PortfolioEdge Update for Sept 1

Key points:

- Stocks have fallen back after major thrusts and retracement

- The overall outlook is more muddied than ever, with vastly contradicting signals

- We're back in a sell-everything mentality, which may yet last a while

Commentary

The last month, and longer, has been a lot of sound and fury. Whether it signifies nothing is open for debate.

I've been dormant with changes to the portfolio because there has been a wild crosscurrent of inputs, and there is no clear message. Things were looking great a few weeks ago; now not so much. During bear markets, it's easy to get whipsawed.

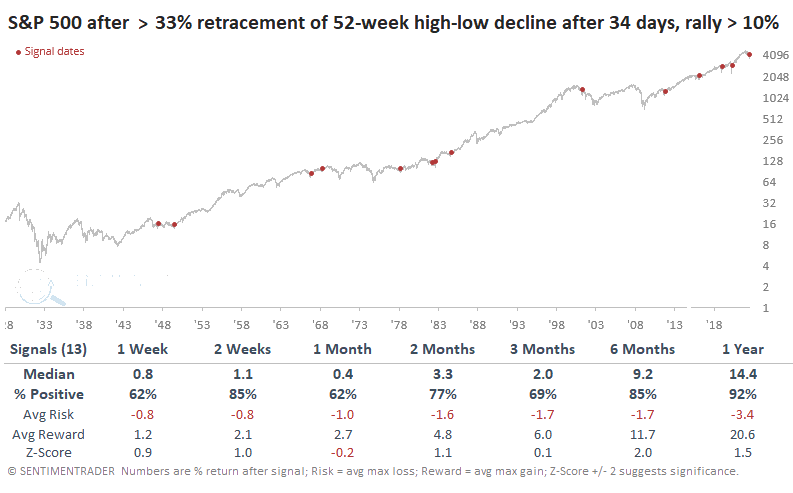

The biggest point in bulls' favor has been the size of the retracement of the decline. The table below shows every rally from a 52-week low when the S&P 500 retraced at least a third of its decline over 34 days. The index had to be at least 10% higher than its low. There was a failure in 2001, which is a concern; it was also the only one.

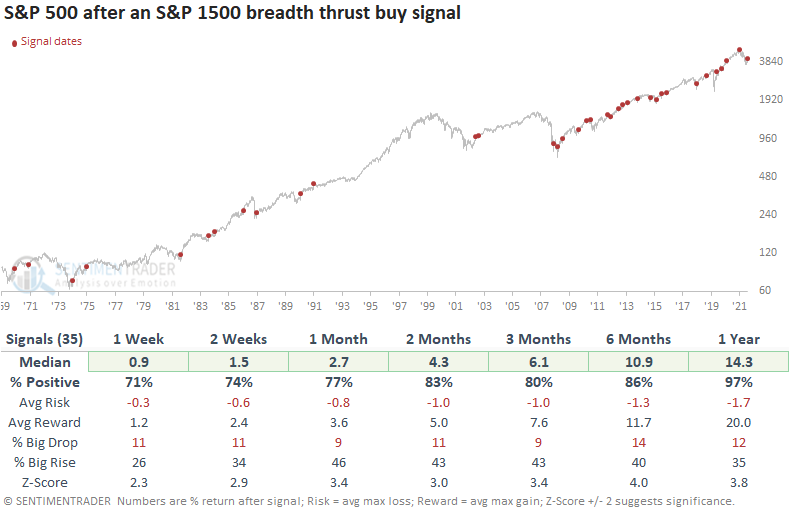

We've spent a lot of time since June on the overwhelming buying interest among a wide variety of stocks and high-yield bonds. When there is participation like we saw at the end of July, it has preceded long-term positive returns almost without fail.

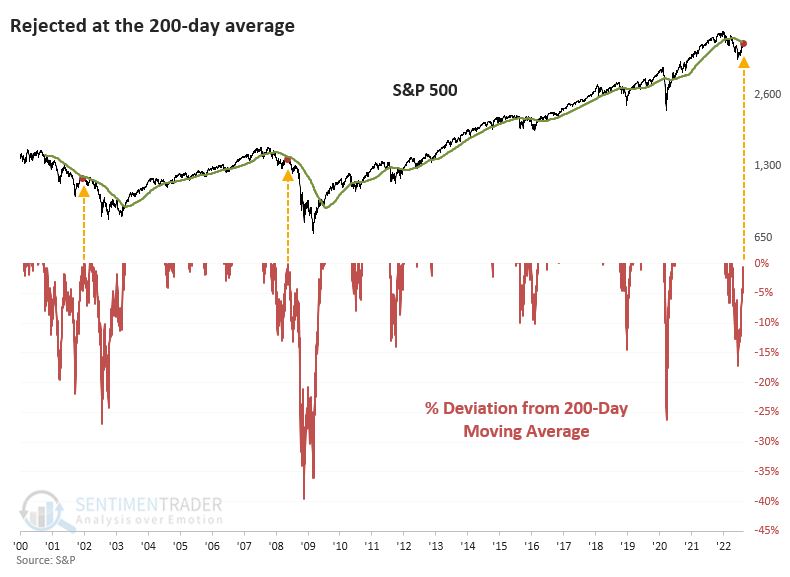

The biggest issue is that in recent weeks, there has been no follow-through. The most important index in the world failed at its most important technical level.

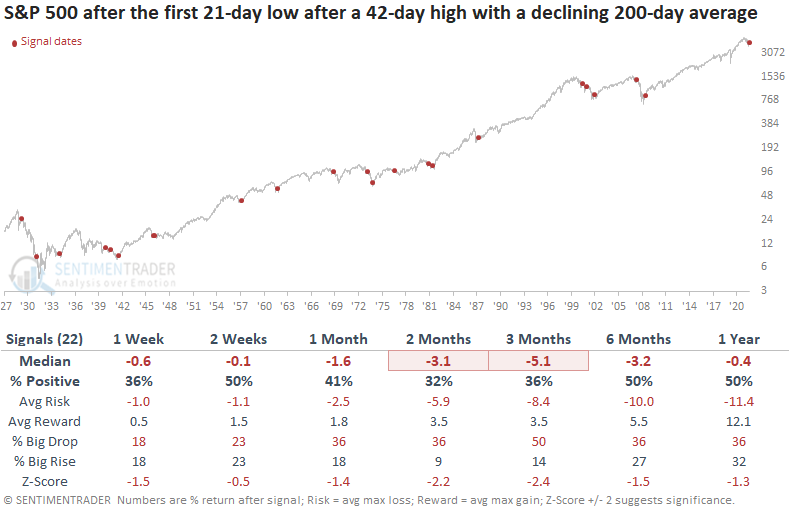

Dean noted that when the S&P has quickly reversed from a multi-month high to a one-month low during a protracted downtrend, it tends to keep going.

Stocks reached an overbought condition with optimistic sentiment, and the reaction since then has been fairly typical but still a bit troubling for bulls. There isn't much, so far, to indicate that all the positive factors that lined up in June and July are now null, but whenever we see such persistent selling in bear markets, it raises the specter of an outright failure.

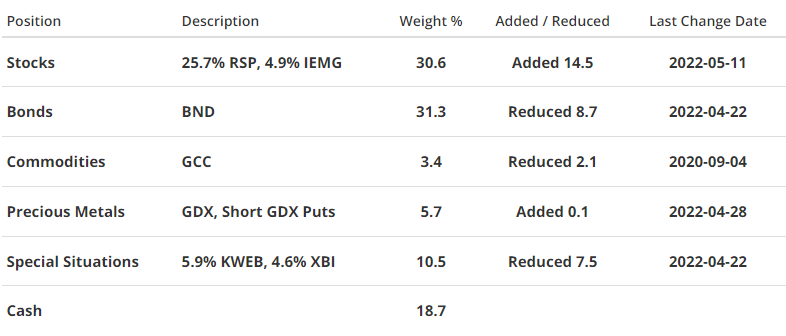

Portfolio updates

STOCKS

S&P 500 Equal-Weight (RSP) - I considered raising exposure to stocks in early July. I didn't want to buy into a rising market in a long-term downtrend, despite the numerous bullish studies we discussed. That was a mistake, assuming I also would have lowered exposure after we became overbought. For now, I don't see the sense in making any big changes, though at the moment I'm more likely to add exposure if we continue to sell off into September and generate some extremes. I'm putting quite a bit of faith in the breadth thrusts that were generated in June and July, with their historical tendency to lead to positive longer-term returns.

iShares Core MSCI Emerging Markets (IEMG) - The strong dollar has not been kind to these shares, and the overall poor environment hasn't helped. I continue to believe emerging markets may be a better opportunity than domestic ones in the year(s) ahead and am holding for now.

BONDS

Vanguard Total Bond (BND) - There were compelling signs that we'd seen capitulatory selling in early June, and the fund rebounded impressively. A hawkish Fed threw cold water on that rally, and bonds have spent most of August reversing their gains. I don't have a lot of confidence here, given so many failed setups in recent months. Holding for now.

PRECIOUS METALS

VanEck Gold Miners (GDX) - Miners saw overwhelming selling in July. The sector has a strong tendency to rebound from bouts like that but managed only a weak bounce before rolling over, and the fund is now probing lower lows. I have no interest in adding exposure to this sector.

COMMODITIES

WisdomTree Enhanced Commodity Strategy (GCC) - I'm not seeing anything especially compelling here, so holding for now.

SPECIAL SITUATIONS

KraneShares CSI China Internet (KWEB) - Investors re-discovered this group in July, and mainstream sentiment has been shifting to a much more positive tone. Almost immediately, that invited selling, which is not encouraging. Still, the setup here is similar to energy in 2020, going from an un-investible area to one socially acceptable. I continue to believe this offers a good opportunity on a very long-term (1+ year) time frame. Holding for now.

SPDR S&P Biotech (XBI) - After repeated failed setups, my conviction in this fund dropped significantly in June. Remarkably, biotech stocks found support at prior lows and surged in July. They've since been consolidating gains, so I'm holding for now.

Portfolio Summary and Disclaimers

RETURN YTD: -6.7%

RETURN YTD: -6.7%

2021: +8.7%, 2020: +8.1%, 2019: +12.6%, 2018: +0.6%, 2017: +3.8%, 2016: +17.1%, 2015: +9.2%, 2014: +14.5%, 2013: +2.2%, 2012: +10.8%, 2011: +16.5%, 2010: +15.3%, 2009: +23.9%, 2008: +16.2%, 2007: +7.8%

Not intended as investment advice. In this account, we roughly follow what has become known as the All Weather portfolio popularized by Ray Dalio. It allocates across four broad assets, designed to hold up no matter the market environment. The goal is modest positive returns while limiting large, sustained losses. We typically use popular ETFs with low costs. At times, we will swap out for a fund we believe has better prospects or simply lower fees if not. At other times, we will diverge quite a bit from baseline allocations, largely depending on the indicators and studies we discuss on the site. The base allocation includes stocks (35%), bonds (35%), gold (5%%), commodities (5%) and cash/other (20%).