PortfolioEdge Update for May 6

Key points:

- This is the most challenging market in at least 25 years, with persistent and widespread losses

- Sentiment is nearing extreme pessimism, but likely within the context of a bear market

- It's difficult to have high conviction in any investment at the moment

Commentary

There have been some tough markets over the last 25 years. This is the toughest I've ever seen.

During 1999 and 2000, FOMO was a daily battle. I was out of tech stocks, and seeing others make daily 25% gains no matter the stock, usually from overnight gaps, was hard to stomach.

The 9/11 tragedy and ensuing bear market weren't easy by any stretch, but quite a few stocks held up reasonably well until the final meltdown in the summer of 2002. The following bull market was probably the most fun of any market I can remember. Most investments went up, and there were solid fundamentals behind them.

Until we got to 2006. I was convinced we were in a bubble, but it kept going. And going. Again, FOMO was terrible during much of 2007, and that's always a hard emotion to battle. I became equally convinced we were in a new bear market in January 2008 and focused chiefly on short trades for one of the rare times in my investing life. Between that and a soaring bond market, the scary near-collapse of our financial system was tolerable.

The massive rebound during the first several months following the panic was also "easy" to have conviction, though daily volatility was extreme. Since that point, there have been multiple difficult markets, on both the upside and downside, where I had high confidence that markets would do one thing or the other, and I was wrong. But at least most moves were relatively minor and didn't last long.

This is something altogether different.

I have never personally experienced a market this confounding, with almost everything losing substantial value amid a mind-numbing number of cross-currents.

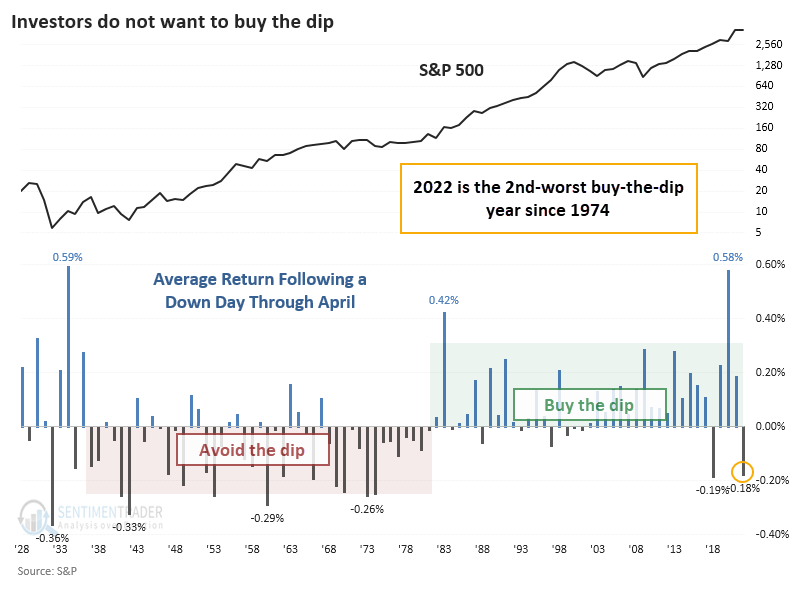

In recent research reports, the theme has been that equity investors are suffering selling pressure and a lack of interest among investors not seen in decades. This is only the 2nd year in history, besides 1932, when the S&P 500's average returns following an up day AND following a down day were both less than -0.1%. Following a down day only, the S&P's return is -0.18%, the 2nd-worst since the early 1970s.

A lousy return in April tends to lead to more bad returns in the following months, and other than an outlier on Wednesday, selling pressure has been overwhelming. Again, this is the type of behavior we've typically only seen during very tough environments that tend to persist for month(s) more. The recent internal breakdown in Financials is also worrying, as similar conditions preceded poor medium-term returns.

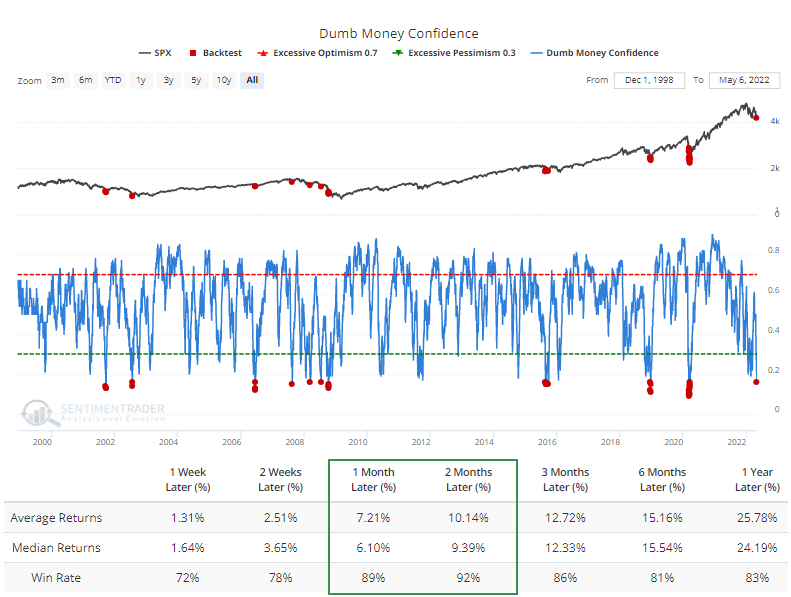

About the only potential positive is sentiment, which has quickly cycled back into extreme pessimism. Even during protracted bear markets, readings like we see now have typically preceded multi-week or even multi-month rebounds.

It's disturbing that more moderate extremes earlier this year only led to a brief reflex rally, and the subsequent buying thrusts failed to see any follow-through. That is a stark change from virtually the entire past 12 years.

I had sell orders ready on Tuesday for half of my already-small allocation to the S&P 500 and the entirety of the flailing Biotech sector. I didn't submit them and felt good about it on Wednesday. Then felt terrible yesterday. It's that kind of market - relief one day, angst the next.

The bottom line is that we remain in an extremely unhealthy environment with risk-off behavior. While sentiment extremes are compelling, they're not necessarily screaming buy signals just yet. As a result, I am standing pat.

Portfolio updates

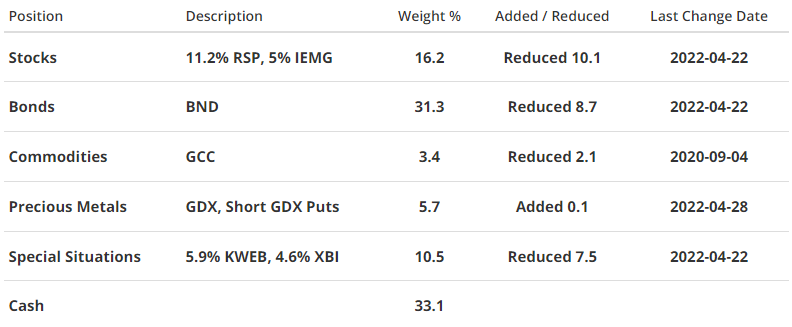

STOCKS

S&P 500 Equal-Weight (RSP) - I continue to favor the S&P 500 as an index for equity exposure, as well as the equal-weight version of the index. That is holding up relatively well and hasn't made a lower low during the latest leg down. I'm not entirely convinced it will continue to do so and don't have high conviction in a sustained rally even with the extremes in sentiment.

iShares Core MSCI Emerging Markets (IEMG) - No change - I'm okay with holding this for now. There's probably a better opportunity here than in U.S. stocks in the months (years?) to come, especially in some of the more beaten-down sectors as we've covered with Brazil.

BONDS

Vanguard Total Bond (BND) - This has been the most aggravating market, even with the meltdown in some other markets. Some of the losses here are bordering on unprecedented, and it has the feel of forced or structural selling pressure. Pessimism is rampant, but it has been for a while and is having no impact. I'm not adding to bond positions yet.

PRECIOUS METALS

VanEck Gold Miners (GDX) - We recently looked at the internal pullback in many gold mining stocks. They've consistently shown impressive medium- to long-term forward returns when they pull back after a surge like they enjoyed starting the year. Holding for now, and may add if they pull back further, either via the short puts or by taking an outright position.

COMMODITIES

WisdomTree Enhanced Commodity Strategy (GCC) - No change here - many commodities have performed splendidly, and we maintain a 2.4% weight, below the target weight of 5%. The issue has been trying to add to positions in this market that have historically done poorly when overbought.

SPECIAL SITUATIONS

KraneShares CSI China Internet (KWEB) - As noted last time, these stocks have had difficulty sustaining any gains due to overwhelmingly poor sentiment. Headline risk is making some of these stocks swing 5%-10% daily. I believe they offer a good risk/reward opportunity on a very long-term (1+ year) time frame for the reasons noted in the last update and before.

SPDR S&P Biotech (XBI) - This simply isn't working. While biotech rebounded modestly from the extremes we noted in February, it has since failed and fell to persistently lower lows. Bullish reversal bars haven't led to short-covering, just more selling pressure. With increasingly attractive valuations, perhaps XBI can find support at its lows from 2018 and 2020, which aren't much further. The fund has already exceeded most of the prior precedents' maximum drawdown from the signal dates, suggesting they are less reliable as guides for how investors may behave this time around, so I do not have high conviction in this fund. I would be more likely to cut it than add any further exposure.

Portfolio Summary and Disclaimers

RETURN YTD: -4.2%

2021: +8.7%, 2020: +8.1%, 2019: +12.6%, 2018: +0.6%, 2017: +3.8%, 2016: +17.1%, 2015: +9.2%, 2014: +14.5%, 2013: +2.2%, 2012: +10.8%, 2011: +16.5%, 2010: +15.3%, 2009: +23.9%, 2008: +16.2%, 2007: +7.8%

Not intended as investment advice. In this account, we roughly follow what has become known as the All Weather portfolio popularized by Ray Dalio. It allocates across four broad assets, designed to hold up no matter the market environment. The goal is modest positive returns while limiting large, sustained losses. We typically use popular ETFs with low costs. At times, we will swap out for a fund we believe has better prospects or simply lower fees if not. At other times, we will diverge quite a bit from baseline allocations, largely depending on the indicators and studies we discuss on the site. The base allocation includes stocks (35%), bonds (35%), gold (5%%), commodities (5%) and cash/other (20%).