PortfolioEdge Update for Jun 15

Key points:

- One failed setup after another has pushed stocks (and bonds, and pretty much everything else) to new lows

- It's a risky time for new buyers as the potential for a waterfall drop is non-negligible

- But it also seems too late to sell, given historical reactions to similar selling pressure

Commentary

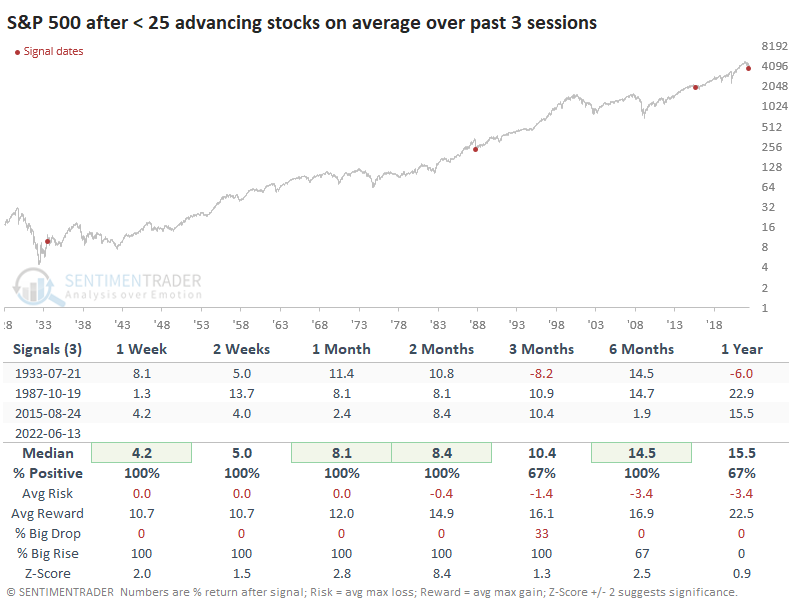

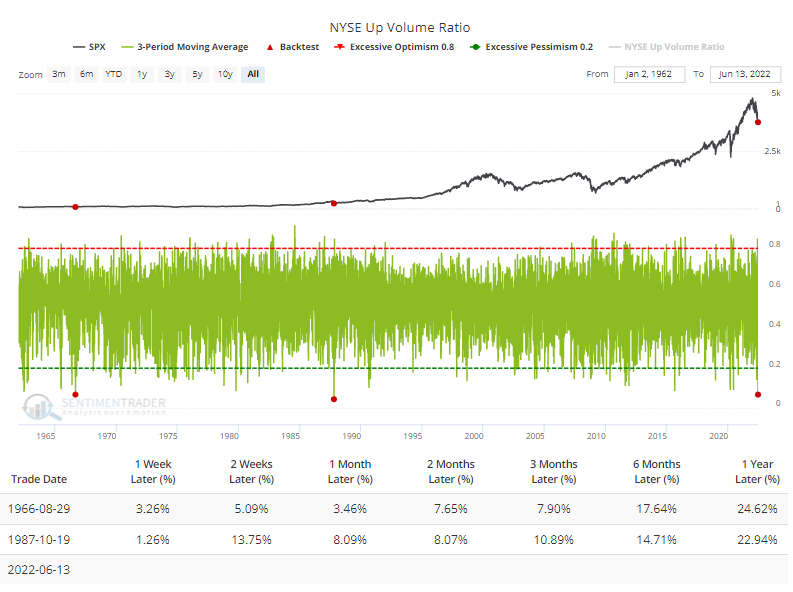

All of the medium-term positive implications from the extreme pessimism in mid-May, then the buying thrust afterward, have failed so far. While it's not unprecedented to see short-term volatility, it is unprecedented to see selling pressure like stocks (and pretty much everything else) suffered over the past week.

We've been looking at some of the carnage in reports over the past few days, and in many respects, it's historic. The 3-day span into Monday was accompanied by some of the most aggressive and widespread selling pressure we've ever seen.

It wasn't just in stocks within the S&P 500, or stocks in general. Bonds also got hit, so overall breadth on the NYSE was horrid. Over that 3-day stretch, an average of more than 93% of volume flowing into declining stocks. In 60 years, only the crashes in 1966 and 1987 can compare to what investors have suffered this week.

Now, we get the Federal Reserve decision and statement on interest rate policy today. I have no idea what they will do, should do, or how investors will react.

If you're looking for macro analysis here, you're going to be disappointed. I've been at this for a long time, and each year, I get less and less interested in macro analysis. It's extremely popular, but after all these years, I'm still unaware of anyone who is consistently effective at guessing the outcomes of macro conditions and their impacts on markets. It's like sports betting; there are a handful of people who have the knack for it and are wildly successful, but you almost certainly don't know who they are. They're not grousing on Twitter, that's for sure.

We're seeing pretty much all the hallmarks of a classic bear market, with clear lower lows and persistently failed bullish setups. For new buyers, this creates a high-risk scenario. For existing holders, it's an even more agonizing situation. While the risk of a further whoosh is relatively high, so is the opposite. Most of what we've looked at lately suggest that selling into the panic has been just as bad a decision (worse, actually) than buying early.

The one-two punch of bear markets in stocks and nearly there in bonds has been a historic challenge, and this is the most difficult market I've ever experienced or studied. It's also why I'm currently in the worst drawdown I've ever experienced. When conditions are highly fluid, I have a history of selling almost everything and re-grouping, even if that means buying back a few days later. I considered it last week, didn't, and am regretting it now, but hindsight is a wickedly bad habit for investors.

Portfolio updates

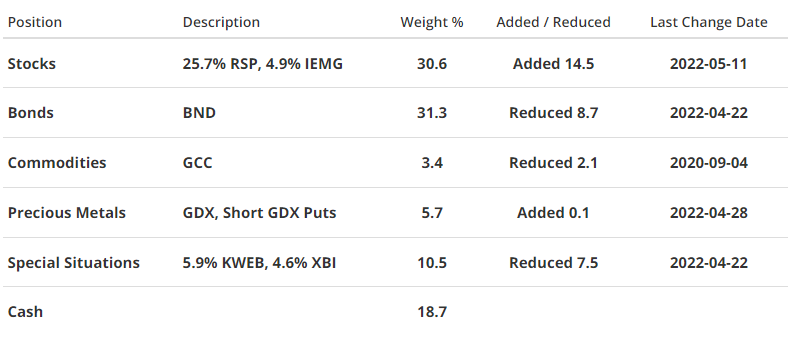

STOCKS

S&P 500 Equal-Weight (RSP) - I continue to favor the S&P 500 as an index for equity exposure, as well as the equal-weight version of the index. This is holding up better than the cap-weighted version, which is a small comfort, I guess. But it's still seeing lower lows and so far, no indications of stabilization. Holding for now, with no plans to add exposure.

iShares Core MSCI Emerging Markets (IEMG) - Even with global carnage in stocks and a skyrocketing dollar, this is holding up okay, thanks in large part to a rebound in Chinese shares. I continue to believe emerging markets may be a better opportunity than domestic ones in the year(s) ahead and am holding for now, with no plans yet to add exposure.

BONDS

Vanguard Total Bond (BND) - Just brutal. There is no other word for it. Bonds of virtually all stripes are suffering historic drawdowns, and the told-you-so crowd is out in force. There are compelling signs that we've seen capitulatory selling over the past week, but I don't have a lot of confidence in that given so many failed setups in recent months. Holding for now, with no plans to add exposure.

PRECIOUS METALS

VanEck Gold Miners (GDX) - In May, selling pressure in miners was so bad that it triggered an extreme reading in a Panic Breadth Composite. They did rebound, which is somewhat encouraging when looking at similar reactions in the past, but they've since succumbed with the latest bout of widespread selling pressure. Really mixed picture here. Holding for now, with no plans to add exposure.

COMMODITIES

WisdomTree Enhanced Commodity Strategy (GCC) - One of the few bright spots, or at least "not horrible" spots. Not much has been going on in this fund for the past three months when commodities went parabolic. Holding for now, with no plans to add exposure.

SPECIAL SITUATIONS

KraneShares CSI China Internet (KWEB) - This has been the one true standout among almost all non-inverse investments in recent weeks. The setup here is compelling, as we've discussed for months, and bucking the worst of the selling pressure lately is encouraging. I continue to believe this offers a good risk/reward opportunity on a very long-term (1+ year) time frame for the reasons noted in the last update and before. Holding for now, with no plans to add exposure.

SPDR S&P Biotech (XBI) - After a rebound from a bounce off support, biotech is right back to its lows. Like almost everything else, this has suffered one failed bullish setup after another, so I do not have high conviction in this fund. Holding for now, with no plans to add exposure.

Portfolio Summary and Disclaimers

RETURN YTD: -7.7%

RETURN YTD: -7.7%

2021: +8.7%, 2020: +8.1%, 2019: +12.6%, 2018: +0.6%, 2017: +3.8%, 2016: +17.1%, 2015: +9.2%, 2014: +14.5%, 2013: +2.2%, 2012: +10.8%, 2011: +16.5%, 2010: +15.3%, 2009: +23.9%, 2008: +16.2%, 2007: +7.8%

Not intended as investment advice. In this account, we roughly follow what has become known as the All Weather portfolio popularized by Ray Dalio. It allocates across four broad assets, designed to hold up no matter the market environment. The goal is modest positive returns while limiting large, sustained losses. We typically use popular ETFs with low costs. At times, we will swap out for a fund we believe has better prospects or simply lower fees if not. At other times, we will diverge quite a bit from baseline allocations, largely depending on the indicators and studies we discuss on the site. The base allocation includes stocks (35%), bonds (35%), gold (5%%), commodities (5%) and cash/other (20%).