PortfolioEdge Update for April 13

Key points:

- Choppy stocks haven't given a compelling reason to alter exposure meaningfully

- Bond carnage should present an opportunity though the risk of "it's different this time" is high

- Most other positions are just in wait-and-see mode

Commentary

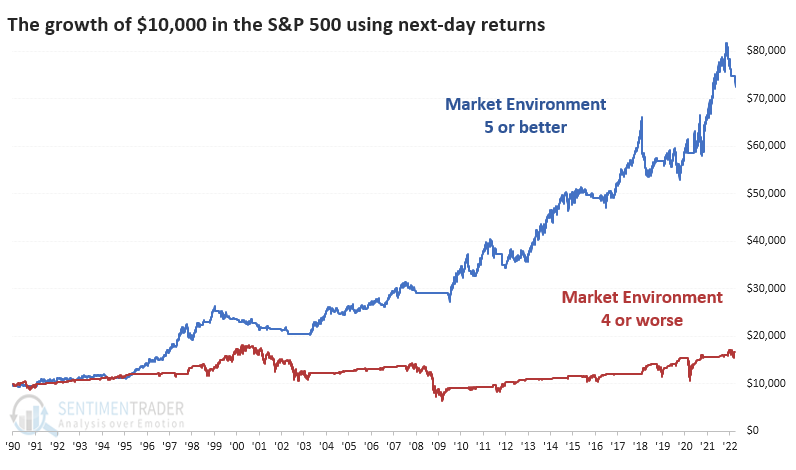

It's been a volatile few weeks in most markets, particularly stocks (chop) and bonds (almost straight down). Most of the extremes in sentiment that triggered in March for stocks were erased during the subsequent rally, which also generated a handful of breadth thrusts in major indexes and sectors.

Unfortunately, there hasn't been much follow-through. That's not encouraging. It's also not a good sign that the market environment remains unhealthy. It's still too early to tell for sure, but the best thrusts have tended to encourage even more buying interest, eventually turning the environment to a more healthy state. We still haven't seen that, and stocks have had a hard time sustaining advances when it was unhealthy.

Possibly (probably) the most important market in the world, the U.S. fixed income, continues a historic drawdown. It's exceptionally rare to see both markets struggle like they have at the same time, neither one offsetting the other's losses. Drawdowns across bond indexes are at or near 30+ year extremes, and sentiment is in the gutter right along with the returns.

If history from the past three decades is any guide, then we're at a remarkable buying opportunity across fixed income. The biggest question, of course, is whether the past 30 years mean anything at all given where we are in the economic landscape. I don't guess about macro factors, so I'll leave that part to others.

Portfolio updates

STOCKS

S&P 500 Equal-Weight (RSP) - I don't see much that makes me want to change it substantially either way. I continue to greatly favor the equal-weight version versus the more popular cap-weight version of the index to reduce the influence of the large big-cap tech stocks.

iShares Core MSCI Emerging Markets (IEMG) - The last change to the portfolio was adding some emerging markets exposure, and I'm okay with just holding this for now. There's probably a better opportunity here than in U.S. stocks in the months (years?) to come, especially in some of the more beaten-down sectors like we've covered with Brazil.

BONDS

Vanguard Total Bond (BND) - Pessimism is rampant in bonds. It has been for a while, and yet they continue to drop. There are hallmarks of forced selling in Treasuries, in particular, and one has to wonder when we'll learn who's been forced out of their positions. It seems like there should be an opportunity here but I'm just not willing yet to step in.

Schwab U.S. TIPS (SCHP) - I continue to prefer exposure to a broad fund along with an inflation-adjusted kicker.

PRECIOUS METALS

VanEck Gold Miners (GDX) - Not much to say here, as the stocks try to work higher. Breadth has improved and is showing some signs of what we normally see during structural bull markets. I'd be more inclined to add than reduce exposure here and am just looking for what looks like a good risk/reward chance to do so.

COMMODITIES

WisdomTree Enhanced Commodity Strategy (GCC) - Many commodities have performed splendidly and we maintain a 2.4% weight, below the target weight of 5%. The issue has been trying to add to positions in this market that have historically done extremely poorly when overbought.

SPECIAL SITUATIONS

KraneShares CSI China Internet (KWEB) - Chinese tech stocks failed horribly from the setup last fall, then presented what looks like another one during the March freefall. Heavyweight Tencent is back in the market buying back its stock daily, double the number of shares that it was buying in January, which itself was double what it was buying last fall. I'll likely be adding more to this position, once again with the outlook of a longer-than-usual time frame of 1+ years.

Energy Select Sector SPDR (XLE) - Energy stocks have done well, but I reduced the allocation a bit based on extended conditions. Energy stocks tend to do well in conditions like we have to I'm not seeing a good reason to make any major changes here.

Invesco S&P SmallCap Energy (PSCE) - Same as the above.

Portfolio Summary and Disclaimers

RETURN YTD: 0.1%

2021: +8.7%, 2020: +8.1%, 2019: +12.6%, 2018: +0.6%, 2017: +3.8%, 2016: +17.1%, 2015: +9.2%, 2014: +14.5%, 2013: +2.2%, 2012: +10.8%, 2011: +16.5%, 2010: +15.3%, 2009: +23.9%, 2008: +16.2%, 2007: +7.8%

Not intended as investment advice. In this account, we roughly follow what has become known as the All Weather portfolio popularized by Ray Dalio. It allocates across four broad assets, designed to hold up no matter the market environment. The goal is modest positive returns while limiting large, sustained losses. We typically use popular ETFs, with low costs. At times, we will swap out for a fund we believe has better prospects, or simply lower fees if not. At other times, we will diverge quite a bit from baseline allocations, largely depending on the indicators and studies we discuss on the site. The base allocation includes stocks (35%), bonds (35%), gold (5%%), commodities (5%) and cash/other (20%).