Small caps when strong internals are a trap

Key points:

- The Russell 2000 just completed a rapid -10% correction from a three-year high.

- Historical base rates for this specific technical breakdown skew bearish over the next two to three months.

- Counterintuitively, strong underlying breadth during the breakdown has historically led to worse intermediate-term outcomes.

A sudden air pocket

The relentless small-cap rally hit a wall last week. On March 20, the Russell 2000 closed 10% below its recent three-year high. The speed matters. This reversal played out in under 30 days, catching offsides a market positioned for an uninterrupted expansion.

Across the 21 times the index has fallen from a three-year high into a correction since 1983, the forward returns are persistently choppy. Over the following two months, the index was higher only 45% of the time, averaging a 1.7% loss. The longer-term risk-reward profile is decidedly symmetrical. Over the subsequent year, the index offered an average maximum gain of 12.7% against an average maximum drawdown of 13.9%.

Speed kills momentum

Fast reversals compound the near-term weakness. Narrowing the lens to corrections that materialized within 30 trading days leaves only eight prior signals. The two- and three-month forward returns for this cohort are dismal. The index was positive just 38% of the time across both windows, averaging outright losses. A sudden shift in the prevailing trend typically requires months of consolidation before a durable bottom forms.

The breadth trap

Counterintuitively, resilient internals make the setup more dangerous. We typically view strong underlying participation as a structural shock absorber during index-level drawdowns. The data points the other way. When the Russell 2000 drops into a correction with the majority of its members still holding above their 200-day moving averages, the selling tends to accelerate.

Across the eight signals featuring the strongest breadth, the two- and three-month forward returns were positive only 29% of the time. The index averaged a loss of roughly 4% to 5% over those windows, and the one-year win rate drops below a coin flip. This suggests that when the index breaks down but individual stocks haven't fully rolled over, the market is merely in the early innings of a broader capitulation.

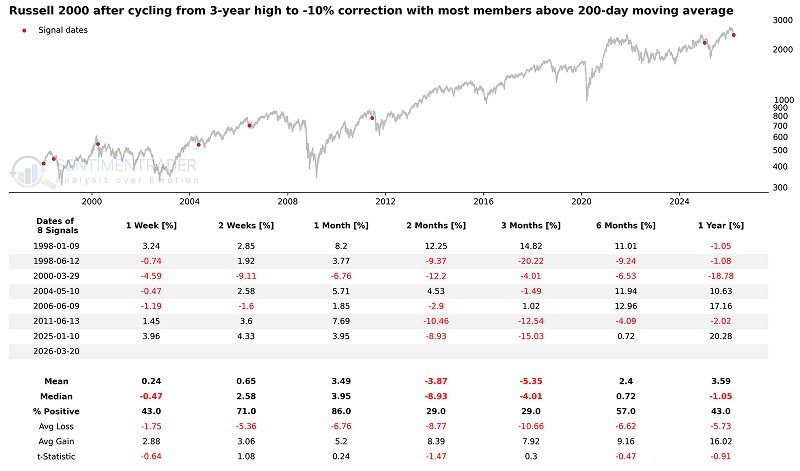

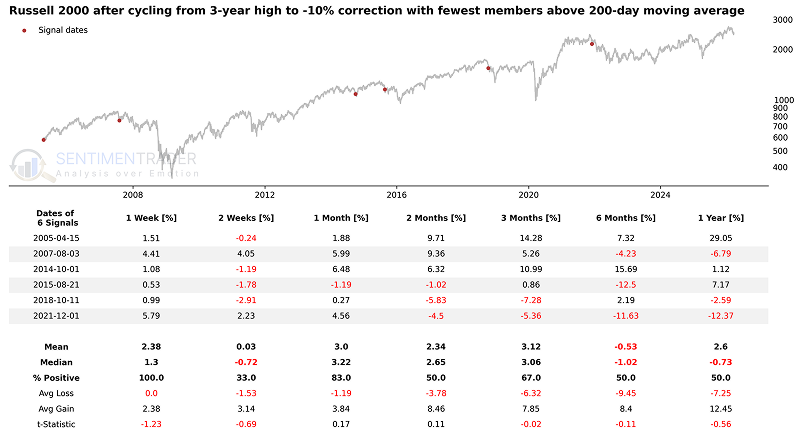

Compare that to corrections driven by entirely washed-out markets. When the fewest members hold their long-term averages at the time of the signal, the near-term returns flip positive. Over the following month, the index was higher 83% of the time. A breakdown built on already-depressed internals sets the stage for a mean-reversion bounce. A breakdown with elevated breadth implies there is plenty of dead wood left to clear.

What the research tells us...

Price action demands respect, and the underlying internals confirm the need for caution. The rapid 10% drawdown from multi-year highs carries a bearish base rate across the medium term. Strong participation above the 200-day moving average historically amplifies that downside risk rather than neutralizing it. History favors a cascading selloff as the remaining stocks holding onto their long-term trends eventually succumb to the gravity of the index. The setup argues for defensive positioning over the next quarter. If the remaining constituents rapidly break below their moving averages, the conditions for a durable, washed-out bottom may begin to form.