Playing gold with options

Key Points

- Gold recently made another run toward all-time highs and then reversed

- Bulls expect gold to break out; bears expect gold to break down

- Options on ticker GLD allow bulls and bears a relatively low-cost and limited-risk way to express their opinion

Stalking a position in gold

Traders interested in gold have essentially three choices: a long position, a short position, or a flat position. A long position makes money if gold rises in price and loses money if it declines. A short position loses money if gold increases in price and gains if it falls. A flat position offers no profit potential but also entails no risk.

For a trader seeking to profit from gold price fluctuations, the most straightforward approach is to trade gold futures, where a short position can be entered just as easily as a long position. The potential negative to trading gold futures is the leverage involved and the potential for unlimited risk.

An alternative is to buy or sell short shares of a gold ETF, such as ticker GLD, which can be bought or sold like shares of stock. One potential holdup is the cost of GLD shares (at $188 a share, a trader must pony up $18,800 to buy 100 shares).

One other alternative is to buy call or put options on ticker GLD. This approach offers the advantages of low cost and limited risk but has unique limitations.

Everyone has an opinion on gold these days, as the yellow metal (and corresponding ETFs) have spent the last four years testing and retesting multi-year price highs without successfully breaking through to the upside.

Some traders believe that gold will eventually break through and that it will run sharply higher when it does. Others believe the multiple failures to break out to the upside will result in another sharp move to the downside. Others don't know where gold will go next and are standing aside.

Let's look at how GLD options might be used by a trader with an opinion regarding where gold is headed next.

A limited risk bullish position

Let's assume that a trader thinks that gold is due to break out to the upside in the next several months. The most straightforward approach would be to enter a long position in gold futures or to buy 100 shares of Gold Shares Trust ETF (ticker GLD). A futures contract position involves a great deal of leverage and essentially unlimited risk, while the 100 shares of GLD require a trader to pay roughly $18,800. This position's particulars and risk "curves" appear in the chart below. All charts courtesy of www.Optionsanalysis.com.

Note that the risk curves are simply a straight line. For every $1 GLD moves up or down in price, the position will gain or lose $100. A position's delta can be considered its "stock equivalent position." Unsurprisingly, a position of long 100 shares of stock has a delta of +100.

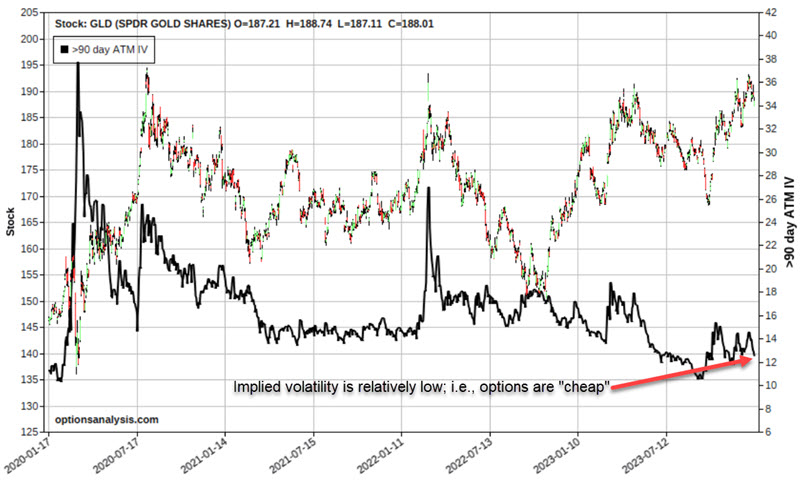

Now, let's consider a lower-cost, limited-risk position. The chart below shows a price chart for ticker GLD and the current and historical values for option implied volatility for GLD options.

To understand implied volatility, note that option price includes "time premium" (essentially the amount of premium paid by the option buyer above and beyond any intrinsic value to the option seller to induce them to sell the option). In a nutshell, high implied volatility means that there is a relatively large amount of time premium built into the options (i.e., they are "expensive"), and low implied volatility means that there is a relatively small amount of time premium built into the options (i.e., they are "cheap"). Buying options when IV is low is generally advantageous to limit the time premium you pay.

As you can see in the chart above, IV is presently near the low end of the historical range. Thus, GLD options are relatively cheap, and buying options can make sense. So, let's consider a specific call option position.

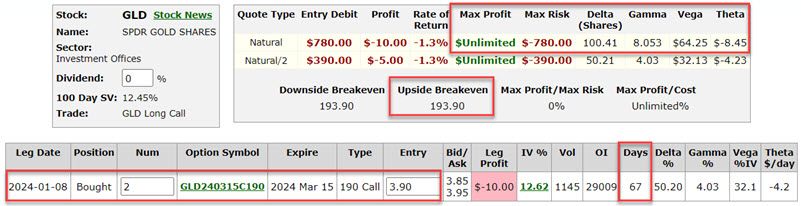

The example position below involves:

- Buying 2 Mar15 2024 GLD 190 calls @ $3.90

The chart below displays the particulars. Note that because we are buying two contracts of an option with a delta of 50.21 ("Delta" in options represents the stock equivalent position), the position delta is 100.41 (50.21 per option x 2 contracts), i.e., it will behave much like a long 100 shares of GLD position. However, note also that the delta can and will change as the price moves and time goes by.

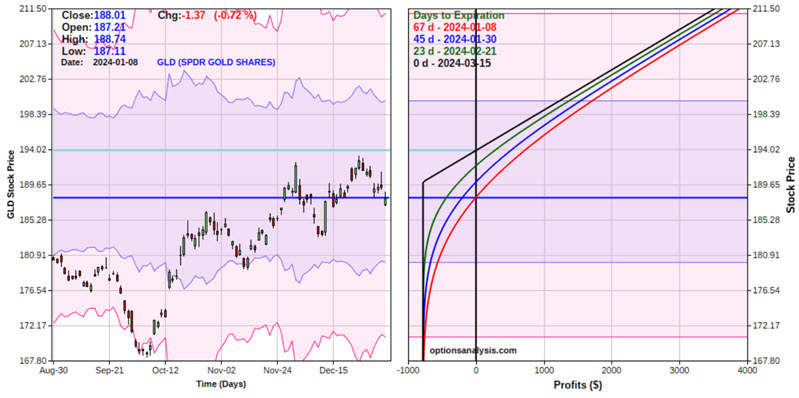

The chart below displays the risk curves for this option position. The black line represents the expected $ profit/loss at a given price for GLD shares as of option expiration on 2023-03-15. The other colored line represents the expected P/L as of a different date leading up to option expiration, with the red line representing the current date.

Things to note:

- The cost to enter - and the maximum risk - is $780 (or 4.1% as much as buying 100 shares of GLD).

- This position's breakeven price at expiration is $193.90 a share for GLD (current price = $188.01). This is calculated as the option strike price (190) plus the cost of the option ($3.90).

- There are 67 days calendar days left until expiration. If the position is held until expiration, GLD must be trading above the breakeven price to show a profit.

- The position delta at entry is 100.41, which means that, for now, it will fluctuate much like a 100-share position in GLD shares.

- The position gamma is 8.053. This means that the delta will rise or fall by this amount if GLD shares rise or fall $1 in price.

- The position Vega is $64.25. This means that the position would gain this amount in value if the GLD option implied volatility rose one full point and vice versa.

- The position Theta is -$8.45. This means the position will lose $8.45 in value due solely to time decay.

Comparing to long 100 shares of GLD

In this example, the good news about buying a call instead of GLD shares is the reduced cost and limited risk. But there are tradeoffs. The chart below displays the risk curve at expiration for the 190 GLD call option position in black and the long 100 shares of GLD position in grey.

Above roughly $200 a share, the long call position will generate a higher dollar profit. That advantage will grow as GLD continues to rise (because the option position's delta value will continue to increase due to the position's positive gamma value).

Between $180 and $200 a share, the long call position will generate either a lower dollar profit or a larger dollar loss than the long 100 shares position. A trader must be willing to accept this risk to enter the long call position.

Below $180 a share, the long 100 shares position will continue to lose another $100 for each $1 decline in GLD share price. The 190 call position can lose no more than the $790 initial premium paid.

A limited risk bearish position

Now, let's assume that a trader thinks that gold is due to break down in the next several months. At the same time, this trader is uncomfortable trading gold futures and is hesitant or unwilling to sell short 100 shares of Gold Shares Trust ETF (ticker GLD). Let's consider a limited-risk option position.

The example position below involves:

- Buying 2 Mar15 2024 GLD 190 puts @ $4.25

The chart below displays the particulars. Note that because we are buying two contracts of an option with a delta of -49.80, the position delta is -99.60, i.e., it will behave much like a short 100 shares of GLD position. However, note also that the delta can and will change as the price moves and time goes by.

The chart below displays the risk curves for this option position. The black line represents the expected $ profit/loss at a given price for GLD shares as of option expiration on 2023-03-15. The other colored line represents the expected P/L as of a different date leading up to option expiration, with the red line representing the current date.

Things to note:

- The cost to enter - and the maximum risk - is $850.

- The breakeven price at expiration for this position is $185.75 a share for GLD (current price = $188.01). This is calculated as the option strike price (190) minus the cost of the option ($4.25).

- There are 67 days calendar days left until expiration. If the position is held until expiration, GLD must be trading below the breakeven price to show a profit.

- The position delta at entry is -99.60, which means that it will fluctuate much like a short 100-share position in GLD shares.

- The position gamma is 8.077. This means that the delta will rise or fall by this amount if GLD shares rise or fall $1 in price.

- The position Vega is $32.10. This means that the position would gain this amount in value if the GLD option implied volatility rose one full point and vice versa.

- The position Theta is -$1.60. This means the position will lose $1.62 in value due solely to time decay.

What the research shows…

There is no such thing as "one best position." There are only tradeoffs. A long futures position or a long 100-shares of GLD position offers exact point-for-point profit or loss based on price movement in the underlying security. A long call or long put position can offer unlimited profit potential and limited risk. However, if the underlying security remains relatively unchanged, losses can accrue. Options also provide the trader only a limited period for the underlying security to make the hoped-for move.