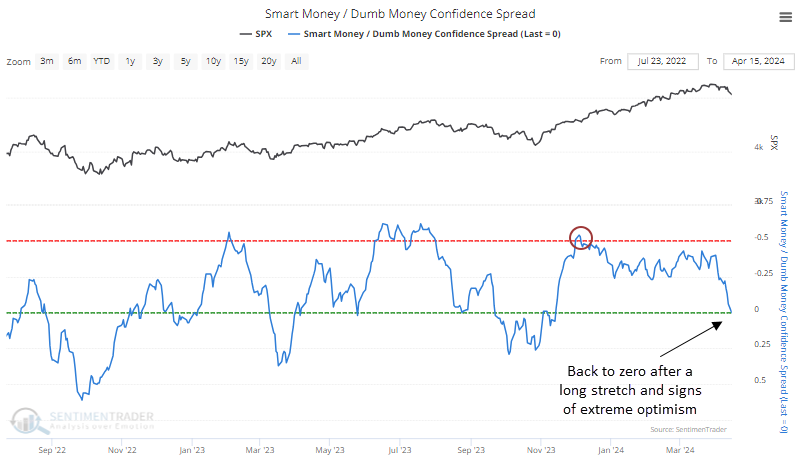

Smart Money = Dumb Money

After nearly six months, investors' optimism has evaporated. All it took was a few days of selling and the cessation of some long streaks of momentum.

For the first time since November, Smart Money is assigning the same confidence of a rising market as Dumb Money. This is a stark change from just a week ago.

When we look at the spread between the two sentiment measures, we can see more clearly that they have equalized after a prolonged period of extreme. During bear markets, we generally don't see the spread last this long without reverting (the scale is inverted to more clearly show the relationship between the indicator and stock prices).

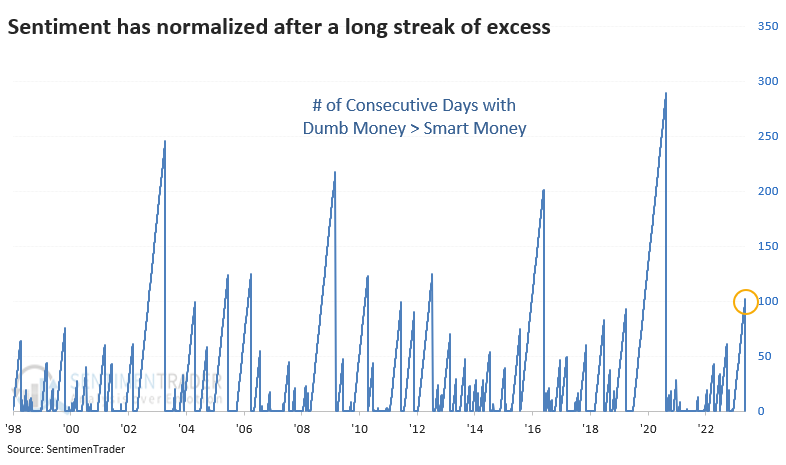

This ended the 7th-longest streak of excess since we began calculating these models in 1998.

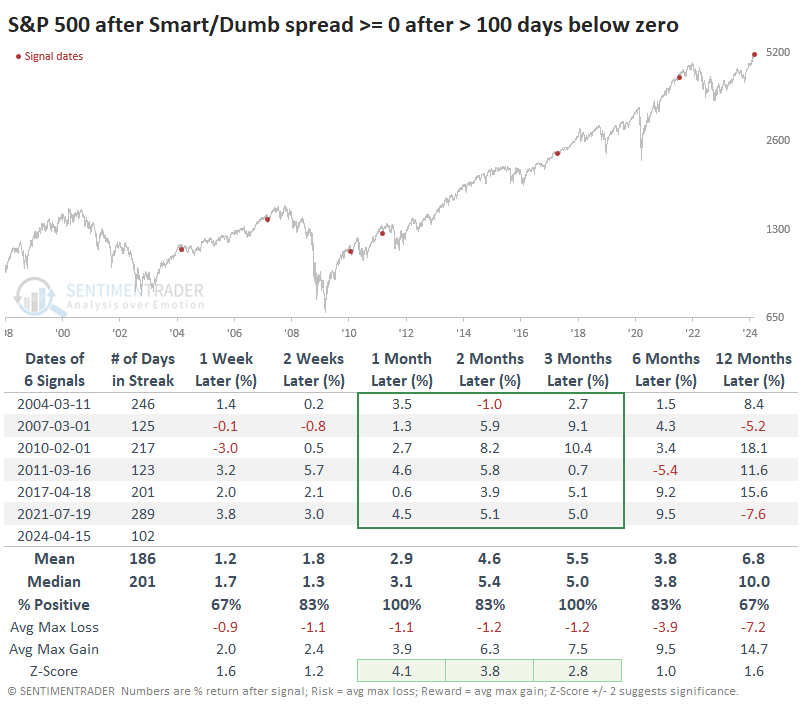

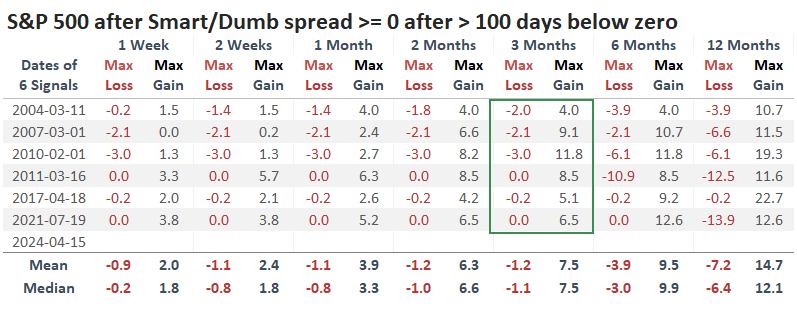

Bulls see their chance after prolonged excess

After sentiment became normalized following a long period of extreme, the S&P 500 has done very well over the medium term. It didn't suffer any losses of magnitude during the next one to three months. Note that the table only includes streaks when Dumb Money exceeded Smart Money by at least 50% at some point.

The most significant drawdown over the next three months was a minuscule -3.0%, while the average drawup (maximum gain) was +7.5%. That suggests a favorable risk/reward scenario for bulls. However, within the three months following that, there was a lot more turbulence.

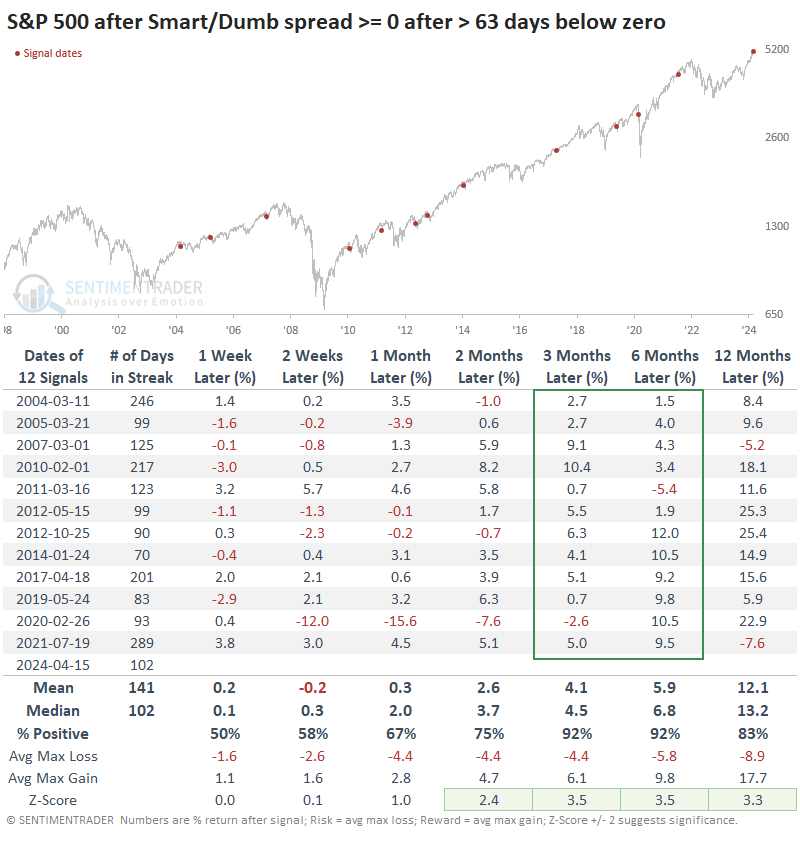

We reach the same general conclusion if we relax the parameters and look at the ends of streaks of three months or more with excessive sentiment. There were twice as many precedents, but every signal showed a gain either three or six months later. It wouldn't have been pleasant for the buyer taking this signal in February 2020, but it did work out if holding for six months+.

What the research tells us...

Last fall, stocks held up magnificently well even after sentiment initially reached extreme optimism. That's a hallmark of developing bull markets and proved to be so once again. Now that we've had the first taste of real selling pressure since November, investors have quickly become fearful, or at least a heck of a lot less optimistic.

When sentiment normalizes after a prolonged stretch of extreme, it has never resulted in an immediate bear market. Or even correction. Or really even a pullback. Bulls who missed out on the gains finally see their chance to get in, and without fail, they've pounced. Of course, we're relying on investors behaving like they have for the past 25 years, which might not work. But the one thing we've become most confident about over the decades is that human behavior is the most reliable aspect of auction markets.