PortfolioEdge Update for Apr 22 - Selling some RSP, XLE, SCHP

Key points:

- Investors are showing signs of bear market behavior

- At the same time, the market is historically split between winners and losers

- I'm reducing equity exposure and raising cash

- The bond market is washed out but that's been the case for months

Commentary

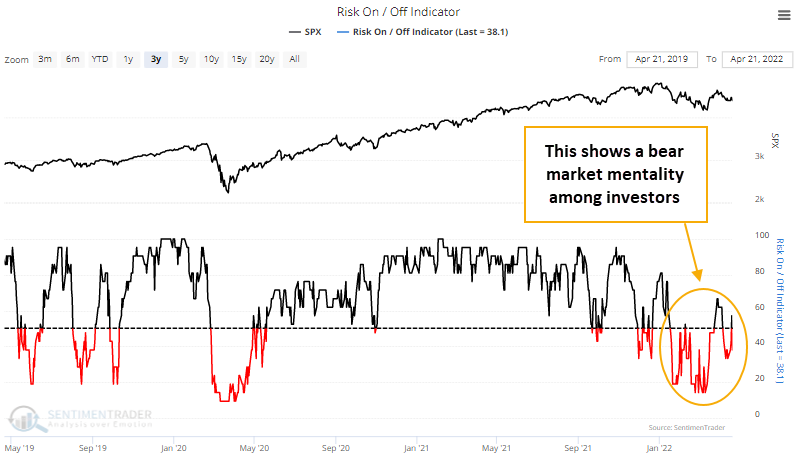

This is not a healthy market. The environmental factors I watch have failed to turn positive, and the late-March breadth thrusts haven't prompted any kind of follow-through among buyers. Our Risk Appetite and Dumb Money Confidence models have refused to flip to risk-on status.

We may not be in a bear market, but this is bear market behavior.

I am generally a contrarian investor, buying into weakness and selling into strength, typically within the context of broader market trends; a mean-reversion tendency within a trend-following discipline. It's relatively unusual for me to sell into declines. But when I'm confused or feel that there is just as much risk as reward, I sell and regroup later. It helps clean out the mental clutter.

This account is structured as a retirement account, so there are no tax implications for sales. These are not day trades and I'm not too concerned with price action over the coming days or even weeks - I have a multi-month time frame in mind whenever I make a change, with some exceptions that I note at the time.

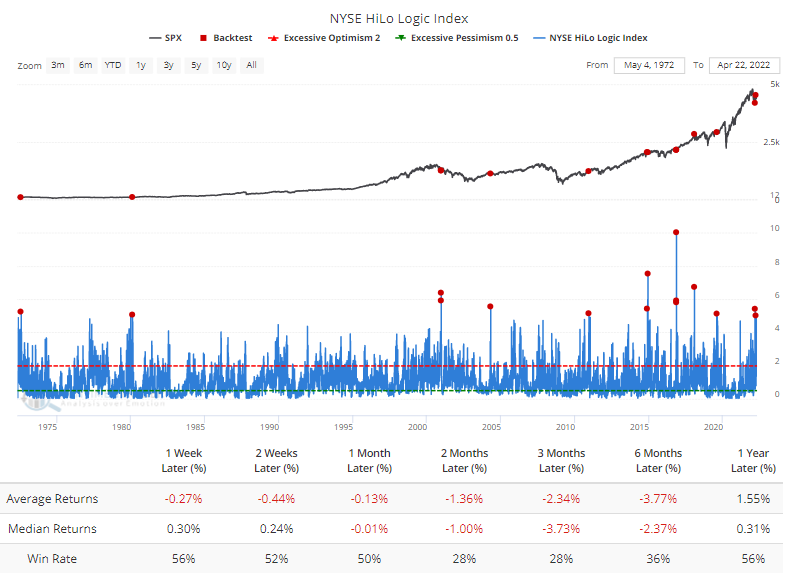

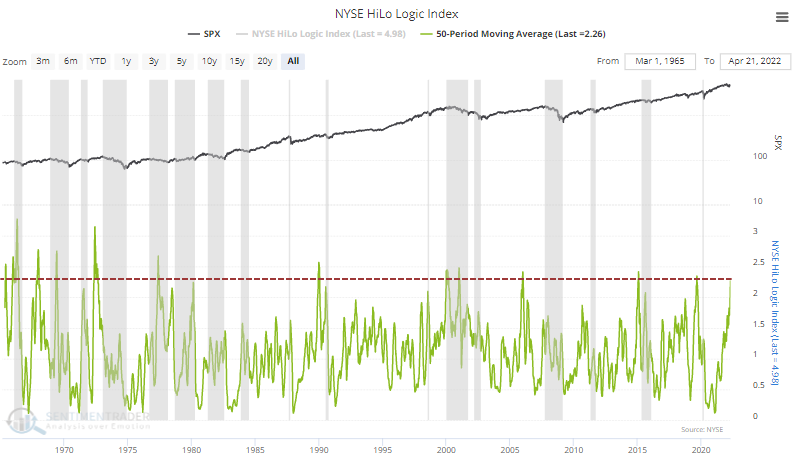

This is my biggest worry, other than the poor environment noted above - stocks are split to a historic degree. Thanks in part to bond market carnage, more than 5% of issues on the NYSE are either at a 52-week high or a 52-week low. Similar conditions had no negative impact in 2016 and only limited impact in 2019, but historically, future returns in stocks have been horrid even after lesser extremes.

It's been a persistent concern, and over the past 50 days, this has climbed to an average of 2.25% of issues. This has never not preceded a bear market (gray shading).

It's not just interest rates driving this. Even within many equity sectors, there is a heavy split between winners and losers. There is no good way to spin that.

I'd become encouraged in March after a spike high in Smart Money Confidence, followed by impressive thrusts in breadth. Those have evaporated and there does not seem to be a strong edge here. Certainly, there are signs that stocks should do just fine, but when there are many apparent cross-currents I like to boil it down to first principles. For me, that means 1) market environment and 2) risk appetite. Currently, that is unhealthy and risk-off.

The bond market panic is remarkable, and as we've noted in several research reports, the last two generations of investors haven't seen anything like this. Anything approaching this level of selling has brought in bond buyers over the past 30 years...but that was the case a couple of months ago, and yet the market continues to plunge. When a market doesn't do what it should, I prefer to let the smoke clear.

Portfolio updates

STOCKS

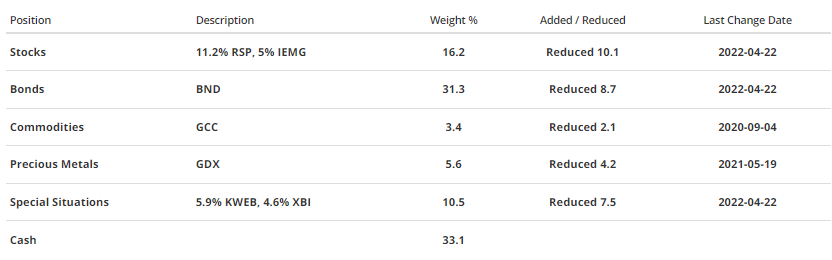

S&P 500 Equal-Weight (RSP) - I continue to favor the S&P 500 as an index for equity exposure, as well as the equal-weight version of the index. But I'm deeply concerned about investor behavior over the past several weeks and am selling down the shares I bought in January for a gain of a few percentage points. I'd rather sit in cash and wait for what appears to be a more defined risk/reward situation.

iShares Core MSCI Emerging Markets (IEMG) - I'm okay with just holding this for now. There's probably a better opportunity here than in U.S. stocks in the months (years?) to come, especially in some of the more beaten-down sectors like we've covered with Brazil.

BONDS

Vanguard Total Bond (BND) - Pessimism is rampant in bonds. It has been for a while, and yet they continue to drop. There are hallmarks of forced selling in Treasuries, in particular. It seems like there should be an opportunity here but I'm not adding to bond positions yet.

Schwab U.S. TIPS (SCHP) - Getting rid of these. The total return has been fine since the purchase almost two years ago, but I'm becoming less interested in any kind of inflation-specific bet in fixed income. I'm more likely to gravitate toward a more general bond fund if we see either a healthier environment or an all-out sell-everything panic.

PRECIOUS METALS

VanEck Gold Miners (GDX) - The breadth metrics we follow for gold miners are acting well. This is a volatile sector, but they're showing bull market behavior. More than 70% of mining stocks are holding above their 50- and 200-day moving averages, thrusts that we typically do not see in bear markets. I'm more inclined to add to this position if a compelling setup arises.

COMMODITIES

WisdomTree Enhanced Commodity Strategy (GCC) - No change here - many commodities have performed splendidly and we maintain a 2.4% weight, below the target weight of 5%. The issue has been trying to add to positions in this market that have historically done extremely poorly when overbought.

SPECIAL SITUATIONS

KraneShares CSI China Internet (KWEB) - These stocks just cannot get moving, rejected after every surge in buying interest. Obviously, not a good sign. At least none of them have (yet) fallen back to 52-week lows. The few other times more than half of them fell to new lows, then none of them did for more than a month, it indicated major bottoms over the past fifteen years. And the most important one of them all, Tencent, continues a massive stock buyback program. Unlike U.S. companies, Tencent's record is astoundingly astute. I'm not making any changes yet, but I'm looking to add more to this position, with the outlook of a longer-than-usual time frame of 1+ years.

Energy Select Sector SPDR (XLE) - After a good run of buying what had been the most-hated sector of all time, I'm getting rid of my energy stocks. I've held them longer than intended and the recent bout of massive corporate insider selling is chilling. I just don't see a big edge there any longer.

Invesco S&P SmallCap Energy (PSCE) - Same as the above.

Portfolio Summary and Disclaimers

RETURN YTD: -2.6%

2021: +8.7%, 2020: +8.1%, 2019: +12.6%, 2018: +0.6%, 2017: +3.8%, 2016: +17.1%, 2015: +9.2%, 2014: +14.5%, 2013: +2.2%, 2012: +10.8%, 2011: +16.5%, 2010: +15.3%, 2009: +23.9%, 2008: +16.2%, 2007: +7.8%

Not intended as investment advice. In this account, we roughly follow what has become known as the All Weather portfolio popularized by Ray Dalio. It allocates across four broad assets, designed to hold up no matter the market environment. The goal is modest positive returns while limiting large, sustained losses. We typically use popular ETFs, with low costs. At times, we will swap out for a fund we believe has better prospects, or simply lower fees if not. At other times, we will diverge quite a bit from baseline allocations, largely depending on the indicators and studies we discuss on the site. The base allocation includes stocks (35%), bonds (35%), gold (5%%), commodities (5%) and cash/other (20%).